Skip to main content

Skip to main content

Don't let the pandemic cost you 20% of your pension

The current global pandemic has barely even started in terms of the effect it might have on the economy and ultimately the pounds in our pockets. As more people worry about money it’s likely that reducing or stopping their pension contributions may be an option to ensure they survive financially.

In light of recent events, we are currently offering all those with £100,000 or more in savings, investments or pensions, the opportunity for a retirement review worth up to £500. Do you know when you can afford to retire or if you can afford to take a pause in the contributions you are making into your pension? Contact us for more details.

Reasons that you might want to pause contributions

Affordability due to changes in circumstance

In times of financial difficulty and uncertainty we all need to look at our budgeting and monthly expenditure. The need to build a fund for retirement doesn’t change because of Coronavirus, but our priorities for monthly spending might, particularly if we lack a contingency fund or have lost earnings.

Concerns about markets

A diversified portfolio shouldn’t have fallen as much as the individual stock markets, but the reality is that your portfolio will have likely fallen in value already.

And although that might make savers reluctant or worried about investing more into their pensions, in fact, buying when markets have fallen is likely a sensible thing to do because you are now buying these investments at a cheaper cost.

Drip feeding into the market during times of volatility (pound cost averaging) is a sensible long-term strategy.

Knowing what impact these changes will have is imperative

If you stop contributions without a plan for however long, you could be hit with a nasty surprise when it’s too late to do anything about it.

The good news is that for those who have no choice but to pull back on contributions in the short term, the damage caused to their pension pot may not impact their future too heavily. But stop for too long and the impact to the value of the pension pot alone could be stark.

For example, take a saver earning £60,000 per year who pays 5% into their pension with a matched contribution from their employer – if they stopped contributing to their pension now and either can’t or don’t reinstate those contributions for 10 years, they could have £93,874 LESS in their pension pot than if they had continued contributing at the same level a 19.87% difference.

That could mean your pension money runs out seven years earlier. Compare that to stopping for a shorter period of two years and the figure drops to £20,627 less, a 4.37% difference than if contributions had not stopped at all.

Stopping for a short period of time, to weather the storm and provide comfort, may not have a huge impact, BUT IT WILL HAVE SOME IMPACT.

Stopping contributions for a long time however, could have disastrous consequences, leaving years of lost growth and therefore a lower income in retirement. Not forgetting the loss of employer contributions and tax relief, which is in effect free money for your retirement.

To put that into context, taking our example above, someone earning £60,000 and paying 5% into their pension with a matched contribution from their employer would see £6,000 added to their pension per year – but the employee will only see a deduction of £2,400 per annum from their pay. The £6,000 contribution is made up of;

- £2,400 personal contribution – deducted from pay

- £600 immediate tax relief added

- £3,000 employer contribution

In addition, as a higher rate taxpayer, with at least £3,000 in the higher rate tax band, a further £600 can be knocked off your tax bill!

So for a pension contribution of £6,000 p.a. – in this example it will cost a higher-rate taxpayer just £1,800.

What is the key to planning your retirement?

Cash flow forecasting is a tool that helps you understand how on track you are or not you can work on what you need to do to achieve the retirement you want.

Think about what a good retirement might look like. Some people just focus on what they need in retirement. Think about what you want to do as well – having the retirement you want is very different from the retirement you need.

Cashflow forecasting - or planning ahead - will allow you to start with the end in mind and then work out whether the retirement you want is achievable. It will create a personal plan around which you can make sensible decisions.

- If you are ahead of the curve you might have a happy set of issues to deal with (better retirement, ability to spend more, retire earlier, or take less risk with your investments)

- If you are behind, a less happy set of issues to deal with (work longer, save more, spend less, take more risk),

We’re always told that we need to save more for our retirement so it is a huge concern that the current pandemic might derail many of our plans, without us even realising.

But, with an honest conversation and the use of our forecasting software, we can understand and figure out what your goal is and from there, what you need to do to achieve it. As the saying goes, ‘a goal without a plan is just a wish’.

The key is understanding how on track you are to achieve the things that you might want to do in retirement.

Case study example of cash flow forecasting

To help show the benefits of cash flow forecasting we have provided a case study example for you to read though. If you are interested in learning more about this, speak to a financial adviser who can help you with your individual circumstances.

Assumptions

*All figures have been inflation adjusted (assumed inflation at 2.5%) which means that these are all in real money terms. Investment return on pension of 5% per annum (2.5% above inflation, net of all fees).

