Skip to main content

Skip to main content

Are you overcontributing to your pension?

When building up your pension it is important to be conscious of what limits apply in order to maximise the full tax benefits.

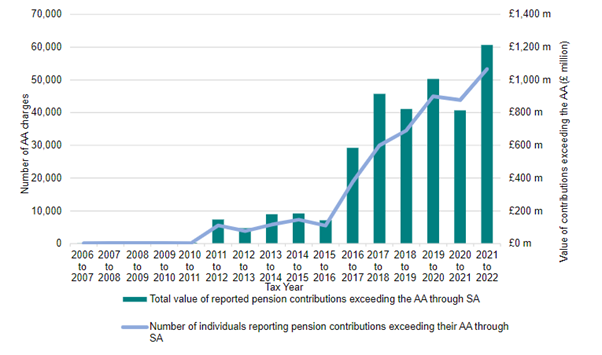

Thousands of people across the UK are experiencing tax charges for overcontributing to their pensions and most don’t even realise. According to HMRC over 50,000 people reported pension contributions that exceeded their ‘Annual Allowance’ (AA) in 2021-2022. This number has been skyrocketing since 2010 and has increased by 10,000 people since 2020-2021, when only approximately 40,000 exceeded their Allowance (Please see chart below).

Figure 1. Number of individuals and value of pension contributions exceeding the AA reported through SA 2006 to 2007 to 2021 to 2022, Source: UK Government

Often people don’t even realise that they are overcontributing until it is too late. So, why are so many people being caught out?

Arrange your free initial consultation

What is an Annual Allowance?

Although there is not a limit on the amount that can be saved into pensions each year, there is a limit on the amount that can benefit from tax relief each tax year. An individuals ‘Annual Allowance’ is the limit that you can contribute to your pension in any tax year whilst benefiting from tax relief. The current annual allowance is £60,000, however, you can only receive tax relief up until your net relevant earnings. Net relevant earnings are the total earnings from salary, bonuses, benefits in kind and trading profits for self-employed individuals in a tax year. So, if your salary is £40,000 for example, you would only receive tax relief up to £40,000, but if it is £80,000, in most cases, you would only receive tax relief up to £60,000 in one tax year.

What if I exceed my Annual Allowance?

If you exceed this allowance in a tax year, any contributions above the limit will typically be subject to an annual allowance tax charge. This excess will be added to your taxable income and be subject to income tax at your marginal rate. In some cases, you might be able to ask your pension scheme to pay the charge from your pension. This is known as Scheme Pays and means your pension would be reduced, but this is not always possible.

Why are people overcontributing?

Although the annual allowance sounds straightforward, there are some caveats that make understanding it a lot more complex. Where your net relevant earnings are more than £60,000 a year and have been a member of a registered pension scheme for more than three years, you may have the ability to use carry forward allowances. If you have not used your full annual allowance from any of the previous three tax years, you can carry this allowance over to the current tax year. This can cause confusion and miscalculations regarding exactly how much more an individual can contribute using carry forward.

Those who have a high income are also subject to more complex rules with regards to their annual allowance. For every £2 of adjusted income (i.e. total taxable income before any Personal Allowances and less certain tax reliefs) that an individual earns over £260,000 their annual allowance is reduced by £1, to a minimum of £10,000. This means that anyone with an income of £360,000 or more has a reduced annual allowance of £10,000.

Another caveat that trips people up is that, in some cases, the annual allowance reduces to £10,000 per tax year when an individual begins drawing down or withdrawing from their pension. This is often triggered for those who are flexibly accessing a defined contribution scheme. It is worth noting this is not the case for all withdrawals, for example when taking a Pension Commencement Lump Sum (PCLS) or annuity. When this reduced allowance comes into effect, carry over cannot be utilised anymore. This can often catch people out and cause them to overcontribute because they think they have more allowance than they do.

It is also worth remembering your annual allowance takes into consideration all contributions to all of your private pension schemes. Therefore, it is not only your personal contributions that count towards the annual allowance, but your employer contributions as well. For those who are fortunate enough to have a Defined Benefit (DB) scheme, otherwise known as a final salary scheme i.e., a pension that traditionally pays out a guaranteed income every year in retirement, calculating the remaining annual allowance is more complex. Any further accrual in a Defined Benefit scheme in a tax year contributes to the annual allowance. These additional complexities make calculating the annual allowance year on year more difficult to understand. As a result, many people find themselves overcontributing and incurring a tax charge without even realising.

Taxation on pension funds has become a hot topic since the 2023 Spring Budget announcement about the intention to remove the ‘Lifetime Allowance (LTA)’. The LTA is the total contributions that one can make to a pension over their lifetime without incurring certain tax charges. Those who weren’t overcontributing prior to this, for fear of exceeding the LTA, have more incentive to re-commence contributions. However, with a general election expected in the autumn of 2024, these changes could be reversed.

If you’re concerned, we can help. With more people than ever exceeding the annual allowance, it is important to be aware of the many factors that need to be considered when calculating how much you should be contributing to a pension. If you have any questions about the annual allowance, or think you might be at risk of a tax charge due to miscalculations; then please get in touch with your Financial Adviser or consider seeking advice.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information in this article is based on current laws and regulations which are subject to change as at future legislations.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

The Financial Conduct Authority (FCA) does not regulate tax advice.