Skip to main content

Skip to main content

Diversification - the name of the game for 2026

Global markets were a mixed bag in November, pausing after several months of strong gains. Volatility increased, as concerns over stretched AI-related and technology stocks resurfaced, prompting a switch towards defensive sectors such as healthcare and consumer staples. The technology sector was challenged, recording its biggest decline since March 2025.

Arrange your free initial consultation

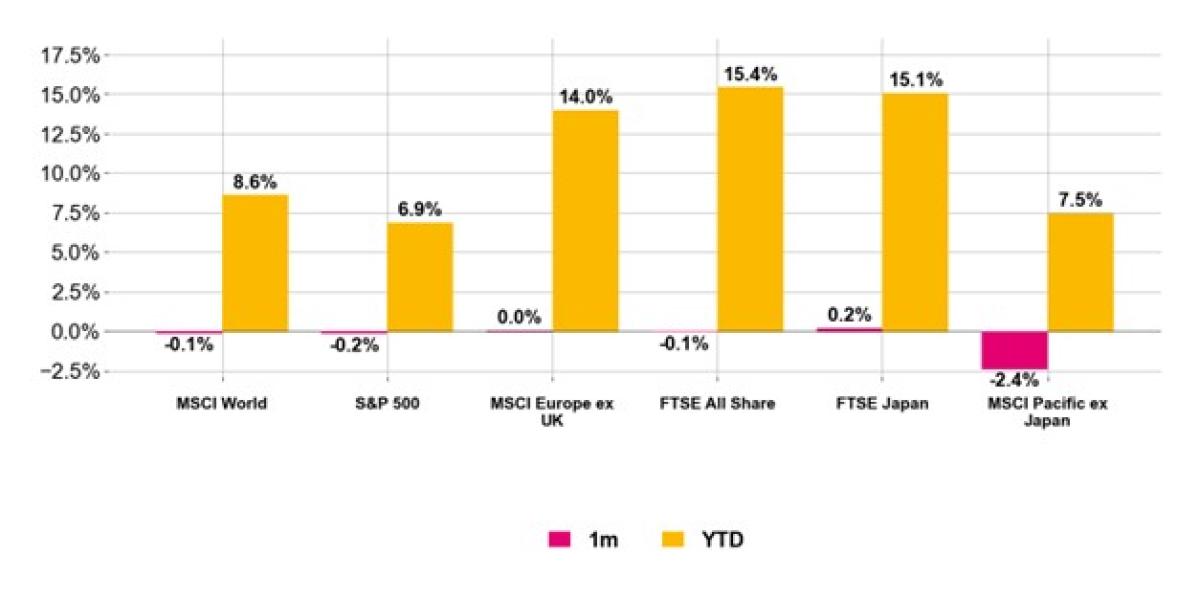

Figure 1. Regional equity returns (Source: Pacific Asset Management, November 2025)

US Markets

US equities remained largely unchanged as investors looked past the positives of strong Q3 earnings and the end of the 43-day government shutdown - the longest in US history - and instead focused on uncertainty around interest rates and concerns around an AI-driven bubble. Volatility was driven primarily by the shifting expectations around Federal Reserve policy. The probability of a December rate cut swung sharply, falling from nearly 98% in late October to about 40% by mid-November, before rebounding above 80% by the end of November. Market movements reflected not only the potential timing of rate cuts, but also investor interpretations of the Fed’s economic outlook and the likelihood of a ‘soft landing’.

European Markets

Across the Atlantic, Eurozone inflation in November ticked up to 2.2% from 2.1%, slightly above forecasts and suggesting that price pressures remain. Economic expansion was modest, with Q3 growth at 0.2% and unemployment steady at 6.4%. The European Central Bank (ECB) indicated a cautious stance, signalling that keeping interest rates unchanged remains the prudent course. European equities remained relatively flat as investors navigated these mixed economic indicators.

