Skip to main content

Skip to main content

Reasons for optimism: Trump shaken as US bond markets stirred!

April 29th marked President Trump's first 100 days in office. His early April ‘Liberation Day’ announcement signalled a major shift in U.S. trade policy. A subsequent 90-day pause (except to China) offered brief relief, but ongoing uncertainty continues to weigh on markets.

Arrange your free initial consultation

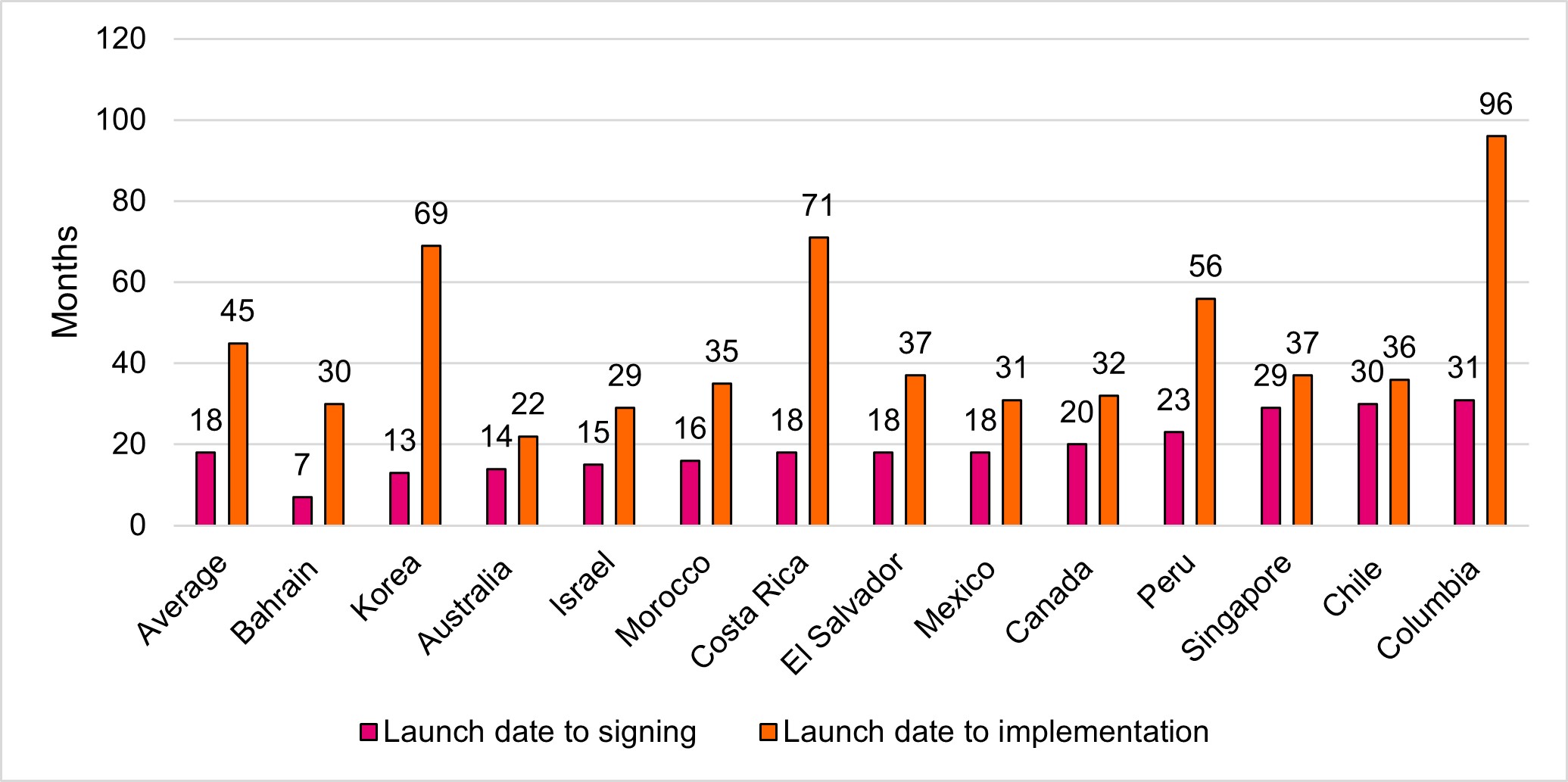

Part of the uncertainty relates to the fact that trade deals are not typically completed within 90 days. If we look back at historic trade deals that the US have negotiated it has taken on average 18 months to agree to a deal and then a further 45 months to implement (see Figure 1.).

