Skip to main content

Skip to main content

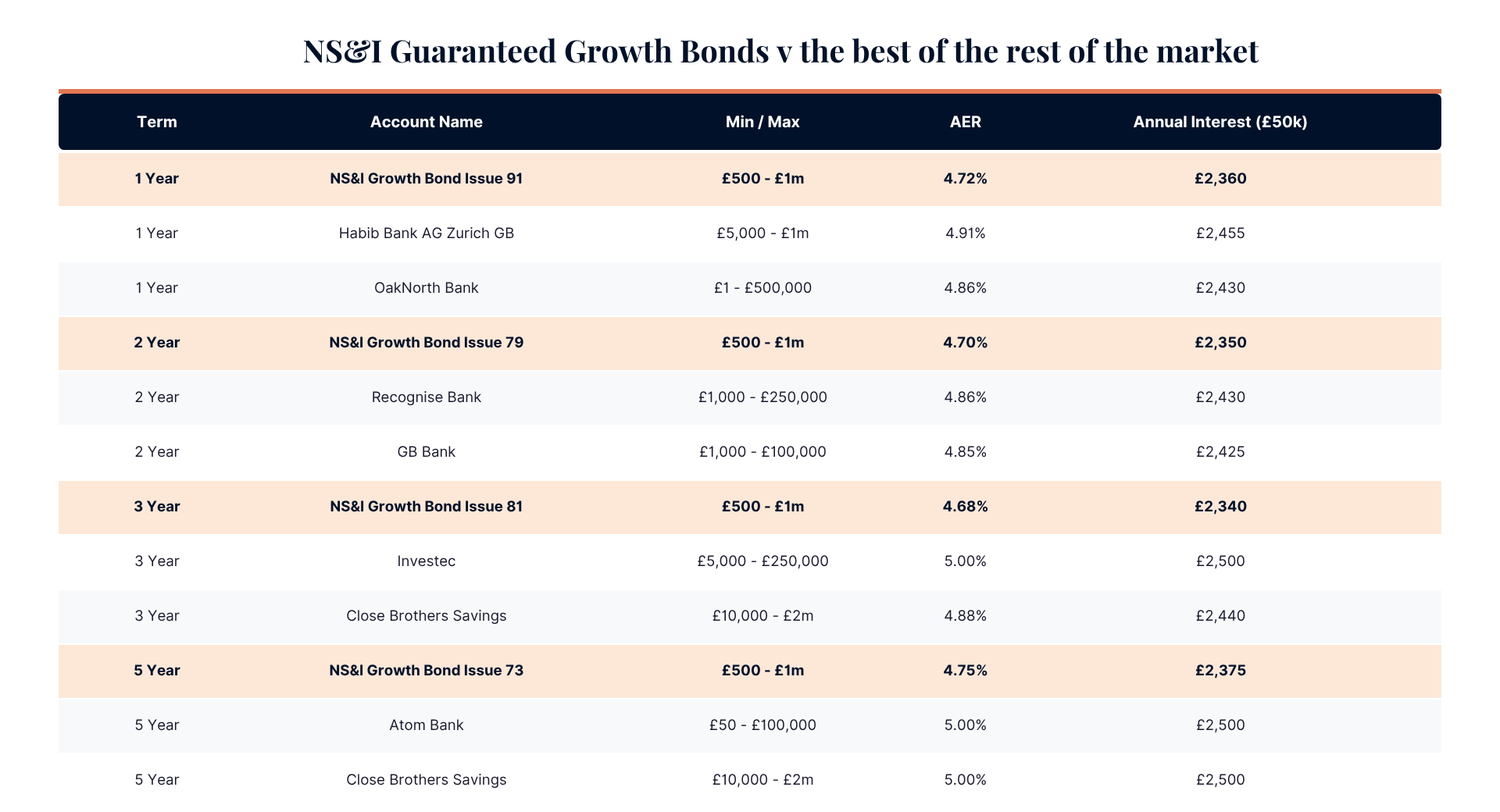

NS&I raises British Savings Bond rates again – but are they good enough?

Just one day after the Bank of England's Monetary Policy Committee (MPC) voted to keep the base rate on hold at 3.75% on 30th July 2026, National Savings & Investments (NS&I) announced another increase to the rates on its Guaranteed Growth and Guaranteed Income Bonds, also known as British Savings Bonds.

This is the third increase to these bonds this year and, given that the base rate was left unchanged, it may seem a little surprising. However, when you look at what has been happening in the wider savings market, the move makes perfect sense.

What are the new rates?

| Product | Previous interest rate (from 23rd June 2026) | New interest rate (from 31st July 2026) |

|---|---|---|

| Guaranteed Growth Bonds 1-year (Issue 91) | 4.69% gross/AER | 4.72% gross/AER |

| Guaranteed Income Bonds 1-year (issue 91) | 4.60% gross/ 4.69% AER | 4.63% gross/ 4.72% AER |

| Guaranteed Growth Bonds 2-year (issue 79) | 4.67% gross | 4.70% gross/ AER |

| Guaranteed Income Bonds 2-year (issue 79) | 4.58% gross/ 4.67%AER | 4.61% gross/ 4.70% AER |

| Guaranteed Growth Bonds 3-year (issue 81) | 4.65% gross/ AER | 4.68% gross/ AER |

| Guaranteed Income Bonds 3-year (issue 81) | 4.56% gross/ 4.65% AER | 4.59% gross/ 4.68% AER |

| Guaranteed Growth Bonds 5-year (issue 73) | 4.55% gross/ AER | 4.75% gross AER |

| Guaranteed Growth Bonds 5-year (issue 73) | 4.46% gross/ 4.55% AER | 4.65% gross/ 4.75% AER |

Why is NS&I increasing rates again?

Unlike commercial banks, NS&I has a very different objective.

Its role is to raise money for the Government in a cost-effective way, so rather than trying to get to the top of the best buy tables, it adjusts its interest rates to attract just enough money to meet its Net Financing Target; the amount NS&I needs to raise as a Government department, after allowing for withdrawals.

If too much money is flowing in, it can reduce rates. If it needs to attract more deposits, it can increase them.

Whilst the Net Financing raised for 2025/26 was £12.1 billion, so was within the leeway target for the year of plus or minus £4 billion, it was just under £1 billion less than the actual Net Financing Target of £13 billion. So perhaps NS&I realises that it needs to be more competitive to raise the funds needed, to meet the current tax years target especially given that the target is higher at £15 billion (+/- £4 billion).

Competition for savers' money has been strong this year. Fixed term bond rates have been climbing higher as banks and building societies compete for deposits, and NS&I will need to stay competitive if it wants to raise the funds it needs.

Competitive, but not market leading

NS&I has become more competitive, but it still is not offering the highest rates available.

