Skip to main content

Skip to main content

Divorce and your financial affairs - are you losing out?

The year 2020 has been tumultuous to say the very least. Not only has the global pandemic placed enormous strain on people financially but it has also strained people’s relationships.

Research from Citizens Advice has found that divorce guidance searches increased 25% in the first week of September this year, compared to this time last year, with many solicitors citing that the extreme change of personal circumstances has exacerbated marriage problems.

A divorce is an incredibly difficult time for many. Indeed, conversations regarding money are often pushed to one side as couple’s battle with the emotional stress that a divorce often brings. But facing the financial issues is a critical part of the process.

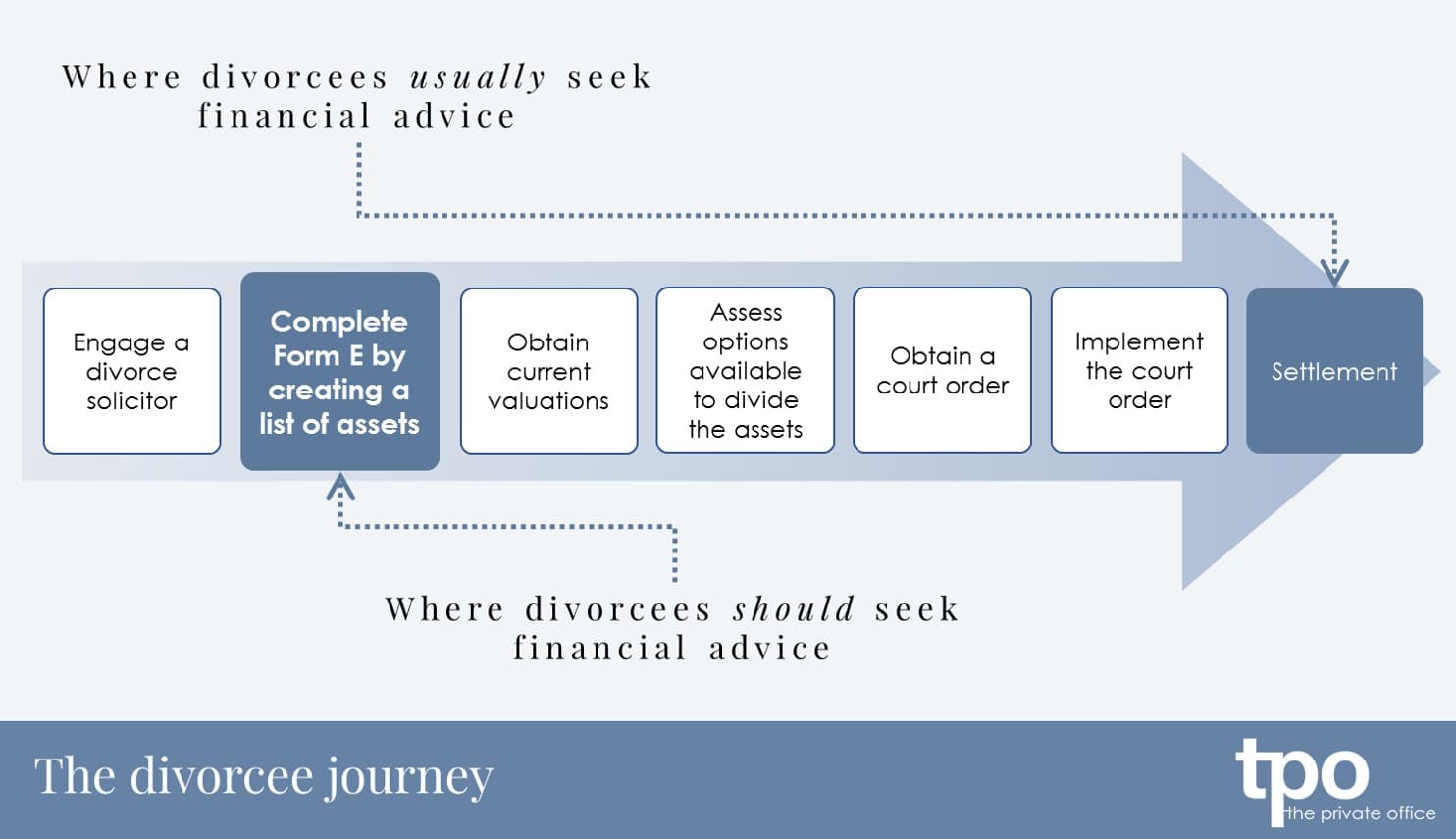

The below diagram illustrates the typical financial journey experienced during a divorce, with the notable point being, that Financial Advisers are typically engaged far later in the process when compared to other professional advisers, such as Solicitors.

Unfortunately, engaging a Financial Adviser right at the very end of a divorce often means that several crucial planning opportunities may have been missed. By engaging a Financial Adviser during the early stages of a divorce, there are many pitfalls that you can avoid, as well as ways that an Adviser can assist you in ensuring that you have a clear plan to secure your financial future.

Being organised

The first important step during a divorce process is ensuring that you are organised. During the early stages of a divorce you will be required to complete a Financial Statement, often referred to as Form E. When completing this form it’s really important that you clearly state all of the assets that you hold including any property, cash, investments and pensions. Failure to fully disclose all of your finances at the outset may often bring additional costs later in the divorce process.

Saving tax

During a divorce, it’s likely that you may have to transfer assets held under your name into your spouse’s name, or vice versa. An important consideration when transferring assets, is any Capital Gains Tax liability that might arise. One way to reduce the tax that you might pay is to ensure that the assets are transferred to your spouse before the end of the tax year, in this case 5th April 2021. The cost of requesting assistance with transferring assets, particularly a Financial Adviser or Accountant in this regard, could quite easily be offset by the resultant tax savings incurred.

Clarifying where assets are held

