Skip to main content

Skip to main content

How to protect your wealth from future tax changes

Two years on and Coronavirus (COVID-19) is continuing to impact many aspects of our daily lives. We have been told there is an end in sight, but what will the aftermath look like and ultimately, who will be paying for it?

This unprecedented crisis has seen global economies band together to try to contain the virus while keeping their respective economies on track. Due to the UK Government providing a wide range of financial support packages, including the Furlough Scheme, it has eased the impact on all of us, including propping up businesses and the financial system, but resulted in an eye watering increase in Government debt over the 2020-2021 tax year.

Now in 2022, the Office for National Statistics has stated that the public sector net borrowing excluding public sector banks, was estimated to have been £16.8 billion in December 2021, £7.6 billion less than in December 20201. However, there is still a long way to go before we can recover and ultimately get our balance sheets in order.

The Chancellor of the Exchequer, Rishi Sunak, has the unfortunate task of reducing the debt while inflation is soaring. Because a key way to reduce public sector debt, is through tax hikes or in this case income tax freezes, it’s a perfect storm for us all – paying more tax while the cost of living is increasing sharply.

There will be a number of changes introduced in the 2022 Spring Statement so it’s important to understand what’s coming and how you can position your wealth to protect it from these changes.

Top tax tips to protect your wealth

ISA allowance

One of the key allowances available to you is the annual ISA allowance. Every tax year individuals in the UK have an ISA allowance, which is currently £20,000. You are limited to opening one of each type of ISA or you can use a combination of the following, each tax year: Cash ISA, a Lifetime ISA for a house purchase or retirement, or a Stocks & Shares ISA. Remember, your £20,000 limit is collective and not per ISA account.

What makes an ISA great from a tax perspective is that any gains, dividends or interest generated are free from tax. But do remember, that if you do not use up your full allowance in any given tax year, any unused allowance does not roll over. If you don’t use it, you’ll lose it.

Another great use of your ISA is the ability to pass your entire ISA pot to your spouse on death via a method called ‘Additional Permitted Subscription’. On your death, the value of your ISA pot can be transferred to your spouse and remain within the tax efficient ISA wrapper, without affecting their ISA allowance for that tax year. However, it’s worth noting that it is included in your estate for inheritance tax purposes.

Pension

When it comes to finding a way to maximise the allowances available to you in a tax friendly environment, there aren’t many better options than investing via a pension. Similar to the ISA, capital gains, dividends and interest are all free from tax within a pension. However, you are only able to access your pension pot from age 55 onwards, which will be increasing to 57 from 2028. This is across all pension accounts and does not alter except in specific circumstances, like ill health.

Current legislation permits that you have an annual allowance of £40,000 gross per tax year. Gross includes contributions from all sources (employer, employee and third party). Depending upon your earnings this could be less. In a simple example that means that if you are earning £30,000 your total gross contribution would be limited to this amount. But if you are earning £60,000 your gross contribution could increase if you have carry forward allowance. This means if you have unused allowance from the previous three tax years your gross annual allowance could be increased to mop up those unused allowances but once again, you are limited to your UK relevant earnings. But you’ll need to hurry, as time is running out for the current tax year.

The amount that you can contribute also changes at both ends of the earnings spectrum. For example: if your total taxable income plus employer contributions are over £240,000 a year, your gross annual allowance reduces by £1 for every £2 of earnings over the threshold, down to a minimum allowance of £4,000. In contrast, if you aren’t earning anything in a tax year, you can still contribute £3,600 gross per tax year to a pension.

What also makes pensions a great tax-efficient way to invest for your future is that the contributions that you make benefit from tax relief. Every contribution that you make to a pension, benefits from a top up by the Government equivalent to basic rate tax, meaning that a £100 contribution technically costs £80 to you and the Government tops up the remaining £20. The pension relief doesn’t stop there though. Additional tax relief is also available to anyone who is a higher or additional rate taxpayer too. The only main difference is to be able to claim the additional tax relief of 20% (higher) and 25% (additional) you must complete a self-assessment tax year at the end of the tax year.

Last but not least, under Pension Freedoms rules, your pension can be outside of your estate for inheritance tax, provided your pension facilitates this, and so is a really tax efficient method to pass on your wealth to your loved ones.

Currently there are no proposed changes to the rules surrounding pension pots.

Capital Gains Allowance

Another quick tax tip is to realise investment gains. Investment gains typically occur in a portfolio that is not held in an ISA or pension, where you have benefitted from growth in a given tax year. In order to not incur a capital gains tax charge you can realise gains up to your annual allowance, which currently stands at £12,300 for the 2021/22 tax year. This can be achieved by selling a proportionate amount of your portfolio so that any gains fall below the threshold. Better still, you can sell your investments and transfer them into an ISA. The overall result being that you don’t pay any capital gains tax, you remain invested, but this time in an ISA that comes with paying no tax on growth, dividends and interest.

What also makes realising investment gains slightly more appealing is that if you choose to realise gains above the annual CGT threshold, then they are only taxed at 10% if the gain does not push you into the higher rate tax bracket when added on top of your income, and 20% for higher or additional rate taxpayers, rather than being aligned to income tax rates of 20%, 40% and 45%. The only exception to this tax rule is the sale of residential property, which is taxed at 18% and 28% on gains respectively.

What to look out for in 2022?