Of course, if it did consistently top the best buy tables, it would almost certainly attract more money than it needs, making it more expensive for the Government to borrow through NS&I than necessary.

Instead, it aims to offer rates that are attractive enough to meet its funding target without distorting the wider savings market.

The latest increases narrow the gap and make the British Savings Bonds look much more appealing, particularly when compared with many of the accounts offered by the well-known High Street banks.

However, if savers are prepared to shop around and use a provider that they are perhaps less familiar with, they can still earn higher rates elsewhere. As long as that bank or building society is part of the Financial Services Compensation Scheme (FSCS), there is no reason not to take a well-informed leap of faith in order to earn more.

Why do many savers still choose NS&I

Of course, the interest rates are only part of the story. Security is another.

Money held with banks and building societies is protected by the Financial Services Compensation Scheme (FSCS), up to £120,000 per banking licence. Whilst that level of protection is more than enough for most people, those with larger cash balances often have to spread their money across several providers to remain fully protected.

One of the biggest attractions of NS&I is the security it offers. Every penny deposited is backed by HM Treasury, giving savers an unlimited Government guarantee.

For those who don’t have the time or inclination to open multiple savings accounts, this is one of the key reasons NS&I remains so popular, even when it is not paying the very highest rates.

Should you choose NS&I?

British Savings Bonds now compare more favourably when compared to many of the products offered by the High Street banks. And they remain one of the simplest ways for those with larger cash balances to benefit from the unique HMRC protection.

But that does not necessarily mean they are the best option.

If your main objective is to maximise the interest on your savings, then the bottom line is that you can earn far more by shopping around.

For the latest rates, visit our Best Buy tables.

Arrange your free initial consultation

Rates correct 04/08/2026

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Is £50k a good salary in the UK?

Earning £50,000 a year should feel comfortable. For many people in 2026, it doesn't.

On paper, it's a good income and comfortably above the UK median full-time salary of £39,039. Yet many people earning £50,000 still find themselves wondering where their money goes each month.

Higher living costs, rising rents, mortgage affordability pressures and frozen tax thresholds mean that the gap between what £50,000 looks like on paper and what it feels like in your bank account can be significant.

Arrange your free initial consultation

Tax breakdown for earnings of £50,000

If you earn £50,000 as an employee in the UK in the 2026/27 tax year, your take-home pay will be roughly £39,519, which works out at about £3,293 a month.

This assumes you receive the standard Personal Allowance of £12,570. The remaining £37,430 is taxed at the basic rate of 20 per cent, giving an income tax bill of around £7,486. A £50,000 salary sits just below the higher rate threshold, which starts at £50,271.

You would also pay employee National Insurance. For 2026 to 2027 tax year, this is usually charged at 8 per cent on earnings between the Primary Threshold of £12,570 and the Upper Earnings Limit of £50,270. On a £50,000 salary, that means National Insurance of around £2,995.

Put together, income tax and employee National Insurance come to around £10,481. That is why a £50,000 salary does not translate into £4,167 a month in your pocket. Your final take-home pay may also vary depending on pension contributions, salary sacrifice, bonuses, taxable benefits, student loan deductions, other income, and whether you are a Scottish taxpayer, as Scotland uses different income tax bands.

You can find all the different tax allowances and reliefs in 2026-27 here

Living costs in the UK

The most recent Office for National Statistics (ONS) family spending figures show average weekly household expenditure of £623.30 in the financial year ending 2024, and this is estimated to have increased in the years since, due to the cost-of-living crisis.

Housing

Housing is often the single biggest factor.

If your rent is around the UK average, you may be spending close to 40 per cent of your take home pay on rent alone. The ONS reported that average UK monthly private rents reached £1,366 in November 2025, with higher averages in England and much higher costs in parts of London and the South East.

For solo renters, this can absorb a large part of your net income.

Imagine two people, both earning £50,000. One rents a one-bedroom flat in central London for £2,000 a month. The other owns a home in Yorkshire with a £900 monthly mortgage. It’s the same salary, and yet they have completely different living costs.

Now factor in childcare costs, student loan repayments, car finance, commuting expenses or re-mortgaging onto a higher interest rate, and the gap widens even further. It's why one person earning £50,000 has enough disposable income to save, while another reaches payday wondering where their salary has gone.

When it comes to buying a house, the average UK house price was £270,000 in December 2025, according to the latest UK House Price Index.

A common mortgage income multiple of around 4.5 times salary would suggest borrowing capacity of about £225,000, although lenders assess affordability more closely than this and will consider debts, dependents, credit history and regular spending. With a meaningful deposit, buying may be achievable in many areas, but it can still be difficult in more expensive regions.

Utilities and council tax

These are the types of essential costs that are difficult to reduce, which is why many people feel pressure on their disposable income even when earning above the national average.

Energy costs remain a meaningful monthly expense. Ofgem set the price cap for a typical household paying by Direct Debit at £1,641 a year from April to June 2026, although your actual bill will depend on usage, property type and tariff.

Council tax also matters. The average Band D council tax bill in England for 2026 to 2027 is £2,392. That is close to £199 a month before any discounts.

Transportation

Transport costs depend heavily on where you live. A commuter using rail into a major city may have far higher costs than someone working from home. If you run a car, then insurance, fuel, servicing, parking and finance payments can quickly eat into the disposable income that looks healthy on paper.

Groceries and dining out

Groceries are another area where inflation has changed the feel of a £50,000 salary. A weekly food shop, occasional meals out and small everyday purchases can now make a noticeable dent in monthly cash flow. Individually these purchases rarely seem significant, but together they can make a noticeable difference to how much is left at the end of the month

Leisure and entertainment

A £50,000 salary should still allow room for holidays, hobbies and socialising, but usually with some trade-offs. If you are also saving for a house deposit, contributing meaningfully to a pension or supporting family, leisure spending may need to be planned rather than casual.

Financial considerations and saving potential

A £50,000 income can be a strong foundation for building long-term wealth, but only if it's supported by a clear financial plan.

Savings

At this income level, you should ideally be building an emergency fund, keeping cash for known short term costs and using tax efficient allowances where appropriate.

Cash ISAs can be useful for savings you want to keep accessible while sheltering interest from tax, and Stocks and Shares ISAs may be suitable for longer term investing. You should also be aware of the Personal Savings Allowance, as interest on cash savings may become taxable once it exceeds your allowance.

If you already have at least £100,000 in investable assets, the question becomes less about whether you can save and more about how efficiently your money is working.

Pension contributions

Pension contributions are one of the most useful planning tools on a £50,000 salary. Your income is close to the higher rate tax threshold, so even modest pay rises, or a bonus could push some of your earnings into higher rate tax. Increasing pension contributions can help keep your taxable income below that threshold while building long term wealth, though it's important to note that you won't be able to access this money until retirement. This is currently age 55, but is increasing to 57 from April 2028.

