Skip to main content

Skip to main content

Markets react to rising Middle East tensions

At the start of the year, we described geopolitical risk as a “known unknown.” We expected geopolitics to play an important role in shaping markets, but the timing and scale of any escalation were uncertain. Only two months into the year, that risk has materialised in dramatic fashion, with global geopolitical tensions now reaching their highest level in more than 20 years (see Figure 1).

This sharp rise in tensions has quickly become the dominant theme for global markets and investors.

Figure 1: Geopolitical Risk Index (Source: Caldara and Iacoviello, March)

Figure 1: Geopolitical Risk Index (Source: Caldara and Iacoviello, March)

Arrange your free initial consultation

What happened?

The escalation followed events on Saturday 28 February, when US and Israeli forces launched coordinated strikes on Iran. The attacks killed Iran’s Supreme Leader, Ali Khamenei, along with several senior Iranian officials. President Trump described the operation as necessary to remove what he called an ongoing threat posed by Iran to the US and its allies, including concerns around nuclear proliferation.

Iran responded quickly, launching missiles at Israel and at American military bases across the Middle East, including strikes in Bahrain, the UAE, Qatar and Kuwait. These developments have significantly heightened tensions across the region and raised concerns about potential disruption to global energy supplies.

How markets responded

Markets reacted swiftly to the news. Major equity indices initially fell as investors assessed the risk of prolonged disruption to global oil and gas supplies.

However, the impact has not been uniform across regions.

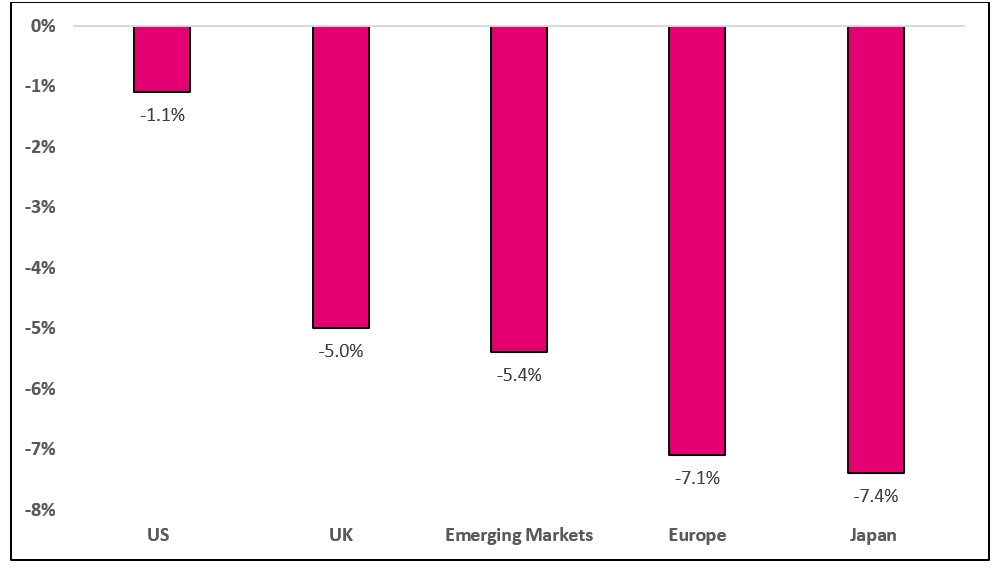

US equities proved relatively resilient. The strengthening US dollar provided support, and the United States’ position as a net exporter of oil and gas helped shield its economy from some of the immediate energy-related pressures.

European and UK markets faced greater headwinds, declining by around 7% and 5% respectively. That said, the UK’s significant exposure to energy companies helped cushion some of the losses compared with other European markets.

Asian markets also came under pressure, particularly in energy-importing economies such as Japan, which remain more exposed to rising energy costs.

Figure 2: Regional Equity Returns in Sterling (27 February – 11 March 2026, Source: Pacific Asset Management)

Figure 2: Regional Equity Returns in Sterling (27 February – 11 March 2026, Source: Pacific Asset Management)

Bonds and interest rates

Government bond markets have also reacted to the shifting outlook.

Initially, investors had expected central banks in the US and UK to continue cutting interest rates as inflation pressures gradually eased. However, the surge in energy prices has changed that narrative.

Oil shocks tend to feed quickly into broader inflation because energy costs affect almost every part of the economy. As a result, markets have begun to reassess the interest rate outlook. Government bond yields have moved higher, with UK gilts falling around 2.9% as investors adjusted expectations.

Markets now see a greater likelihood that the Bank of England will keep interest rates at the current level of 3.75% for longer than previously anticipated.

Policymakers respond

A key question now is how long energy prices remain elevated.

Energy shocks are particularly challenging for economies because they can simultaneously push inflation higher while slowing economic growth. If sustained, higher oil and gas prices could reignite inflationary pressures just as they had begun to ease across Western economies.

Policymakers have already begun responding. The International Energy Agency (IEA), which was established after the oil crisis of the 1970s, has authorised the largest emergency release of strategic oil reserves in its history.

The agency’s 32 member nations have agreed to release 400 million barrels of crude oil into global markets. This represents roughly one third of government-held reserves and is more than double the amount released following Russia’s invasion of Ukraine in 2022. The aim is to stabilise energy markets and prevent supply shortages from pushing prices significantly higher.

Looking ahead

The situation remains highly fluid and continues to evolve.

Historically, equity markets often react to geopolitical shocks with an initial period of volatility before stabilising as investors assess the longer-term economic impact. Ultimately, the path of markets will depend on how events affect corporate earnings, energy prices and inflation.

One key risk would be a prolonged disruption to the Strait of Hormuz, a critical shipping route through which around one fifth of the world’s oil supply passes. If this route were to remain closed for an extended period, energy prices could rise further, increasing the risk of higher inflation and slower global growth.

That said, the global economy is far less dependent on oil than it was during the energy crises of the 1970s. Energy supplies are now more diversified, and alternative sources play a greater role, which helps reduce the potential economic impact compared with previous decades.

History also shows that while geopolitical shocks can create short-term volatility, their effects on equity markets are often relatively short-lived.

As we noted at the start of the year, the combination of a more assertive US administration and the approach of mid-term elections increases the likelihood of geopolitical developments shaping markets. In this environment, we remain vigilant and continue to monitor events closely.

Most importantly, we ensure that portfolios remain well diversified and positioned to navigate periods of uncertainty while continuing to capture opportunities as markets evolve.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 12/03/2026.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.