Skip to main content

Skip to main content

Inheritance Tax, not just a concern for the wealthy

Often referred to as the ‘death tax’, Inheritance Tax (IHT) is a financial levy imposed on a deceased person’s estate that determines the distribution of wealth to their beneficiaries. Despite popular belief, IHT is not exclusive to the wealthy; its impact resonates across a wide spectrum of society.

IHT is calculated on the total value of the deceased’s estate, with a headline rate of 40% applied to estates that exceed the £325,000 nil-rate band (NRB). The misconception that only the wealthy need concern themselves with IHT is ousted, as longer life expectancies and changes in demographics bring the impact of this tax closer to home.

Arrange your free initial consultation

The current landscape

The Office for Budgeting Responsibility (OBR) are predicting that IHT receipts in the UK will rise sharply from the record-breaking £7.1 billion collected in 2022-2023 to £8.4 billion by 2027-2028. According to HMRC data, one in every 25 estates are subject to IHT, meaning that this tax is no longer exclusive to the wealthy. Recent data from HMRC reveals a staggering £2.6 billion in IHT receipts were collected in just 13 weeks between April and July of 2023, which is more than the total IHT bill for 2009. Based on projections, the average IHT bill is expected to rise to £304,567 in 2025-2026 and £345,084 in 2027-2028.

With its tax-free allowance, known as the NRB, remaining unchanging at £325,000 since April 2009, IHT may be considered as one of the longest-standing stealth taxes. Over the past decade there has also been no increase to the £3,000 gifting allowance. Rising house prices and frozen allowances are drawing more households into the IHT net, debunking the common misconception that IHT is solely for the wealthy.

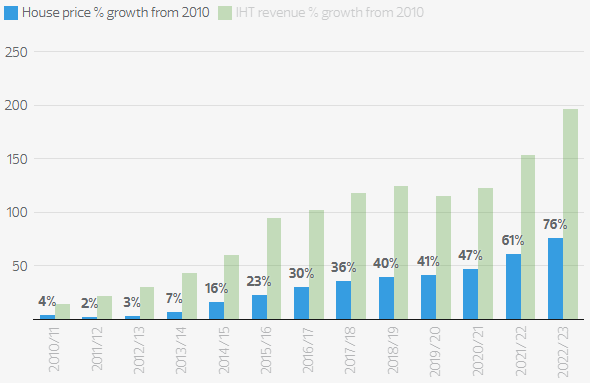

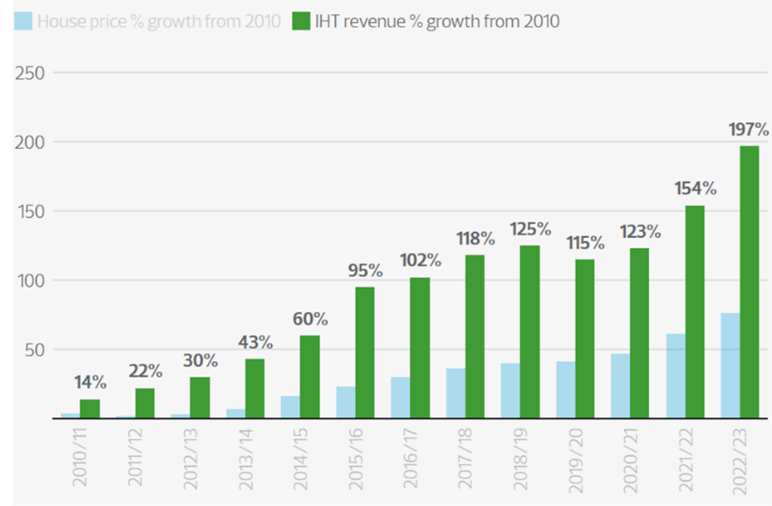

The Office of National Statistics has released figures showing a 73% increase in house prices in the ten years from 2013 to 2023. This consistent rise in house prices over the last decade has contributed significantly to the rise in IHT receipts. Although an individual’s property value is not the sole contributor to the value of their entire estate, it accounts for a substantial proportion of it, therefore expanding the number of households within the scope of IHT. To help somewhat offset IHT, there is an additional threshold, the residence nil-rate band (RNRB), which was introduced in 2017. If an individual leaves their main residence to a direct descendant, they are able to pass on an additional £175,000 IHT free.