Salary sacrifice can be especially helpful where available, as it may reduce both income tax exposure and National Insurance, depending on your employer’s scheme. Even relatively small increases in pension contributions made consistently over many years can have a significant impact on retirement outcomes thanks to investment growth and tax relief.

Debt management

Debt can change the whole picture. A £50,000 salary with no unsecured debt and manageable housing costs can feel comfortable. The same salary with credit card balances, car finance and high mortgage or rental costs can feel tight.

The priority is to understand which debts are expensive, which are strategic and which are restricting your ability to invest for the future.

Financial planning

This is often the point where financial advice starts to add real value. Around this level of income, many people find themselves balancing competing priorities. Should you overpay your mortgage or invest instead? Increase pension contributions or build your emergency fund? Make use of your ISA allowance or keep more cash available? There is rarely a single 'right' answer, but getting these decisions right can make a meaningful difference over the long term.

Is a pay rise above £50,000 worth it?

The short answer is yes. A common misconception is that moving into the higher-rate tax band leaves you worse off overall. In reality, only the income above the threshold is taxed at the higher rate, so you'll always take home more money after a pay rise.

Once your income moves above £50,270 in England, Wales and Northern Ireland, earnings above that threshold are generally taxed at 40 per cent, with employee National Insurance at 2 per cent above the Upper Earnings Limit. You’ll also lose 50% of your personal savings allowance, dropping from £1,000 a year tax free, to £500 a year, as soon as you fall into the higher rate tax bracket.

That does not mean you are worse off. It simply means each extra pound above the threshold may be taxed more heavily. Pension contributions can help manage this, particularly if you do not need all of the additional income immediately.

Career progression and future earnings

Though £50,000 is a reasonably high salary, the bigger question is whether your income is likely to rise, whether your career is resilient, and whether your savings and investments are growing alongside your earnings.

Frozen thresholds have changed the way many professionals experience pay rises. The Personal Allowance and higher rate threshold have been fixed since 2021/2022 tax year and are due to remain frozen until 2031, which means more people are being pulled into higher tax bands as pay increases.

So, is £50,000 a good salary?

By UK standards, yes. It remains comfortably above average and has the potential to support a good lifestyle, meaningful savings and long-term wealth. However, salary alone no longer guarantees financial comfort. How far your income goes depends on where you live, the financial commitments you have and, perhaps most importantly, the decisions you make with your money.

That's where financial planning can make a real difference. At TPO, we use Cash Flow Forecasting to help clients understand how today's financial decisions could shape their future, giving them greater confidence to enjoy their money now while still working towards long-term goals.

If you’d like help mapping out your financial future, why not get in touch for a free initial conversation to see how we can help.

Arrange your free initial consultation

This article is for information only and does not constitute individual advice. The information provided in this article is based on the current allowances and legislation and is subject to change.

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Savings round-up: why rates have defied expectations

It’s been an interesting year so far for savers – and much more positive than many expected. As we pass the halfway point of 2026, here’s a look at what’s happened to savings rates so far, and what we might expect going forward.

At the start of the year, the expectation was that the Bank of England base rate, and therefore savings rates, would continue to fall. At the Monetary Policy Committee (MPC) meeting in February, although the base rate remained at 3.75%, four members voted for a 0.25% cut, indicating that the rising cost of living was expected to slow further.

But then the war in Iran changed everything. At the next MPC meeting on 18th March, all nine members voted to keep the base rate at 3.75% as rising global energy and commodity prices threatened to push inflation higher.

As a result, instead of expecting further cuts, markets began pricing in future rate rises. Bad news for borrowers, but good news for savers.

And although we are expecting to see inflation increase a little going forward, at the moment inflation has actually eased slightly to 2.85%, whilst savings rates have improved. This means that there are currently plenty of inflation busting accounts. For basic-rate taxpayers, a savings account paying at least 3.56% gross should still keep pace with inflation at 2.85% after tax. It’s trickier for higher and additional-rate taxpayers, as they need gross rates of at least 4.75% and 5.18% respectively.

Easy access savings

One provider has dominated the easy access market throughout the year. The Chase Saver with Boosted Rate has paid 4.50% AER since September last year and has topped the best-buy tables for much of that time.

But it won’t be suitable for everyone. The account must be opened through the Chase app and requires an eligible Chase current account. The headline rate also includes a 2.25% bonus for the first 12 months, so it's essential to review the account once that bonus expires.

Whilst the Chase account sits at the top of our best buy table, there are some other accounts that could also be considered for those with lower balances, looking to squeeze as much as they can from their savings.

Cahoot's Sunny Day Saver pays 5% AER on balances of up to £3,000, while Santander's Edge Saver pays 6% on up to £4,000, although it requires a fee-paying Edge Current Account, so it's important to check that the overall package represents good value.

If those accounts aren't suitable, there are still plenty of providers paying well above the rates available at the beginning of the year.

As well as the Sunny Day Saver, Cahoot is paying 4.32% on up to £500,000 on its Simple Saver account, which as the name suggests does not include a short term bonus or restricted access.

Ulster Bank also has an unrestricted Limited Edition Saver paying 4.30% AER. Even after basic-rate tax, these accounts continue to outpace current inflation.

Of course, easy access rates can change at any time, so review your account regularly and switch if it becomes uncompetitive.

Fixed-rate bonds

Bearing in mind that base rate has remained at 3.75% since December last year, it’s extraordinary to see how much fixed term bond rates have improved across all terms.

At the time of writing the top 1-year bond is paying 4.90% with Marcus: by Goldman Sachs, compared with 4.45% at the start of the year.

Longer-term bonds have also improved significantly. The top two and three-year bonds now pay 4.85%, up from around 4.20% at the start of the year, while the leading five-year bond has risen from 4.31% to 4.90%.

For anyone with cash they won't need in the near future, now could be a good time to lock in these higher rates. Competition has eased in recent weeks, suggesting the market may be approaching its peak.

Check out our Best Buy tables for the latest rates

Cash ISAs

Cash ISAs have continued to be popular this year, because higher interest rates have pushed more people into paying tax on their interest, as well as the significant changes announced in last year's Autumn Budget.

From April 2027, the annual cash ISA allowance for under-65s will fall from £20,000 to £12,000. At the same time, tax on savings interest will increase by 2%, taking the rates to 22% for basic-rate taxpayers, 42% for higher-rate taxpayers and 47% for additional-rate taxpayers.

It's no surprise, then, that cash ISA balances continue to grow. Bank of England figures show that between the end of November 2025 and the end of May this year, deposits increased by £34.3 billion, compared with £24 billion during the previous six months.

