Skip to main content

Skip to main content

Extra income tax revenue forecasted to hit £27.8bn a year

As has been its habit in the past few years, the Office for Budget Responsibility (OBR) has reworked its calculations on the impact of the freezes to the personal allowance and higher rate threshold and the cut and freeze of the additional rate threshold in its latest Economic and Fiscal Outlook (EFO).

In the March 2021 EFO, which accompanied Rishi’s Sunak’s original announcement of a freeze on the personal allowance and higher rate threshold through to 2025/26, the OBR estimated that by 2025/26 the net effect would be:

- Extra income tax revenue of £8bn a year;

- 1.3 million more taxpayers than if the personal allowance had been indexed; and

- million more higher rate taxpayers than if the higher rate threshold had been indexed.

A year later, inflation prompted the OBR to revise its 2025/26 figures to:

- Extra income tax revenue of £17.5bn a year;

- 2.8 million more taxpayers than if the personal allowance had been indexed; and

- 2.0 million more higher rate taxpayers than if the higher rate threshold had been indexed.

In the latest EFO which emerged last week, the OBR has once again revamped its spreadsheets, this time taking the timeline out to 2028/29, the end of five year forecast period. It now reckons that by 2025/26 the impact will be:

- Extra income tax revenue of £27.8bn a year;

- 3.5 million more taxpayers than if the personal allowance had been indexed; and

- 2.3 million more higher rate taxpayers than if the higher rate threshold had been indexed.

- 0.4 million more additional rate taxpayers than if the £150,000 threshold had remained.

Taking the view out to 2028/29 gives the following:

- Extra income tax revenue of £34.5bn a year;

- 3.7 million more taxpayers than if the personal allowance had been indexed; and

- 2.7 million more higher rate taxpayers than if the higher rate threshold had been indexed.

- 0.6 million more additional rate taxpayers than if the £150,000 threshold had remained.

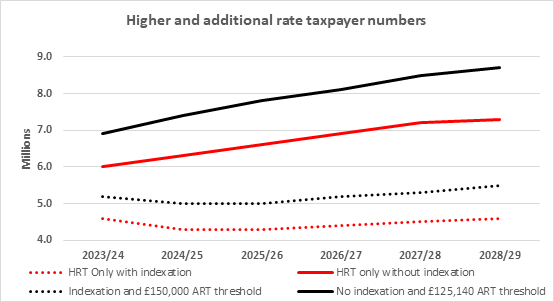

The EFO projections also show that by 2028/29, 22.3% of all income taxpayers – over a fifth – will be paying more than the basic rate against 14.5% in 2021/22 (and 10.4% in 2010/11 when additional rate tax was introduced). The path of taxpayer numbers from 2023/24 is shown in the graph below.

Higher and additional rate taxpayer number estimates. Source: Techlink

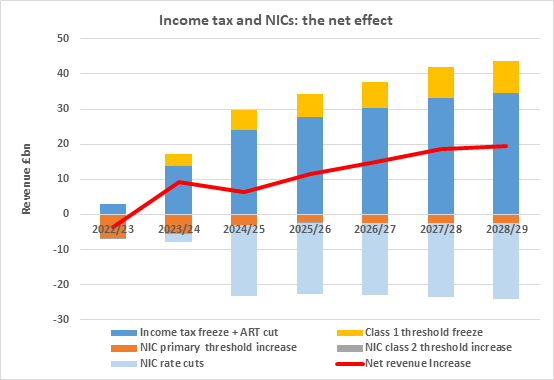

As Mr Hunt would doubtless point out, the extra income tax is to a degree offset by the reductions in National Insurance (NIC) rates made in the Autumn Statement 2023 and the Spring Budget 2024 and the earlier hikes in the class 1 primary threshold and class 2 threshold. However, there is still a substantial overall net increase of funds flowing to the Exchequer of nearly £20bn in 2028/29, as the red line on following graph shows:

Net revenue increase of income tax and NICs. Source: Techlink

The NIC rate cuts have clawed back some of the pain inflicted by the income tax freezes, however the distribution across income bands is not even. Middle earners have done better than those at the lower end of the income scale who pay little NICs while at the upper income end the frozen higher rate threshold and additional rate threshold cut/freeze are not compensated for by a maximum NIC saving of about £1,500.

Maximising tax allowances has become more important as the frozen tax thresholds has a greater impact. Please speak to your usual TPO Adviser for more information, or if you'd like to request a copy of our updated Tax Tables 2024/25.

The information in this article is correct as of 12/03/2024.

Please note: The Financial Conduct Authority (FCA) does not regulate tax advice.