Skip to main content

Skip to main content

Tax rises may be coming - are you prepared?

2020 was an unprecedented year. The world, as we know it, was plunged into a huge human crisis with the outbreak of Coronavirus (COVID-19). The virus has touched almost every aspect of our daily lives, and regrettably, a return back to normality is not within our immediate sight.

Governments and institutions across the world have faced a truly extraordinary crisis, as they have battled to contain the virus (with varying degrees of success), whilst keeping their economies afloat. The UK Government has been no stranger to this balancing act, implementing a wide range of financial support packages for individuals and small businesses, the most notable of which being the Furlough Scheme launched in March last year.

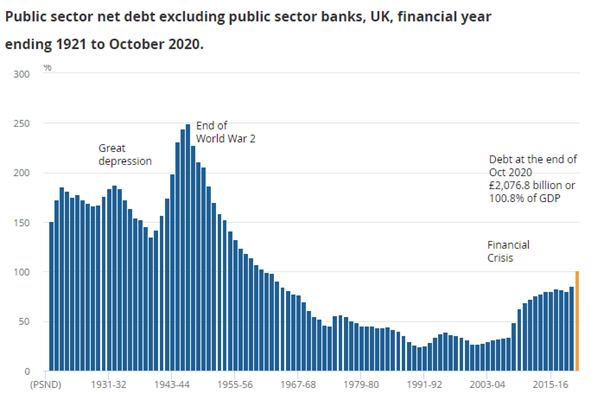

The vast wave of Government support packages has resulted in a significant increase in Government debt, with the UK’s Public Sector net borrowing increasing by £214.9 billion from April 2020 to the end of October 2020, and according to the Office for Budget Responsibility1, is forecast to rise to £372.2 billion by the end of March 2021. The monumentally large issuance of debt now means that the UK’s debt now equates to 104.7% of our GDP, a level of debt to GDP which we have not experienced since the early 1960’s (see diagram below).

How will we pay for the Covid-19 Bill?

Given the circumstances, the Chancellor, Rishi Sunak, has elected to borrow from the future to pay for today. However, the large elephant in the room remains. How will the UK pay for the COVID-19 Bill once the dust settles? Mr Sunak’s most unenviable task awaits.

As Financial Planners we keep a keen eye on what is going on in the UK, and the rest of the world, for that matter. However, we are acutely aware that delving into the granular detail can often distort the bigger picture when it comes to saving and investing. What matters most is ensuring that your personal finances are in shape to tackle any looming tax changes that the UK Government may implement further down the tracks. Part of this is to make sure you do the basics when it comes to your wealth.

So what action can you take now to protect your wealth?

Use your ISA allowance

Arguably one of the most important steps that you should undertake if you are considering investing money is using your annual ISA allowance. Every tax year individuals in the UK have a £20,000 ISA allowance that you can use, whether that’s to hold in cash in the form of a Cash ISA, a Lifetime ISA for a house purchase or retirement, or a Stocks & Shares ISA, the latter of which is the most popular amongst UK investors.

What makes an ISA a great investment vehicle from a tax perspective is that any gains, dividends or interest generated from the assets that you hold in your ISA are free from tax. But do remember, that if you do not use up your full £20,000 in any given tax year, any unused allowance does not role over into the next tax year.

Use your pension

When it comes to finding a way to maximise the allowances available to you in a tax friendly environment, there aren’t many better options than investing via a pension. Similar to the ISA, capital gains, dividends and interest are all free from tax within a pension. However, where there is a distinction between the two, is that it may be possible to contribute more to a pension each year. Current legislation permits that you can put up to the lower of your earnings, or £40,000, into a defined contribution pension each year. In a simple example that means that if you are earning £30,000 you can contribute up to that amount. But if you are earning £60,000 you can typically only contribute up to £40,000. That comes with the caveat that you might be able to contribute more than £40,000 in a tax year if you have unused allowance from the previous three tax years.