The good news is that cash ISA rates have also been on the up this year, which means there are a lot of competitive, inflation busting rates available.

Easy access cash ISAs

As with the non ISA easy access best buys, there has been plenty of good news for those prepared to shop around, especially for those happy to open and manage their accounts through an app.

Many of the market-leading rates continue to come from digital savings platforms such as Moneybox, Plum and Chip.

Although these aren't banks themselves, deposits are held with fully regulated UK banks and are protected by the Financial Services Compensation Scheme (FSCS). The important point is that protection applies to the underlying bank's licence, not the app,

The FSCS protects up to £120,000 per person per bank licence, and this limit applies to all the cash you hold with that bank in total. That means you must add together any money you hold directly with the bank and any money you hold with it through different apps.

Today, in our top five, the best two accounts are offered by Plum, (who deposits your funds via its partner banks CitiBank, Lloyds and QNB), and Chip whose partner banks include Barclays, Lloyds, HSBC, Qatar National Bank, Santander, National Bank of Kuwait and Nationwide Building Society. These providers are paying 4.44% and 4.42% respectively. A year ago, Plum was once again offering the best rate but that issue is paying 4.27% - so rates have improved.

Normally I would suggest moving your cash from a lower paying account, however because of the way the bonus works on the Plum ISA, if you close the account within 12 months, you will forfeit the bonus that is included in the headline rate. So, you to need make sure switching would still be the best option. This illustrates why it’s so important to always read the small print before opening any savings account.

If financial apps are not for you, there are some other competitive options. The Stafford Building Society, for example, is paying 4.36% on its Cash ISA Double Access account, although again the small print is all important. As the name suggests you can make just two penalty free easy access withdrawals a year – any more and the account will revert to the standard cash ISA which pays a lower rate.

Fixed-rate ISAs

Like fixed rate bonds, fixed term cash ISA rates have steadily increased so far this year, which means that there are many accounts comfortably outpacing inflation.

The top 1-year ISA has improved from 4.30% in January to 4.60% today, whilst the longer term ISAs have all improved from around 4.16% to 4.66% today. And because the interest is tax free, the returns are even more valuable for many savers.

At first glance, fixed-rate bonds often appear to offer better value because of their higher headline rates. However, once tax is taken into account, cash ISAs can provide a better return for anyone who has already used their Personal Savings Allowance.

For example, at the moment the top 1-year fixed rate bond is paying 4.90% AER, whilst the top 1-year fixed rate cash ISA is paying 4.60% tax-free/AER. For those who don’t pay tax on their savings, the bond is clearly the winner as it would provide an extra £30 of gross interest for each £10,000 deposited.

But if you are a taxpayer, you could earn more in the ISA. The rate on the bond would fall to 3.92% after basic rate tax (at 20%) has been deducted, so a basic rate taxpayer with a deposit of £20,000 would earn £920 in the cash ISA, but just £784 from the bond, if they have already used their Personal Savings Allowance.

What’s next?

At the latest MPC meeting on 18th June, there was a majority vote of 7-2 to keep base rate at 3.75%, with two members voting to increase to 4%.

Although energy prices and inflation have eased slightly in recent weeks, inflation is still expected to rise later this year as higher energy costs continue to pass through the economy.

Meanwhile, the increases to the top rates appear to have slowed suggesting that much of the expected movement in the base rate has already been priced into the market.

Of course, we’ll have to wait and see, but with many of today's best savings rates sitting at their highest levels for well over a year, now could be a good time to lock away some of your cash, if you won’t need access to it.

Inertia and inflation are the true enemies of the saver – and whilst you can’t control inflation, you can make your cash work as hard as possible in order to mitigate as much as possible of the damage that it can cause.

It’s simple; shop around, ditch and then switch to put more money in your pocket.

For the latest rates, visit our Best Buy tables.

Arrange a free initial consultation

Rates correct 08/07/2026

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

NS&I makes more rate hikes

Bearing in mind that the Bank of England maintained the base rate at 3.75% at its latest Monetary Policy Committee (MPC) meeting on 18th June, it was interesting to see that National Savings & Investments (NS&I) subsequently announced rate increases to its fixed rate savings accounts, Guaranteed Growth Bonds and Guaranteed Income Bonds – also known as British Savings Bonds.

What are the new NS&I Guaranteed Growth Bond rates?

- 1-year bond: up from 4.50% to 4.69% AER

- 2-year bond: up from 4.48% to 4.67% AER

- 3-year bond: up from 4.45% to 4.65% AER

- 5-year bond: up from 4.40% to 4.55% AER

Whilst inflation has remained steady in the 12 months to May 2026 at 2.80%, we still expect inflation to jump up a little in the near future, as the effects of the war in the Middle East bite – and we know that the energy price cap increased by 13% this month!

However, the expectation that the base rate would remain the same this month is reflected by the slowdown in savings rate hikes that we’ve seen recently. So, it’s good news that NS&I is getting in on the action.

As well as reacting to the rest of the market, NS&I also adjusts rates it is offering, to manage the flow of funds into the state-owned Bank, to help it meet its Net Financing Target - the amount it is tasked with raising for the Government each tax year after taking account of both deposits and withdrawals.

The target has been increased from £13.6 billion to £15 billion for the 2026/27 tax year. In addition, the recent revelation that some bereaved families had not received all the money due from deceased relatives’ NS&I accounts, may have prompted higher than usual withdrawals. According to the Bank of England, some £160million was withdrawn in the first month of the tax year.*

Be aware if you choose the monthly income option

The British Savings Bonds offer a choice between having the interest paid monthly as income, or allowing it to roll up and be paid at maturity.

That choice is worth thinking about carefully, particularly if you pay tax on your savings.

If you choose to have the interest added to the bond each year so that it compounds, you won't receive it until the bond matures, which could be more important in longer term bonds. For tax purposes, that means all the interest is treated as being received in the tax year in which the bond ends.

Because your Personal Savings Allowance (PSA) can't be carried forward, receiving several years' worth of interest in one tax year could mean you exceed your allowance and pay tax on some of the interest. In some cases, it could even push you into a higher tax band for that year.

It won't affect everyone, but it's certainly something worth considering before deciding how you'd like your interest paid.

Are the new rates competitive?

The latest increases undoubtedly make NS&I more competitive, especially when compared with many of the high street banks.

However, savers prepared to look beyond the familiar names can still find significantly better returns elsewhere.

For example, a £50,000 deposit for 12 months would earn £2,345 (before the deduction of tax) with NS&I’s 1-year bond, compared with £2,450 with Marcus: from Goldman Sachs, which currently pays 4.90% AER.

