Skip to main content

Skip to main content

Understanding the Current State of the World Economy and Markets

Inflation, Growth, Equities, and Fixed Income

As the first quarter of 2023 has now drawn to a close, we look back on how events in global markets have influenced the current state of the economy. The shock waves in the banking sector have had a heavy impact across the economy, so 2023 will see markets trying to recover.

Inflation has fallen, but remains above central bank targets, whilst economic growth has slowed resulting from contractions to bank lending. Equities are at or below long-term average valuations, and corporate profits are expected to show weak growth in 2023. To add further fuel to the fire, the shock waves in the banking sector have left fixed income markets in a highly volatile state, however, not all is negative, with most of these income markets posting positive Q1 returns.

Inflation

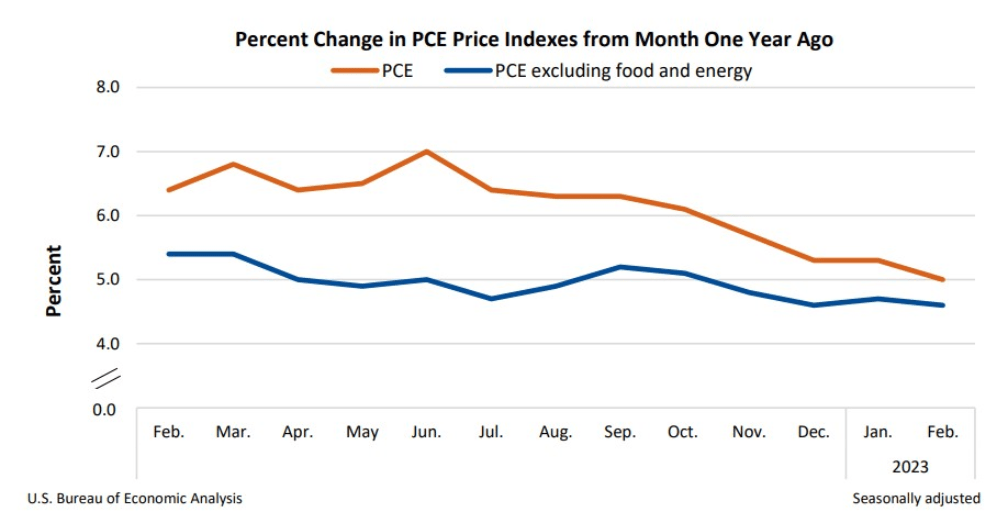

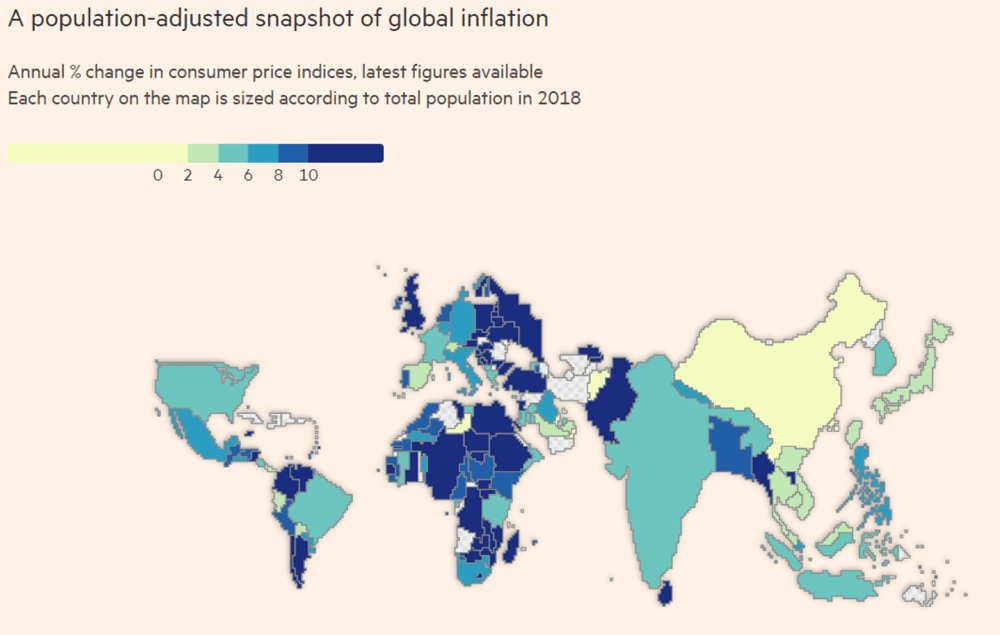

Inflation is an important indicator of the health of an economy. The US Core PCE (Personal Consumption Expenditures) is the inflation measure that the Federal Reserve looks at when setting policy. This measure excludes food and energy prices and shows the year-on-year changes in prices - see figure 1. The most recent figure shows that inflation has been coming down slowly but surely, but it's still above the Fed's target of 2%. The month-on-month figure is at 0.3%, which annualises to about 3.6%. This is below the year-on-year figure but still higher than the Fed's target. It's important to note that inflation is not just a US phenomenon, but a global one, with many countries experiencing high inflation – see figure 2.

| 2022 | 2023 | ||||

|---|---|---|---|---|---|

| October | November | December | January | February | |

| Headliner PCE | 0.4 | 0.2 | 0.2 | 0.6 | 0.3 |

| Core PCE | 0.3 | 0.2 | 0.4 | 0.5 | 0.3 |

Figure 1. Core PCE Inflation. (Source: BEA, 2023)

Figure 2. Global Inflation heatmap. (Source: FT, 2023)