Japan Markets

In Japan, headline inflation climbed to 3.0% in October - the highest since July - driven by energy costs, currency fluctuations, and ongoing supply chain strains. A softer yen provided support to export-focused equities but also contributed to higher inflation, while government bonds underperformed as yields rose amid doubts over the long-term sustainability of fiscal and monetary support.

UK Markets

The UK’s Autumn Budget 2025, long anticipated and partially pre-empted by the early Office for Budget Responsibility (OBR) publication, had a relatively muted immediate impact on markets.

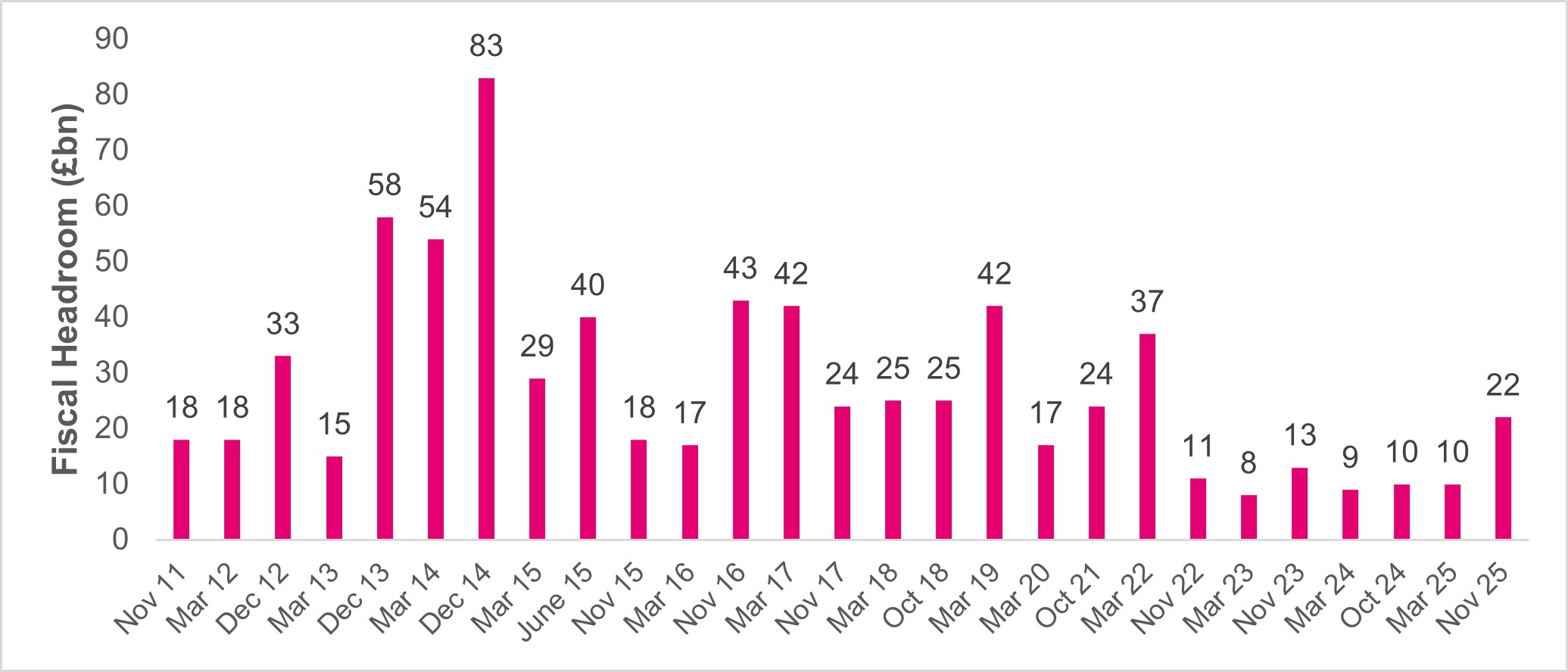

The Chancellor outlined £26 billion in tax measures; however, with many provisions deferred over several years - some beyond the next general election - the near-term fiscal landscape remains largely unchanged. Fiscal flexibility is set to improve, with the Chancellor projecting a buffer of approximately £22 billion - more than double last year’s level - which had been largely eroded and fueled months of speculation over potential tax increases. While this represents a meaningful increase in fiscal headroom, it remains below average, with the typical revision to an OBR forecast over six months around £21 billion, leaving little room for error (see Figure 2.).