It's the same with the longer fixed terms. The top 2-year bond is paying 4.86% versus the NS&I bond paying 4.67% Over 3-years, the top rate is 4.85% compared to 4.65% with NS&I and over 5-years you can earn up to 4.90% compared to NS&I’s option which is now 4.55% AER

So, whilst NS&I’s new rates have improved, they don’t make it into the best-buy tables.

Despite rarely topping the tables, NS&I continues to benefit from huge customer loyalty. A key reason is its unique Government guarantee. Every penny held with the provider is backed by HM Treasury, giving savers complete protection, regardless of how much they hold.

You can invest £500 up to £1 million into each issue of the British Savings Bonds, making them particularly appealing for those with larger sums who prioritise safety over the best returns.

For most savers, though, whose balances fall below the £120,000 Financial Services Compensation Scheme (FSCS) protection limit that applies to all other regulated and authorised banks and building societies, there are still better-value options elsewhere.

*Bank of England Table A7.1 (changes tab)

For the latest rates, visit our Best Buy tables.

Arrange a free initial consultation

Rates correct 02/07/2026

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions. The Financial Conduct Authority (FCA) does not regulate tax advice.

Fixed rates near their peak?

The latest inflation figures are out and surprisingly the Consumer Prices Index (CPI) remained at 2.8% for the 12 months to May 2026. That said, we still expect inflation to jump up a little in the near future, as the effects of the war in the Middle East bite – and we know that the energy price cap is set to increase by 13% in July!

But this latest inflation news means that it’s no real surprise that the Bank of England’s Monetary Policy committee (MPC) held the base rate at 3.75% this month.

Seven of the nine members voted to hold although there were two members who supported a rate rise as they are concerned that higher energy costs could lead households and businesses to expect inflation to stay higher for longer, which could push up wages and prices more generally. They believed a small increase now would help keep inflation expectations under control and reduce the risk of inflation remaining above target in the future.

Nevertheless, the expectation for the base rate to stick is reflected by the slowdown in savings rate hikes that we’ve seen recently; we’ve even seen a few reductions of late. However, there are still plenty of really competitive rates available - so for those looking to lock away some of their cash, it's time to get a move on!

What’s been happening to rates?

At the beginning of the year, we were expecting to see some base rate cuts throughout 2026 as there were signs of inflation easing. But the war in Iran which started at the end of February overturned that sentiment, and the markets expected the Bank of England to start hiking interest rates instead.

As a result, fixed-term savings rates started to rise in anticipation. So, let’s take a look at what’s happened so far;

Fixed Rate Bonds

Since the beginning of the year the top fixed savings rates have soared, even though the Bank of England base rate has remained at 3.75% since December last year.

In the 1-year table, in January the top rate was 4.45% with Union Bank of India and the average of the top five was 4.30%. But rates have increased steadily and at the time of writing you can now earn up to 4.85% with MBNA.

The increase has been even more dramatic in the longer-term tables.

At the beginning of the year, the top 2-year bond was paying 4.20% and the top 3-year available was 4.21%. Today you can earn as much as 4.85% with the app-only bank Afin Bank for both terms.

And over five years, the top rate available has increased from 4.31% six months ago, to 4.90% today, once again with Afin Bank.

For those who would prefer not to use an app to open an account, the rates are not too much lower. The top 2-year online account is with GB Bank paying 4.82%, the top 3-year and 5-year online accounts are with Oxbury Bank paying 4.83% and 4.88% respectively.

Fixed Rate ISAs

From April 2027, the amount that the under 65s will be able to deposit into a cash ISA will fall to £12,000. This has boosted their popularity, as those who can afford to make use of the full £20,000 allowance whilst it’s still available have rushed to do so. So, it’s good to see that the top rates available have reacted to market expectations too.

The top 1-year ISA today is 4.68% with Investec, up from 4.30% in January whilst once again the increases have been even higher for the longer-term accounts.

At the moment you can still secure a rate of 4.72% for 2-years and 5-years, whilst the top rate for a 3-year ISA is 4.68%. But when you consider that at the beginning of the year you could earn just 4.16%, that’s a significant improvement – and one to take advantage of if you can.

Of course, it looks as though the ISA rates are worse than the equivalent fixed rate bonds, but if you pay tax on your savings, then the tax efficient nature of the ISA becomes more obvious. Whilst the top 1-year bond is paying 4.85% AER, higher than the ISA rate of 4.68%, if you deduct tax from the return, the ISA can produce a far better return.

Let’s assume a deposit of £20,000. If you were to put this into the 1-year bond, this would produce £970 in gross interest. If you have already fully utilised your Personal Savings Allowance however, you would have to pay 20% tax on this amount which is £194, giving you a net amount of £776. If this £20,000 were in the cash ISA however, the tax-free return would be £936 – so you would take home more, even though the headline interest rate is less.

And let’s not forget that the tax on savings interest is increasing to 22% from April 2027.

For many a stocks and share ISA is the preferred choice and over the longer term is likely to provide a better return, but for those who are not currently using their full ISA allowance and have savings in taxable accounts, it makes sense to be as tax efficient as possible. So don’t waste the allowance as if you don’t use it, you will lose it.

Are the good times over?

There’s been a marked slowdown in activity in the fixed rate bond and ISA tables recently and we’ve even seen a few top paying accounts withdrawn, and in some cases replaced with lower paying issues.

So, for those who have been thinking of locking some of their cash away, taking action sooner rather than later could prove worthwhile. While nobody can predict exactly where rates will go next, today's best buys already reflect much of the market's expectation for higher inflation and interest rates.

For the latest rates, visit our Best Buy tables.

Arrange your free initial consultation

Rates correct 19/06/2026

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions. The Financial Conduct Authority (FCA) does not regulate tax advice.

Investment returns are not guaranteed, and you may get back less than you originally invested.

Stocks & Shares ISAs to face 22% tax next year

Rachel Reeves is expected to bring in a 22 per cent tax charge on interest generated from cash held within stocks and shares ISAs , with the changes due to come into force next April.

From April 6, 2027, savers under 65 will see their cash Isa allowance reduced to £12,000, although the overall £20,000 Isa limit will still be available through a stocks and shares Isa.

The Chancellor first signaled the policy in last year’s Budget, presenting it as a measure designed to encourage greater investment in the UK and to prevent savers from using their stocks and shares ISA as surrogate cash ISA after the cash ISA allowance reduction. However, until now, few details had emerged about how the revised system would work in practice.

Now, as part of the new “anti-circumvention rules”, investors will pay a 22 per cent charge on interest earned from cash balances held in stocks and shares ISAs from April 2027.

The proposal echoes the Isa rules that existed before 2014, when cash interest inside stocks and shares ISAs attracted a 20 per cent charge. Under the updated regime, the levy would match the savings interest tax rate, which is set to rise to 22 per cent in April 2027.