Figure 1. US Historic trade deals (Source: Apollo, April 2025)

In equity markets, we saw the volatility of US equities spike with the ‘Volatility Index’ (VIX) reach a level not seen since the onset of the COVID-19 pandemic, as investors looked to appraise what US trade policy means for the outlook on global growth and inflation.

Against this backdrop, equity markets were challenged, with US equities struggling and the S&P 500 down over 4.3% (in sterling terms) last month. This means President Trump has the unenviable claim of being one of the few post-war modern Presidents to have the S&P 500 fall during their first 100 days and is the worst return since Nixon’s second term back in 1973.

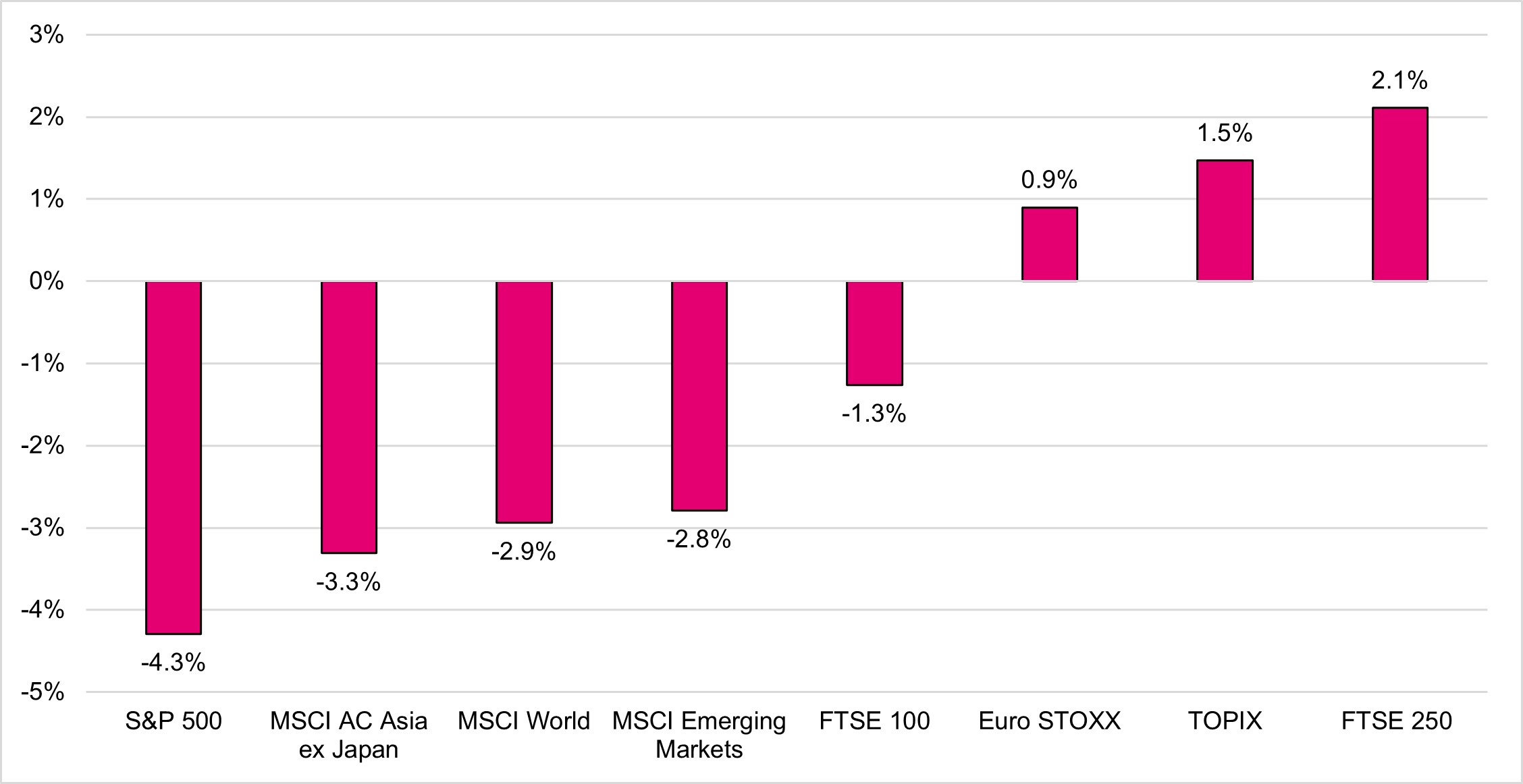

Investors though were once again rewarded for being diversified and looking beyond the US. After a volatile start to the month, European equities rallied, led by Germany on the prospect of increased fiscal spending and Spain, whose economy is less exposed to US trade policies. Likewise, UK mid-cap stocks - benefiting from their domestic focus and reduced vulnerability to US tariffs - rose 2.1% (see Figure 2.).

Figure 2: April 2025: Regional Equity Returns in sterling (Source: FE Analytics)

Fixed income was not immune to the volatility, as we saw the US 10-year bond yield experience its largest weekly rise since 2001, climbing to 4.6% before retracing to 4.2% by month-end (Bond yields rise as prices fall). It is widely believed that this caused President Trump to walk back his tariff policy and implement the pause, given that he and his administration are seeking to lower yields (and the cost of Government debt) in the US.

In this backdrop we saw the price of German Government bonds increase as the spread (compensation for risk) increased between German and US bonds. Meanwhile UK Gilts rallied in April as investors expect the Bank of England to be more aggressive in cutting rates following the continued weakening in the labour market and the announcement that inflation in the UK fell from 2.8% to 2.6% in March.

In commodities, we saw the price of oil collapse 18% and trade at levels not seen since 2021. This followed the news that eight countries who form part of OPEC+, agreed to increase output of oil production at a time when investors are becoming increasingly concerned about a recession which could hamper demand.

