Skip to main content

Skip to main content

Living to 100 years - are you financially prepared?

The number of individuals aged 100 or older in England and Wales has reached an all-time high.

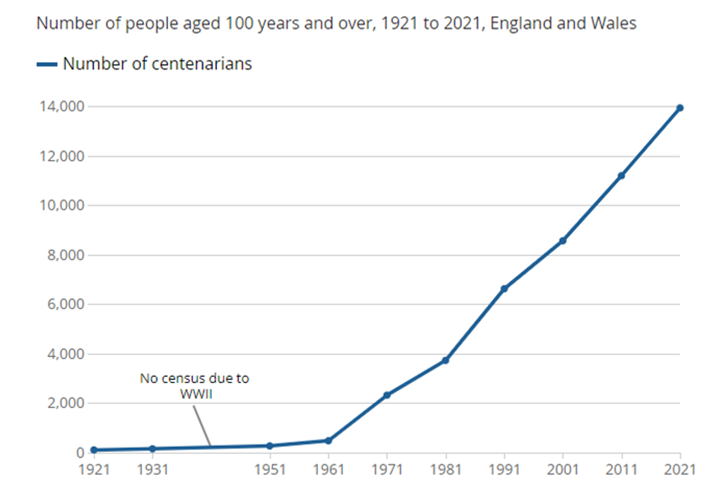

In September 2023, the Office for National Statistics (ONS) released statistics showing that over the past century, the number of centenarians living in England and Wales has increased 127-fold, shown in Figure 1 below. Figures are reported to have hit a record high of 13,924 centenarians in 2021; of this number of centenarians, 11,288 were women and 2,636 were men.

Figure 1. The number of centenarians in the population increased rapidly from the second half of the 20th century, Source: Historic Census data (1991 to 2021) from the Office for National Statistics

ONS report the UK ranking as the seventh country worldwide for highest number of centenarians and in 2021, the ONS reported that there has been a 24.5% increase from 2011 of centenarians living in England and Wales.

Although an ageing population is a major achievement of modern science and healthcare, the rise in the UK’s ageing population raises concerns around financial planning and retirement readiness.

Arrange your free initial consultation

So, how can living longer affect your own financial planning and retirement readiness?

Whilst the news that an increased number of individuals living longer in England and Wales is good news at the surface level, the challenge to this is that there is a greater need for people to acquire sufficient pension savings to fund a longer retirement.

This issue was identified by the World Economic Forum in 2019, where their findings showed that people may be expected to live longer than the pot of money they have saved for retirement by between 8 to almost 20 years on average. Han Yik, Head of Institutional Investors Industry at the World Economic Forum, stated that “The real risk people need to manage when investing in their future is the risk of outliving their retirement savings”.

Earlier this year, the below estimates were calculated by Interactive investor, using the Pensions and Lifetime Savings Association (PLSA) Retirement Living Standard:

A 65-year-old living to Age 84 would require a starting fund value of £212,000.

Whereas a 65-year-old living to Age 100 would require a starting fund value of £324,000.

These figures indicate that someone expecting to live to 100, compared to the current average life expectancy would need around a further 54% in the starting value of their retirement savings.

It is important to note that these calculations assume that the individual is entitled to the full State Pension of £10,600 p.a. and they also own their home, therefore having no rent or mortgage costs.

Whilst the UK Government provides the State Pension to qualifying individuals, which can provide a solid foundation for retirement, this needs to be supplemented to ensure a genuinely comfortable later life. Although it is technically possible to live on the state pension, additional incomes sources are crucial for a more comfortable and enjoyable retirement. And that’s before the likelihood of further costs to consider such as at-home Care or Care Home needs.

How can you be better prepared for your financial future?

Starting your financial planning as soon as possible brings many benefits including possible higher return on your investments, time to weather market volatility and ability to take more risks.

A key tool used when giving financial advice and looking ahead to your financial future is cash flow modelling. Cash flow modelling helps you to visualise what your future could look like, and then more importantly, what needs to be done before then. For example, it helps you answer questions such as:

- “How much do I need to start saving in order to retire at age 60?”,"If I was to require Care, would I be able to afford it?”, etc.

While we can make sensible assumptions, the one difficult thing to predict is one’s life expectancy. With the general population living far longer, it’s important to take a cautious approach and always overestimate, which is why we usually plan our cash flow models to age 100.

A good place to start planning your future is by understanding where you are now within your financial planning journey and what your life goals and expectations might be. A useful tool to get a basic understanding of this is our retirement calculator. From your own inputs, you will be able to forecast an estimate of the pension income you will get when you retire and receive a target retirement income to aim for based on your choices, taking into account your salary.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

The Financial Conduct Authority (FCA) does not regulate tax advice or cashflow modelling.