Clarifying where your assets are held, involves understanding how they are structured and how they are invested. Prior to a divorce it’s common that you will have treated your financial affairs as being held jointly, and as such, you will have made decisions based on your financial future with your spouse. However, after a divorce it may be the case that you wish to pursue a different course with your assets, whether that be how you wish to draw an income or how your assets are invested for your future. Either way it’s important to ensure that you have a clear understanding of where your assets are currently held, so that you can devise a plan moving forward.

Don’t be scared of pensions

There are myriad complex pension terms out there, and although your solicitor may be able to provide you with general guidance, they will typically recommend that you seek specialist financial advice in respect of pension assets that might become subject to divorce negotiations. Employing the skills of a Financial Adviser experienced with dealing with pensions on divorce, will help demystify this complexity and provide reassurance that you are seeking expert help on arguably one of your most valuable financial assets.

Establishing a plan

Once a divorce settlement has been agreed many clients are relieved to have reached the end of what can be an arduous experience. Naturally, many think that a settlement marks the end of the road for your finances, but if anything, it marks the beginning.

During your marriage many of your financial decisions will have been made jointly with your spouse, and therefore you had an idea of what those plans might have looked like. A divorce is likely to offer you an opportunity to reflect and review your future goals and aspirations, and what that might mean for your finances moving forward.

At this moment it’s important that you neither shy away from making tough financial decisions, nor rush into hasty ones that you may regret later down the line.

The role of a Financial Adviser may be crucial when considering your lifestyle and the level of future expenditure that will be required to achieve your aspirations.

At The Private Office (TPO) we use lifetime cashflow modelling to establish your budgeting capability in the immediate term and in the long term. Clients who are experiencing a divorce often find that our cashflow modelling provides them with clarity of thought on what their finances look like now, as well as helping them develop a much clearer picture of what their future might look like.

Taking ownership of your finances before, during and after divorce may appear daunting but by taking a few relatively simple steps, in coalition with your advisers, you will be empowered to achieve your future lifestyle aspirations.

Please note: The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax advice.