Skip to main content

Skip to main content

Santa rally got here early in November, but will it stay for Christmas?

Better than expected inflation data has led investors to speculate that central banks have room to cut interest rates in 2024 by more than the bankers have previously been implying. The shift in sentiment had a big impact on equity and bond markets but can this momentum be maintained?

This article explains some of the background and concludes that markets have room to move higher, but question marks will resurface as central bankers don’t want to be seen to be soft on inflation risks.

Arrange a free initial consultation

Changing expectations on inflation?

Interest rates and inflation expectations have fluctuated significantly in 2023. After over a year of rising rates as central banks battled high inflation, markets have begun pricing in the possibility of rate cuts in 2024 as price pressures start to ease. This article will examine interest rate expectations in the US, UK, and Eurozone (with emphasis on the US) and explore how these shifting expectations have impacted asset prices and investor sentiment.

Figure 1. The journey that US inflation has been on as represented by Headline Consumer Prices, Source: U.S. Bureau of Labor Statistics

Figure 1 above shows the path of consumer prices in the US, the figure is the headline rate when comparing prices now to a period 12 months prior. The headline figure includes volatile items such as energy and food prices, along with the more stubborn inflation that is associated with wages. It is the latter that the central banks worry about. In November, it was the lower than expected consumer prices figure that got investors excited that the Federal Reserve in the US may have room to cut interest rates more quickly than they have been indicating.

As it stands today, the Federal Reserve is indicating that there might be 3 rates cuts next year, each of 0.25%. However, following the November inflation number and more recent comments from the Federal Reserve Chairman, Powell, investors are now factoring in 6 interest rate cuts of 0.25%. The last time expectations of interest rate cuts got to anything like this level was during the regional banking crisis in May this year. So, you can see that dramatic moves in interest rate expectations are more usually associated with crisis situations.

US inflation has slowed materially in the last few months, as the labour market has come into greater balance. In addition, supply chain pressures have eased and falling oil prices have dampened cost pressures on businesses and consumers. As inflation has come closer to the 2% target (core inflation has run at around 3.5% over the last three months) investors have begun to look ahead to a return to interest rates that are closer to the so-called ‘natural’ rate of interest – this is the theoretical rate of interest consistent with neither a contracting or overheating economy and is estimated at around 1-1.5% above the rate of inflation by the Federal Reserve Bank of New York.