Figure 1: House price growth vs IHT revenue % growth from April 2010, Source: RSMUK, 2023.

The political elephant in the room

Rumours around Government changes to IHT?

Navigating potential changes to IHT and political uncertainties is essential, as rumours concerning the possible elimination of IHT, or introduction of a wealth tax continue to circulate ahead of the next Budget on 6th March. In an effort to win over votes, reports indicate that the Conservative Party may abolish IHT, while a wealth tax on the wealthiest individuals is also being considered, however, with the potential of a changing government with an impending General Election, how long any changes stay in place is impossible to call. To effectively plan and reduce IHT, individuals should instead concentrate on the rules and regulations currently in place, rather than basing their decisions on rumours and speculation.

How can you ensure as much as possible of your estate goes to your loved ones?

In order to mitigate IHT, a thorough strategy combining strategic financial planning and maximising available allowances is needed.

Some key strategies include:

Increase your spending - Spending additional cash to lower the value of your estate is a straightforward yet effective tactic. While this may seem straightforward, individuals should aim to strike a balance between reducing their estate, whilst ensuring they don’t compromise their long-term financial security. For this, putting in place a robust financial plan is key.

Responsible financial planning – IHT encourages individuals to engage in financial planning. It is key for this to be updated each year to ensure individuals can enjoy their desired lifestyle whilst also maximising various allowances. Working with a qualified financial adviser can help you comprehend the potential effects of IHT and encourage you to look into mitigation techniques.

Annual gifting – Making use of the £3,000 annual gifting allowance per person offers an opportunity to reduce the taxable estate. If you have not used your annual exemption in the previous tax year, then you are eligible to combine this to your current tax year to make an allowance of £6,000. Utilising additional exemptions above the £3,000 yearly allowance can also be achieved by making use of small gifting of up to £250 to different individuals, although not to anyone who has already received a gift of your whole £3,000 annual exemption.

Regular gifting - A less known allowance is gifting out of surplus income. If individuals can demonstrate that their regular income can comfortably meet their lifestyle expenditure with surplus income remaining, this can be gifted to one beneficiary or split across several. It is important that this gifting has a regular pattern as it is supposed to come out of surplus income. Given that these requirements are met, these gifts out of surplus income would not be subject to IHT.

It is very important to ensure that these gifts would not be classified as a gift out of capital.

As a reminder, any capital gifts over the annual allowance of £3,000, will be classified as Potentially Exempt Transfer (PET). This means that 7 years need to pass following the capital gift, so it is IHT exempt. Careful financial planning can help to determine, if regular gifting out of surplus income is affordable.

Gifts to charities – Gifting to charities can lower the net value of your estate whilst simultaneously giving to a charity you wish to help. Furthermore, charitable donations are free from IHT, offering a strategic way to reduce the total IHT obligation. If you leave 10% of your estate to a charity, then IHT payable above the £325,000 threshold will reduce from 40% to 36%.

Contribute to a defined contribution pension – Since the introduction of pension freedoms in 2015, pensions have emerged as one of the most tax-efficient means of wealth transfer as they do not form part of your estate for IHT purposes. Most pensions are written under a form of trust, meaning the entire pot, including tax relief, can be passed down to loved ones without incurring IHT. Older defined contribution pensions might not be written into trust, which can mean that they might still be paid into the individual’s estate, therefore this should be checked. Since most defined contribution pensions do not form part of your estate on death, pension savings aren’t usually covered in a Will. It is essential to ensure expression of wish forms are set up and kept up to date with pension providers, so they know who to pay out the benefits.

What can you do as the Budget and Tax Year end draw near?

Making the most appropriate use of the above exemptions and annual allowances can help to reduce the taxable value of your estate. These need to be tailored to your individual needs and it is key that a bespoke gifting strategy is put in place without compromising your own lifestyle. Early engagement with a financial adviser plays a key role in ensuring you are making an informed decision in the ever-changing financial landscape. With careful financial planning, individuals can make sure their hard-earned assets are protected for their chosen beneficiaries.

Key dates to have in mind: The Budget on 6th March and the end of the current tax year on 5th April.

If you’d like to learn more about how you can minimise the tax bill on your estate, why not get in touch for a free initial consultation with one of our experts.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

This article is also based upon our understanding of current law, HM Revenue and Custom's practice, tax rates and exemptions which are subject to change.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning or tax advice.