Skip to main content

Skip to main content

Stealth tax raid on your wealth

Although many could be forgiven for believing the tax year 23/24 has been a fairly quiet year from a tax perspective, the simple act of freezing tax brackets and freezing or reducing allowances means these are likely to be the biggest tax raising measures since the 1970s. This statement continues to ring true even after taking into account the announcements made in the Autumn Statement back in November. As we now move closer to the Budget, due on the 6th March, with the current government looking at all options to keep them in power in an election year, one thing is for sure, we’re all feeling the effects of stealth taxes. So, will this change?

Arrange your free initial consultation

Stealth tax refers to government policies that increase tax revenue without directly or explicitly labelling them as tax hikes. These taxes often take the form of adjustments to existing taxes and allowances, fees, or other government charges, rather than the introduction of new higher taxes.

The term stealth taxes implies that these changes are designed to be less noticeable to the general public. Bluntly, the Government may look to introduce these less obvious changes, or indeed make no changes at all, so as to avoid criticism, potentially relying on blind siding taxpayers.

However, some would argue that such measures can be necessary for funding government programs and services or indeed paying back the mountain of debt the UK is now faced with, while avoiding public backlash. One thing is certain however, there are currently many different types of stealth taxes, which means few people are immune from paying much more tax now and potentially in the coming years. Even those not normally concerned are starting to sit up and notice; with the impact of fiscal drag on their finances, it’s hard not to feel the pinch.

Latest figures from HM Revenue and Customs (HMRC) show that total tax receipts for April 2023 to November 2023 are £515.9 billion, which is £24.0 billion higher than the same period last year.

In ‘normal’ times the Government has typically pursued a policy to increase tax allowances with the rate of inflation. However back in in 2021 the Government announced plans to freeze allowances and thresholds until 2026. This was later extended to 2028. A clever and rewarding move by the Government. The impact of this is staggering and continues to grow, for example, according to the BBC, simply freezing Income Tax bands until 2028 will create an additional 3.2 million new taxpayers and mean 2.6 million more people will pay higher rate tax. In fact, the Institute for Fiscal studies has stated that by 2027/28 one in eight nurses and one in four teachers will pay higher rate tax.

Even pensioners aren’t immune. According to HMRC an additional 800,000 pensioners will be paying income tax this year due to higher inflation pushing up state pension, which will take many of them over the frozen personal allowance.

Added to this, in the spring Budget early in 2023, the Chancellor announced a reduction in the amount you could earn before paying additional rate tax at 45%. Previously you would have breached the additional rate tax band once your earnings exceeded £150,000 per year, however, from April 2023 it was cut to £125,000, dragging many more people into the additional rate tax net.

Impacts of the Autumn Statement 2023

Following the Autumn Statement delivered by the Chancellor, Jeremy Hunt, in November last year, it should be noted that despite some changes designed to give the public back some money in their pocket, by reducing National Insurance payments, stealth taxes continue to be ever present. My colleague Alex Shields wrote a great article summarising the changes outlined in the Autumn Statement.

The first area of note is the changes to National Insurance (NI) payments - as a result of higher inflation, higher interest rates and frozen tax bands, the Office for Budget Responsibility (OBR) states “Living standards, as measured by real household disposable income per person, are forecast to be 3.5 per cent lower in 2024-25 than their pre-pandemic level.” With this in mind even the 2% reduction for employee NI contributions only results in a £754 p.a. for anyone earning over £50,270, which is a relatively small amount given the increasing day to day costs driven by inflation over the last 12-18 months.

What Stealth Taxes are the biggest earners?

Income Tax Freeze

The stealth tax which is arguably the most prominent and takes in the largest receipts are the income tax bands, which are frozen until 2028. Given that on average UK wages increase year on year, and even more so while inflation rocketed, individuals have been moving up the income tax bands, potentially without realising, just by receiving routine pay increases each year. Some 5.59 million people in the UK currently pay higher rate tax, official HMRC figures show, with an additional 310,000 dragged into it in the year 2022 alone. Over the last few years inflation and interest rates have been in a constant battle in order to try and bring inflation back to its 2% target, while wage inflation had been steadily increasing in the background. Although inflation had been falling in recent months, this month saw a surprise small uptick from 3.90% to 4%, meaning it’s stickier than expected and certainly well above the target 2%, so it’s little wonder that demand from the UK labour force for higher wages continues to increase. This, in tandem, drives up the impact of this particular stealth tax – as wages increase over the frozen income tax bands.

Furthermore, as mentioned above, pensioners received a boost as the Government remained committed to the State Pension triple lock; it was announced in the Autumn Statement 2023 that the full State Pension will be increasing to £11,501 per annum from April 2024. But, this in turn leads to many pensioners having to pay more tax than the year before given the freeze on income tax bands. In fact, those on low pension incomes are in risk of paying tax for the first time as they breach the personal allowance of £12,570. This could squeeze the finances of those pensioners on lower incomes more than they were previously, while also pushing others into a higher tax bracket – pointing to the benefit of ongoing financial planning.

