Skip to main content

Skip to main content

May returns encourage investors to stay not go away

‘Sell in May and Go Away’ is a popularised investing strategy which recommends investors sell on the 1st May and re-buy on the 31st October.

The strategy has gone through various iterations but it is believed this was coined in 18th century Britain when aristocrats and bankers left the City for their summer holidays only to return on the day of the St. Leger Stakes.

Arrange your free initial consultation

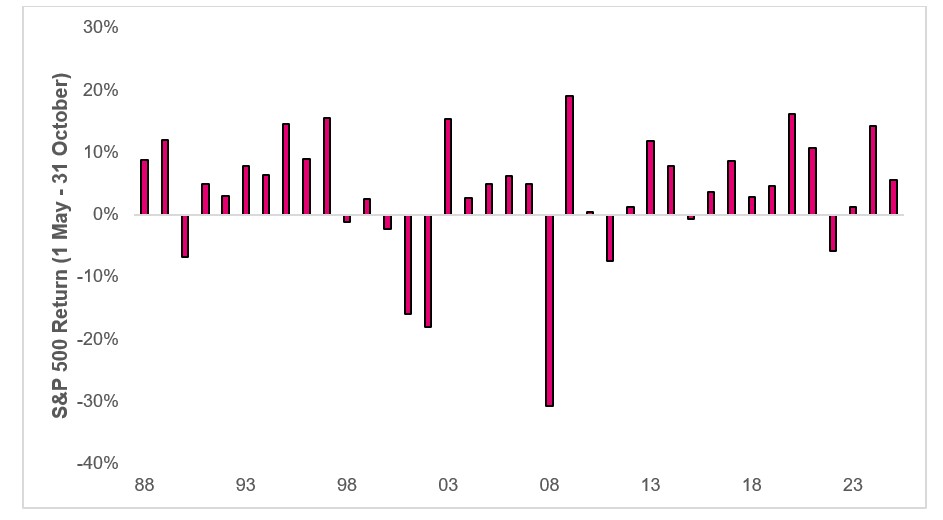

The idea underpinning the strategy is that market liquidity tends to decline during the summer months, making markets more vulnerable to volatility. However, empirical evidence is mixed, as the S&P 500 has posted negative returns in only nine summers since 1988 (see Figure 1.).

Figure 1. Returns of the S&P 500 between 1 May – 31 October (Source: FE Analytics, April 2025)

Figure 1. Returns of the S&P 500 between 1 May – 31 October (Source: FE Analytics, April 2025)

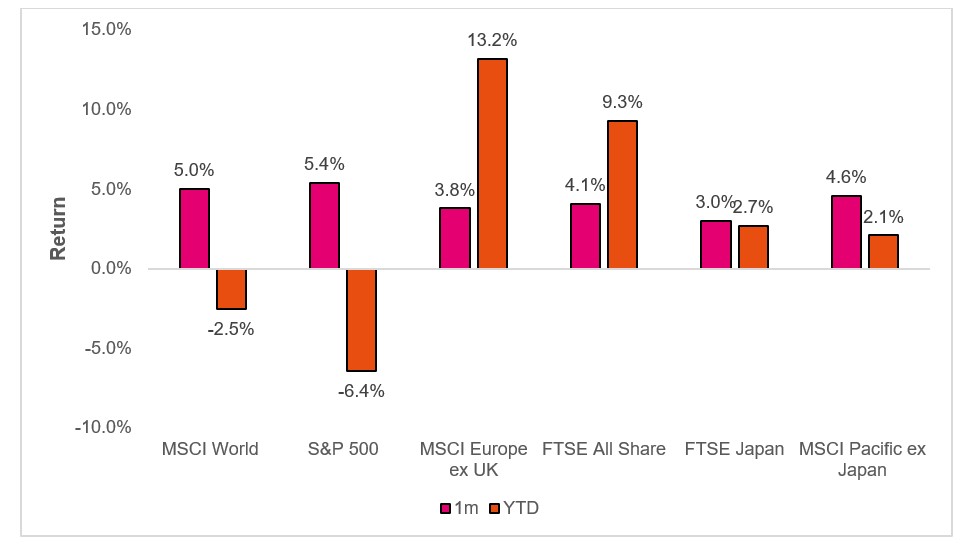

Had investors followed this strategy last month, they would have missed out on a 5.4% gain in the S&P 500. This was part of a broader rally in risk assets, driven by news of a trade deal between the US and China, which reduced recession fears and eased some of the uncertainty in markets (see Figure 2).

Figure 2. Regional equity returns (Source: FE Analytics, May 2025).

US equities in particular were supported by another round of strong earnings. US corporates defied expectations with year-on-year earnings growing 13% in Q1 and in a sense of déjà vu the Magnificent 7 led the way growing earnings 28%. Meanwhile the broader US equity market (the ‘S&P 493’) grew earnings 9.4% which is a marked increase from the 4.8% that was forecasted back in March.