Life expectancy:

- Male age 40 = 85 years is average life expectancy. 1 in 4 chance of living to 94 and a 5.7% chance of living to 100.

- Female aged 40 = 87 years is average life expectancy, 1 in 4 chance of living to 96 and a 8.8% chance of living to 100.

Circumstances

| Gender | Male |

| Age now | 40 years old |

| Salary | £60,000 per annum in line with inflation each year |

| Pension value now | £150,000 |

| Monthly contributions normally | 5% of salary – matched by employer: £3,000 Gross Employer and £3,000 Gross Employee at outset, increasing in line with salary increments. |

| Normal retirement age | 65 |

| Annual spend from retirement | £30,000 net per annum |

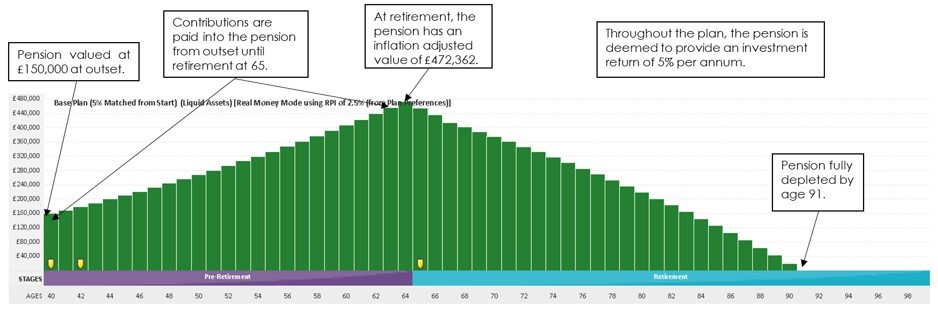

Example 1 Pension contributions unchanged – the ‘Pre Corona scenario’

Pension value at retirement: £472,362 – inflation adjusted

Pension funds run at age: 91

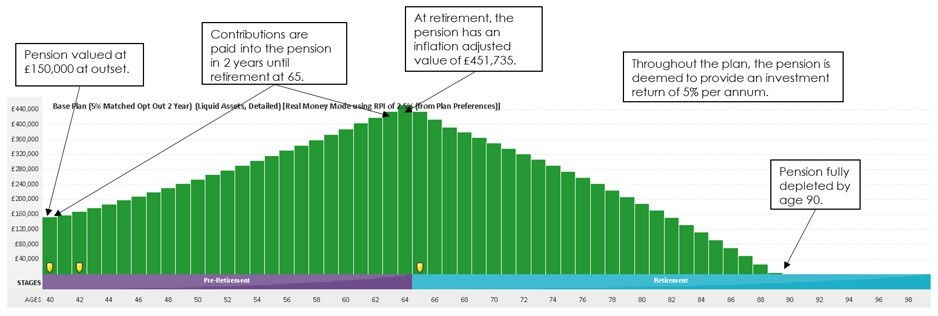

Example 2 Break in contributions for 2 years – A ‘mini Corona virus break’

Pension value at retirement: £451,735 – inflation adjusted

Pension funds run at age: 90

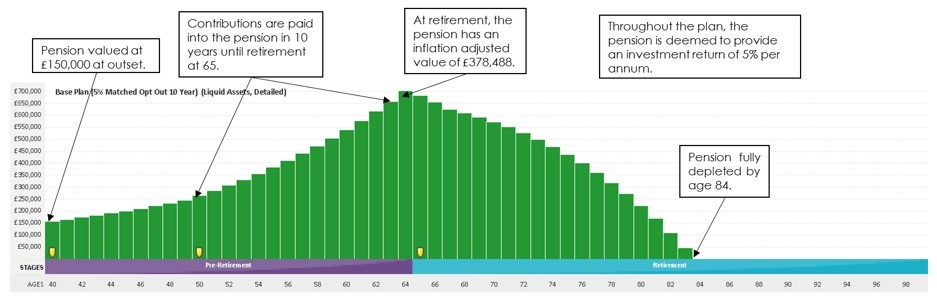

Example 3 - Break in contributions for 10 years – ‘A major Corona virus payment shock’

Pension value at retirement: £378,488 – inflation adjusted

Pension funds run at age: 84

If you feel you might value from speaking to us about your retirement plan, get in touch and speak to an adviser

Please Note: The value of investments can fall as well as rise. You may not get back what you invest. The Financial Conduct Authority (FCA) do not regulate cash flow planning.