Skip to main content

Skip to main content

Taking income from your investments without damaging your wealth

Accumulating funds over the long term is a relatively simple process. Money is invested, and it grows. Admittedly, there will be ups and downs along the way but as any long term investor knows, if you sit out the storms, within a year or two the portfolio is likely to have recovered and over the long term, returns are likely to be superior to leaving the money in the bank. This is, after all, the whole point of investing.

The problem arises when the time comes to use the portfolio to provide an income, and for most people this is when they stop earning and enter into retirement. No more funds are added, and the portfolio has to generate income for the rest of your life.

With many retiring early and longevity increasing, this could be 30 or 40 years. A frightening concept which only goes to highlight why it’s so important to save from a young age. Ideally, the income generated should increase to combat inflation. If the intention is to leave money to children or other loved ones, in which case your pension can be your most inheritable asset, then we are asking quite a lot from our carefully accumulated fund.

One popular method is to invest in companies which pay dividends (you can also read more here about the dividend tax-free allowance). The COVID pandemic came as a shock for many as dividends were severely cut globally. Investors who bought bank shares to generate income before the financial crisis of 2008/09, have an even sorrier tale to tell.

So, what happens if we simply make regular encashments from our portfolio?

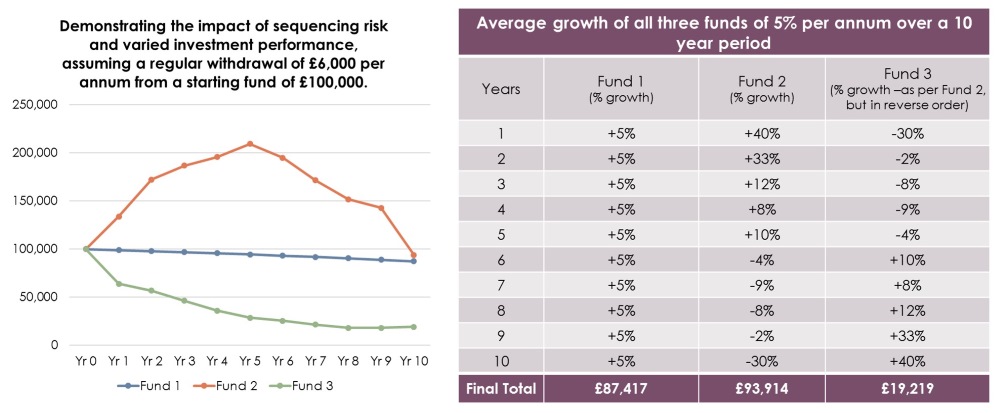

Let’s say we start off with £100,000. If the portfolio grows at 5% each year after all charges have been deducted and we withdraw 6% a year what would happen after ten years?

Presumably the portfolio would reduce by only a small percentage each year and this might sound acceptable. The problem is that investment returns are not predictable and although a portfolio may grow on average by 5% a year, in reality some years may see high growth and some years may see negative growth.

The illustration below charts the value of £100,000 with a withdrawal of £6,000 a year (6% of the original investment) in three different scenarios.

What is important here is that in all three cases the portfolios achieve exactly the same 10-year growth - so without any withdrawals, you would end up with exactly the same portfolio value.

- The blue line demonstrates what would happen if the growth is a predictable 5% a year. In this case, as we would expect, the capital value reduces gradually so that after 10 years it is worth £87,417.

- The orange line demonstrates what would happen in a volatile market where most of the growth occurred in the first five years. In this case, after 10 years it is worth £93,914.

- The green line demonstrates the danger of most of the growth happening later – whilst remaining modest or even negative in the early years. In this scenario, if the withdrawals are fixed at £6,000 per year, real damage is done during the early years and the portfolio can’t recover, so after 10 years would be worth just £19,219. This is known as sequencing risk.

"Real damage is done during the early years and the portfolio can’t recover, so after 10 years would be worth just £19,219. This is known as sequencing risk."

This highlights how unnerving it can be and reveals the real danger of making withdrawals at the wrong time.

How can you try to remove this risk?

It is not realistic to retire with a lump sum and only withdraw money during years of good performance and for most, just leaving the money in the bank will not generate the returns we need.

Historically, deposit returns do not keep up with inflation resulting in a reducing value in real terms. How then, are we to invest in such a way that we can generate good returns over the long term and still receive a regular income without interruption or sleepless nights?

