Skip to main content

Skip to main content

Inheritance tax planning – Strategies to protect your wealth

Former Labour Chancellor, Roy Jenkins, famously described Inheritance Tax (IHT) as a “voluntary levy paid by those who distrust their heirs more than they dislike the Inland Revenue”. While that statement may divide opinion, there is no doubt methods exist in order to mitigate or avoid completely an IHT liability on your estate on death.

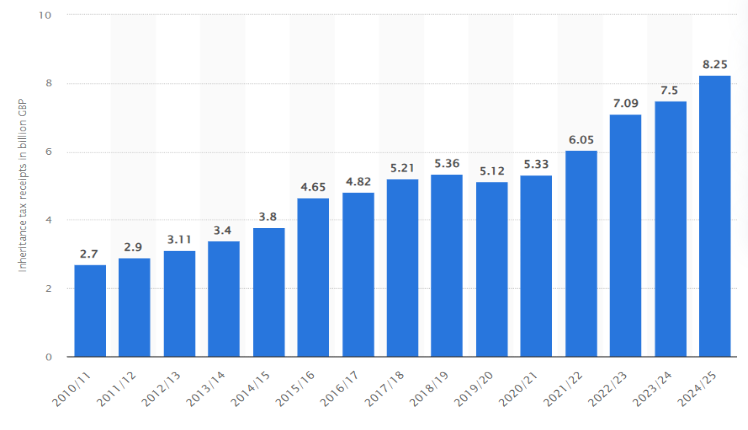

Inheritance tax receipts

IHT receipts in the UK amounted to £8.25bn in the 2024/25 tax year, a staggering increase of over £700m from the previous tax year which was a previous peak.

Figure 1 - Inheritance tax Receipts 2020-2025, Source: Statista

This can be in part attributed to a ‘stealth tax raid’ from the Government, as allowances have been frozen for a number of years, with the chancellor, Rachel Reeves, also announcing in her Autumn Budget last year that the current IHT thresholds would be frozen until at least April 2031.

Currently, the ‘nil rate band’ allows you to pass on £325,000 of your estate without paying IHT, and an additional ‘residence nil rate band’ of £175,000 is potentially available if your main residence is passed on to direct descendants, giving an IHT allowance of £500,000 per individual or £1m for a married couple/ civil partners. Any value of your estate above these thresholds will typically be subject to IHT at 40% (as noted in more detail below, the latter allowance can be tapered if your estate value exceeds £2m).

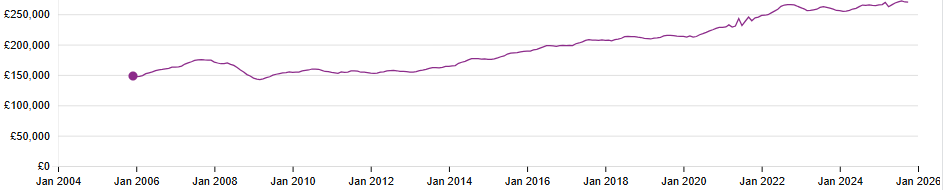

Although an IHT-free threshold of £1m may seem quite generous, the number of people caught in the IHT net has been increasing for several years, due in the main to the rapid increase in property prices. In the 20 years running up to October 2025, which is the latest stats from the Land Registry, the average UK house price has almost doubled to nearly £270,000.

Figure 2 - Average price by property in UK, Source: Land Registry

The residence nil rate band taper

Inheritance tax planning becomes increasingly valuable for estates exceeding £2 million, where the potential tax savings can be most significant. For every £2 of your estate value over £2m, the residence nil rate band is reduced by £1. Therefore, the full residence nil rate band is lost if the value of your estate exceeds £2.35m for an individual or £2.7m for a married couple.

What this means in practice is that for a married couple with an estate value of £2.7m the IHT-free allowance can be reduced from £1m down to £650,000, potentially resulting in an additional IHT liability of up to £140,000 (£350,000 @ 40% IHT) due to the loss of this valuable additional allowance.

What can I do to reduce my Inheritance tax bill?

Whilst inheritance tax planning can take the form of complex trust arrangements where appropriate, below are some of the key IHT mitigation strategies to consider:

Spend more – an often overlooked but simple and effective method of reducing the value of your estate, which you will also hopefully get some personal enjoyment from!

Gifting – as shown below, there are certain types of gifts that will fall outside of your estate immediately for IHT purposes. Any gifts that are not immediately tax exempt or within the annual allowances are treated as either potentially exempt transfers (PETs) or chargeable lifetime transfers (CLTs). PETs allow you to make gifts of unlimited value which will be exempt from IHT if you survive for a period of 7 years, subject to the 14 year rule not applying. If you don’t survive the gift by 7 years, the PET becomes chargeable and is added to the value of your estate.

Certain gifts, most commonly gifts into trust, may instead be treated as CLTs and could give rise to an immediate IHT charge, depending on the circumstances. Specific rules may apply to any gifts made into trusts. Please do get in touch if you require information in this regard.

IHT gifting strategies

Annual gifts

Individuals can give up to £3,000 each tax year free of inheritance tax, and any unused allowance from the previous year can be carried forward one year, allowing up to £6,000 to be gifted in a single year.

