Skip to main content

Skip to main content

What is a stakeholder pension?

What are stakeholder pensions and could they be the right fit for you?

Pensions are a tax-efficient way of saving money in preparation for retirement and it is important to choose the right pension fund for you. However, with different types of pension schemes available, choosing the right one could be confusing, especially if you don’t know what you’re being offered. Stakeholder pensions are often overlooked, and whilst they don’t differ greatly from personal pensions, there are some unique aspects to be aware of as they could be more suitable for what you’re looking for, than you might think.

With the ability to make lower and more flexible contributions into your pension fund, capped pension charges and default investments for those not sure where best to invest their money, stakeholder pensions are ideal for new savers or people looking to contribute smaller amounts each month to their retirement fund.

Key features of stakeholder schemes include:

- Ability to make lower minimum contributions.

- Added flexibility offering the ability to stop and start contributions when you wish.

- Capped annual charges of 1.5% for the first 10 years and then only 1% every year thereafter.

- Transferring from a stakeholder pension to any other pension scheme is offered at no extra cost.

- A default investment fund is offered if you don’t want to choose where to invest your pension.

- A lifestyling approach is offered so that as retirement approaches you can take lower risks with your pension investments.

What is a stakeholder pension?

A stakeholder pension is a form of defined contribution pension (the most common type of pension with the pot value based on contributions made), aiming to make saving for retirement more accessible for everyone. Stakeholder pensions must meet specific Government requirements, for example limits on charges and flexible contributions as mentioned above. They offer people the ability to invest as little as £20 per month into a retirement fund, compared to other schemes such as workplace pensions that have an 8% minimum contribution (in most cases 3% of this will come from your employer) set by the government.

Another beneficial aspect to stakeholder pensions is that when you select a pension provider, they must offer a default option if you’re unsure of the funds you want to invest in. This can be particularly useful for new pension savers, if you don’t have much knowledge on what makes a worthwhile investment fund or you’re simply not sure where to start.

You can also set up a children’s stakeholder pension. This is where you open a pension fund in your child’s name and the money remains invested until they reach retirement age. A big appeal to doing this is that you still gain tax relief on all investments that are made into the child’s stakeholder pension, so your child reaps the benefits of tax relief even before they start contributing themselves.

Stakeholder pensions are often personal pensions rather than those offered through a workplace scheme, but some workplaces do offer them, so make sure you check with your employer if a stakeholder pension is an available option for you to invest in, should you wish too.

Is a stakeholder pension a personal pension?

No, whilst a stakeholder pension can be defined as a form of personal pension, there are important differences which mean they are classed as separate pension schemes. See the key features above.

How does a stakeholder pension work?

All forms of defined contribution pensions are built up from your own and/or your employers' contributions, with tax relief on all contributions at your marginal rate. This is then managed by a pension provider either of your choice, or one chosen for you through your employer, until your retirement approaches. The amount in your stakeholder pension will depend on how much is paid into the fund over the years and how well your investments do over time.

Stakeholder pensions are not allowed to charge more than 1.5% of the value of your pension fund annually for the first 10 years and then no more than 1% after that, making them a low-cost form of pension.

Unlike other schemes, stakeholder pensions do not require you to pay set payments into the fund. So, if one month you want to take a break from adding to your pension pot and save that little extra in disposable income, that choice is all yours. You can make monthly contributions at a fixed amount each month, or if you value flexibility then you have the ability to make contributions on an ad hoc basis, which could make a stakeholder pension the right fit for you.

What is the best stakeholder pension?

Essentially, there is only one type of stakeholder pension, offered by different providers. You want to make sure that once you’ve decided upon a stakeholder pension, that you’re getting the best provider possible, and that they’re going to provide you with the lowest fees, good investment options and the best service.

Stakeholder pensions are particularly well tailored for self-employed and low-income workers due to low contributions, lower fees and flexibility of contributions. So, it may be wise to check your provider gives you the best of what you need from the list of key benefits detailed above.

Not all pension providers offer stakeholder schemes, so it’s important to explore the market for the right provider if a stakeholder pension is what you’re looking for. To understand more about who the right provider for you is, you can speak to one of our advisers who can direct you, according to your pension needs, with a free consultation.

