Skip to main content

Skip to main content

Spousal bypass trust - Reduce Iht on your pension

What is a spousal bypass trust?

A spousal bypass trust is a Discretionary Trust designed to provide you with control over who may benefit from your pension funds when you die.

You may leave an expression of your wishes for your chosen trustees so that they are aware of your preferences when making their decisions. There are advantages and disadvantages to setting up a spousal bypass trust and you should understand what these are prior to making any decisions.

Following the introduction of Pension Freedoms in 2015 you might be asking yourself ‘why do I need to use a Trust to pass my pension fund on to my family when I die?'

In this article we will provide some background to the 2015 changes and explore the reasons why a trust might still be the right answer to your planning needs.

When pension freedoms were introduced in 2015 there was a lot of attention given to the changes in how you can access your pension funds when you retire.

The Government announced in the Autumn 2024 Budget that from 6 April 2027, when a pension scheme member dies with unused pension funds, those unused funds and death benefits will be treated as being part of that person’s estate and therefore may be liable to Inheritance Tax. Please read on for a summary of the current position and information about Spousal Bypass Trusts.

While these changes were welcomed, one of the most significant changes to take place related to the options available to your beneficiaries and the tax treatment of your pension funds when you die if you have defined contribution pension plans – these are often referred to as money purchase arrangements or private pensions.

What were the changes?

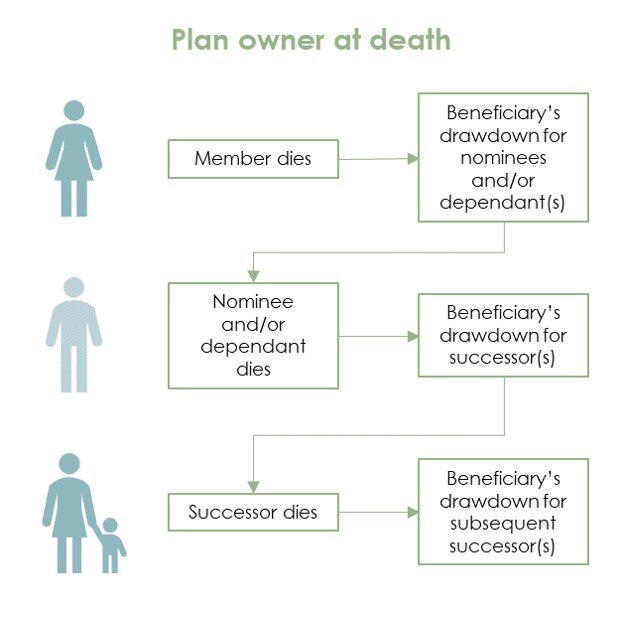

From April 2015 your pension fund can provide an income to anyone you nominate - not just a financial dependant such as a spouse or child – and if you die before age 75 any lump sum or income payments they received will, in most cases, be tax free.

If you die after age 75 the same beneficiary rules apply but the payments are no longer tax free as the beneficiaries will pay income tax on any benefits they receive.

It was also confirmed that your pension funds will not be subject to inheritance tax1 and can pass from your children to your grandchildren and so on until the funds are exhausted and would not form part of their taxable estate either!

You can even choose to skip generations and nominate directly to your grandchildren if you wish, or nominate to someone who is not related to you – perhaps a family friend?

The important point to note is that, if you are survived by a dependant (spouse, child under 23 etc), an income using flexi-access drawdown can only be paid to someone who isn’t a dependant if you nominate them while you are alive.

The cycle continues until Flexi-Access Drawdown funds are exhausted

The added benefit of these changes is that most private pensions are able to offer this beneficiary flexibility on death without you having to set up a new plan or incur fees and charges by using a trust.

There are, of course, exceptions to this and we would be happy to help you review your existing pension plans and report back on the options they provide on death for your beneficiaries.

Why consider using a spousal bypass trust?

