Skip to main content

Skip to main content

The general election - what does the result mean for investors and savers?

And the results are in….

Now the dust has settled a little following a landslide win by the Conservatives, what does this actually mean for investors and savers?

The Tories have confirmed that there will be a Budget within the next 100 days, so probably February or March this year and of course the devil will be in the detail.

But just what could the manifesto promises mean to your finances?

Below is a summary of some of the Conservative manifesto pledges made before the election.

Taxation

- According to the manifesto, there should be no income tax, VAT or National Insurance rises over the five year parliament.

- And the threshold at which worker’s pay National Insurance is set to rise from £8,632 to £9,500 in 2020/21 – this would be worth about £85 a year for those earning £9,500 a year or over.

- A review (and reform) of entrepreneurs’ relief is likely, so look to see if your Enterprise Investment Scheme (EIS) or other business property relief holdings are affected.

- Regarding Capital Gains Tax (CGT), it is likely that there will be a continuation of the previously announced tightening of private residence relief rules and earlier payment rules (30 days).

Pensioners

- The state pension is to see a 3.90% boost – the largest increase since 2012 – with the full, new state pension set to rise from £168.60 a week to £175.20.

- Pension triple lock to remain – meaning the state pension will rise each year by the higher of, inflation, earnings or 2.50%

- Pension tax relief – despite being a potential target area for successive Governments, it’s unlikely that this Government will target pension contributions in the short term at least.

- Promise that no-one should have to sell their home to meet care costs.

Property

- Introduce a stamp duty land tax surcharge of 3% for non-residents purchasing UK residential property

Other

- Minimum wage is set to rise to £10.50 an hour within the next five years – up from its current level for the over 25s of £8.21

In the meantime, what should investors do?

Should I be selling and waiting for the dust to settle – or investing more?

The press is dubbing it the ‘Boris bounce’, as the UK stock markets rallied strongly after the result and since 12th December, at the time of writing, the FTSE 100 is up over 3% and FTSE 250 is up nearly 6% .

The FTSE 100 saw its best day in over a year on 16th December, rising by 2.25% – adding more than £80 billion to the value of Britain’s biggest companies.

Of course, we now have Brexit to deal with.

It’s almost certain that the UK will leave the EU by the end of January and The Bank of England Governor, Mark Carney, has said that the chance of a No Deal Brexit has now receded as the Prime Minister will be able to pass his withdrawal agreement bill in the House of Commons, unchallenged.

That said, if the post-Brexit transition period is not extended beyond 31st December 2020, that could increase the possibility of No Deal once again – and bring with it more economic uncertainty and market turmoil.

So, although the result of the election has removed some uncertainty, Brexit still poses many questions which could mean further volatility for investors. And rather than making the common mistake of buying and selling at the wrong time, for a less bumpy ride maintaining a good spread of assets and investments should mean that you can focus on the upcoming changes following Brexit, rather than worrying about your investment portfolio.

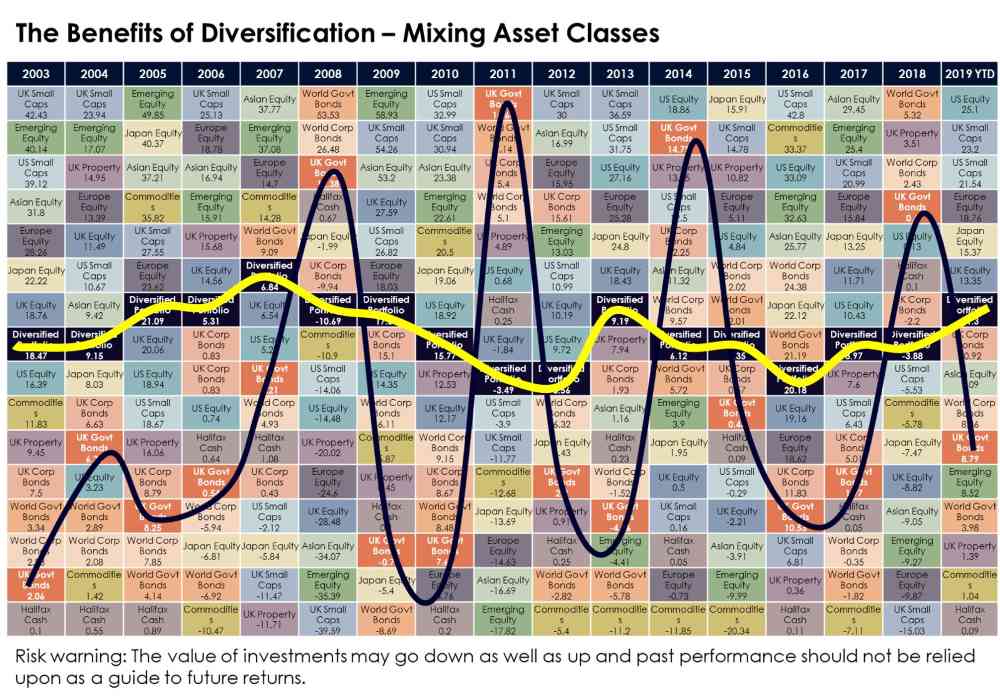

The chart below shows just how volatile different asset classes can be - for example, orange is UK Government Bonds, pale blue is UK Small Caps.

What it illustrates is that what does well one year has the potential to do really badly the next.

But with the right investment portfolio you can make your investment journey less dramatic.

The yellow line in the middle of the chart illustrates a diversified portfolio and shows that a good mix of assets can take away much of the volatility.

What about interest rates?

At the last Monetary Policy Committee (MPC) meeting, the base rate was once more kept at 0.75% with a majority vote of 7-2. For the second meeting in a row, two of the nine MPC Committee voted for an interest rate cut.

That said, it is interesting to see that 10 year gilt yields have been increasing recently – which could indicate a longer term increase in the base rate.

All of this aside, as has been the case for a long time, and especially in the run up to Brexit, no-one can be sure as to what the Bank of England will do with the base rate in the short term, never mind the longer term.

But a number of economic indicators point towards a base rate cut being on the cards at the moment, rather than a rise. For example, if inflation continues to remain lower than the official target, the rate could be cut to try and boost economic growth (which is also in the doldrums) and inflation.

Take advantage of allowances, while we still have them.

Although many people wait until the last minute to use pension and ISA allowances, it could be prudent to get this job done sooner rather than later.

Although there were no specific mentions about the fate of these particular allowances, remember that the tax year end won’t change, so if you plan to use them, why wait?

If you have any concerns, make sure you get in contact with your adviser. If you are not yet a client of The Private Office, you are still welcome to call and speak to someone so that we can see if we can help.

The contents of this article are for information purposes only and do not constitute individual advice.

The value of an investment and the income from it could go down as well as up. The return at the end of the period is not guaranteed and you may get back less than you originally invested.