Skip to main content

Skip to main content

The importance of cash in your retirement plans

Whether you are considering retiring, or have already done so, one thought that would cause anyone to lose sleep at night is the idea of running out of money. This concern is even more evident in today’s world with high levels of inflation and stock market volatility leaving many to wonder whether their hard-earned savings will be able to keep up with the increased cost of living. In some cases, retirees may feel that taking more risk within their pension pot can help mitigate this outcome by searching for higher returns, even if this is at the expense of greater fluctuations in the short term.

In recent years, many investors have developed a false sense of security with relatively consistent and positive investment returns, however the last year has brought us back to reality with the reminder that investing comes with very real, and potentially damaging risks. This can be daunting for retirees, however, there are certain steps you can take to mitigate the impact of volatile markets and a good place to start is by considering how to manage taking an income from your pension, and how incorporating cash into your plans for retirement can help you sleep a little easier.

Arrange your free initial consultation

What is sequencing risk and how can it impact my retirement?

Sequencing risk, or ‘sequence of returns’ risk, is the risk of receiving lower or negative returns early on in your retirement when you begin drawing an income from your investments. The negative impacts of sequencing risk can have the effect of eroding your savings at a faster rate and can potentially increase the chances of running out of money.

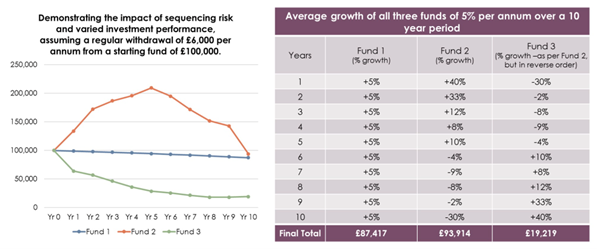

To put this idea of sequencing risk into context, let’s consider the journey of three retirees, each with £100,000 in savings and the requirement to draw £6,000 per year to fund their retirement income.

- The first retiree is invested in ‘Fund 1’ and achieves a consistent return of 5% each year. As the income being withdrawn is slightly greater than the return being achieved, the outcome shows this investor is left with £87,417 after 10 years.

- The second retiree is invested in ‘Fund 2’ and achieves varying (and more realistic) returns. In the first 5 years, we see returns ranging from 40% to 8% with an average annual return of 20.6%. The next 5 years provide negative returns ranging from -30% to -2% with an annual average return of -10.6%. The outcome shows this retiree will be holding £93,914 at the end of the 10-year investment period.

- The third retiree is invested in ‘Fund 3’ and achieved the same returns as ‘Fund 2’, but in the opposite order, with negative returns experienced for the first 5 years, which turn positive in the second period. Due to the ‘sequence of returns’ this investor is left with just £19,219, which represents a difference of £74,695 less left in their pension pot, compared to the second retiree.

This example illustrates that although ‘Fund 2’ and ‘Fund 3’ achieved the same ‘average annual returns’ over the 10-year period, the losses experienced in the earlier years, coupled with withdrawing funds each year, meant the third retiree was unable to make up for the negative returns experienced in the early years of retirement. This shows that the order of returns can be just as important as the average return that is achieved, and that controlling the volatility and withdrawals in a falling market can be essential to ensuring the long-term success of any withdrawal strategy.

As with all risks, sequencing risk can be managed through careful planning and adopting a suitable investment strategy, that both meets your requirements while also accounting for the natural uncertainty surrounding investment markets.

Why is cash a key component to reduce your risk?

One way to manage the impact of sequencing risk is to purchase an annuity at retirement. This creates a stream of guaranteed income for life which can be escalating to help reduce the impact of inflation. This option helps to eliminate sequencing risk by removing the investment element of your pension assets. However, it can limit the flexibility you have in retirement. Added to the fact that annuity rates, although much improved in the last year, are still relatively low by historical standards.

For retirees who want to retain the flexibility of accessing their pension via drawdown, it is not realistic to plan to only withdraw money during years of positive market returns and for most, leaving money in a bank, to shelter the impact of volatile markets, will not generate the returns required to sustain your income needs throughout your retirement. The answer to managing sequencing risk for invested assets, lies in developing a comprehensive investment strategy that incorporates cash as a key component.

Cash provides investors with predictable, albeit over the long term, lower, returns but can help reduce the need to surrender your investments at unfavourable times – if markets are down, you can draw on your cash pot to provide your income until markets recover. The main challenge is understanding the ideal balance between cash holdings, to provide security during market downturns, and investments, to ensure a suitable return is achieved to maximise the longevity of your pension assets.

How much cash should I be holding?

Most people will understand the importance of holding an emergency cash fund, which can act as a safety net to prevent having to sell investments, potentially at the wrong time when valuations are down., However, the answer to this question can vary substantially between individuals based on their unique circumstances and ambitions for retirement.

History has shown us that the average bear market, which is defined as a ‘prolonged drop in investment prices, generally experienced when a broad market index falls by 20% or more’, lasts for an average of 9 months, with the longest bear market, since 1950 lasting two and a half years. This suggests that a cash buffer of between one- and three-years’ worth of expenditure should be enough to help you ride out periods of falling markets. Although history provides us with a guide, it cannot predict the future and therefore speaking with an Independent Financial Planner can support you in developing a bespoke and comprehensive strategy which is regularly reviewed, to help to retire comfortably.

The good news is cash rates have risen considerably over the last year or so, so money held in cash can now also be working hard for you, giving you valuable interest that has not been experienced for some years.

Contact us now for an initial consultation to see if we can help you make more of your money. We are currently offering those with £100,000 in investments, savings or pensions a free, initial financial review worth £500.

Arrange your free initial consultation

Please note: The FCA does not regulate cash advice. This article is intended for general information only and should not be taken as personal financial advice. The value of investments can go down as well as up, so you could get back less than you invested. Past performance is not a reliable indicator of future performance.