Skip to main content

Skip to main content

Are lifestyle funds in control of your retirement?

With the challenging economic conditions we are experiencing, lifestyle pension funds have been a widely discussed topic focusing on whether they remain fit for purpose for those approaching retirement. You may be asking, ‘what is a lifestyle fund?’. If you’ve ever paid into a workplace pension or selected a ‘default’ retirement fund, you may be invested in one.

Whether you are still saving, approaching retirement, or have already retired, understanding how your pension is invested is essential when planning for a comfortable retirement. So, let’s take a look under the bonnet of lifestyle funds to see how they work and touch on some of the key factors to consider.

What is a lifestyle fund?

Lifestyle investment funds are designed to ‘lock in’ the growth that has built up within your pension pot as you get closer to retirement. This is achieved by slowly transitioning from equities, which provide long-term growth coupled with higher levels of volatility, into more defensive assets such as cash and UK Government Bonds. This ‘switch’ usually takes place over a number of years leading up to your pre-determined retirement date and as such, these funds are commonly referred to as ‘Target Date Funds’.

On the surface, lifestyling appears to be a strategy that would suit most investors by maximising growth in the early years and preserving capital as you approach retirement. However, there are a few different types of lifestyling funds that can result in very different outcomes. The main lifestyle strategies include:

- Annuity: This strategy assumes that you will purchase an annuity at retirement and, therefore, preservation of capital is most important. This fund will likely transition into cash to prevent any impact from market crashes, and Government Bonds, where their value is negatively correlated to annuity rates (we will touch more on this later).

- Drawdown: This strategy assumes that you will remain invested and begin drawing an income from your pension, most likely through flexi-access drawdown. This type of fund will remain invested, but in lower risk assets to reduce the volatility within the fund while retaining the purchasing power against inflation over the longer term.

- Tax Free Cash: This strategy can be used in conjunction with either of the above two options and assumes that you will take a tax-free lump sum from your pension at your retirement date. It is likely that this type of fund will transition part of the fund (25%) into cash to reduce the impact of any market falls on the lump sum you plan to withdraw.

As you can see, although the different strategies work in similar ways, the outcome of each will be very different and could potentially leave you worse off if you are not in a fund that is in line with your plans for retirement.

Is a Lifestyle fund suitable for me?

In our eyes, every investor is unique so it is impossible to say whether a lifestyling strategy is suitable before understanding what you are looking to achieve in retirement. As with all investments, there are both benefits and drawbacks to be considered.

For a large proportion of savers, pensions are set up and forgotten about until retirement and, therefore, there is a substantial benefit of having an automated strategy which switches into less volatile investments as you approach retirement. The potential issue with the automated approach is that the decisions of when you planned to retire, and how you would access your pension would have been made years (and potentially decades) ago, so may not be in line with your current plans and could result in your fund ‘de-risking’ too soon or remaining invested in more adventurous assets for too long.

The implications of ‘de-risking’ your pension too soon can harm your chances of enjoying a comfortable retirement. A report from AJ Bell showed that by moving a pension into a lower risk investment too soon could reduce a £100,000 pot by £12,000 – if the fund grew at 3% rather than 5% over a 5-year period.

Another consideration is that lifestyling was initially introduced during a time when the majority of pension savers were ‘forced’ to purchase an annuity at retirement. Following Pension Freedoms in 2015, the number of retirees opting for an annuity has reduced to around one in ten, showing that the vast majority of retirees are now opting for a drawdown strategy. However, research has suggested that the majority of lifestyle funds are still geared towards annuities, highlighting a potential mismatch between the objectives of these funds, and the goals of the savers who are invested in them.

It is important to ensure your pension investments are in line with your plans for retirement, speaking to an independent financial adviser can help with this.

Why has the value of my pension fallen, just as I am about to retire?

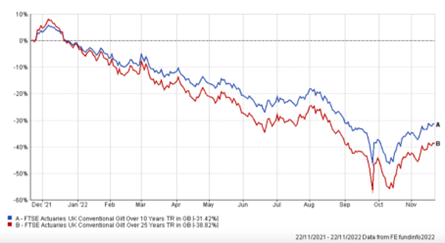

One of the primary reasons for the falls in value, comes down to the objective of the lifestyle fund that you are invested in. Over the last 12 months, some of the heaviest falls in value have been experienced by those invested using the annuity lifestyle strategy, where the funds have transitioned into government bonds (Gilts) in preparation for an annuity purchase. This is because, as the price of Gilts fall, the available annuity rates will increase, therefore maintaining the value of the income that the retiree can purchase.

To provide some background, the level of income that you can purchase through an annuity (the annuity rate) is closely linked with the yields (interest) provided by long-term Gilts. As the yields of Gilts increase, so do annuity rates. This is because pension providers use Gilts to secure the income needed to match their long-term liabilities (the annuity payments to pensioners), and the more they can earn from Gilts, the more they can pay their pensioners.

The price and yield of Gilts move inversely to one another, so an increase in the yield of a Gilt, will result in a fall in its value. During periods when interest rates increase, as we are experiencing now, the price of Gilts tends to fall (as illustrated in the chart below) which results in an increase to annuity rates. This year alone, we have seen annuity rates increase by 44%.

An investor who intended on buying an annuity, will likely be able to purchase a similar level of income now, compared to the start of the year, however, an investor who did not intend on purchasing an annuity may now be wondering how they can recoup the losses that have been experienced, just as they look to begin drawing an income.

As you approach retirement, it is essential to understand how your pension is invested and whether it is invested in line with your own plans. Lifestyle pension funds can provide some excellent outcomes for those approaching retirement, but if mismatched with your objectives, can have the opposite effect.

If you’d like to understand how your pension is invested and whether this is in line with your ambitions for retirement, please get in touch with our financial planners, to arrange a free consultation.

Arrange a free initial consultation

Note: a pension is a type of investment, the value of these investments can go down as well as up - you may not get back what you originally invested.