The roadmap for Interest rates

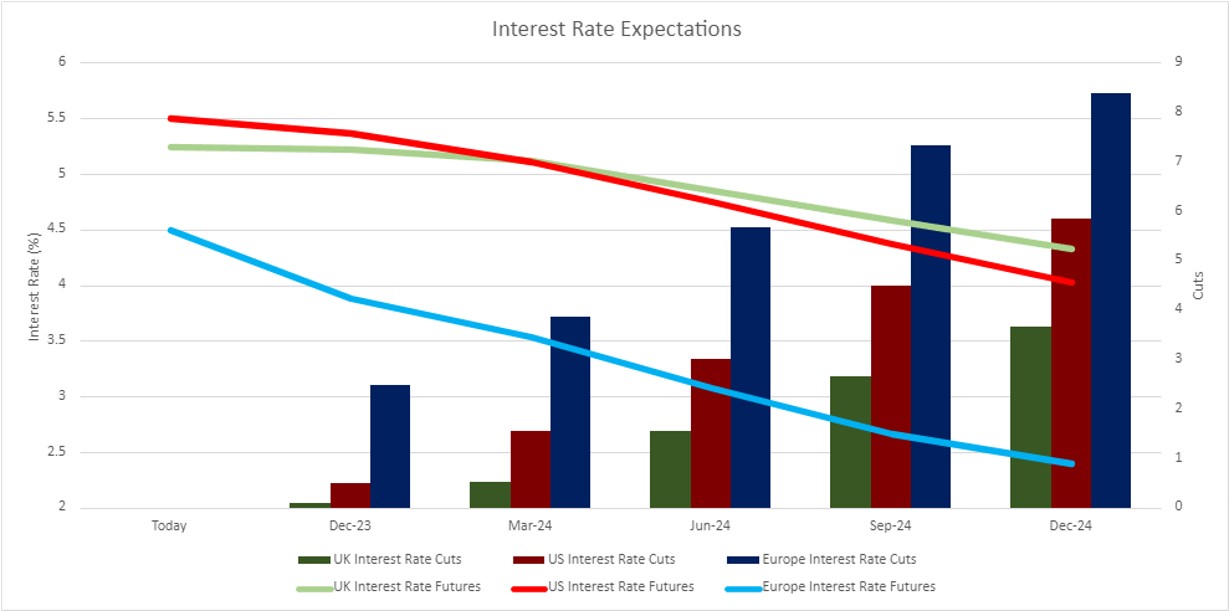

It is not only in the US that markets are seeing slowing inflation and an increased likelihood of interest rate cuts, as the following graph shows:

Figure 2. The path of expected interest rates in the US, UK and Europe, Source: Trading Economics

The above chart compares investor expectations for the number of interest rate cuts of 0.25% in 2024, across three central bank regions, the US, UK and Europe. The bars show the number of cuts expected in each region

Looking at an international comparison, we see that interest rate cuts are not only expected in the US, but also in the UK and EU. Europe stands out, with markets expecting over 8 cuts by December 2024. European inflation has followed US inflation down, however that is only half the story, as economic growth in Europe is expected to deteriorate to a greater extent than in the US. Growth has been weaker in the EU than US throughout 2023 and that relative position is expected to continue, with US growth slowing and the EU expected to see economic contraction.

Markets expect the ECB will have to loosen monetary policy substantially in a bid to kickstart growth. The UK, on the other hand, is expected to have comparatively few interest rate cuts. This is owing to the perception of more entrenched UK inflation, particularly wage-driven inflation in the services sector. (this topic was covered in the previous edition of the investment market update).

Figure 3: Performance of the S&P 500 (orange line) and the markets expectations of a fall in US interest rates (white line), Source: Trading Economics

This graph shows the S&P 500 equity index (the main US stock market) in orange, with the number of cuts expected by December 2024 in white.

There is clearly a link between rate cut expectations and equity market performance. This has led the S&P 500 to gain over 8% through the month of November. The increase though in the S&P 500 during November and over the course of the year has been the result of seven of the largest stocks dubbed the ‘Magnificent 7’ outperforming given that they are beneficiaries of the artificial intelligence wave which has been a key theme in markets. Conversely the performance of remaining 493 stocks has been broadly flat which has created a divergence in the performance of US large cap companies and small cap companies.

We have begun though to see increased attention for those stocks which have underperformed year-to-date most notably with small cap companies. This move from an ‘only the 7 rally’ to ‘everything rally’ was not an exclusively equity market phenomena, with rallies seen in government bonds, corporate bonds and even beaten-down asset classes like infrastructure. Rallies in bond markets pulled bond yields down, which allowed corporations to access financing at lower rates than they had seen in months, leading to a bumper month of corporate bond issuance.

The result of this is that the traditional 60% equity and 40% bonds portfolio saw its best November since 1991, returning 9.6% in dollar terms. This highlights the benefit of staying invested in markets, as if you we're to have missed out on last month's returns then this will have compromised your returns for the overall year.

And what does the future hold?

Looking ahead we continue to expect a supportive environment for financial markets.

The recent increase in small cap (or unloved) companies means equity markets are trading at (relatively) more attractive valuations which provides an opportunity for investors, but also reduces the risk that the small minority of companies (the Magnificent 7) which have contributed to most of the recent performance, will fall in price. Similarly with bonds the combination of robust corporate balance sheets and that companies do not need to immediately refinance their debt (and in doing so increase their ongoing costs) means the outlook for bonds is also positive and offer investors an attractive level of income.

As a final word, while recent market developments have been encouraging, reasons for caution remain. As noted in the paragraph comparing interest rate expectations internationally, in Europe the expectations for cuts are driven in large part by expectations of deteriorating economic growth. While the US is expected to be stronger there is still the expectation that growth will slow and as a result, we continue to favour holding a diversified portfolio which provides diversification not just by investing in several different countries but also investing across multiple asset classes (equities and bonds) and different industries.

Arrange a free initial consultation

Note: This Market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Additionally, past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.