The amount that you can contribute also changes at both ends of the earnings spectrum. For example: if you are earning over £240,000 a year, your annual allowance reduces by £1 for every £2 of earnings over the threshold, down to a minimum allowance of £4,000. In contrast, if you aren’t earning anything in a tax year, you can still contribute £3,600 to a pension.

What also makes pensions a great tax efficient way to invest for your future is that the contributions that you make benefit from tax relief. Every contribution that you make to a pension, benefits from a top up by the Government equivalent to basic rate tax, meaning that a £100 contribution technically costs £80 to you and the Government tops up the remaining £20. The pension relief doesn’t stop there though. Tax relief is also obtainable to anyone who is a higher or additional rate taxpayer too. The only main difference being that instead of the top up going into your pension as an additional contribution, it is deducted from your income tax bill when you complete your end of year tax return. The result, an increase in your pension pot and a reduction in your income tax bill – a big win.

Will I lose some of the tax efficient benefits of a pension?

Overall, contributing to a pension in the current climate is a very tax efficient way to invest. However, there are murmurings that the Government may look to take away some of the tax benefits associated with investing in a pension, such as reducing the amount that you can contribute or the amount of tax relief that individuals benefit from. Even if these possible changes are merely paper talk, it’s important that you maximise the benefit from a pension in a way that is affordable to you now, in order to help you grow your pot for the future.

Use your allowance and realise gains

Another quick tax tip is to realise investment gains. Investment gains typically occur in a portfolio that is not held in an ISA or pension, where you have benefitted from growth in a given tax year. Realising a gain means selling your investments up to the value of your annual capital gains tax (CGT) allowance, which currently stands at £12,300. That can be achieved by selling a proportionate amount of your portfolio so that any gains fall below the threshold. Better still, you can sell your investments and transfer them into an ISA. The overall result being that you don’t pay any capital gains tax, you remain invested, but this time in an ISA that comes with paying no tax on growth, dividends and interest.

What also makes realising investment gains slightly more appealing is that if you choose to realise gains above the annual CGT threshold, then they are only taxed at 10% for basic rate taxpayers, and 20% for higher or additional rate taxpayers, rather than being aligned to income tax rates of 20%, 40% and 45%. The only exception to this tax rule is the sale of residential property, which is taxed at 18% and 28% on gains respectively. Although CGT rates may seem attractive, relative to income tax rates, that could be set to change with the Government potentially earmarking a tax hike to pay for the Covid-19 bill.

What might the Government do?

Capital Gains Tax (CGT) proposals

One of the major UK personal taxes that has been the subject of much speculation is CGT. It was only in July of last year that the Government requested that the Office of Tax Simplification (OTS) review its current structure and implementation of the tax.2 Whilst this request was actually deemed relatively normal, given that the Government has asked for such a report for several years now, the findings were considerably stark. The overarching conclusion reached by the OTS was that capital gains tax rates should become aligned to income tax rates, which would mean CGT rates should be increased.

With such stark differences in the rates of tax applied, it would be easy to recommend an increase in CGT rates to help settle the Covid-19 debt bill and align them more closely with income tax. However, many experts warn against such a move and estimate it will only reduce the amount of revenue received by the Government as behaviour changes.

Currently, unlike income tax, the revenue from CGT is paid in large sums but by a small number of people (265,000 people a year compared to 32 million who pay income tax). Data has shown that the majority of gains registered in recent years fall just under the annual exemption (£12,300 for 2020/21), demonstrating its voluntary nature. An increase in rates will likely distort the behaviour of taxpayers and discourage them from cashing in any gains3. They could instead only realise gains up to the annual exemption to avoid paying any tax at all or retain the investments until death, at which point the assets can be passed to beneficiaries free of any gains.

The significant difference in rates also makes capital-based remuneration much more attractive for higher earners. Higher and additional rate taxpayers can expect tax savings of 20/25% if their pay packet includes company shares through a share incentive scheme compared to a salary, as any growth is generally treated as a gain when vested. A difference in the way these shares are taxed (as suggested by the OTS) could prove costly for those in such schemes and it may be beneficial to vest any shares received this way before any changes take place.