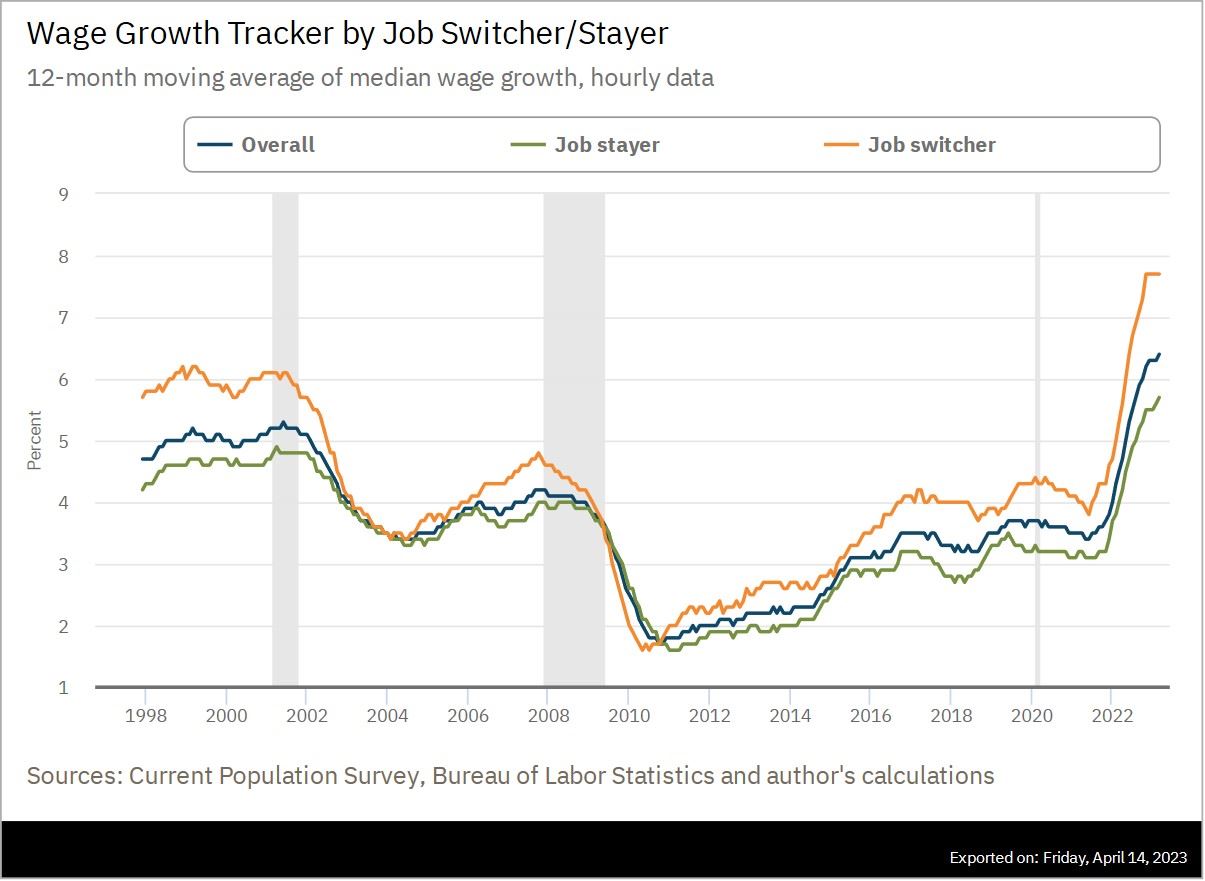

Wages are one of the main drivers of inflation, and US wage gains have been substantial, particularly for job switchers, despite the labour market having slowed slightly – see figure 3. This indicates that the labour market remains very tight and appears resilient despite the Fed increasing interest rates.

Figure 3. US Wage Growth. (Source: Atlanta Fed, 2023)

Growth

Growth is another important indicator of an economy's health. The Atlanta Fed's GDP Now estimate – see figure 4 – shows that the US economy is still growing at a healthy real rate of 2% (i.e. taking into account inflation). However, the green line on the graph shows that growth has started to slow down after the banking crisis, which caused credit