Gold, however, reached a new high hitting $3,500 for the first time. This continued demand for gold reflects a confluence of several economic, political and financial factors.

Gold has in the past performed well during periods of geopolitical uncertainty, and ongoing global tensions have once again caused investors to view the precious metal as a ‘safe-haven’ asset. In addition to geopolitical uncertainty, the potential inflationary impact of new US tariffs has boosted gold prices, with investors hedging against the falling purchasing power of currencies such as the US Dollar.

Falling interest rates has also supported the price of gold as the asset does not pay any interest or dividends meaning the opportunity cost of holding gold is smaller. Finally Central Banks such as China and India have significantly increased their purchases of gold as countries shift away from the US Dollar and look to reduce the reliance on the US.

Looking ahead we continue to see a notable distinction between sentiment and ‘hard’ data.

Sentiment indicators, such as surveys - which by their nature are forward looking - continue to trend down, with US consumer confidence declining five consecutive months in a row and at a level not seen since the onset of the COVID-19 pandemic.

Conversely, April’s US jobs report showed 177,000 jobs added—surpassing the forecast of 138,000—while 76% of companies reporting quarterly earnings beating expectations. This suggests that the economy is more robust than sentiment indicators would initially lead us to believe.

On the tariff front, we are beginning to see an impact with a slowdown in activity at US ports and air freight as China, the world’s largest exporter, continues to face tariffs. We are all well aware of how interconnected the global supply chain is following the COVID-19 pandemic and the longer tariff uncertainty continues the more pronounced the issue will be.

We’re cognisant that we are in a transition period, where there’s a lot of uncertainty about the data currently being reported, and this is likely to contribute to ongoing market volatility. With that said, we continue to see a broadening opportunity set for investors, and in the absence of a clear direction, being well diversified remains the best course of action.

As ever, if you’ve any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO adviser team.

Arrange your free initial consultation

The information in this article is correct as at 16/05/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.