Skip to main content

Skip to main content

Why you shouldn’t let redundancy affect your financial plan

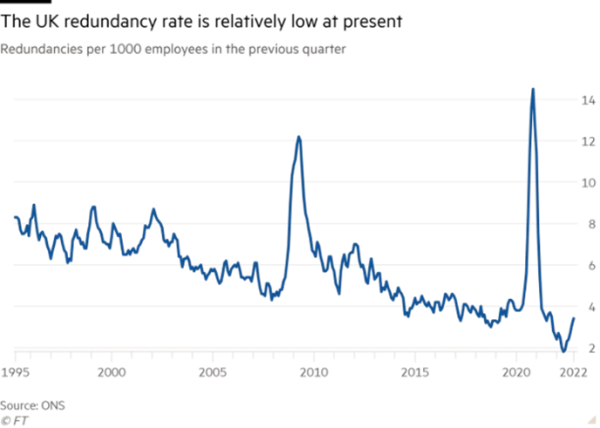

Since COVID-19 and the introduction of the furlough scheme, redundancy has been far more present. Following a steady decrease in the UK redundancy rate after the initial shock of COVID-19, there was an increase towards the end of 2021 and start of 2022 (see below). Despite this fairly recent trend, the redundancy rate remains comparatively low in the UK at roughly 3.4 per thousand employees (ONS Statistics: May, 2023).

However, the redundancy rate is anticipated to keep raising as confidence in businesses continues to fall, as per a recent Reuters poll on 25th April 2023. This lack of confidence is primarily driven by stickier than anticipated high inflation and interest rate hikes, making it difficult for many UK businesses. Moreover, the global situation remains turbulent, with the recent Silicon Valley Bank and Credit Suisse banking crisis, showing how fragile markets can be. This, alongside the Russian invasion of Ukraine, continues to contribute to the uncertainty and fears of further heightened conflict.

Naturally, the uncertainty facing us all also impacts businesses, with many household name companies laying off large amounts of employees, such as Google, Amazon and Morgan Stanley to name a few. This means more people are facing the threat of redundancy, so is important that being made redundant doesn’t impact your long-term financial goals.

How to help avoid your financial plan being derailed by redundancy

Cash Emergency Fund

A part of any financial plan needs to include a substantial emergency cash reserve, to ensure you are not immediately impacted by any shocks such as redundancy. As a guide, an emergency cash fund would typically be between 3 and 12 months of income. At TPO we spend significant time with our clients, using cash flow modelling, to provide answers around the size of your cash fund and how to build this buffer.

In turn using cash flow modelling and sticking to a financial plan, built with your adviser, you should have the comfort and reassurance that if a shock such as redundancy was to occur, you have built savings and investments to sustain you during such a period.

Age at which you are made redundant

Although redundancy is a shock to your financial plans and typically seen as a negative, it can also present an opportunity for those approaching retirement. One of the opportunities which may present itself is to make use of your redundancy payment as a contribution into your pension (up to your annual allowance or carry forward allowance). If you are close to retirement, it is an effective way of increasing the value of your pension pot with tax relief, before you potentially look to draw on it, in a tax efficient manner. All linked to your retirement plan.

For those who are younger when they experience redundancy, during the critical ‘accumulation’ stage of the financial plan, redundancy can point to the importance of having a financial plan and initiating these conversations with an adviser. Furthermore, typically those who are made redundant and are able to find new employment fairly quickly, there is an opportunity to implement a new refreshed financial plan to protect against any future shocks, which once again can we modelled within cash flow.

Remember, a drop or complete stop in both you and your employer’s pension contributions could seriously affect your financial plans, not least if this also includes a stop on any other benefits you may have received from your employer, such as a company car, phone or health benefits that may need to be replaced. So, it’s really important you take the opportunity to step back and re-evaluate the financial plans you have for the future, especially if you don’t get back into employment fairly quickly.

Redundancy Payment

A redundancy payment is treated as taxable income over the £30,000 tax free allowance. This payment therefore provides an amount to protect the employee from any initial cashflow problems. In terms of options for this payment there are many. As mentioned above you could contribute to your pension, which is especially tax efficient for those approaching retirement at the point of redundancy. However, there are other options as well. For instance:

- Make an overpayment/pay off a mortgage; this is a potential option to make your wider situation more secure and provide some additional comfort in a time of uncertainty.

- Hold the payment in cash accounts and draw on the money where appropriate to ensure you remain stable; this means ensuring your cash is earning the best interest is critical

Benefit of receiving advice

Conducted by one of our experienced financial planners, cash flow modelling provides you with clarity on your current financial position and what it might mean for the future.

It simply lays out all of your income and expenditure to map out your financial future. The earlier you seek advice and begin implementing a plan the more robust your situation will be to ride out any financial shocks such as redundancy. Having a clear plan with your finances is proven to be beneficial in the long run, and with our clients at TPO we utilise cash flow modelling to give them the comfort in case of redundancy or any other similar financial shock.

If you’d like to speak to an independent financial adviser about your own personal financial plans, whether you’re concerned about redundancies or not, then why not get in touch. We can map out your financial future so you have the confidence that your wealth will last you for as long as you need it.

Arrange your free, initial consultation

Please note: The financial conduct authority (FCA) does not regulate cash flow planning. Investment returns are not guaranteed, and you may get back less than you originally invested. Past performance is not a guide to future returns.