creation to decline and banks to stop loaning out as much money. Although growth estimates remain high, there's an expectation that growth is likely to slow as a result of the banking crisis.

Figure 4. US Q1 2023 Real GDP Estimate. (Source: Atlanta Fed, 2023)

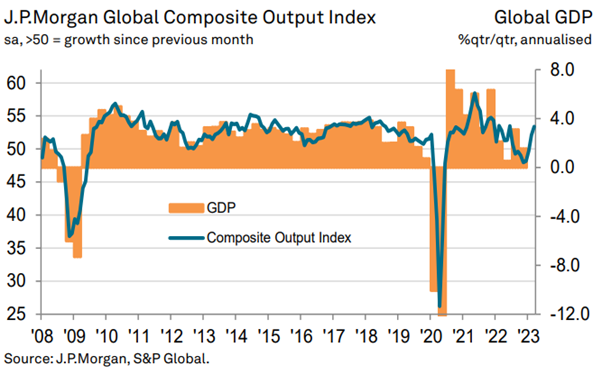

On a global level, GDP figures show a slowdown going into last year, but the PMI (Purchasing Managers' Index) has picked back up – see figure 5 - particularly in China where the government is starting to stimulate the economy again. In the first quarter of this year, China spent more on railway investment than at any point in history, indicating that they are pushing for growth.

Figure 5. Global Composite PMI and Global GDP Growth. (Source: JPM/S&P Global, 2023)

