Skip to main content

Skip to main content

The cost of Inheritance Tax gift mistakes soars to £336m

HMRC collected an estimated £336 million in inheritance tax (IHT) over the past five years from failed gifting arrangements, after the assets involved were deemed not to have been fully given away.

Between 2021 and 2026 nearly 2,500 gifts with a combined value of £840 million were classed by HMRC as gifts with “reservation of benefit”. This applies where the person making the gift continues to enjoy some benefit or use of the asset after it has been passed on.

As a result, these gifts, which had an average value of £338,840, did not qualify for inheritance tax exemption and left families facing an estimated £336 million tax charge.

What is a gift with reservation of benefit?

A gift with reservation of benefit essentially means when someone gives away an asset but continues to enjoy, or is able to enjoy, some benefit from it. The classic example is a person who gives their house to their children but continues to live in it rent-free.

As a result, the gift is not regarded as an effective lifetime transfer for inheritance tax purposes. Instead, the asset – the house in the above example - is treated as remaining within the donor’s estate when they die, meaning its full value is included in the inheritance tax calculation. The asset may also be subject to tax again on the death of the recipient.

What counts as the gifter still ‘benefitting’ has a fairly wide definition and applies to many other assets too. Examples include handing over valuable possessions while still making regular use of them and transferring shares in a family company while keeping the right to receive dividends or exercise voting power. In these situations, the legal ownership may have changed, but the donor is still considered to retain an interest in the asset. It is important to understand whether you will be classed as still ‘benefitting’ from the asset you have gifted before you go ahead and ‘gift’.

You can find out more about gifts without reservation of benefit here.

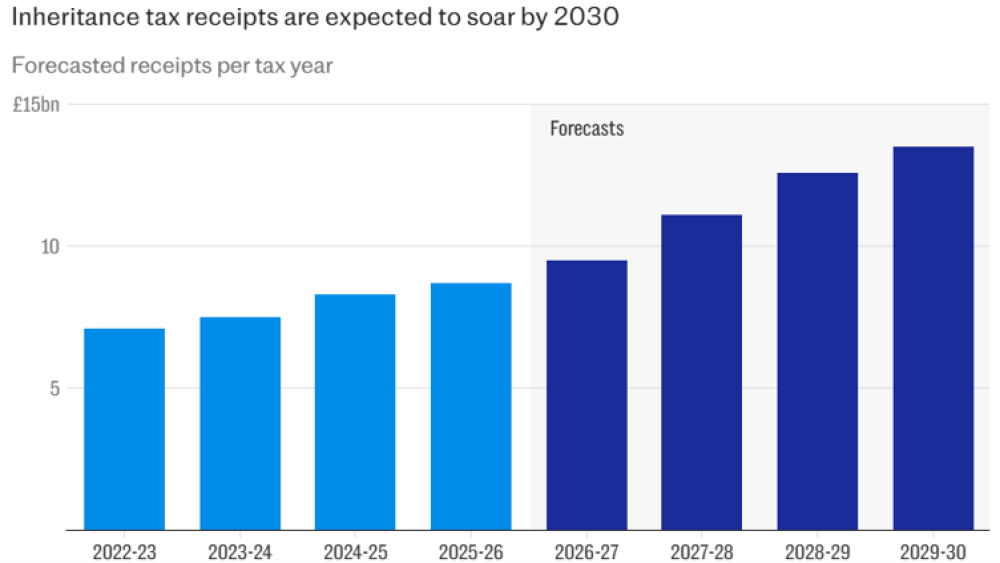

Why are IHT receipts always on the rise?

Total IHT receipts collected by the Government has been steadily on the rise since the IHT threshold freeze and are showing no signs of slowing.

Source: Inheritance tax receipts are expected to soar, OBR, 2023

This was initially announced by the then Chancellor, Rishi Sunak, in his 2021 Budget. The Budget outlined that the IHT threshold would be frozen for five years until 2026.

However, after ex-Chancellor Jeremy Hunt’s 2023 Autumn Statement, it was confirmed that the freeze would be extended a further two years until April 2028, and then after Rachel Reeves’ 2024 Autumn Statement, this was extended once again a further two years until April 2030, and finally after her 2025 Autumn budget, it was again extended, this time until April 2031.

Many have been calling this move an example of a ‘stealth tax’, as the freeze ultimately means an increasing number of Britons will fall into the tax threshold each year until the freeze ends in April 2031 – if it indeed does end and hasn’t been extended again by that time – and by then the Government will have collected billions of pounds worth of extra IHT from the UK taxpayer.

The inheritance tax allowance of £325,000 increased from £312,000 on 6 April 2009. This means the IHT nil rate band has now been frozen for over 15 years and will continue to be frozen until at least 5 April 2031. Though some additional relief was introduced in April2017 through the residence nil rate band, which can increase the tax -free allowance where a main home is passed to direct descendants, the main nil rate band itself will have been frozen for a staggering 22 years of higher taxes on death - over two decades.

If you’re interested in how to manage your inheritance tax to ensure the best possible wealth protection for you or your family, we can help. Give us a call on 0333 323 9065 or book a free non-committal initial consultation with a member of our team to find out more.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.