Small gifts

You can give as many gifts of up to £250 per person each year, provided each recipient is different. These small gifts are separate from and additional to the annual £3,000 exemption. However, they can't be in addition to the £3,000 given to one individual.

Wedding gifts

Certain gifts made in anticipation of a wedding or civil partnership are exempt. The limit is:

- £5,000 to a child

- £2,500 to a grandchild or great-grandchild

- £1,000 to any other person.

Gifts from income

Regular gifts can be made from surplus income without triggering inheritance tax, as long as these payments are genuinely from income rather than capital and do not reduce your normal standard of living. They must also form a pattern.

Gifts to charities and political parties

Gifts to registered charities and qualifying political parties are free from inheritance tax, whether made during your lifetime or on death.

Lifetime gifts

Gifts that do not fall under a specific exemption are treated as potentially exempt transfers or a chargeable lifetime transfer (CLT). These may become fully exempt if you survive seven years, but they can be brought into account if death occurs within that period.

How to reduce your IHT rate from 40% to 36%

Another benefit of gifting to charity is if 10% of your net estate (i.e. the value of your estate above the tax-free allowances) is gifted to charity on death, the rate at which IHT is charged on your taxable estate falls from 40% to 36%. This can significantly reduce any ‘cost’ of a gift to charity and ultimately the amount of your estate that is paid to the taxman.

Life insurance to reduce IHT

Set up a life insurance policy – although not mitigating IHT, a life insurance policy can ensure that your beneficiaries have sufficient capital to cover the IHT liability. It is important to consider writing the policy in trust, so it doesn’t form part of your estate and the payment on death is accessible for your beneficiaries prior to any required IHT payment.

Investing in business relief assets to reduce IHT

Invest in Business Relief (BR) assets- originally designed to allow family businesses to be passed through generations without the need to be sold or broken up to meet an IHT liability, Business Relief can apply to certain qualifying investments, such as shares in unquoted qualifying companies. While most lifetime gifts are subject to the seven‑year rule, qualifying Business Relief assets can be transferred free of IHT once they have been owned by the donor for at least two years.

There are two tax points for IHT that the donor should be aware of on a gift of Business Relief assets. One is at the point of making a gift and the other is at the point of death of the donor, if death occurs within seven years of the gift. The gift of BR shares should provide relief from IHT, provided they were held for at least two years. It is important to note that once an asset has been gifted, control over that asset cannot be retained by the donor. On death, the recipient needs to hold the shares for seven years or, if earlier, at the time the donor dies, for the gift to continue to provide relief from IHT in the donor’s estate. If the recipient disposes of the shares before the donor’s death or before seven years have elapsed, the relief may be lost and the value could become subject to IHT in the donor’s estate.

From April 2026, the combined allowance for Business and Agricultural Property Relief will be capped at £2.5 million per individual (transferable between spouses), with any excess qualifying for relief at 50%. This allowance will refresh every seven years for lifetime gifts and will be indexed to CPI from 2031. In addition, unquoted shares listed on recognised exchanges such as AIM will only qualify for 50% relief under the new rules.

These types of assets are however typically very high risk and can be difficult to sell, hence should be approached with caution. Therefore, this will not be appropriate for all clients.

Changes in pension legislation

One of the most significant recent changes in the IHT space is the change in pension regulation, expected to come into force from 2027. From 6th April 2027, the Government is planning a significant shift in how pensions are treated for IHT. Under the new rules, most unused pension pots and death benefits will count as part of your estate, meaning they could be taxed at up to 40% if they push the total value of your estate over your available thresholds. This is a significant change from current treatment, where pensions have generally been exempt from IHT and therefore used as an estate‑planning tool.

Looking ahead, pensions will play a much bigger role in estate planning than before. With upcoming changes to the IHT rules, it is important to review how your pension fits into your overall strategy. This could open up new opportunities to protect wealth, manage tax efficiently, and ensure your assets are passed on in the way you intend

With these changes in mind, it is important to keep pension funding as a key part of your wealth building strategy before retirement. Pensions don’t just help you prepare for later life, they also provide valuable tax advantages, such as tax relief on contributions and tax efficient growth. Making the most of these benefits now can give you greater flexibility and security in the future. What’s more, recent changes have made pensions even more attractive as the standard annual allowance for contributions has increased from £40,000 to £60,000, and the lifetime allowance has been removed, giving you more scope to invest for the long term.

Can I just gift my main residence to my children?

In simple terms, no. If you continue to live in the property after the gift was made, this will be treated as a ‘gift with reservation of benefit’ and the property would remain in your estate. In order for this strategy to be effective, you would need to pay your children the full market rate rent after gifting the property to them, which can result in additional tax consequences.

How we can help

A starting point for estate planning is ensuring you have a valid Will in place. This will ensure that your estate is distributed as per your wishes and could reduce the potential IHT liability payable on your death.

Thereafter, whilst mitigating IHT may seem like a key objective, a balance needs to be struck between tax efficiency and retaining sufficient assets to meet your own needs in later life.

One method in which we can assess the viability of different IHT mitigation methods is through cash flow modelling, whereby your financial future is mapped out so you can see what wealth you need for the life you want, so why not get in touch today to arrange a free no obligation initial discussion with one of our expert advisers

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

This article is also based upon our understanding of current law, HM Revenue and Custom's practice, tax rates and exemptions which are subject to change.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, will writing, tax or trust advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.