Skip to main content

Skip to main content

How much inheritance is tax free?

In simple terms, inheritance tax is a tax on a deceased person’s estate and some lifetime gifts. Savings, Investments, property, and possessions are all included, along with any other assets they may have – once funeral expenses and any debts have been taken out of the equation. Of course, whether or not inheritance tax needs to be paid will depend on the value of the estate, who the beneficiaries are (e.g. exempt or not) and whether it meets the inheritance tax threshold.

Arrange your free initial consultation

How much can you inherit before paying inheritance tax? Or, in other words, what is the inheritance tax threshold in the UK? How is inheritance tax calculated? These are some of the most commonly asked-about questions when it comes to inheritance tax – read on where we explain in more detail.

Understanding the Inheritance Tax Allowance and Rules

Inheritance tax is only charged on the value of an estate above a certain threshold. This threshold, known as the nil rate band (NRB), is currently £325,000 per individual. An additional allowance called the residence nil rate band (RNRB) may also apply if the deceased leaves their main residence to direct descendants such as children or grandchildren. This adds up to a further £175,000 per person, to the tax-free threshold, giving a total allowance of up to £500,000. For married couples or civil partners, these allowances can be combined, potentially allowing estates worth up to £1 million to pass on without any inheritance tax. However, the residence nil rate band (RNRB) tapers away for estates valued above £2 million, meaning it may not apply in larger estates.

These allowances are frozen until April 2031. It is important to understand how they apply to your personal circumstances, as effective use of both thresholds can make a significant difference in the amount of inheritance tax owed. Keeping track of current thresholds and rules is essential to ensure your estate is structured in the most tax-efficient way.

How is inheritance tax calculated?

In the UK, inheritance tax is currently set at a hefty 40%. However, this only applies to anything over the tax-free threshold, assuming the estate is not being left to a spouse or civil partner. It’s also worth noting that where at least 10% of the deceased person’s net estate is left to charity, there will be a lower rate of 36%.

Lifetime inheritance tax (on chargeable lifetime transfers) is charged at 20% – half of the death rate – but if the settler dies within seven years of making the transfer, there could be an extra charge. This is because there is a 7 year rule in Inheritance Tax, you can read more about that here.

What is the inheritance tax threshold?

You don’t have to pay inheritance tax if the deceased person’s estate is worth no more than £325,000 – or up to a combined £650,000 for a married couple. The rules also allow a spouse or civil partner of the deceased person to receive everything inheritance tax free. However, it’s not automatic, as the surviving spouse’s personal representatives will need to claim this in the event of their spouse’s death. If the deceased person left everything to a body exempt from inheritance tax, like a charity or political party, no inheritance tax will need to be paid either.

In addition, the inheritance tax threshold can be passed on between spouses or civil partners. For example, imagine that your estate is worth £600,000, and you leave £130,000 to your children and the rest to your wife. The £130,000 left to your children takes up 40% of the threshold, leaving 60% of the threshold – this can then be passed onto your spouse. If the threshold when your spouse dies is still £325,000, their threshold would increase by 60% to £520,000.

For everything else, in general inheritance tax will be 40% of the estate’s value above £325,000. For example, if an estate worth £400,000 is left behind, £75,000 would be liable to inheritance tax, meaning an inheritance tax bill of £30,000 (£75,000 minus 40% is £45,000, the difference being £30,000).

With rising property values and in turn, potentially large estates at stake, even those with average wealth could be subject to a big tax bill, so it’s never been more important to look at ways to minimise your inheritance tax bill.

How to reduce inheritance tax

There are a few ways to minimise inheritance tax. However, it’s generally the job of the deceased person to plan for this before their passing, meaning that you may need to start some uncomfortable conversations between generations to work out how to minimise inheritance tax in the most appropriate way.

In addition to a person's tax free threshold of £325,000, introduced in April 2017 was the home allowance known as the residence nil rate band, mentioned above. This increased the tax-free threshold when someone leaves their home to either their biological children, adopted, foster/stepchildren, children under their guardianship, grandchildren, or great-grandchildren and their spouses/civil partners. As of 2021, this additional allowance is £175,000.

However, the home allowance will only apply if the deceased person’s estate is worth less than £2 million. For every £2 over this threshold, you lose £1, so if an estate is worth over £2.35 million, the residence nil rate band will be lost.

