Skip to main content

Skip to main content

What happens to my pensions after death?

The introduction of what is commonly referred to as ‘Pension Freedoms’ on 6th April 2015 not only changed the way you can access your pension pot if you have built up a retirement fund in a Private (defined contribution) Pension Plan but also how it can pass to your beneficiaries.

Important: If you are a member of a defined benefit (final salary) scheme the pension freedom rules will not apply to you.

If you would like to understand more about what benefits your scheme will provide when you die please read our separate article on defined benefit pensions or speak to a TPO adviser.

Arrange a free initial consultation![]()

Who gets my pension after death?

Collectively referred to as beneficiaries, these can be a Dependent(s), a Nominee(s) or a Successor.

| Dependent | Nominee | Successor |

|---|---|---|

Your widow(er) or civil partner; | You, as the member, can nominate any individual who does not fit the criteria to be a dependent. | Any individual nominated by the dependant or a nominee to receive the remaining pension value after they die. |

| The pension provider will pay out to your dependent(s) in the first instance, unless you create a nominee. | You can nominate a charity provided you have no dependents; A scheme administrator can nominate if you have no dependents. | Each individual who will receive the remaining pension value after the first dependent or nominee is referred to as a successor. |

If you do not know who your beneficiary is, you should contact your pension provider to check. If you don't have a named beneficiary or you would like to change who would currently receive your pension death benefits when you die; you can get in touch with your provider to request a nomination form or expression of wish form.

What is a beneficiary?

A beneficiary can be one of the following: A Dependent such as a widow(er) or civil partner, any children under age 23 or any person financially dependent on you. A Nominee – this can be an individual or a charity. A Successor – is an individual nominated by the dependant or nominee to receive the remaining pension value after they die.

What happens to pension beneficiaries after death?

Pension death benefits can be passed to your beneficiary in a number of ways:

- Lump sum payment: This is a single payment which will fully extinguish the pension fund

- Lifetime annuity: Your beneficiary can choose to buy an annuity which provides a guaranteed income for life

- Dependant’s or Nominee’s drawdown (Beneficiary Drawdown): Your beneficiary can opt to draw an income directly from your pension fund. This differs from the Lifetime Annuity option as it allows them to vary the amount of income they receive and the frequency of the payments. The trade-off is that the income is not guaranteed as the pension fund remains invested.

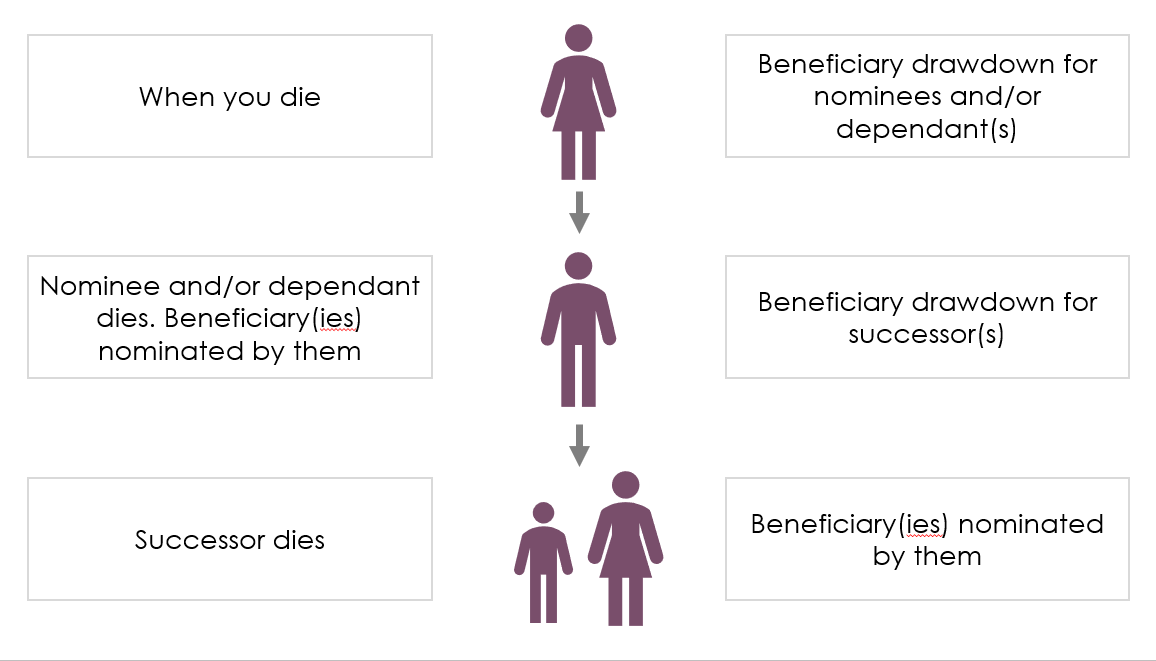

More about beneficiary drawdown

There is no limit to how many times a beneficiary drawdown plan can be passed on to a subsequent beneficiary following your death.