So, you may well be asking yourself ‘why would I want the trouble and expense of setting up and maintaining a spousal bypass trust if I can nominate benefits directly from my pension plan to anyone I choose?’

That is an excellent question and the simple answer is ‘CONTROL’.

Unfortunately, in these modern times it is not uncommon for marriages to fail with the Office for National Statistics reporting that 42% of marriages in England and Wales will end in divorce and half of these will be within the first 10 years of marriage (ONS Statistical bulletin – Divorces and Dissolutions in England and Wales 2023).

Of course, many people go on to marry again and, given the rate of divorce, it is not surprising that the second (or subsequent) marriage is often to someone who has also been in a previous relationship and who may also have children from an earlier marriage.

Unfortunately, not all second (or subsequent) marriages are harmonious and there can often be conflict between step-parents and step-children.

If you want to provide security for a second (or subsequent) spouse during their lifetime but also require certainty that any children from your previous marriage(s) will ultimately benefit from your pension funds after your death this cannot be achieved through a pension nomination.

Basically, once your pension fund passes to your spouse they are able to nominate their own beneficiaries (called Successors) to receive any remaining money held in your pension fund when they die - they are not bound by any nomination you have made while you are alive!

We are often asked ‘What if I leave my pension fund to my children in my Will?’

Unfortunately any bequest of pension funds in your Will is not binding and the pension provider has discretion on who receives your pension fund when you die.

As you can see, while there are many positive changes brought about by the 2015 rule changes the only way to have certainty on who may benefit from your pension funds when you die is to use a Trust.

Although the trust itself is a discretionary trust you can leave an expression of your wishes for your chosen trustees so that they are aware of your preferences when making their decisions. Your trustees will be people you trust and it is also possible to include a professional trustee such as a solicitor if preferred (although they will charge for their services).

There are other reasons why you may want to consider a spousal bypass trust such as:

- Protection from bankruptcy as a potential beneficiary has no absolute entitlement

- Protection for potential beneficiaries in the event of their own divorce

- Potential beneficiary is not financially prudent

- Provision for a family member who is vulnerable through physical or mental impairment

- Access to a wider range of investment opportunities, including residential property

- Capital ring-fenced from assessment for Long Term Care funding assistance

The disadvantages of using a trust

We have already talked about the cost of setting up and operating a trust. When you are considering a spousal bypass trust you also need to think about the different ways in which a pension and a trust are taxed.

Taxation of a spousal bypass trust

If you die on or after your 75th birthday and nominate your pension funds to a spousal bypass trust there is a 45% tax charge on the transfer (called a special lump sum death benefit charge) payable to HM Revenue and Customs.

This tax charge does not apply if you die before your 75th birthday.

The remaining 55% of your pension funds are invested in the trust and are taxed in exactly the same way as other discretionary trusts.

Distributions from the trust to your beneficiaries are taxed as income when they are received by your beneficiaries but they will receive a 45% tax credit if your trust was subject to the special lump sum death benefit charge when it was set up.

Do pension funds pay taxes?

The money you invest in your pension plans grows free of income and Capital Gains Tax during your lifetime and after you die. It is also free of inheritance tax in most cases until the aforementioned change takes place in April 2027.

If you die before age 75 your beneficiaries do not pay any income tax on any withdrawals they make from your pension fund.

If you die after age 75 they pay income tax at their marginal rate of income tax.

As you can see there are a lot of issues to consider and compromises to be made if you want to control the ultimate destination of your pension funds after your death and we have only been able to provide a brief overview of the issues in this article.

We have decades of experience in advising clients on pension and estate planning matters and encourage you to speak to a financial adviser before you undertake any planning of this type.

Note: The Financial Conduct Authority does not regulate estate planning, tax advice, wills or trusts.

References

- Your pension funds are normally free of inheritance tax – there are certain actions that can cause inheritance tax to be payable if they occur when you’re in ill-health and you die within the following two years – these actions include transferring your pension fund from one pension to another, assigning death benefits into trust and substantially increasing pension contributions.