Skip to main content

Skip to main content

How to prepare your finances before you die

Whilst uncomfortable to think about, we should all consider how prepared our finances and affairs are before we pass away.

Not only does this help save your loved ones a large financial headache after the event, but it also ensures your wishes are met for your estate.

We have produced this article to help provide some practical steps that you can take today to get your finances in order in the event of your death.

Arrange your free initial consultation

1) Create a valid will (and ensure it reflects your wishes)

In short, a Will gives you the power to control:

- What happens to your estate following your death.

- Who carries out your wishes and manages the estate until it is distributed (this role is known as the executor; it can be more than one person)

- Who receives your estate (known as the beneficiaries)

There are various guides and services available to you to create your own will, however, we recommend you seek out legal guidance, especially if your wishes may be complex.

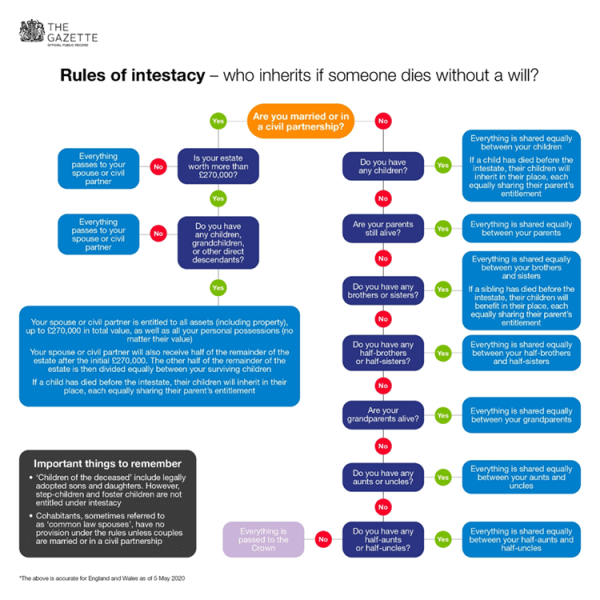

What happens if I die without a will?

If you die without a valid will in place it is called dying ‘Intestate’. This means that your estate will be distributed in line with the rules of intestacy.

The London Gazette have a helpful flowchart guiding you through the rules of intestacy:

Source: https://www.thegazette.co.uk/wills-and-probate/content/103523

This highlights the importance of having a will in place.

We recommend you review your will whenever important life/ personal changes occur – e.g. the arrival of a new family member/ divorce / etc.

2) Understanding your Inheritance Tax (IHT) position

It is also worth reviewing what your IHT bill might be on death. IHT is chargeable at 40% over your allowances, but there are certain allowances and actions that can help reduce the impact on your beneficiaries and your estate, for example:

- The exemptions on your estate that are covered by the Nil Rate Band (£325,000) and Residence Nil Rate Band (£175,000).

- If appropriate, gifting 10% of your net estate to a registered charity will reduce the IHT charge from 40% to 36%.

This is a complex area with rules governing the use of these allowances, especially when large gifts have been made whilst you are still alive. When gifts are made, we would recommend that you make a habit of keeping an accurate record.

This is because it is your executor’s duty to inform HMRC of any gifts before probate is issued, and HMRC may challenge them. Gifts up to your annual exemption amount of £3,000 (regarding tax year 2022/23) do not need to be recorded with HMRC. However, HMRC will closely examine the gifts made within 7 years of death, and most of us are unlikely to know when we will die!

The timing, amount and type of gift can impact the inheritance tax position of the estate, so accurate records are crucial.

Inheritance tax planning is a complex area, so it is always worth taking independent financial advice to understand your potential IHT position and the potential consequences of any actions. It also helps future generations understand how to plan for receipt of any inheritance that you may have allowed for in your will.

If you would like further information on this topic, we have another article that covers IHT and Estate planning in more detail.

3) Have appropriate Financial Protection

Financial protection can be used to give the financial support to those we leave behind. Nobody wants to have to contend with the loss of a loved one and worrying about how to pay the bills.

Financial protection can be used for many purposes for example:

- A lump sum payment covering the mortgage on the family home

- A regular income stream to replace the loss of household income

- Having funds to cover inheritance tax liabilities

There are many benefits to having life insurance and like a Will, this is something you should regularly consider with changes in life.

Reviewing what protection you can obtain, or already have, through work (whether employed or self-employed) is often a good starting point. For example, Death in Service plans are quite common and will cover set multiples of your salary. Employers may also offer further protection benefits where they cover the premium costs (but there will probably be income tax considerations on the benefit).

Deciding what level of cover and type can be overwhelming amongst the many plans and variations on offer. For a stress-free approach an independent financial adviser can help guide you to a bespoke solution to give you peace of mind.

4) Pensions: Checking your Pension Nominations and Death Benefits

Defined Contribution pensions are typically setup under a trust arrangement meaning they are separate from your estate when you die. However, each pension provider will have their own rules on what happens to the pension benefits on death.

Typically, you can nominate who will receive your pension on death. So, like a Will it is important to keep this up-to-date with your wishes.

Now you have a beneficiary(s) in place, it is worth considering what options your pension provides on death, if any.

It’s important to be aware that some plans may not offer any options and could pay the fund back into your estate or that of your nominated beneficiary(s).

The most flexible plans will allow your beneficiary(s) to fully control the pension regarding flexible access and investment choices.

Learning what your pension death benefits are and the flexibility offered will help determine if you have the right setup to leave your loved ones. You can consider transferring to a more flexible arrangement, but it is worth seeking independent financial advice on this as pensions are a complex area and you may have guarantees that could be lost on transferring.

5) In Case of Emergency (ICE) Document

Keep an In-case of Emergency (ICE) document, containing all the important details should something happen to you. This can help you record all financial and personal information in an accessible way to help your loved one's deal with your affairs.

We have vast experience in helping people manage their wealth and putting into place effective strategies for passing wealth on to future regenerations. If you’d like to learn more about how we can help you, why not get in touch for a free initial consultation.

Arrange your free initial consultation

Please Note: The value of investments can fall as well as rise. You may not get back what you invest. The Financial Conduct Authority (FCA) do not regulate wills, estate or cash flow planning, or tax advice.