Do stakeholder pensions offer drawdown?

It is not guaranteed that all stakeholder pensions come with the drawdown strategy as an option. The best thing to do is check with the pension provider before you go ahead.

A pension drawdown is an alternative method of accessing your pension funds without using the traditional annuities method. The annuity method changes your pension into an annual income providing you with a regular income for life. Whereas with drawdown, you don’t have to withdraw your entire pension fund, you can take out the amount you wish at a certain time and leave the rest of the funds in your pension pot invested to hopefully grow more.

You are normally able to access up to 25% of your pension funds as tax-free cash, which you can withdraw in one lump-sum and then leave the rest of your funds invested to draw flexibly as and when you wish. After the initial 25% is taken as tax free cash, all other funds are taxable, so be aware of this if you’re planning to withdraw large amounts at a time. You don’t want to accidentally become a higher-tax payer.

It’s always important to know that, because of the nature of pension investments, your assets stand the chance of falling in value as well as rising.

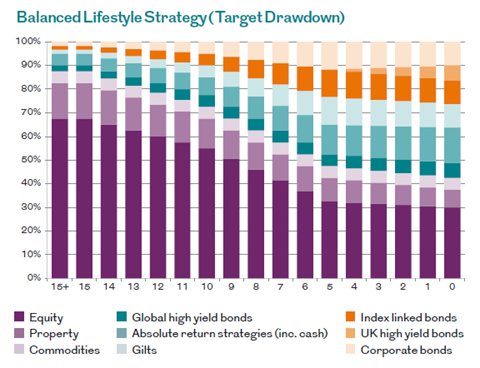

What is lifestyling in pensions?

Lifestyling is a strategy used to reduce the risk of your pension investment as you approach retirement age by shifting your funds into lower risk and less volatile investments. You will have a specific retirement age in mind that this strategy considers. Approximately 10 years before you reach this age your pension funds will start to change into something of lower risk, guaranteeing their safety as retirement approaches.

Lifestyling provides investors with the ability to automatically switch their pension savings into another fund. They may deliver lower returns but a lifestyling strategy importantly reduces the threat of your investments taking a hit from stock market changes. It also allows for the funds in your pension pot to be aligned with your plans for using them, paving a clear pathway for your retirement whilst protecting the savings that will get you there.

The graphic below shows how lifestyling operates the closer your retirement gets. It provides a 15-year scale where you can see as you approach retirement your investment gradually changes from high to lower risk.

Fig. 1: https://adviser.royallondon.com/investment/our-investment-options/royal-london-investment-default/

Advantages of Lifestyling

- Can help reduce the likelihood of short-term decline of your pension value as you head towards retirement.

- Flexibility means you have the option to move your pension funds out of the lifestyle when you wish and be able to use them.

- Good for those who don’t want to make investment decisions

Disadvantages of Lifestyling

- It is based on a long-term expectation of how the invested funds will perform, this fixed strategy does not account for changes that may happen to economic and market conditions.

- In a high inflation environment like we’re currently seeing, your pension would have to grow more than the inflation rate to keep up with the cost of living, which with lower risk investments could prove difficult. But high inflation is usually a short-term impact, so if you’re planning on investing long—term the results shouldn’t have lasting effect on your investments.

- You cannot influence when these changes take place as they are automatic, at a time where you want your pension to be growing as much as possible reducing the risk in the last 10 years might not be suitable.

- One size does not fit all, the strategy is designed to de risk your pension as you get towards retirement as it assumes you will be taking an annuity.

- It is reliant on your actual retirement date matching the pension retirement date

- Does not consider your personal circumstances such as when you might be drawing on the pension.

How we can help

If you would like to know more about if a stakeholder pension is right for you, or any other guidance about pensions and planning for your retirement, why not get in touch with one of our expert financial advisers to see if we can help, with a free initial consultation.

Note: The Financial Conduct Authority does not regulate Tax Advice or Estate Planning. A pension is a long-term investment, the value of investments can fall as well as rise. You may not get back what you invest. Your eventual income may depend on the size of the fund at retirement, future interest rates and tax legislation.