The cycle below will continue until the pension funds are exhausted. This makes such arrangements very useful as a means of passing wealth to the next generation in a very tax efficient manner.

Important Note: If you are survived by a dependant, flexi-access drawdown can only be offered to a non-dependant beneficiary if you name them on the nomination form.

Do pension funds pay taxes?

The age at which you die determines how your pension fund will be taxed when it passes to your dependants or nominated beneficiary.

Generally, if you die before your 75th birthday your pension fund will pass to your nominated beneficiary free of income tax and they will be able to take a withdrawal (either as a lump sum or a regular income) without paying tax.

We say generally because there is a condition which needs to be met for the payments to be free of income tax – the pension fund has to be paid to your beneficiaries within two years of your death.

This can be confusing as it does not mean that they have to take all of the money out of your pension.

It simply means that your beneficiary needs to have told your pension provider how they want to access the money and the pension provider needs to have made payment – either as a lump sum payment or by setting up a beneficiary drawdown arrangement. You can read more about drawdown here.

If you die on or after your 75th birthday your beneficiary can still choose to take the pension fund as a lump sum or enter a beneficiary’s drawdown arrangement but they will pay income tax on any money they withdraw.

Until April 2027 most pension plans are free from inheritance tax (on death at any age). For the fund to be free of inheritance tax any nomination you have made needs to be revocable – this means that it cannot be a binding instruction.

Some of your pension fund may also be subject to inheritance tax if you have moved money between pension plans in the two years before your death at a time when you knew you were in poor health and may have a reduced life expectancy.

From April 2027, most pension funds remaining when you die will be included in your estate and subject to inheritance tax when you die unless they are passing to a surviving spouse. The final details of how inheritance tax will be applied to your pension fund on death after April 2027 are expected shortly.

If you would like to know more about this particular issue please see our separate article about inheritance tax on pensions

How does the lump sum and death benefit allowance work?

Following the abolition of the Lifetime Allowance in April 2024, there are no limits to the amount of pension fund you can build up in a tax-advantaged environment but there are limits on the amount that can be paid out as a tax free lump sum to your beneficiaries when you die.

For most individuals this limit is £1,073,100 and any lump sums you received during your lifetime have to be deduced from this allowance.

If you die before your 75th birthday, your beneficiaries will have the option to receive their benefits as a lump sum or they can choose to keep their inheritance in a pension and designate it as a beneficiary drawdown arrangement.

If they choose a beneficiary drawdown arrangement they will pay no income tax on any withdrawals they make regardless of the total value of your pension fund when you died.

If they choose to receive their inheritance as a lump sum instead then the total lump sum benefits paid to all beneficiaries will be assessed against your remaining Lump Sum and Death Benefit Allowance.

Any lump sum payments made which exceed the available remaining allowance will be subject to income tax at the beneficiaries marginal rate of income tax.

A word of caution

The options that will be available to your beneficiary are very much dependent on:

- The type of pension plan you have: Retirement Annuity Contracts and Section 32 Buyout plans typically have less flexibility when compared to a Personal Pension or a Self-Invested Personal Pension (SIPP)

- Your pension provider: Different pension products have different rules and some contracts, such as Stakeholder Pensions, may not provide the full range of freedom options for your beneficiary

- The age of your pension: Older pensions will not necessarily be able to provide the same freedom options that a more modern contract allows.

If flexible pension death benefit options are important to you then you need to know what your pension plan can provide for your beneficiary as they may not be able to make use of your pension in the most suitable or tax efficient manner for them if their options are limited.

We have many decades of experience helping people manage their pension wealth and putting into place effective strategies for passing wealth on to future generations.

The Financial Conduct Authority does not regulate Tax Advice or Estate Planning.

If you would like to ensure that your pension plans provide the maximum flexibility for your family when you die or would just like to know a little more get in touch with us and speak to a financial adviser.