Equities

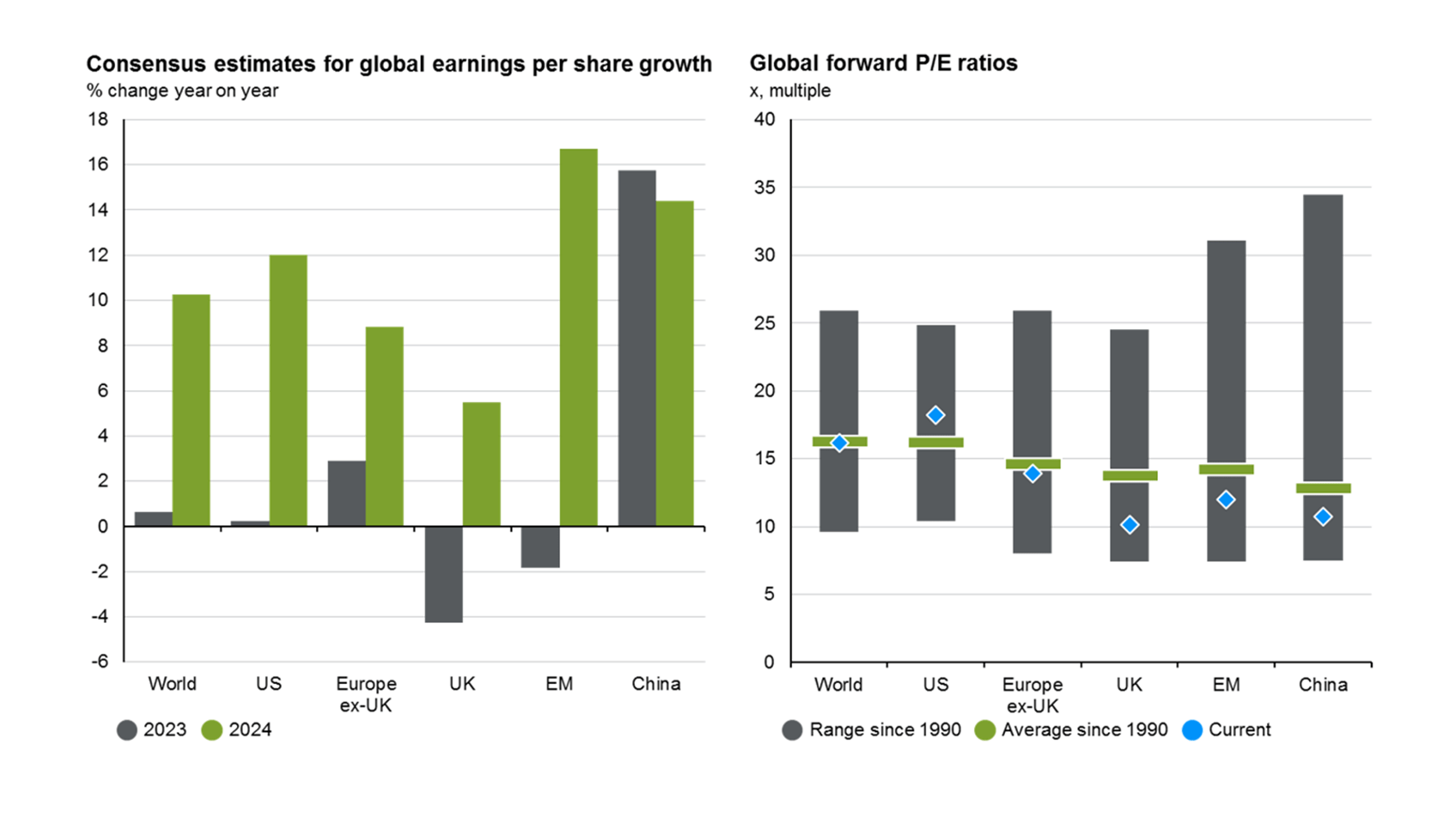

Figure 6. Global equity earnings expectations and valuations. (Source: JPM, 2023)

Equities, or stocks, are a way for investors to invest in the growth potential of companies. Corporate earnings growth is a key indicator of the health of the equity markets. The grey bars on the left-hand graph show expected earnings growth for 2023, and the green bars show expected earnings growth for 2024. The US market is expected to have weak earnings growth this year, barely above 0%. Europe is expected to have a good year in 2023, bouncing back from a poor year in 2022. Emerging markets, however, are not expected to perform as well.