HM Revenue & Customs (HMRC) had already indicated that interest on cash held in stocks and shares ISAs would become subject to a charge from that date, although it had not previously specified the rate that would apply.

What is an ISA?

An ISA, or ‘Individual Savings Account’, is a scheme that allows anybody to hold cash, shares and unit trusts free of tax on dividends, interest, and capital gains. Essentially, it’s a savings account that you don’t pay tax on.

A Stocks and Shares ISA is a tax-efficient investment account that allows you to put your money into a range of funds in various asset classes, with the goal of hopefully achieving better long-term returns than you might from a traditional savings account.

Unlike a Cash ISA, which simply protects your interest from tax, a Stocks and Shares ISA puts your money to work in the financial markets. This means you can invest in things like funds, shares and bonds, while still benefiting from the ISA’s tax-free account status (or ‘wrapper’).

You can save up to £20,000 each tax year across ISAs and receive tax-free interest payments, so when the value of your cash ISA increases, you get to keep all of it tax-free. However, it’s important to note that from April 2027, the annual allowance for the cash ISA specifically will be reduced to £12,000 for those under 65.

While there is a £20,000 allowance in place for how much you can put in a year, there is not a cap on how much you can accumulate in an ISA over a lifetime.

When choosing a style of investment to suit your needs, you may want to consider how long you plan to invest for and how much you would like your money to grow. It is also important to understand what movement in value you may or may not be happy with and any potential losses that may happen. That is why soliciting professional advice can be crucial for understanding how to take those first steps towards a secure financial future.

If you want to find out more, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our chartered advisers to see how we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash or tax advice.

Investment returns are not guaranteed, and you may get back less than you originally invested. Past performance is not a guide to future returns.

Inflation drops to 2.8%... but can it last?

The rate of inflation in the UK has dropped more than anticipated to 2.8% in the year to April, according to the latest figures from the Office for National Statistics (ONS). This is a notable drop from the 3.3% figure in the year to March.

Inflation continued to ease even as fuel costs climbed in the wake of the Iran conflict.

Data from the ONS showed petrol averaged 156.8p per litre last month, marking its highest level since November 2022. Diesel prices also jumped by more than 30p in April, pushing the average cost up to 190p per litre, the highest recorded since July 2022.

According to the RAC, petrol prices have continued to rise in May, reaching a new peak of 158.52p per litre on Tuesday.

So why has inflation fallen this time, and will it stick?

According to the ONS, energy costs had fallen thanks to a combination of reduced wholesale prices and the government’s energy bill support measures introduced before the Iran conflict began.

But economists are warning that inflation is likely to be on the rise again soon, potentially hitting around 4% by the end of the year, with ongoing tensions in the Middle East continuing to drive up global prices.

It’s also important to note that it can often take about a year for food supply cost changes to truly be reflected in food prices in the UK, so there are likely to be some price shocks as the economy catches up to the supply chain issues caused by the conflict.

What is inflation and how is it measured?

Inflation is a measure of how the prices of goods and services have increased over time. Goods are tangible items sold to customers, such as food, while services are tasks performed for the benefit of recipients, such as a haircut. Generally, this increase is measured by considering the cost of things today compared to how much they cost a year ago. The average increase between these prices is demonstrated in the inflation rate.

Rising inflation directly affects the cost of living. For example, if the price of a bottle of milk is £1, and inflation is increasing by 5%, then your bottle of milk will cost you 5p more. Or, in other words, the spending power of your money has decreased by 5%.

Ideally, the Government wants to keep inflation low and stable. The general mandated target for the Bank of England is 2%.

Anything significantly above or below this target is thought to cause issues for the economy.

The cost of living surged in recent years, with inflation peaking at 11% in 2022 - way above the Bank of England's 2% target, partly due to the increase in energy prices following Russia's invasion of Ukraine.

While the rate has dropped, falling inflation does not mean the goods and services are coming down in price overall, it is just that they are rising at a slower pace.

Our chartered financial advisers are expert and unbiased, meaning that they can give whole of market advice, and so are best placed to give you a plan tailored exactly to your personal financial goals.

If you’d like to know more, request a free non-committal initial consultation with one of our team or give us a call on 0333 323 9065 and get in touch.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

What is the Personal Savings Allowance?

The Personal Savings Allowance (PSA) is the amount of interest you can earn on your savings each tax year without paying tax on it. It applies to interest from ordinary savings accounts and similar products held outside an ISA (Individual Savings Account).

For many people, it means their bank interest is covered automatically. However, higher interest rates and larger cash balances mean more savers now need to pay attention to it.

Arrange your free initial consultation

How much is the Personal Savings Allowance?

How much you get depends on your Income Tax band. If you are a basic rate taxpayer, your Personal Savings Allowance is £1,000. If you are a higher rate taxpayer, it is £500. If you are an additional rate taxpayer, it is £0.

This matters more than it used to because savings rates have been much healthier in recent years. When interest rates were very low, many people did not come close to using their allowance. Now, a relatively sizeable balance in a competitive account can create enough interest to bring the allowance into play. For example, £25,000 in an account paying 4% will produce £1000 of interest per year

You should also remember that HMRC works out your tax band by adding your savings interest to your other income. So, if you are close to the higher rate threshold, your interest could push you into the higher rate band for income tax. That does not mean you should avoid earning interest, but it does mean you should know where you stand before the end of the tax year.

What interest is covered by my Personal Savings Allowance?

Your Personal Savings Allowance covers taxable savings interest which usually means interest from bank and building society accounts that are not sheltered inside an ISA. It can include interest from easy access accounts, fixed rate bonds, notice accounts, regular savers and current accounts that pay interest. It also includes interest payments (coupons) received from gilts.

It can also include interest from some other savings products, so it is worth checking the tax position before assuming that interest is outside the rules. HMRC’s guidance is pretty clear though, that the allowance applies to savings interest, and that the level of allowance depends on your Income Tax band.

The key word here is interest. The allowance is not designed for dividends from shares, rental income, capital gains or investment growth. Those areas have their own rules and allowances. But, if you have several different types of income, it is sensible to look at the whole picture rather than treating your savings in isolation.

What is the ISA allowance vs the Personal Savings Allowance?

A cash ISA, or Individual Saving Account, and the Personal Savings Allowance both help you reduce tax on savings, but they work in very different ways.

The ISA allowance is the amount you can pay into ISAs each tax year. For the current tax year, which runs from 6 April 2026 to 5 April 2027, you can save up to £20,000 into ISAs. You can put that into one ISA or split it across different types of ISA, within the rules. GOV.UK also confirms that money kept in ISAs remains tax free while it stays inside the ISA wrapper.

