Skip to main content

Skip to main content

Dividing assets in a divorce

A divorce can be a challenging experience, with many life changing decisions. One of these decisions will be how you should divide your assets. We look here at what assets are, how you can protect them and the considerations that a court may take into account when they divide them.

What are assets in divorce?

Assets in divorce can be split into two categories, matrimonial and non-matrimonial. Matrimonial assets are those that you and/or your spouse acquired during the timeframe of your marriage. Assets that were acquired before your marriage or after your divorce would be categorised as non-matrimonial assets.

Matrimonial assets can include, but are not limited to, property, savings, pensions, investments, vehicles, furniture, and businesses. When you are married, the law states that these are owned jointly with no dependence on who funded the purchase. For example, if you have regularly contributed to a pension during your marriage, your husband or wife is entitled to a share in it. It is worth noting that debt can also be considered matrimonial and therefore will be split between the two parties in the financial settlement.

Formalised with a financial settlement, the matrimonial and non-matrimonial assets will be split upon divorce, and this must be fair and reasonable for both parties. By law, all assets – jointly and solely owned - must be declared before the divorce proceeding can commence.

Matrimonial assets will not necessarily be split in half between the two people involved. Instead, it will depend on the personal and financial situation of both individuals. This could entail the court ruling one person to give a third of their pension pot to the other to ensure they can remain financially stable.

Non-matrimonial assets are more difficult to divide and are sometimes asked to be excluded entirely from the financial settlement.

Specialist, professional advisers can be key in helping clients review their situation objectively as well as helping navigate what may be uncertain territory.

How to protect your assets during divorce

If we begin by looking at the family home, protecting this asset is dependent on how the ownership is written. If it is written in one name, the other can register their interest in the house to ensure it cannot be sold or re-mortgaged without notifying the other. If the property is written in both names under ‘Joint tenants’, it might be of interest to change this to ‘Tenants in common’. Under ‘Joint tenants’, if one party were to pass away, their share of the property will automatically be placed into the surviving party’s name.

If you are in the process of divorce, you may want to consider changing the ownership to ‘Tenants in common’ as your share in the house is carved out and you are able to name beneficiaries to receive your portion of the asset upon your death and for it not to pass to your ex-partner.

For your joint bank accounts or loans, it is important to contact the bank or building society to inform them of your separation, especially if the situation is sensitive or did not end well. You can ask the account provider to change the way your account is set up so that you both have to agree when each party wants to withdraw money from it. This could be a useful interim agreement while the divorce is going through the court.

How are assets divided in divorce?

The court will decide who gets what in a divorce by referring to the Section 25 Factors. This relates to Section 25 of the Matrimonial Causes Act 1973 which outlines a number of considerations the court has to consider when looking at the circumstances of the case.

What are the considerations?

Welfare of any children

The starting point for the court is to consider the needs of any dependent children and they must be the first consideration as the child’s needs should always come first.

Financial needs of each party

The section 25 factors are not ranked, however, need will always outweigh all other considerations. The court will look to ensure viable accommodation for the children and custodial parent. In some cases, this will use all the declared matrimonial assets which will ultimately leave no available assets to the non-custodial parent. If there are assets left after this, the next requirement of the court is to accommodate the non-custodial parent.

Respective incomes and outgoings are reviewed when the court considers financial needs. This can require detailed budget analysis to be undertaken for the court to assess this. Engaging a financial adviser early as part of this process is key.

Equally, if one or both of the parties have remarried or cohabit, the court will assess the new spouse/partners situation as this can majorly impact the outcome of the decision when the court rules the split of assets on divorce.

Income and property

As mentioned above, income for each party plays a crucial role for divorce cases. Income considers salary, past bonuses, benefits in kind, and the potential for future income.

The definition of property when looking at assets in divorces is wide as it covers savings, life policies, investments, trusts, pensions, annuities, shares, matrimonial home, cars, rental properties, holidays homes and business interests as well as any addition asset that could be valued. The court also has the ability to include any property that is likely to be received in the foreseeable future, however, when it comes to inheritance, this is usually not taken into consideration when splitting assets in divorce.

The value of a business is considered an asset upon divorce, especially if it has built up value over the same time as the marriage length. The business would need to have an in-depth valuation but it is highly uncommon for a court to order a business to be sold or for the other party involved in the divorce to be given it, or a share of it, as an asset.

When we look at pensions being divided upon divorce, there are a number of technicalities around this asset. If the court deems a divorcee to have insufficient funds, they can issue an order to share or offset the pensions they have built up over their lives. A pension sharing order will entail a percentage of the fund to be either transferred away to a new scheme in the receiving parties name or for them to become a named member on the existing scheme with a portion of benefits allocated to them with their spouse’s benefits being reduced proportionately. Which divorce sharing option is chosen will be dependent on the scheme rules.

