Skip to main content

Skip to main content

Financial planning on divorce

.png)

The splitting of marital assets can throw your financial plans and investment arrangements into disarray and, alongside bereavement, is probably one of those times when help from a reputable and certified firm of financial advisers is most needed.

Reaching a financial divorce settlement is often a complicated and drawn-out process which requires you and your estranged spouse or partner to gather information about all of your marital assets and a judge to sign off an agreed split of these.

Here is some helpful guidance and tips to support you through what is often an emotional, and sometimes acrimonious, process.

Sarah Nesbitt, Adviser, shares tips to guide you through financial planning in divorce.

How long does the divorce process take?

On average, the divorce process in England and Wales takes between four to six months. However, there are a number of factors that can impact on the length of a divorce including lack of cooperation by one party, complicated financial matters and/or child arrangements along with delays at divorce centres and family courts.

We offer guidance about financial matters here and explain how advice can help with this part of the process.

Get organised and fully disclose

It can be difficult to organise and gain a firm grasp of your finances if you have not been directly responsible for them during your marriage.

As part of the divorce proceedings you will be required to complete a detailed financial statement (called a Form E) and you should treat this as an opportunity to identify what your financial assets actually are, where they are kept and whether they are still suitable.

Although this can be a complicated process, particularly for high net worth individuals, it is vital that you make full disclosure of all financial assets and income during divorce negotiations. Failure to do so has serious legal consequences and can result in significant, future litigation costs.

In some cases, failure to disclose may be a deliberate, if ill conceived, tactic by one party to keep certain assets outside of a divorce settlement. However, non-disclosure can also arise purely by mistake.

For example, a pension provider’s failure to provide annual statements might result in a particular pension asset accrued during a previous period of employment being omitted from disclosure. This is particularly important for women due to the gender pension gap.

Being organised and methodically cross-referencing pension assets against particular periods of employment will avoid the consequences of such unintended errors of omission.

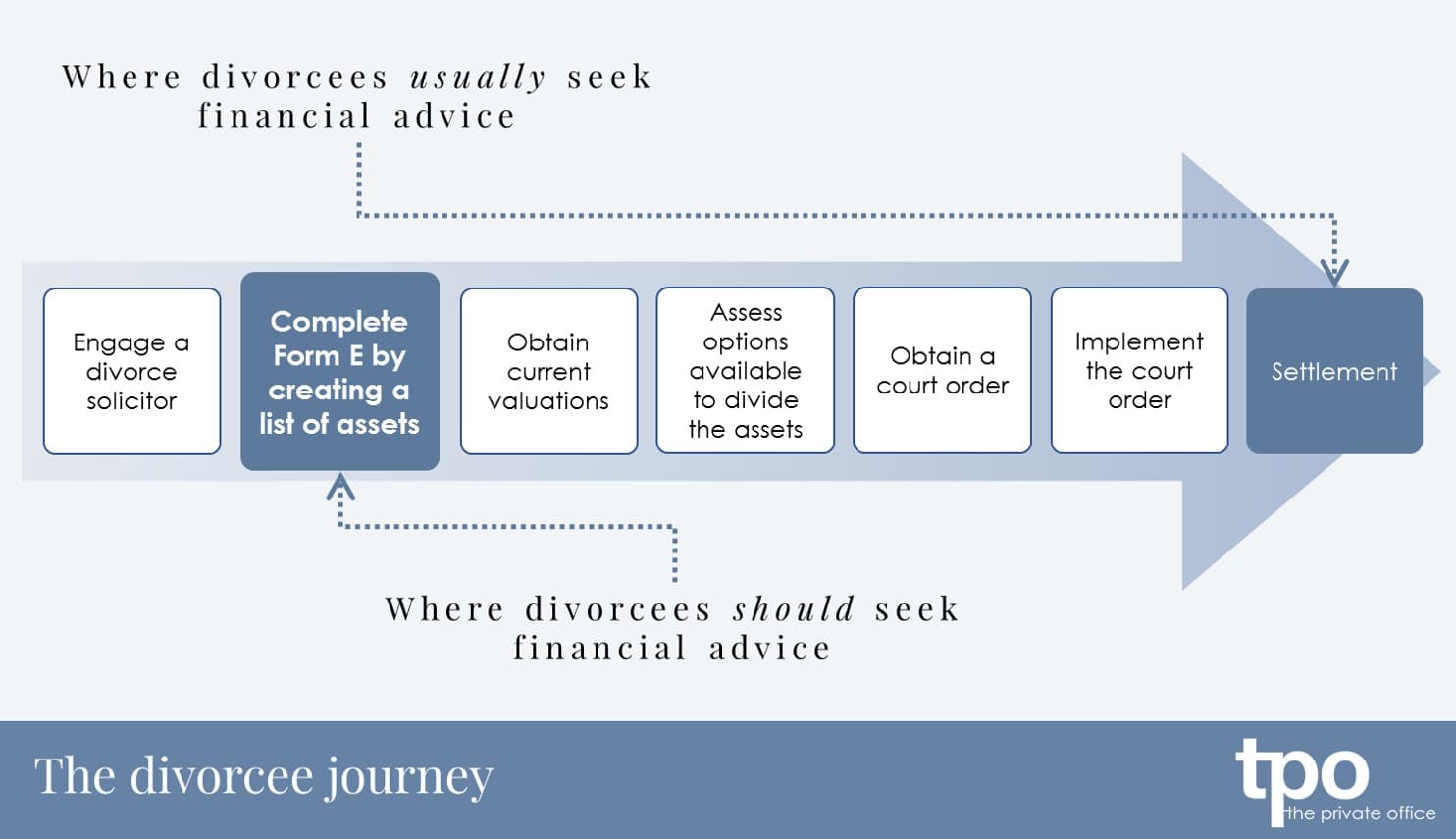

A typical client journey

The diagram below demonstrates a typical client journey.

As you can see, this often results in a financial adviser being engaged once a settlement has been agreed at which point it can be too late to carry out some of the crucial planning needed to avoid both of you paying unnecessary taxes or providing a longer-lasting maintenance order.

Provided both parties are amenable, engaging the services of a financial adviser at the start of the process can help ensure that any tax planning opportunities available to married couples prior to divorce are used.

This is particularly important for assets that are subject to a potential Capital Gains Tax (CGT) liability when you sell them.

For example, it is possible to benefit from the inter spouse CGT exemption provided any transfer of assets is conducted prior to the end of the tax year in which a married couple separates.

Jointly achieving tax efficiency within your financial affairs prior to reaching a divorce settlement is likely to increase the value of assets available to you both.

What we can do to help afterwards?

During your marriage, you will have likely formed joint decisions on what your future, including retirement, would look like.

After a divorce, you will probably no longer have the same attitude towards investment risk, the same capacity for loss, or you may not be able to maintain the same lifestyle. Moving to a single income is a major life change; without a partner's salary to fall back on, making sure your mortgage and bills are covered if you're ever unable to work is essential. Income protection insurance acts as a vital safety net, giving you peace of mind that you can still support yourself and your family if you get ill or injured.

Reflecting upon and reviewing your lifestyle and financial objectives is an important step post-divorce.

The help of a financial adviser is crucial at this point but it is important to consider your lifestyle objectives and the level of future expenditure that will be required to achieve your aspirations before making any investment decisions.

The use of lifetime cash flow modelling with your adviser will be vital in establishing whether your aspirations are realistic and will inform subsequent investment decisions.

Although there may be a temptation to get on with the rest of your life and make such decisions as soon as possible it is important not to rush financial decisions that may impact your lifestyle long into the future.

During the period of reflection following divorce it is invariably prudent to hold assets in cash until you have had time to formulate a plan for the future.

You will need to ensure that any lump sum awards are managed properly and in a manner that is aligned to your personal objectives, your attitude towards investment risk and your ability to absorb any losses.

Sometimes, cash savings are the right place until you have clarity and certainty after you have considered your options.

We can help with a range of services through this difficult time and ensure you get a fair outcome. For help on this matter download our guide or please get in touch to arrange a consultation with an adviser.