The Personal Savings Allowance, by contrast, applies to interest on taxable savings accounts outside cash ISAs. Most banks and building societies pay your interest Gross of tax – i.e. they do not take off any tax that may be payable to HMRC. So the Personal Savings Allowance simply gives you a band of savings interest that is taxed at 0 percent, provided you qualify for the allowance.

A cash ISA can therefore be useful if you are already fully using your Personal Savings Allowance, if you expect to use it in future, or if you want to build a pot where the interest does not need to be considered for savings tax. For lower balances, a standard savings account may still be attractive, especially if it pays a better rate and the interest you earn remains within your allowance. The right answer is not always “ISA first”. It depends on your tax position, your balance, the rate on offer and whether you are likely to become a higher rate taxpayer.

What happens if I go over the UK Personal Savings Allowance?

If your savings interest goes over your Personal Savings Allowance, only the excess is taxable. You do not lose the allowance altogether, unless you become an additional rate taxpayer. You should also be aware that if you become a higher rate taxpayer, your Personal Savings Allowance will half, to £500.

In many cases, HMRC collects the tax automatically by changing your tax code. This often applies if you are employed or receive a pension through PAYE. If you already complete a Self Assessment tax return, you usually report the savings interest there. Banks and building societies normally pay interest without deducting tax, so it is your overall tax position that decides whether anything is due.

The rate of tax depends on the band the interest falls into. At present, savings income is taxed at the same rates as Income Tax for basic, higher and additional rate taxpayers, although the Government has announced that tax rates on savings income will rise by two percentage points from April 2027. This means that a basic rate taxpayer will pay 22%, a higher rate taxpayer will pay 42% and an additional rate taxpayer will pay 47% tax on savings income.

Going over the allowance does not result in paying a fine or penalty. It simply means some of your interest becomes taxable. From a `planning point of view, it may be a prompt to review whether more of your cash should sit in ISAs, whether a spouse or civil partner has unused allowances, or whether your savings are spread in the most tax efficient way.

Does all interest count towards the Personal Savings Allowance in the UK?

Not quite, as some interest is already tax free and does not need your Personal Savings Allowance. Interest earned inside a cash ISA is the most common example, because ISA interest is sheltered from Income Tax, regardless of how much. Premium Bond prizes are also tax free, although they are prizes rather than interest.

Interest from ordinary savings accounts usually does count. That includes accounts with banks, building societies and National Savings and Investments products where the interest is taxable. The exact treatment can vary by product, so it is worth checking before you commit a large sum.

You should also be aware of the starting rate for savings, which can help people on lower incomes. The starting rate for savings can be up to £5,000, but every £1 of other income above your Personal Allowance reduces it by £1. This is separate from the Personal Savings Allowance and can be very valuable if your income from work or pensions is modest.

This is one of the areas where people can accidentally underestimate their position. Someone with a low income may be able to receive more savings interest tax free than they expected, because the Personal Allowance, the starting rate for savings and the Personal Savings Allowance can all interact.

Is the Personal Savings Allowance in addition to my Personal Allowance?

Yes. The standard Personal Allowance is £12,570 for the 2026 to 2027 tax year. This is the amount of income most people can receive before paying Income Tax. But the Personal Allowance reduces once adjusted net income goes above £100,000 and is lost completely at £125,140 or above.

The Personal Savings Allowance sits alongside the Personal Allowance, but it is not quite the same type of allowance. Technically, it gives eligible savings income a 0 percent tax rate but - that savings income within the Personal Savings Allowance still counts as taxable income, even though it is taxed at 0 percent.

That distinction can matter if your income is close to a tax threshold. Your interest may not create a tax bill in itself, but it can still form part of the calculation that decides which tax band you fall into.

Used well, the Personal Savings Allowance is a useful part of your savings toolkit. It should not be viewed in isolation, though. The best approach is to know your tax band, check how much interest your savings are likely to generate, compare taxable accounts with cash ISAs, and make sure your money is working hard without creating avoidable tax.

If you’d like to find out more or want to see how you can structure your savings and investments in the most tax efficient way, why not get in a touch for a free initial consultation.

Arrange your free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

More winners and better rates from NS&I

Hot on the heels of an increase to the NS&I British Savings Bonds rates, which happened at the end of last month, NS&I has now announced a further boost for savers, with improvements to Premium Bonds and increases to rates across four of its variable savings accounts.

Immediate increases to NS&I variable rate savings accounts

The changes occurring immediately are increases to the easy access Direct Saver and Income Bonds accounts, as well as the tax-free Direct ISA and Junior ISAs.

The new rates are:

| Product | Previous Rate | New Rate |

|---|---|---|

| Direct Saver | 3.05% gross/AER | 3.45% gross/AER |

| Income bonds | 3.01% gross/AER | 3.40% gross/AER |

| Direct ISA | 3.50% gross/AER | 3.80% gross/AER |

| Junior ISA (JISA) | 3.55% gross/AER | 3.70% gross/AER |

Whilst a decent improvement, especially given that the base rate has remained at 3.75% since December last year, these rates can be easily beaten elsewhere, with plenty of easy access accounts and easy access cash ISAs paying over 4%, and the top JISA with the Leek Building Society is paying 3.75%.

Take a look at our Best Buy tables to find the top rates currently available.

Savings rates have remained buoyant recently as there is a real likelihood that the Bank of England will need to raise interest rates in the near future, to try and control inflation.

Premium Bond boost

In addition to these rate hikes, from the July 2026 Premium Bonds draw, the prize fund rate will rise from 3.30% to 3.80% tax-free, while the odds of winning will improve from 23,000 to 1 to 22,000 to 1 for every £1 Bond held.

The changes reverse the reductions introduced in August last year and April 2026, bringing the prize fund rate back to the level it was a year ago. And it will be welcomed by the more than 22 million Premium Bonds holders across the UK.

More prizes every month

The increase in the prize fund rate means that NS&I expects to pay out around 322,000 extra prizes each month compared to the May 2026 draw.

In total, the July 2026 draw is expected to pay out around £436.8 million in prize money, up from £376.2 million in May.

There will still be two £1 million jackpot winners every month, and the number of higher-value prizes will increase. NS&I estimates there will be:

- 12 additional £100,000 prizes

- 24 more £50,000 prizes

- 49 extra £25,000 prizes

The number of £100 and £50 prizes will also rise sharply, helping to spread more winnings across a larger number of bondholders.

What are Premium Bonds?

Premium Bonds remain one of the UK’s most popular savings products. But, rather than paying interest in the traditional way, each £1 Bond is entered into a monthly prize draw where savers can win tax-free prizes ranging from £25 to £1 million.

Up to £50,000 per person can be held in Premium Bonds, including for children under 16, and you can have access to the funds should you wish.