If a pension is ‘offset’ it is essentially a trade for another asset. For example, if one party wants a bigger share of the family house, the court could grant this and give the other divorcee a share of the others pensions to compensate their loss on the property value.

Standard of living

The ‘Standard of Living’ factor is usually only used when there is a substantial amount of assets involved. If there is surplus left over to divide once each party’s need has been handled, standard of living will be considered. In many cases, replicating the same standard of living as both parties had before divorce is not possible due to needing an additional property, and if there are children under 18 involved, the custodial parents living arrangements will come first. However, the court will look to meet the divorcees’ living standards as fairly as possible with the remaining matrimonial assets.

Length of marriage

The age of the separated spouses and the length of marriage can play a big factor in the court rulings. If the individuals involved are young and financially independent, the court will try to ensure they can have a ‘clean break’ from one another. The younger the individuals are, the more mortgage capacity they have, which can be vital when considering the sale of the joint home.

On the other hand, the longer the marriage has been, typically, the greater financial dependence there is on one another. If they have had children, one party involved may have taken longer leave from their career to raise the child in the early years which can result in a loss of earnings and loss of career development time. This would leave them at a disadvantage financially now. This could mean the party at a disadvantage will be entitled to greater assets to make up the shortfall.

How we can help

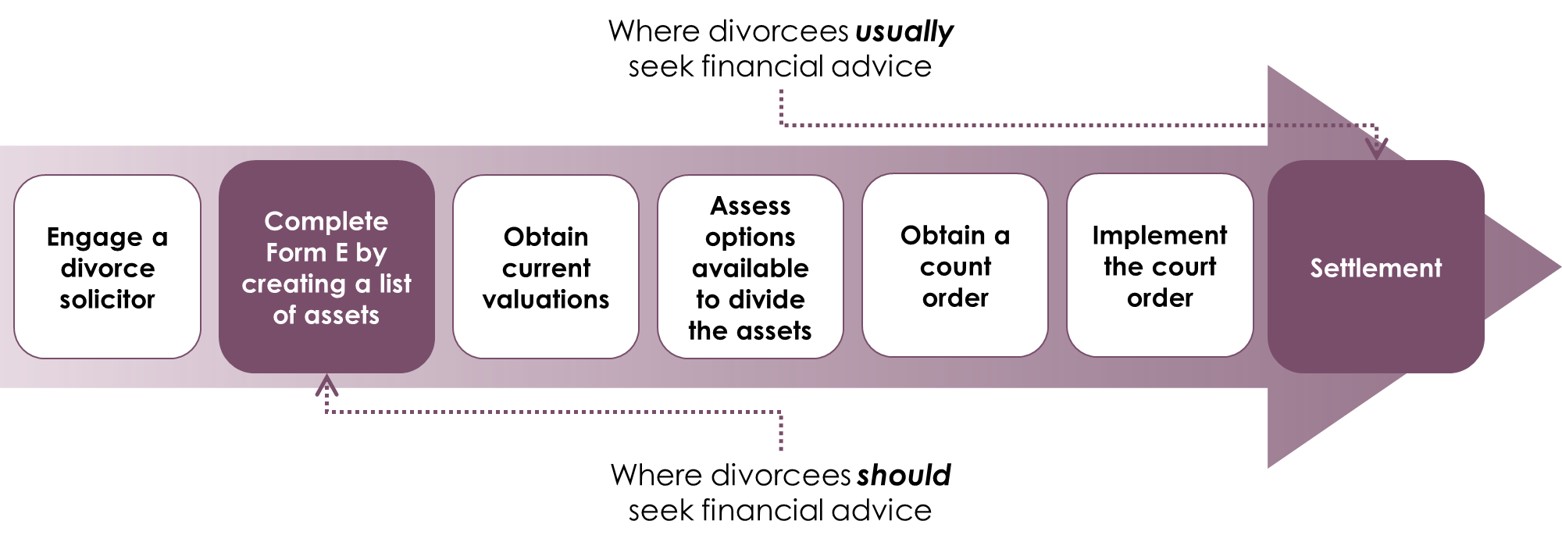

The diagram below shows the typical journey clients go through from implementing divorce proceedings, through to settlement and a division of assets:

In our expert opinion, far better outcomes are achieved when appointing a financial adviser much sooner in the process. Advice can help to understand tax implications, planning opportunities and most importantly establish how much capital and income you need to live the lifestyle you wish to live.

A divorce can invoke some of the most important financial decisions of your life. It would make sense to engage a financial adviser who has experience in this field earlier in the process, as critical information can be provided to help you achieve a fair financial settlement and a better financial future.

Understanding the legal principles, process, and the common mistakes of designing and agreeing a financial settlement is essential.

Our experience in this field is extensive and has proven very valuable to our clients. If you would like any help in this area please get in touch to arrange a free initial consultation.