Skip to main content

Skip to main content

ISA changes: why 2026/2027 tax year matters more

The start of the new tax year is often a good time to take stock of your finances, to review what you already have and consider what you need to do next. And in today’s environment, where every penny counts, making full use of the tax allowances that are still available has never been more important.

The ever-popular Individual Savings Account, or ISA is a good place to start. Like a lot of our tax allowances, the ISA allowance has been frozen for many years, so for the 2026/27 tax year, the overall ISA allowance remains at £20,000, offering one of the simplest and most effective ways to protect your savings and investments from tax on interest, dividends, and capital gains.

However, there are changes coming for those who favour the cash element of an Individual Savings Account (ISA).

Cash ISA allowance to be cut

Cash ISAs regained their popularity over the last few years, as interest rates increased, which led to savers paying more tax than they had for over a decade when interest rates were at rock bottom. There is now some £458 billion stashed away in cash ISAs, almost a quarter of the total amount held in cash savings. But for savers under the age of 65, the current tax year is the last chance to make use of the full ISA allowance for cash only deposits.

From 6 April 2027, the rules are set to change. Whilst the overall ISA allowance will remain at £20,000, only £12,000 of that can be deposited into a cash ISA for those aged under 65. To use the full allowance, the remaining £8,000 will need to be invested in a stocks and shares ISA.

To add insult to injury, at the same time that the cash ISA allowance is to be cut, the tax on savings interest will be increasing by 2%. So, a basic rate taxpayer will pay 22% on any taxable interest, it’s 42% for higher rate taxpayers and 47% for additional rate taxpayers, making the cash ISA even more valuable.

The good news is that those aged 65 and over are not affected by this change. They will still be able to place the full £20,000 into cash if they wish, a welcome exemption for older savers. But it highlights a broader policy direction, encouraging younger savers towards investment.

A nudge towards investing

Whilst the comfort of a cash ISA is understandable, particularly in volatile times, it’s important to be aware that inflation can quietly erode the value of savings, and even with improved interest rates, cash may struggle to deliver meaningful real returns over time if inflation is higher than the interest you are earning. So, it might be worth asking yourself whether a purely cash-based approach is the right strategy for the longer term.

This is where stocks and shares ISAs come into play. They are not without risk though as values can go down as well as up. But they offer the potential for growth that cash generally cannot match over the long term, as long as you are prepared to accept the inevitable bumps in the road. You can of course, choose investments that better reflect your own personal attitude to risk, which will help minimise any potential downs and ups.

These changes could therefore be viewed as a prompt to diversify if you don’t need access to your money for the longer term, so more than five years. Using some of your ISA allowance for investment could make a meaningful difference to your future financial health.

Use it or lose it

Given the upcoming changes, this tax year (2026/27) is an opportunity not to be wasted. If you are under 65 and prefer cash, it may make sense to maximise your cash ISA contributions while you still can.

And due to the ongoing conflict in the Middle East, with the expectation that inflation and therefore the Bank of England base rate could rise, savings rates have been increasing recently. Good news for savers, especially those who don’t also have debts.

So, if you have funds sitting in taxable accounts, now is the time to consider sheltering them, as once the tax year ends, you can’t carry it forward.

Don’t overlook the Lifetime ISA

Alongside the standard ISA options, there is also the valuable Lifetime ISA (LISA), which is available to those aged between 18 and 39. The LISA allows you to contribute up to £4,000 per tax year, which counts towards your overall £20,000 ISA allowance and the real attraction is the generous 25% government bonus. In simple terms, a £4,000 contribution is topped up to £5,000, an immediate and very attractive return, even before any interest of investment growth is added.

Traditionally, the LISA has served a dual purpose: helping people save for their first home or for retirement. However, it is currently under review, and there is growing speculation that the retirement element could be removed going forward, making it simply a product for first-time buyers.

In the meantime, for those eligible, it remains a compelling option, particularly if you are saving for your first home.

ISAs for the next generation

It’s also worth remembering that children have their own ISA allowance through the Junior ISA (JISA).

With a current annual allowance of £9,000 per year, the Junior ISA allows parents, grandparents, and others to build a tax-free savings pot on behalf of a child. It can be held in cash or invested, depending on your preference and time horizon.

There is, however, an important point to bear in mind: there is no access to the money until the child turns 18, at which point they gain full control of the account, which could have grown to a really significant amount. The funds become theirs to use as they wish, whether that’s for university, a car, a house deposit, or, indeed, something less sensible.

Alternatively, the funds can be rolled over into an adult ISA, retaining the tax-free status and allowing the savings habit to continue into adulthood.

For those who save for their children, it makes sense to have open conversations with them as they grow older, so that hopefully they will do the right thing with this valuable gift. Financial education is just as important as the savings themselves.