Fixed income

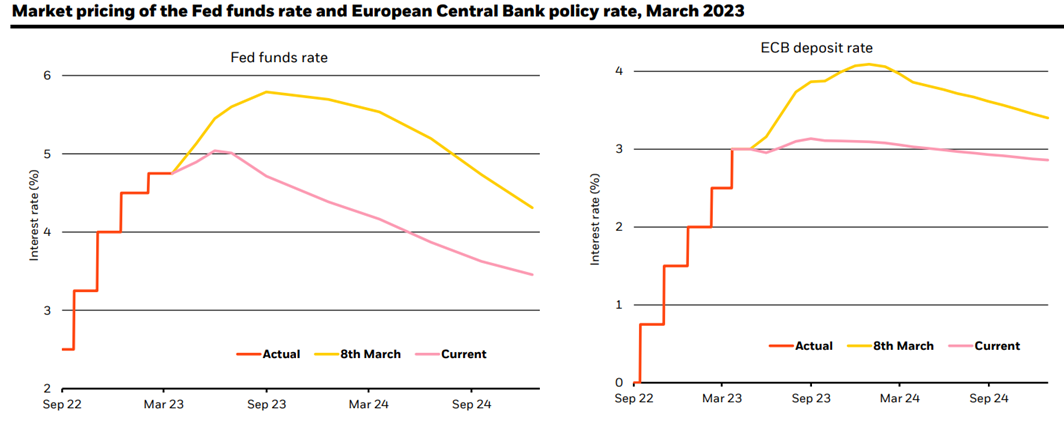

Figure 7. Market expectations of short-term interest rates. (Source: Bloomberg, 2023)

The first quarter of 2023 brought positive returns to the bond market in most markets. UK gilts rose 2.2%, US Treasuries increased slightly, while Japanese government bonds fell due to uncertainty over the Bank of Japan's yield curve control policy. In the corporate bond space, investors in higher credit quality and longer-dated issuances, such as those found in the investment grade space, performed well due to volatility in Silicon Valley Bank (SVB) and Credit Suisse. Meanwhile, European high yield was down, reflecting its larger allocation to banking debt and its challenging period.

Central banks continued to raise rates in Q1. The Federal Reserve raised rates twice, the Bank of England raised rates in February and March, and the European Central Bank raised rates by 1% in Q1. This led to investors moving into shorter-dated government bonds due to their higher credit quality, low duration risk, and the belief that central banks may be less inclined to raise rates further.

Investor expectations for interest rates have changed since March – see figure 7 - with investors becoming more concerned about the impacts of higher rates on the economy. The markets are forecasting rate cuts, but the Fed remains relatively hawkish and is keeping the rates high for longer. The argument is that it's easier to raise rates when inflation is high, but with headline inflation falling and core inflation being more sticky, the argument becomes a lot more difficult.

The market is attempting to call the Fed's bluff on their hawkish stance, but for this scenario to materialise and for the Federal Reserve to cut interest rates, there would have to be a harder landing in the US and a more entrenched recession. While there has been no sign of a significant downturn in the US economy yet, the slowdown in credit creation and falling liquidity is cause for concern.

Conclusion

In summary, the world economy is facing challenges related to inflation, growth, and equity earnings. Inflation remains higher than the Fed's target, with wages being one of the main drivers of inflation. The US economy is still growing at a healthy rate, but growth is likely to slow down because of the banking crisis. China is pushing for growth, but other emerging markets are not expected to perform as well. The equity markets are also facing challenges, with weak expected earnings growth for the US market this year.

Understanding these indicators is essential for investors and policymakers to make informed decisions about the global economy and equity markets. This creates uncertainty moving forward, so whilst we maintain a constructive view on asset classes over the medium term, we do expect elevated volatility moving forward.

Please contact your adviser if you require assistance, or if you're looking to get started and have £100k or more in investable assets, arrange your free initial consultation.

Arrange a free initial consultation

Note: This Market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Additionally, past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.