With all of this speculation swirling, investors may wish to consider whether it makes sense to realise gains within the current 10% and 20% regime if they have strong feelings that CGT rates will rise and so want to take action now.

What might happen to pensions?

As we mentioned earlier, the tax relief earned on personal pension contributions makes a pension a very valuable investment for your retirement. However, the generosity of the current rules has made reducing tax relief an easy target for HMRC clawing back some additional tax revenue. What is more, contrary to some other taxes, a reduction in tax relief has gained some political traction with Rishi Sunak who is said be very attracted to a flat rate of income tax relief on contributions. It is rumoured that any proposed changes could see a new flat rate of 25% or 33% applied to tax relief on all contributions, irrespective of your income tax threshold, such a result would not bode well for higher or additional rate taxpayers.

A study by The Resolution Foundation4 think tank has revealed that such a cut would likely save the Government £4bn a year in tax relief. Whilst this is a lot of money to you and me, it is surprisingly only 10% of what pension tax relief costs the government each year and less than 1% of the estimated final bill of the pandemic.

Furthermore, due to the administrative burden involved and the added complexities of public sector/defined benefit pension schemes, it will be both costly and difficult for the Government to implement fairly.

Wealth tax

After almost 50 years, wealth tax continues to spark debate with Politicians and taxpayers alike. A wealth tax would be a tax on all assets held including your home and pension aimed at wealthier individuals.

In July 2020, Rishi Sunak said he believed there would never be a time for a wealth tax, however, a recent study by Ipsos Mori reveals that 75% of Britons disagree with him. This is not the first time such a tax has been debated in the UK, having surfaced in the mid-70s and several more times since.

Shortly after the announcement of a wealth tax in Argentina on 4th December 2020, the independent Wealth Tax Commission5 released a report strongly endorsing a one-off wealth tax in the UK and outlining how it could be implemented. It makes special note to reinforce this should only be a one-off tax rather than a recurring event, which could be harmful in the long term and cost considerably more, but one that has the potential to raise £260 billion over 5 years.

The Commission does not reference a particular threshold that should be implemented but offers differing outcomes based on several scenarios. It also gives detail to the definition of ‘wealth’ in this instance and includes all personal assets (including pensions, property, savings etc.) in its description for the purposes of the calculation. Such a definition aims to be as fair as possible by measuring all who are likely to be affected on a level playing field.

The report findings are overwhelming and whilst it seems there is significant public support for the tax, it isn’t clear how politically successful it would be in practice, although Governments have levied emergency windfall taxes in the past. A lower threshold than expected will have a huge impact on the support the tax receives and even then, will only go a small distance in reducing the debt incurred by the recent economic events.

What should you do now?

Tax changes are a recurring theme when a Government Budget approaches, but this year is pretty exceptional with such interest being heightened by the financial fallout from the Covid-19 pandemic. In truth, whether the Government will react to the pandemic through tax hikes at the next Budget remains unclear.

Aside from the points raised above, other speculation surrounds property taxes, changes to National Insurance Contributions for the self-employed, and the possibility of a solidarity tax to help pay for the recovery. However, what we do know as Financial Planners is that tax legislation has changed markedly over the past few decades. It is therefore imperative that you are having these discussions with your Financial Planner, because your financial plan is a continually evolving piece that can change immensely over time.

If you do not have a financial adviser or you are simply looking for further advice regarding your own personal finances in this uncertain time, we offer a free initial consultation, why not get in touch and speak to an adviser.

Please note: Information regarding taxation levels and basis of reliefs are dependent on current legislation and individual circumstances, are not guaranteed and may be subject to change.

References

- Office for National Statistics. Public sector finances, UK: November 2020.

- Office of Tax Simplification. Capital Gains Tax review, November 2020.

- Office of Tax Simplification. Capital Gains Tax review, November 2020.

- Resolution Foundation. Save it for another day: Pension tax relief and options for reform. March 2016.

- Economic and Social Research Council. Wealth Tax Commission. A wealth tax for the UK: Executive Summary.