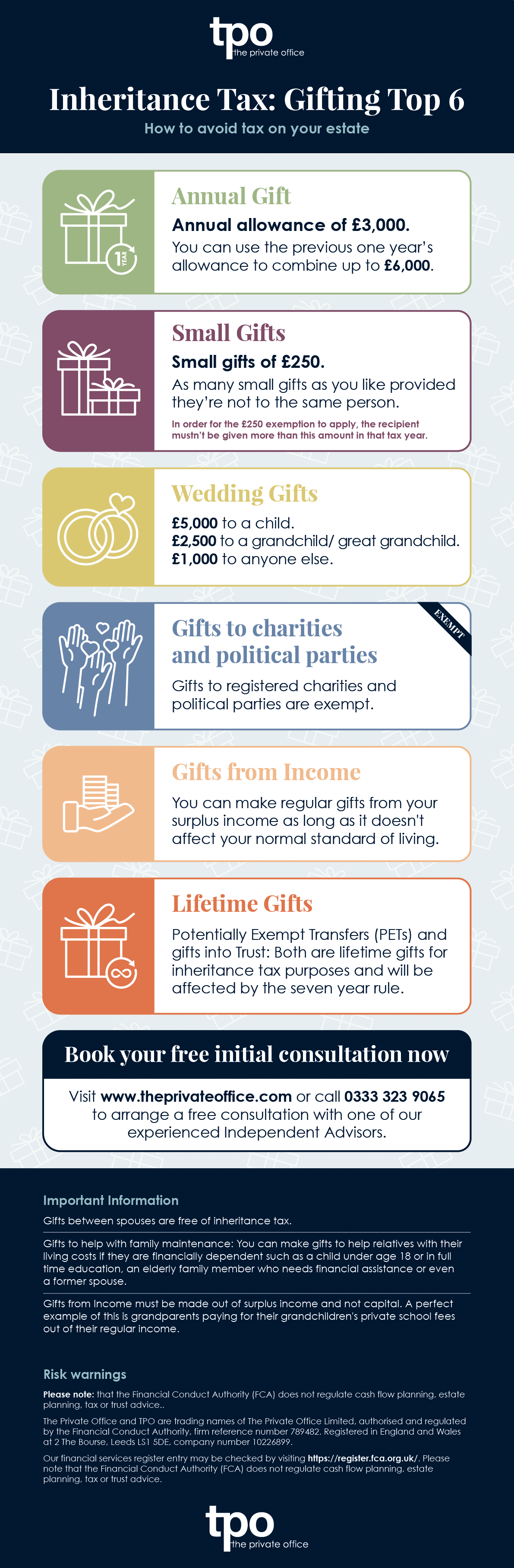

Alternatively, you can help mitigate inheritance tax altogether. There are a couple of different ways to go about doing this. Consider the annual exemption: HMRC lets individuals give £3,000 to family and friends each year, tax-free, while a married couple/civil partners can give £6,000 per year tax-free. By deducting these from the value of your estate, no inheritance tax will be due on them.

You can carry the exemption forward for one year, too. For example, if you don’t give anything away in 2025/26, you can give away £6,000 in 2026/27. However, if you don’t give away the £3,000 you carried over from 2025/26 in 2026/27, you’ll lose it.

Inheritance tax gifts

Another way to avoid paying inheritance tax is giving a gift – be it property, money, or something else – assuming that the ‘giver’ lives for another seven years. This is referred to as the seven-year rule in inheritance tax. There are also tax benefits to charitable giving which you can read about here.

Another way to get around inheritance tax is when spouses give each other tax-exempt gifts. However, there are a few requirements for this.

Under the new Long Term Residency Rules, that have been effective from 6 April 2025, the spousal exemption for inheritance tax (IHT) has changed to focus on long-term UK residence rather than domicile status. Transfers between spouses or civil partners are fully exempt from IHT if both meet the long-term UK residency criteria, defined as UK tax resident for at least 10 out of the previous 20 tax years. It still remains a crucial IHT relief, but eligibility now depends on the long-term UK residency status of both partners, not just domicile.

There are tax-free thresholds for wedding gifts too, which are as follows:

- £5,000 from your parents

- £2,500 from your grandparents or great-grandparents

- £1,000 from a friend or another relative

Gifting Top Tips

Here are some of the key figures to remember when looking to gift to avoid Inheritance Tax (IHT). This is so you can check, at a glance, if you can avoid being hit with an otherwise avoidable tax bill.

If you would like to know more about how we can help keep more of your wealth for your loved ones, contact us to speak with an expert adviser.

Arrange your free initial consultation

Download our handy IHT Gifting checklist

When is inheritance tax paid?

When it comes to paying inheritance tax, it has to be done within six months of the death – after this point, HMRC will begin to charge you interest.

In general, the tax will be taken out of the inheritance, and in most instances the deceased person will have appointed an executor, who will take care of this process. However, if you happen to be the legal heir, and there’s no Will, it’ll be your responsibility to designate somebody to administer the deceased person’s estate.

The executors can decide to pay the tax on some assets, like property, through instalments over a period of up to ten years, but interest will still be required on the amount of tax left to pay. Should the asset be sold before your tax bill is paid in full, the executors will need to make sure that all instalments, as well as interest, are paid.

Even if no inheritance tax is due, you may still need to report to HMRC, although this process was simplified in January 2022 so that the personal representatives of low-value estates or exempt estates may no longer need to complete an inheritance tax return. However, if the estate is likely to pass the inheritance tax threshold, it’s recommended that the executor pay some of the tax within six months of the death. Known as payment on account, this will reduce the amount of interest that will be charged further down the line. If the executor has overpaid on inheritance tax, HMRC will issue a refund once probate is given.

It’s also important to keep records when valuing an estate, including information like an estate agent’s valuation of the property, as HMRC can request these records for up to twenty years after the inheritance tax is paid.

How can TPO help

The question of how to minimise inheritance tax doesn’t always have a straightforward answer, and it can be confusing to keep track of the inheritance tax threshold.

If you’re not sure how to move forward and would like to discuss how to minimise inheritance tax on your estate with one of our financial advisers, get in touch for a free initial consultation.

Arrange your free initial consultation

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

| Content reviewed by: | |

| Chartered Financial Planner, FPFS |