For many savers, the appeal is the combination of complete security but mainly the ‘what-if’ factor. The excitement that, however unlikely it is, as well as one of the smaller prizes you might just be one of the lucky few to win one of the big ones!

However, unlike a traditional savings account, the risk is that you may win nothing at all – and many bondholders will earn less than the headline prize fund rate.

Although on the face of it, the rate of 3.80% looks less competitive as you can easily earn more than 4% on an easy access account elsewhere, if you pay tax on your savings interest, you’d be hard pressed to find an equivalent savings account paying as much.

For example, if you were to win the equivalent of the new prize fund interest rate of 3.8% tax free, as a basic rate taxpayer this rate is the equivalent of earning 4.75% on a taxable easy access account, 6.33% if you are a higher rate taxpayer and 6.91% for additional rate taxpayers!

So, even though savings rates remaining competitive and inflation is still a concern for many households, the higher prize fund rate and improved odds are likely to reinforce Premium Bonds’ popularity – especially for taxpayers.

As always though, savers should review their wider cash savings strategy regularly to ensure their money is working as hard as possible.

Arrange your free initial consultation

Please note: This article is intended for general information only and does not constitute individual financial advice.

The Financial Conduct Authority (FCA) does not regulate cash or tax advice.

NS&I hikes rates on British Savings Bonds

National Savings & Investments (NS&I) has announced rate increases across its Guaranteed Growth Bonds and Guaranteed Income Bonds – otherwise known as British Savings Bonds. This announcement came just ahead of the latest Bank of England Monetary Policy Committee (MPC) meeting, where the base rate was held at its current level of 3.75%.

What is telling however, is how the votes went at this meeting compared to the last. On 19th March, just three weeks into the conflict in the Middle East, the MPC voted to keep base rate on hold, following six previous cuts since August 2024. At that stage, the vote was unanimous – with all nine members on the same page.

But with the ongoing conflict, which has seen the price of fuel rocket upwards and with inflation expected to tick up further, one of the members, Huw Pill, voted for an increase this time around, which means the possibility of a rate hike has far from gone away.

In fact, the markets are now expecting to see two or three rate rises this year! A complete turnaround from a couple of months ago, when the trajectory was downwards.

Whilst bad news for those with debt, this news has seen a boost for savers, as savings rates have improved significantly, especially fixed rate accounts. At the beginning of February 2026, before the conflict began, the top 1-year fixed rate bond available was 4.25% - today you can earn 4.67% with Kent Reliance. Similarly, over 5-years the top rate available has increased from 4.31% to 4.70% which is available via two providers, GB Bank and the Market Harborough Building Society.

Things are changing fast though, so keep an eye on our Best Buy tables for the current rates.

Even NS&I is getting in on the action

The new issue of the NS&I 1-year British Savings Bond has increased from 4.07% to 4.50% AER, whilst the 2-year bond has increased from 3.98% to 4.48%. The 3-year bond has increased from 4.02% to 4.45% whilst the 5-year bond has seen the lowest increase, from 4.05% to 4.40%.

The bonds also have a monthly interest option, giving savers the choice of either a regular income or to have all the interest paid at the end of the term. This choice can be important though, particularly for those who pay tax on their savings.

With the longer-term bonds, if you opt to have the interest added to your bond each year and left to compound, it won’t be accessible until maturity. And from a tax perspective, that means the interest will be treated as if it were received in one go at the end.

This matters because you can’t spread the interest over the term for tax purposes, and your Personal Savings Allowance (PSA) can’t be carried forward from one year to the next. So, if your total interest in the maturity year exceeds your PSA, you could find yourself paying tax on the excess – and possibly nudged into a higher tax band too, for that tax year.

For many savers this might not have a major impact, but it’s well worth keeping in mind.

Why is NS&I increasing rates now?

Whilst these increases could be a reaction to the rest of the market, NS&I often changes the rates it is offering, to either increase or stem the flow of funds into the state owned Bank, in order to meet its Net Financing Target. This is the amount NS&I is tasked with raising on behalf of the Government each tax year – and takes into account both inflows and outflows. For the 2026/27 tax year, that target has been increased from £13.6 billion to £15 billion. In addition, the back-office issue that was recently unearthed, that many families had not been repaid all the funds from their loved one’s accounts following a bereavement claim, may have led to some withdrawing their funds, which will need to be replaced.

Are the new rates competitive?

These latest rates are certainly more competitive, particularly compared to the high street names. Currently the 1-year bonds available from the main high street providers pay between 3.15% (Lloyds Bank) to 4% (Nationwide).

However, there are still better-paying options available for those happy to look beyond the household names, as the table show. For example, a £50,000 deposit for 12 months would earn £2,250 (before the deduction of tax) with NS&I’s 1-year bond, compared with £2,335 with Kent Reliance, which as mentioned above is currently paying 4.67%.

NS&I Guaranteed Growth Bonds (British Savings Bonds) vs the best accounts available

| Term | Account Name | Minimum deposit | Maximum deposit | AER | Annual interest on a deposit of £50k |

| 1 Year | NS&I British Savings Bond Iss 89 | £500 | £1,000,000 | 4.50% | £2,250.00 |

| 1 Year | Kent Reliance | £1,000 | £1,000,000 | 4.67% | £2,335.00 |

| 2 Year | NS&I British Savings Bond Iss 77 | £500 | £1,000,000 | 4.48% | £2,240.00 |

| 2 Year | Kent Reliance | £1,000 | £1,000,000 | 4.69% | £2,345.00 |

| 3 Year | NS&I British Savings Bond Iss 79 | £500 | £1,000,000 | 4.45% | £2,225.00 |

| 3 Year | Kent Reliance | £1,000 | £1,000,000 | 4.66% | £2,330.00 |

| 5 Year | NS&I British Savings Bond Iss 71 | £500 | £1,000,000 | 4.40% | £2,200.00 |

| 5 Year | GB Bank | £1,000 | £100,000 | 4.70% | £2,350.00 |

So, whilst NS&I’s new rates are a marked improvement, they don’t make it into the best-buy tables.

Despite rarely offering the top rates, NS&I continues to attract huge loyalty based on its longevity and unique protection. Every penny held with the provider is 100% backed by HM Treasury, offering unmatched peace of mind. You can invest up to £1 million into each issue of these bonds, making it particularly appealing for those with larger sums who prioritise safety over the best returns.

For most savers, though, whose balances fall below the £120,000 Financial Services Compensation Scheme (FSCS) protection limit that applies to all other regulated and authorised banks and building societies, there are still better-value options elsewhere.

Arrange your free initial consultation

Rates correct at 01/05/2026

This article is for information only and does not constitute individual advice.

The Financial Conduct Authority (FCA) does not regulate cash or tax advice.