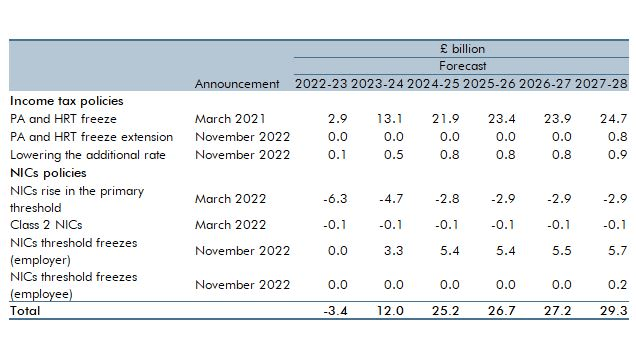

Latest costings of personal tax threshold measures

Source: Office for Budget Responsibility

Savings Allowance Freeze

Another potential stealth tax to be aware of is the tax on savings interest. A basic rate taxpayer can earn up to £1,000 interest outside an ISA without facing a tax bill. This is known as your Personal Savings Allowance (PSA). The allowance is £500 for those paying higher rate tax, and additional rate taxpayers have no allowance at all. Due to very low interest rates in previous years, this tax allowance has been all but forgotten about, with the majority of savers accumulating savings interest tax free.

However, given the Bank of England base rate rose 14 times consecutively from December 2021 in an attempt to combat inflation, cash savings rates became much more attractive as a result (see Savings Champion best buys). Many savers will now accrue significant taxable interest, which in turn takes them over their Personal Savings Allowance and they will therefore need to pay tax.

To put this into context, back in December 2021 a saver could deposit over £133,000 in a best buy account before breaching the basic rate taxpayers PSA. Fast forward to October 2023, when interest rates were peaking, if you saved in the top easy access account, you would breach the PSA on a balance of just over £19,000.

In fact, it’s been reported that the number of people paying tax on their savings income in the 2022/23 tax year has almost doubled to 1.77 million compared to the 0.97 million people the year before. And the amount collected has more than doubled from £1.2 billion to £3.4 billion.

Inheritance Tax

In a similar light to the Income Tax freeze, the Inheritance Tax (IHT) nil rate band (NRB) and residence NRB have also been frozen until 2028. Worst still, however, the current NRB hasn’t changed since 2009, so has remained the same for 14 years. As it stands for the current tax year 2023/24, you will have to pay Inheritance Tax if the value of your estate exceeds £325,000. Anything below this threshold is tax free. Anything above this threshold would be charged at 40%. Those who are passing down their main home to direct descendants are also entitled to an additional allowance of £175,000, known as the residence nil rate band (RNRB), however this allowance actually starts to be withdrawn where the value of the estate exceeds the £2 million taper threshold.

Due to the rising rate of inflation coupled with increasing property values across the UK, the freeze essentially means that a greater number of people will cross the inheritance tax threshold each year, as the value of their total assets have increased, whilst the allowance has remained the same. In the 22/23 tax year a record £7.1 billion in IHT receipts was raised, which was up £1 billion from the previous tax year. With freezing this allowance and estates growing, IHT receipts are expected to increase consistently. In fact, figures from HM Revenue & Customs (HMRC) show a record breaking £2.6bn of inheritance tax receipts were collected in just the 13 weeks between April and July 2023.

The latest figures from HMRC show Inheritance Tax receipts for April 2023 to November 2023 were £5.2 billion, which is £0.4 billion higher than the same period last year.

Why should there be more awareness of these stealth taxes?

Given the current economic climate, it’s wise to ensure your hard-earned money, whether that’s income, investments or savings, are working for you in the most tax efficient way possible. These stealth taxes, if left unattended, will drag on your accumulated and accumulating wealth. The good news is, there are simple ways of mitigating the impact of stealth taxes by being aware of and using the allowances available to you (but be conscious not to creep over them). Moreover, ensuring you are investing, saving, and contributing to tax efficient savings and investments with tax free wrappers will also help to mitigate some of these stealth taxes.

A few examples include:

Use your ISA Allowance

- Saving money into an ISA (the most common being Stocks and Shares or Cash); everyone gets a £20,000 per tax year allowance and any growth within an ISA is totally tax free.

Fund your pension

- If you find yourself entering a new tax bracket, whether that is higher or additional rate, by funding a pension you will receive tax relief at your marginal rate, so are effectively given a tax boost by contributing. For example, a basic rate taxpayer would receive tax relief at 20%, a higher rate by 40% and additional rate by 45%.

- Added to the fact, by contributing to a pension you could even reduce your income as the money is taken at source, so therefore you could change the income tax bracket you fall into.

Watch out for the 60% tax trap

If you earn over £100,000 you begin to lose your personal allowance and could find yourself effectively paying 60% income tax as you lose it – this makes pension funding in this bracket especially attractive.

High Income Child Benefit tax charge

- For parents claiming child benefit, if you or your partner have an income of more than £50,000 a tax charge applies. One way you may avoid the tax charge is if a personal pension contribution is made. If the contribution is enough to reduce your income below £50,000, the High Income Child Benefit tax charge will be avoided.

Use allowances before they are cut

- From 6th April 2024 both the Capital Gains Tax and Dividend Allowance are being halved, £6,000 to £3,000 and £1,000 to £500 respectively.

Whatever side you’re on, working through the political landscape right now can be hard. Therefore, having regular financial planning sessions with a professional independent financial adviser could help mitigate against many of the stealth taxes, so why not get in touch and see how we can help you.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

This article is also based upon our understanding of current law, HM Revenue and Custom's practice, tax rates and exemptions which are subject to change.

Savings Champion and their associated services are not regulated by the Financial Conduct Authority (FCA).

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.