Time to take action

The beginning of the tax year is a great time to make use of your ISA allowance, for a couple of reasons.

First, during the ‘ISA season’ of which April is the pinnacle, cash savings providers tend to compete with each other, which pushes rates higher, providing plenty of choice.

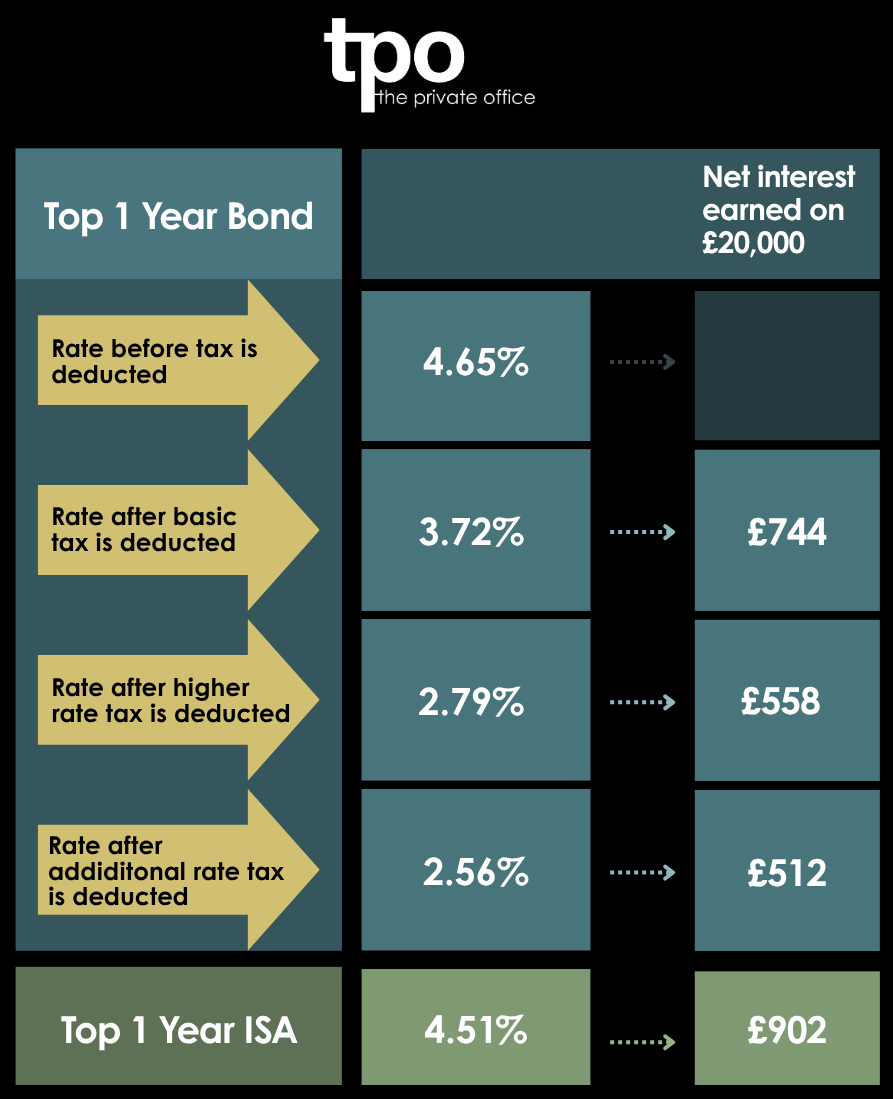

Secondly, why leave your cash in a taxable account any longer than you need to. Although often the headline rates on taxable fixed rate bonds may look higher than the same term cash ISAs, once you deduct income tax, you can earn far more in the tax-free ISA, as the table below illustrates:

Now is also a good time to review your old ISAs, to see if you could be earning more by switching. The key rule is vital though - never withdraw the funds yourself. Instead, always use the official ISA transfer process provided by your new provider, who will liaise directly with your existing bank or building society. If you take the money out and attempt to redeposit it, it could lose its ISA “wrapper” which crucially means you would forfeit the tax-free status tied to those historic allowances. Given that ISA allowances cannot be reinstated once lost, this is an irreversible and often costly mistake.

Reviewing your old ISAs whilst making the most of your new ISA allowance means that you can make your cash work as hard as possible, particularly important if we are to see inflation spiking upwards once again.

If you want to make your cash work harder, it is important to compare rates regularly and move money when better deals arise. In a market that is shifting and where relatively small rate differences can add up to hundreds of pounds over a year, staying informed is the best way to keep your savings working as hard as possible. Check our best buy tables for the most up to date savings rates.

Arrange your free initial consultation

Rates correct as at 07/04/2026.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning.