Skip to main content

Skip to main content

Planning for the costs of a private education

The introduction of VAT on private school fees in January 2025 has marked a significant turning point for families and private schools alike. Already grappling with inflation and rising living costs, parents now face an even steeper financial hurdle to provide their children with an independent education. Schools themselves are also under pressure, contending with squeezed budgets and declining enrolments.

Arrange your free initial consultation

Since the start of the year, more than 32,000 pupils have left private education in the UK, many moving into the state sector. In the same period, at least 21 private schools have closed their doors permanently due to reduced demand and increasing running costs, this in addition to those who closed pre-empting the increase in taxes, both VAT and employers National Insurance.

Despite some of the political controversy surrounding the role of fee-paying schools, the fact remains that the parents of over 620,000 children choose an independent school.

Many middle-class families spend decades planning in the cost of a private education to their finances, but despite the perception of some, it remains the case that for many, affording a private education is the result of tough decisions and compromises, often made years before a child ever sets foot in a classroom.

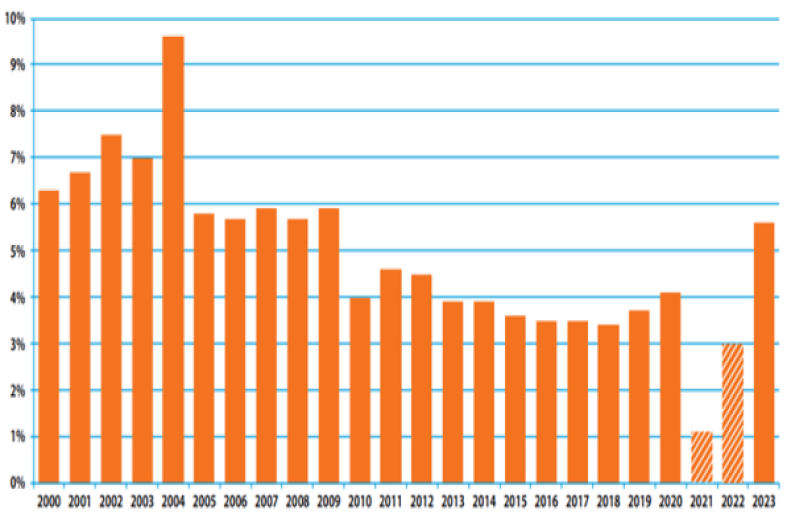

With the cost of living in the UK remaining elevated, many parents will find themselves increasingly stretched in covering Private School fees, which have displayed an average increase of 7.1% from 2024 and some reports suggest this has doubled in 2025.

Figure 1 - Fee increases since 2000 (like-for-like)*

*Source: ONS, ISC Census, 2023

With school fees in England averaging £18,036 a year for day fees, or £42,300 for boarders, this is the highest level on record. Looking back to 2013, the average annual cost of sending a child to a Private School with boarding was £27,600. There is also the implicit sums to be paid beyond the headline fees. The cost of lunches across the school year, musical lessons and overseas trips can often mean that real cost is actually far higher. These are averages and generally junior schools cost much less than senior schools; so many parents face a stark choice at age 11 or 13 when costs can increase significantly.

This, coupled with the added strain of paying such fees from income that has often already been taxed at 40 or 45%, means that many who have previously worked hard to privately educate their children may be reconsidering the affordability of doing so. With many families often having more than one child in education at once, this only serves to add to the pressure on the balance sheet of the Bank of Mum and Dad, or Grandma and Grandad.

Unfortunately, school fees cannot be offset against a tax bill, however there may be some measures that can be taken through careful planning and structuring that can help to ease the burden.

Many could be missing a trick with some of the options available for reducing the all-in cost on parents or grandparents to giving their children or grandchildren an independent education:

Paying fees upfront

Perhaps the simplest option, but with the most significant initial cost. Although less suitable for those concerned with shorter-term affordability, those with sufficient liquid wealth who are willing to take a longer-term view may benefit from paying the cost of their child’s education as a one-off lump sum.

As detailed earlier, private school fees can inflate significantly over the course of an education so there may be merit in locking in a lower cost by paying everything at the outlay. This is something that is offered by many schools.

Some schools will also offer investment schemes, wherein parents or grandparents pay a lump sum in advance which is then invested by the school into low-risk investments. As private schools have charitable status, the returns on the investment will be tax-free. If you were to make the same investments yourself, you could have to pay tax on the growth.

Before considering either of these options you should take advice, paying in advance is in effect making a loan to a business, often a small one and some institutions that have closed their doors offered such options.

Family Investment Companies

Sometimes considered as an alternative to trusts, for those with larger amounts of investable wealth, properly structured they can be excellent planning tools for a family.

Like adults, all children have a personal allowance of £12,570 which can be earned tax free. Similarly, they will also have a dividend allowance of £500 for the 2025/26 tax year.

Given that many school-age children are unlikely to have earnings using up the full extent of their allowances, allocating non-voting shares to children so that these allowances can be utilised can be an effective way to pay fees tax-efficiently, and make use of assets that are already generating capital growth or income for the company.

This can be particularly effective where more than one child is attending a fee-paying school as each child will have their own allowances.

An important point to note is that this option only works where the shares in the company are gifted by grandparents rather than parents. This distinction matters as parents will be taxed on their minor children’s income where they have gifted shares to their children.

The parental rule applies to income and not gains, so in some circumstances funds settled by parents could use a child’s capital gains exemption and then pay the lower rate of CGT, currently 18% for gains in the basic rate tax band, up to £37,700

Family Trust Options

Trusts are separate legal entities, managed and controlled by trustees for the benefit of the trust’s beneficiaries. Like with companies, beneficiaries of a trust will be taxed on any income in their personal name. Therefore, a grandparent settling funds into a trust structure can be a useful way of reducing an inheritance tax liability, whilst retaining control and paying fees tax-efficiently. If a trust is set up by parents then tax falls back on the parents, so this route is only effective for grandparents, or where funds are earmarked for later in life, when the beneficiaries are adult.

Offshore Bonds

For those already holding, or considering the set-up of an offshore bond, there are also planning options:

Bonds are normally split into multiple policy “segments”, and a grandparent can gift segments to the child who encashes it to pay for school fees in a given year or term.

The policy segments can be assigned to children when they reach school age via a Bare Trust. As a result (providing that the grandparents have invested wisely and reviewed their investment on a regular basis) the tax on the gain would, in theory, be payable by the children. However, if within their personal tax allowances, it will be tax-free.

How we can help

As with most complex areas of planning there is a balance to be struck between tax-efficiency, control and flexibility. Whilst the savings can be significant if things are structured correctly, the margin for error is high and can leave you in a worse position than at the outset if the appropriate steps are not taken. There are a number of nuances above that are detailed in this article and it is therefore important to seek professional advice in exploring your options to ensure that you do not fall foul of HMRC rules.

Why not contact us today to speak to one of our experts for a free initial consultation?

Arrange your free initial consultation

The information contained within this article is for guidance only and does not constitute advice which should be sought before taking any action or inaction. Investment returns are not guaranteed and you may get less than you originally invested.

The Financial Conduct Authority (FCA) does not regulate Trusts.