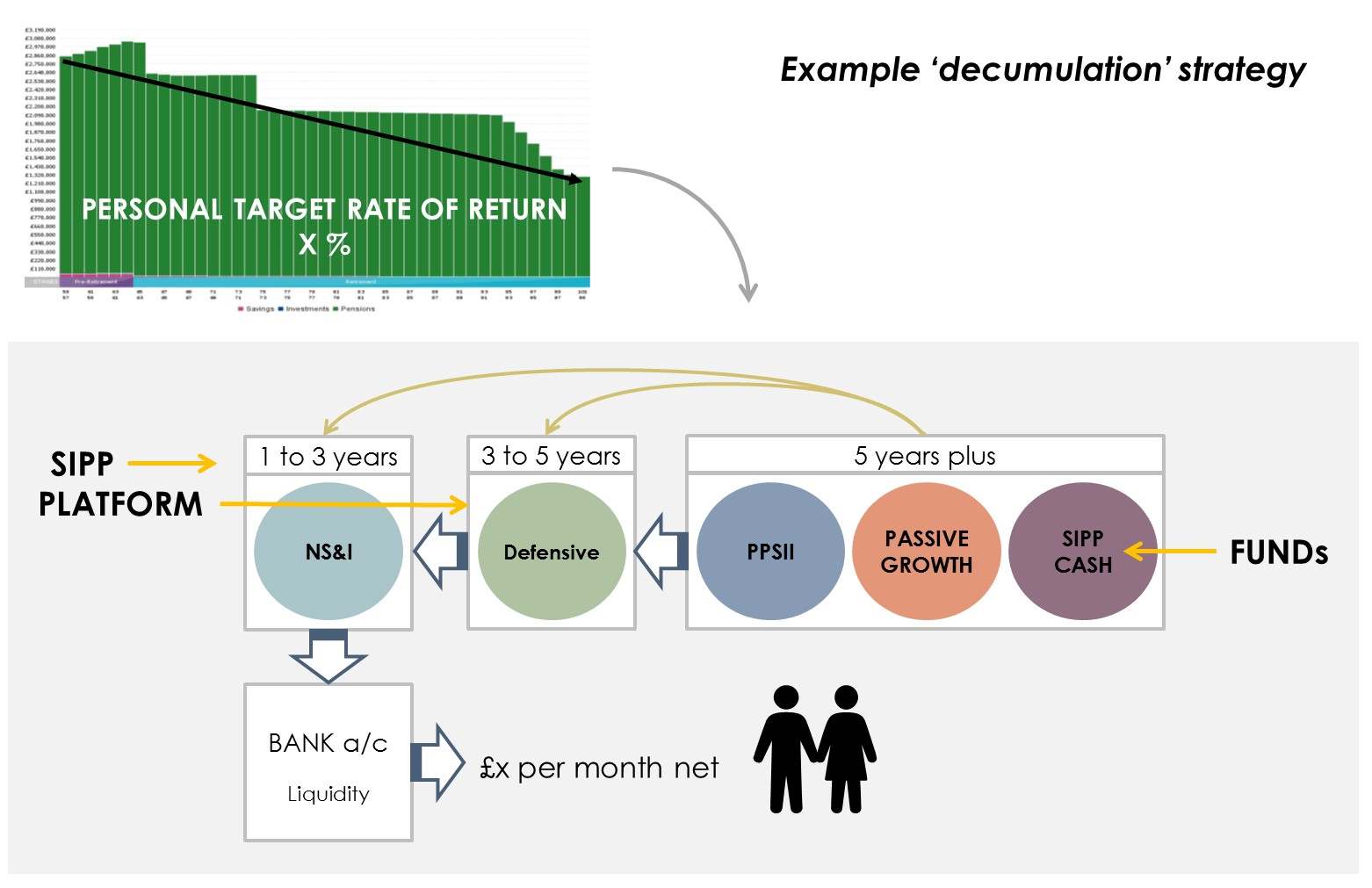

"The answer lies in structuring the portfolio in layers. Instead of one portfolio with one risk profile, we need three portfolios, and possibly more."

The first thing to do is to establish what we need to spend every year and then set aside two or preferably three years’ worth of income in cash. In our example above this would mean setting aside 3 X £6,000 = £18,000 in cash.

From a practical point of view it would probably not be a good idea simply to put £18,000 into the current account, but we could, for example, set up a deposit account (getting better interest) which feeds £500 per month into the current account. Let’s call this Pot 1.

The second step is to consider the medium term, say years three to seven - Pot 2. This should be invested in a lower risk portfolio. Lower risk portfolios, typically, have less exposure to equities (shares) and a higher exposure to fixed interest and other asset classes which are designed to offer more capital protection in exchange for lower growth potential. In our example this would mean investing £30,000 in lower risk.

This would leave £52,000 available (Pot 3) and this can now be invested in a higher risk portfolio. This is where we would expect to see the highest volatility and, of course, the highest returns over the long term. The beauty of this structure is that Pot 3 need not be touched for 8 years if need be, which should give us enough time to recover from the worst crash imaginable.

Although Pot 3 might seem to pose a higher risk than you might normally take with your investments, looped together with the other pots, it actually means your overall investment strategy is much more balanced, as, in our example, nearly half of the investment portfolio has been taken up by cash and a lower risk portfolio.

The secret is to review regularly

The structure requires annual reviews. After the first year our cash pot (Pot 1) has reduced by £6,000 so we need to top it up with another £6,000 so that we can maintain the important buffer of three years’ cash at any moment in time.

If, in this first year, markets have done well we can take “profits” from Pot 3 to top up cash. If returns have been poor, then we can top up the cash from Pot 2 (or not at all if it has been such a bad year that even a low risk portfolio has performed poorly). In some years it may be necessary to take “profits” from Pot 3 to top up cash and Pot 2 so that the overall structure retains the correct risk profile.

In this way “income” can be accommodated permanently without fear or guilt and, at the same time, we are not sacrificing long term returns by forcing the whole portfolio to be de-risked. After all, retirement is about enjoying your well-earned money, not stressing about the volatility of stock markets.

"After all, retirement is about enjoying your well-earned money, not stressing about the volatility of stock markets."

Here’s an example of how it might work in a situation where regular income needs to be generated from a Self Invested Personal Pension (SIPP). The example is known as a decumulation strategy, simply put when you are looking to draw an income for your retirement. In a personal review, the graph would show you want target rate you’d need to achieve to maintain your lifestyle and wealth, whilst the pots show you a typical scenario.

If you’re looking for advice on the best way to generate income on your wealth why not get in touch and speak to one of our Independent Chartered Financial Planners. We’re happy to help.

We’re currently offering all of those with £100,000 or more in savings, investments or pensions a FREE cash flow investment and retirement ‘do-nothing’ scenario review worth up to £500. The review can help you look at what your financial future may look like and what small changes you can make now to make a big difference to your outcome. Have you got enough for your retirement? Find out more here.

Past performance is no guarantee of future returns. The value of investments and the income from them can fall as well as rise, you may not get back what you originally invested.