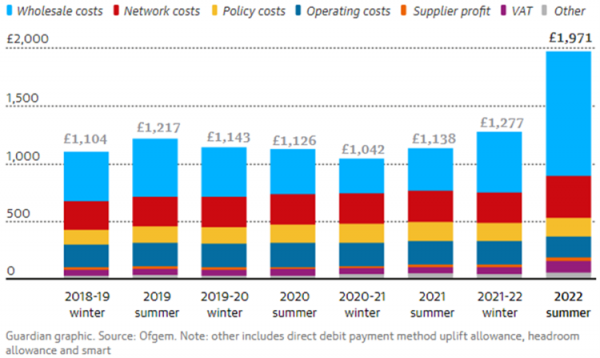

One of the biggest challenges that the UK government is facing in 2022 is the surge in living costs due to rising energy prices and consumer inflation reducing household income. We are on track to see inflation rise to 7% by the spring before it begins to fall again. This will have a huge impact on your income, eradicating some/all salary increases and maybe bonuses too. The Bank of England say it is unlikely that the prices of energy and imported goods will continue to rise and expect inflation to be closer to the 2% target in two years’ time. So what provisions are being put in place to help ease this increase in the cost of living?

Cost of living package

Rishi Sunak, Chancellor of the Exchequer, has announced his £9 billion package to reduce the strain of the £700-a-year rise in the average household’s energy bills in April. This takes the form of the following:

- All households are to receive £200 off their energy bills in October – but must pay this back in equal payments of £40, over 5 years from 2023.

- English council taxpayers in bands A to D will receive a £150 rebate from their bills, which will not have to be paid back.

- Local authorities would receive £150 million to make discretionary payments to the neediest.

- The number of poorer households who will be eligible for the warm homes discount will be increased by a third to 3 million.

There is no application process for the £200 energy discount as it will automatically be applied by your energy supplier. This will take place in the Autumn and the government will initially pay the difference with their intention to have it recouped over 5 years from 28 million households. Secondly, as council tax prices are due to rise in April, in the same month there will be a refund of £150. This will automatically be paid into the bank accounts of those who pay via direct debit. This rebate is not to be repaid.

National insurance increases

One new policy to be aware of is the Health and Social Care Levy. The funds generated from this levy are to be directly used for the NHS, health and social care which comes into effect in the UK on the 6th April 2022. This new policy will be funded through a 1.25 percentage points increase in National Insurance contributions, affecting employers, employees and the self-employed. This increase is intended only for one year before the levy becomes its own separate tax. From April 2023 you will see the 1.25% levy on your payslips as a separate deduction.

Can you avoid the social care levy?

The separate levy tax will be unavoidable from April 2023 but one method to reduce the amount of National Insurance contributions you pay is to make higher pension contributions through salary sacrifice. Not only does increasing your pension contributions through your employer reduce the amount of National Insurance both you (employee) and your employer pay but can potentially bring you into a lower tax band (depending upon your earnings). If you earn just over the basic/higher rate tax band or receive a bonus that pushes you over the threshold, you can ask your employer to increase your salary sacrifice pension contributions to reduce your overall tax liability. Another method is bonus sacrifice, by paying the bonus directly into your pension pot you can avoid being taxed on your bonus and may reduce your marginal tax rate. This is an option to consider should you wish to make pension contributions from your earnings, and you have the affordability to do so.

Frozen allowances

Announced in the Spring 2021 statement, your personal allowance of £12,570 and the higher rate threshold for income tax of £50,270 will be frozen for the next four years, along with the Inheritance Tax threshold of £325,000, pension lifetime allowance of £1,073,100 and annual Capital Gains Tax exemption of £12,300. What this means is that over the next four years the UK government is due to generate more funding as more of your income, estate and investments will be taxed over this period. The Treasury has released a forecast that states these income tax freezes will raise an additional £2.77 billion in 2022/23, rising to £13.04 billion in 2025/26. Total receipts from income tax are now forecast to rise from £229.6 billion in 2022/23 to £268.4 billion by 2025/265. The above statistics only account for income, imagine the amount the Treasury stands to make from the other allowance freezes too, so making use of your tax efficient allowances has never been so important.

Aside from salary sacrifice into a pension, there are other ways you can reduce your income tax liability. If you are married, you can make use of what is known as the Marriage Allowance! Should your spouse earn lower than their personal allowance or be a non-taxpayer due to use of other allowances (dividend, PSA, starting rate band etc.) they are able to transfer up to £1,260 to the higher earner (as long as they are still a basic rate taxpayer) to save around £252 per tax year.

By not using all the available allowances, more people will pay tax and more people will pay tax at higher rates as a result, as well as more estates being liable for Inheritance tax. Once again, the one saving grace is making full use of your pension pot. This incredibly tax-efficient tool is normally (there are some exceptions) outside of your estate for inheritance tax.

Second to that is making use of your gifting allowances; due to the frozen Inheritance Tax threshold, gifting in your lifetime is vital to avoid the 40% tax charge your beneficiary would pay on death. You can gift up to £3,000 per tax year, make regular gifts from excess income, make as many gifts as you like up to £250 per person per tax year or make charitable/political party gifts. All are immediately counted outside of your estate for inheritance tax. You can make further gifts outside of your gifting allowances, but this is subject to the 7-year rule before they are inheritance tax free.

How can you ensure you are prepared?

Legislation changes can cause volatile periods in the market and have huge effects on your investment returns and tax liability. Periods like this are when you see the benefits of a Financial Planner constantly monitoring the market changes and reviewing your financial plan on a regular basis.

Speaking to your Financial Planner and determining whether your assets are appropriately placed to weather any impending legislation changes will allow you to have peace of mind that there is nothing further you can do.

If you do not have a financial adviser or you are simply looking for further advice regarding your own personal finances in this uncertain time, we offer a free initial consultation, why not get in touch and speak to an adviser.

Please note: Information regarding taxation levels and basis of reliefs are dependent on current legislation and individual circumstances, are not guaranteed and may be subject to change. The value of your investments can go down as well as up, so you could get back less than you invested.