Figure 2. Forecast headroom against fiscal room (Source: Pacific Asset Management, IfG, November 2025).

Markets responded positively to the extra fiscal headroom and the reduced risk of near-term borrowing pressures or unexpected tax adjustments. UK government bonds delivered one of their strongest Budget-day performances in twenty years, reflecting renewed confidence in the fiscal outlook. Meanwhile, equity markets, which had softened amid pre-budget leaks and speculation, stabilized as investors assessed the measures as supportive of macroeconomic stability without introducing major new uncertainties.

Commodities and Gold

Away from equities, commodities posted modest gains in November, with performance varying across sectors. Gold emerged as the standout performer, supported by sustained investor demand for safe-haven assets amid ongoing macroeconomic uncertainty, including inflationary pressures, central bank policies, and geopolitical risks.

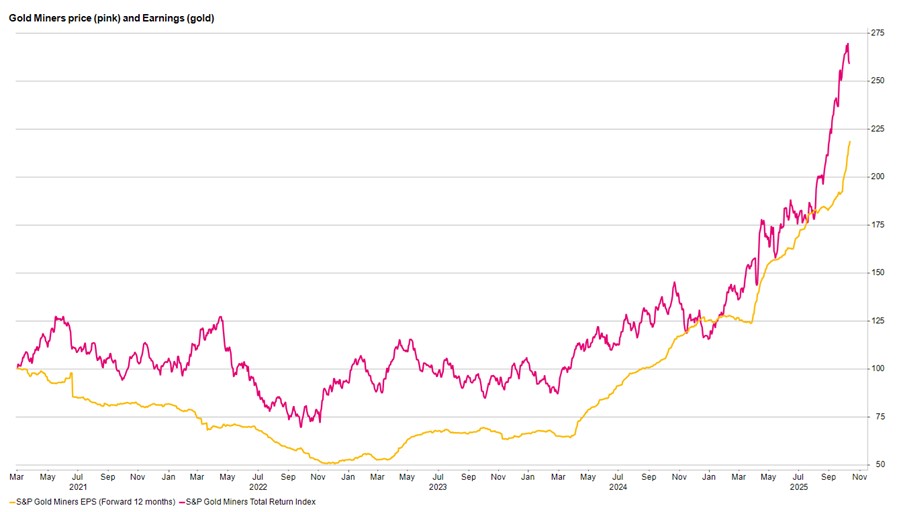

While November’s advance was more measured than recent rallies - partly due to profit-taking - the metal’s underlying fundamentals remain strong. Structural demand, constrained supply, and its role as a portfolio diversifier continue to underpin gold’s outlook into 2026. Gold mining companies also continue to benefit from elevated gold prices and more disciplined capital management, with earnings growth reflecting these favourable conditions (see Figure 3.).

Figure 3: Goldmining companies return and earnings profile (Source: Pacific Asset Management, November 2025).

Summary

Despite some volatility in November, global equities are positioned to deliver another strong year in 2025. Equity markets in the UK, Europe, and Japan have all shown relative outperformance compared with the US, underscoring the value of international diversification. Moreover, the recent underperformance of technology stocks highlights the importance of sector diversification - not only as a risk management tool but also as a potential source of returns.

Looking back over November, there were no major shifts in economic fundamentals. Instead, market movements reflected changes in sentiment, emphasizing how investor perceptions and expectations can drive short-term volatility - even in the absence of significant economic or market developments. This serves as a reminder that as we move into the next year, investors will continue to face sentiment-driven risks alongside structural considerations, including central bank policy, inflation dynamics, and sector-specific trends.

Overall, the performance of global equities this year reinforces the importance of maintaining a diversified investment approach that balances geographic exposure, sector allocation, and risk management strategies.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 12/12/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.