It’s important to note that Q1 earnings were reported before the full impact of tariff-related uncertainty was felt in the markets. Although tariffs were mentioned in 89% of US earnings reports, we’ll need to wait for the next quarter’s results to properly assess their effect. That said, the current level of earnings growth indicates that US corporates entered this period from a position of strength.

Outside of the US we saw UK equities post another strong month with the FTSE All Share index up 4.1%. This follows improving economic data and the Bank of England cutting interest rates by 0.25% to 4.25%. Meanwhile European equities added to their strong year-to-date returns as cyclical sectors like technology rallied on falling trade tensions and the prospect of the German infrastructure bill which is likely to have benefits for broader Europe.

Whilst equities performed well it was another challenging period for bond investors as concerns around government fiscal largesse and spending policies were back in the spotlight.

The announcement of the ‘Big Beautiful Bill’ in the US which can be best described as ‘Front loaded tax cuts and back loaded spending cuts’ saw US Treasury yields rise with the 10yr yield climbing above 4.60%.

The US administration’s shift from fiscal prudence to growing out of debt is a laudable goal but history is not on their side and developed countries across the world have struggled to generate economic growth without the need of vast stimulus programs.

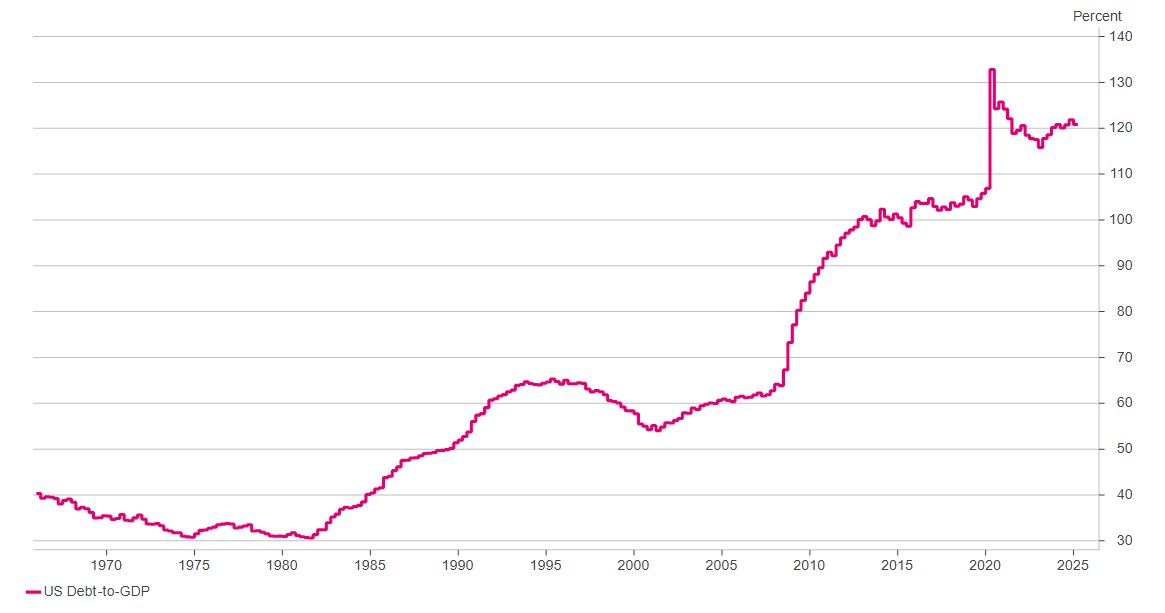

Since 2020 the US’s debt-to-GDP has grown from 100% to over 120%. In other words the level of debt in the economy is growing quicker than economic growth (see Figure 3.).

Figure 3. US Debt-to-GDP (Source: Macrobond, May 2025).

We also saw Moody’s downgrade the US’s credit rating (Aaa to Aa1) which whilst a largely symbolic move illustrates the level of pessimism there is towards the US’s current fiscal position.

Credit markets were more resilient as improving risk appetite saw High Yield Bonds outperform Investment Grade bonds. Investment grade bonds were broadly flat on the month, however we saw a continued narrowing in high yield spreads (the compensation one gets for investing in bonds with credit risk) with US High Yield spreads falling to 3.3% - the index was trading at 4.6% back in early April.

Looking ahead, attention will now turn to the 9th July when the pause on the reciprocal tariffs will end. We expect countries to try and lock in a trade deal with the US between now and early July. This should provide further clarity for investors and allow for the impact of tariffs to be accounted for.

In summary investors were rewarded for taking risk in May, as strong equity gains driven by solid earnings and easing trade tensions outpaced concerns over fiscal policy and rising yields. While risks remain, recent market resilience highlights the benefit of staying invested through uncertainty.

As ever, if you’ve any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO adviser team.

Arrange your free initial consultation

The information in this article is correct as at 13/06/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.