Skip to main content

Skip to main content

Is cash still king?

The political turmoil, both home and away, over the last few years has reportedly seen many people cashing in investments and flocking into cash. Yet, interest rates on cash savings have been very low – leaving people between a rock and a hard place.

The latest inflation figures from the Office for National Statistics shows that the Consumer Prices Index (CPI) rose sharply in January 2020 to 1.80%, having fallen in December 2019 to its lowest level since August 2016, at 1.30%.

Because savings rates have continued to fall, there are now just 50 savings accounts that match or beat the current rate of inflation – and you’ll have to tie your money up for at least two years to achieve this. If you are not in a savings account paying more than CPI, your money will be eroded by inflation – making it worth less in real terms.

This isn’t an unusual situation. Figures from our sister company, Savings Champion, show that just two years ago, when inflation was as high as 3%, there were no savings accounts available that could beat or even match inflation.

For this reason, those with a longer time horizon for their money needs, should consider investing into other assets, as this can produce valuable rewards – albeit with a degree of risk, dependent on your personal preference.

You don’t need to become a risk junkie if you move some of your money away from cash. In fact, maintaining exposure to several different assets including UK and global equities, fixed interest and alternatives, (which can include gold or other commodities and structured products with well-defined returns) as well as keeping your short term money in cash is actually a good way to reduce the risk of holding all your money in one asset class.

We do know how important it is to hold some money in cash – but there is no reason to let this remain with your high street bank. By actively managing your cash you can at least mitigate the effect of inflation, even if you can’t eradicate it.

For example, at the time of writing, HSBC is paying just 0.10% on its easy access Flexible Saver account, whereas Marcus by Goldman Sachs is paying 1.30% on its Online Savings Account. On a balance of £50,000 that is the difference between earning £50 gross per annum, or £650!

But for the longer term, you might want to consider investment elsewhere as it can produce valuable rewards. In a world of uncertainty, having the right assets to keep your investment journey as smooth as possible, is important.

More importantly, by having a mix of assets, investors don’t have to worry about wobbles in the stock markets – and when the best time is to buy and sell. By having a mix, this means that you can protect yourself from some of the downside, while still benefiting from some of the upside.

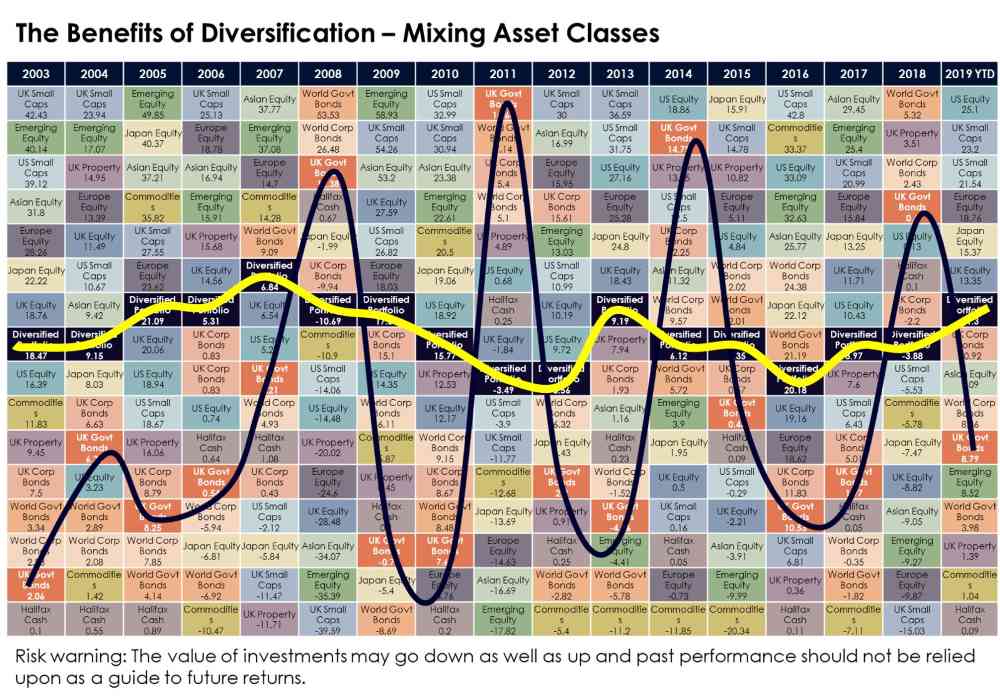

The chart below shows just how volatile different asset classes can be - for example, orange is UK Government Bonds, pale blue is UK Small Caps.

What it illustrates is that what does well one year has the potential to do badly the next.

But with the right investment portfolio you can diversify your risk and make your investment journey less dramatic.

The yellow line in the middle of the chart illustrates a diversified portfolio and shows that a good mix of assets can take away much of the volatility.

At TPO we currently have 17 Investment Portfolios - which means that you can find the portfolio that matches your investment goals and appetite for risk.

For example, TPO’s lower risk Portfolio I broadly holds 29% in UK and global equities, 34% in fixed interest and 37% in alternatives.

Compare this to the higher risk Portfolio VI which has 85% in equites, including Small Cap and Emerging Markets which are generally more volatile. The remaining portfolio is invested in alternative assets, including gold.

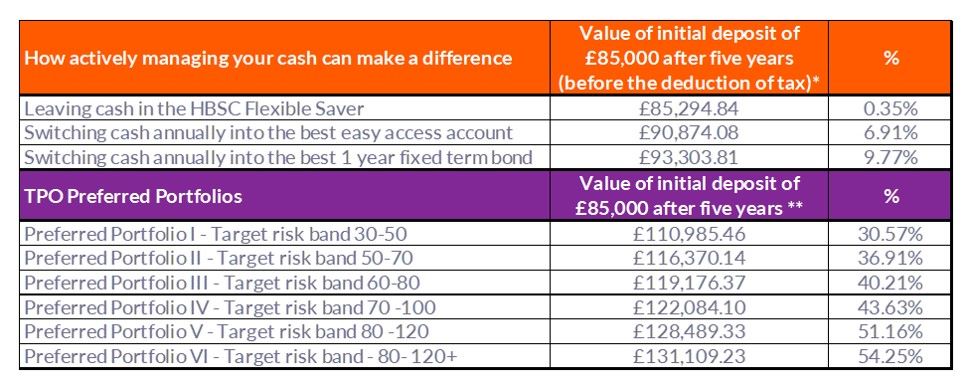

What you would expect to see is that the lower risk portfolios will outperform cash over the longer term but the higher risk portfolios will potentially produce the best returns – and this has certainly been the case over the last five years, as the table below shows.

Research from Savings Champion illustrates what a difference actively managing your cash could have meant over the last five years, compared to leaving money to deteriorate in a high street bank.

But it also shows that for the longer term, a balanced investment portfolio could do even better.

(We use - amongst other metrics - the standard deviation of the portfolios returns to assess the investment risk of a portfolio)

The key thing to remember is that the journey on some investment portfolios is likely to be far bumpier than others, so it’s important to take advice to make sure that you can use TPO’s investment and asset allocation expertise to help you weather the storms that are bound to be on the horizon.