Skip to main content

Skip to main content

You can’t control a market crash, but you can plan for it

Economic recessions, unfortunately, are inevitable. The economy booms and busts as years go by and there is little that we can do to avoid this cycle. One thing we are able to do, however, is plan for these events so that we limit any damage caused by them. If we look at the last 18 months as an example, markets have been put through a whirlwind of events. In April 2021 we started to see the back of the COVID-19 lockdowns in the UK but since the start of 2022 we have seen lockdowns in China combined with Russia’s military invasion of Ukraine. These events have pushed commodity prices up significantly which ultimately led inflation to levels we haven’t seen in decades. This generated turmoil in both the equity and bond markets and we may be about to witness the country’s first recession since 2008. Anyone who invested at that time will remember the impact, but if this is your first experience then you will, understandably, feel uncomfortable – especially when an end is not yet in sight.

This uncertainty can lead to impulsive decision-making or reactive behaviour, which can lead to poor financial decisions being made. Investing into the stock market should be seen as a long-term decision and as a rule of thumb, we advise clients only invest money that they will not need to draw upon in the next 3-5 years. This means, in falling markets, the best course of actions is to sit tight and wait for conditions to improve so these can recover- a loss is only crystallised once the investment is sold. This can be a difficult and uneasy experience for many first-time, and even seasoned, investors, but the act of remaining calm when things are not going well is often the best course of action.

Arrange your free initial consultation

How forecasting can help you plan ahead

At TPO, we use cash flow financial forecasting to help inform decisions at times like these. By building your situation in terms of assets, income, liabilities and incorporating your financial objectives, we can accurately inform on investment decisions based on your specific situation.

If a client was on track to achieve their financial objectives and there was no immediate need to draw upon their invested wealth, we would be able to show this graphically and help put them at ease despite their investments not performing as well as they’d hoped. Ultimately, values of investments change every day – to react to these short-term figures would be unwise. Cash flow financial forecasting helps the client see the bigger picture and show them that they are still on track to meet their objectives and expenditure, even in falling markets.

We often utilise helpful strategies that can be used in tandem with cash flow financial forecasting to help prevent any turmoil when the markets experience a downturn. For example, we can position portfolio so that you have segments of your wealth invested in various risk levels for different purposes. Keeping a cash buffer, for example, allows you to hold a level of funds in a pot that is free from equity risk to be drawn upon in times of market volatility without incurring any investment loss. Savings Champion, our sister company, offers whole of market, unbiased cash advice and compares interest rates for all types of savings accounts. On the other hand, holding some of your investments in “risk-on” assets, such as equities to achieve growth over the long term is beneficial as your portfolio will have the potential to increase before you need to access it later in life.

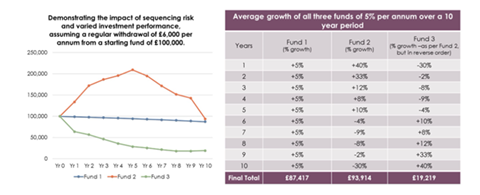

What is sequencing risk?

Holding all your investments in one pot would expose you to sequencing risk. This is the risk that, when drawing upon investments regularly, a dip in the value early on can significantly impact your fund in the latter years. The fund may experience a higher growth rate after the dip but because the fund has already shrunk and you have taken withdrawals from it, it is much more difficult to grow the fund back to its original level, as shown in the charts above. By holding a portion of cash, you effectively allocate a segment of your portfolio towards facilitating regular withdrawals without reducing the value of your invested wealth, thus mitigating any sequencing risk.

There are ways to ensure that turbulent market environments do not have a significantly adverse impact on your invested wealth. Investing for the long term and picking appropriate risk mandates helps ensure that you will not need to draw on money that suffers greatly from short term volatility. At The Private Office we invest our clients in portfolios which have been selected to benefit from long term growth in line with each individual’s needs and objectives.

If you’d like to learn more why not get in touch with one of our expert advisers for a free initial consultation.

Please note: The Financial Conduct Authority (FCA) does not regulate cashflow modelling.