Skip to main content

Skip to main content

HMRC responds to surge in pension withdrawals with cautionary warning

HM Revenue & Customs (HMRC) has warned savers not to act impulsively with pension withdrawals ahead of the upcoming November Budget.

This message is aimed at those savers who might look to take advantage of the 30-day cooling-off periods to request withdrawals but with the option of putting them back again within 30 days, should the Budget leave the current rules unchanged.

Now HMRC have said pensioners who took out their lump sum after December 5 2024 and put the money back in, within the 30 days, could be pursued by the tax man with each cash reviewed on a "case-by-case" basis.

They clarified that once a tax-free lump sum has been paid, it cannot be reversed, even if the cancellation period is still open.

In its latest update, HMRC has reiterated that these 30-day windows do not provide any tax exemptions, meaning those who took and then returned their tax-free lump sums since December 5 last year are potentially facing charges of 55% in most cases, and up to 70% in others.

“Once lump sums are paid, the associated tax consequences (including the use of the individual’s lump sum allowance and lump sum death benefit allowance) cannot be undone, even if the payment is returned or cancellation rights are exercised” said HMRC.

62% rise in those accessing tax free cash lump sum?

Most pension savers have the option of withdrawing up to 25% of their pension, tax free. Many pensioners choose to take a lump sum to clear mortgages or help children with university costs, but after reports last year that Chancellor Rachel Reeves was considering reducing the tax-free allowance to £100,000, many savers rushed to access their money early, with tax-free pension lump sum withdrawals rising significantly amid fears this allowance could be reduced or scrapped completely.

Figures from the Financial Conduct Authority (FCA) show pension withdrawals rose by nearly £20 billion in the 2024/25 tax year compared with the previous year.

The amount of money withdrawn from pensions jumped by almost 36% in 2024/25, with savers taking out £70.9bn compared to £52.2bn the previous year, according to the FCA’s latest Retirement Income Market Data. Of this, £18.3bn was tax-free cash, an increase of 62% on the £11.3bn the previous year.

The latest data showed that just shy of one million pension plans (961,575) were accessed for the first time during the year, up 8.6% on the amount accessed in 2023/24.

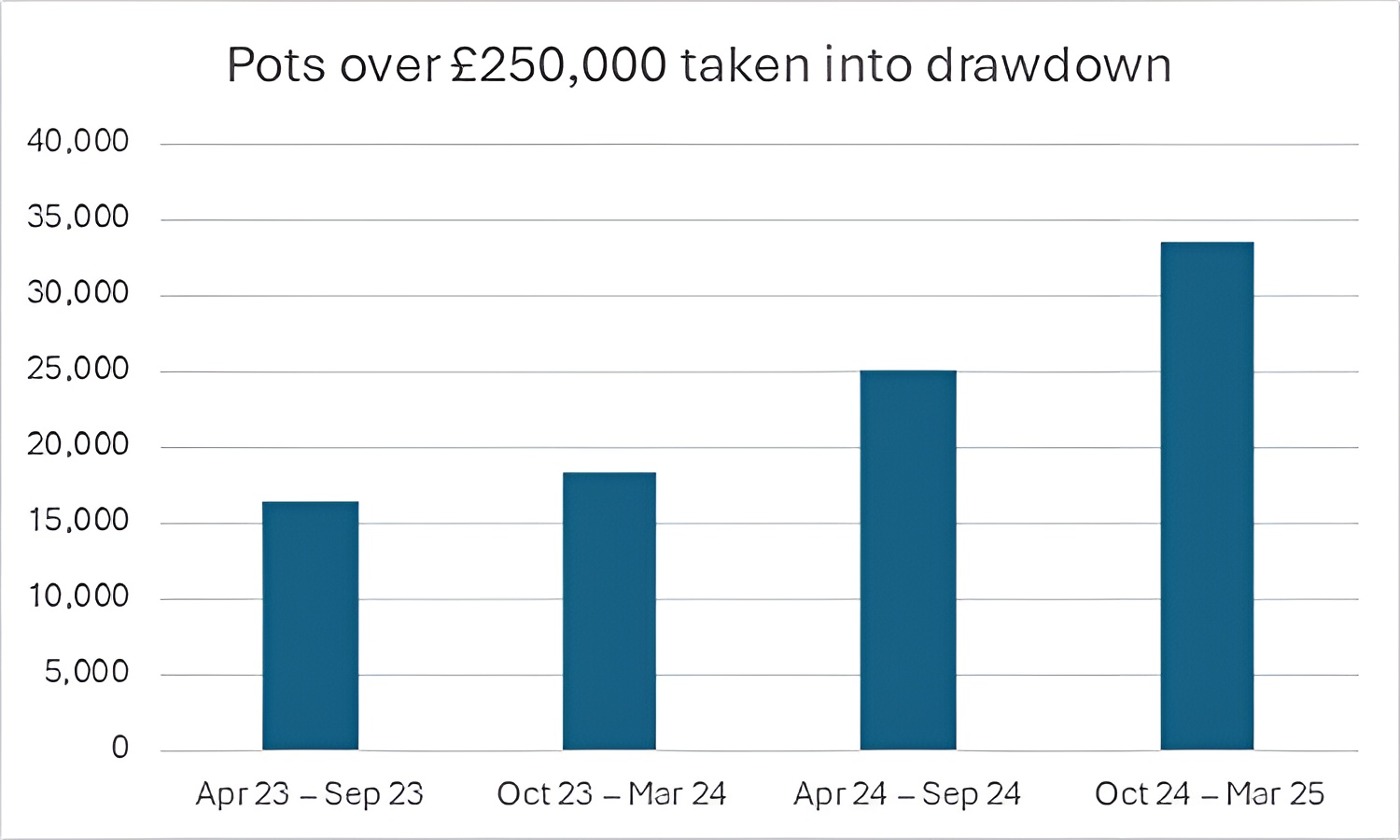

Figure 1: Pots over £250k taken into drawdown, Source: FCA, 2025

The FCA data also showed that the number of pensions being accessed without regulated advice had grown, with only 30.6% of pension plans accessed for the first time in 2024/25 being taken with regulated advice, slightly down from 30.9% the previous year.

If you’re concerned about the Budget or simply want to discuss the best way to plan for your retirement, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our qualified and regulated financial advisers to find out how we might be able to help you.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.