Skip to main content

Skip to main content

The big pension changes in 2024 and how to plan for them

2024 will see some huge changes to pensions, not least the much-publicised abolition of the Lifetime Allowance (LTA). So how do you prepare for a rapidly changing pension landscape? With a general election around the corner and the likelihood of a changing Government how can you plan for changes in legislation that could well be scrapped later down the line?

Arrange your free initial consultation

Lifetime Allowance

Taxation on pension funds has been a hot topic since the 2023 Spring Budget when the Chancellor announced his intention to abolish the ‘Lifetime Allowance (LTA)’. The LTA is the total value that someone can accrue within a pension over their lifetime without incurring certain tax charges. Under LTA rules you could face a tax charge of up to 55% on pension savings above £1,073,100. So, for people with large pension pots, the prospect of abolishing this allowance was welcomed.

The announcement also signposted the introduction of two new allowances which will restrict the amount of tax free lump sums which could be paid under the new pension regime from 6 April 2024.

The new Lump Sum Allowance is the upper limit on the tax-free cash someone can take from their pensions during their lifetime and is capped at 25% of the previous LTA (£268,275).

The second allowance, the Lump Sum and Death Benefit Allowance will restrict the tax free lump sum which can be paid from your pension funds to your beneficiaries if you die before your 75th birthday. The Lump Sum and Death Benefit Allowance is set at £1,073,100 and the new regulation does not have any provision for these to increase over time to keep pace with inflation.

If you had previously registered for one of the many forms of protection against the Lifetime Allowance and have not broken the conditions for maintaining your protection you will benefit from a higher Lump Sum and Lump Sum and Death Benefit Allowance.

To account for benefits taken between 6 April 2006 and 5 April 2024 a transitional calculation has been provided so that individuals can calculate their remaining available Lump Sum Allowance and Lump Sum and Death Benefit Allowance.

There is a secondary calculation which can be undertaken for individuals who did not receive the full tax free cash lump sum entitlement of 25% when pension benefits were taken previously which may enable them to receive an increased Lump Sum and Lump Sum and Death Benefit Allowance. It is advisable to take financial advice when undertaking these calculations as they can be complex.

As soon as the Chancellor announced the abolition of the LTA, Labour announced that they would reintroduce the LTA if they are elected following the impending General Election with the current Prime Minister, Rishi Sunak, suggesting this will happen in the second half of this year.

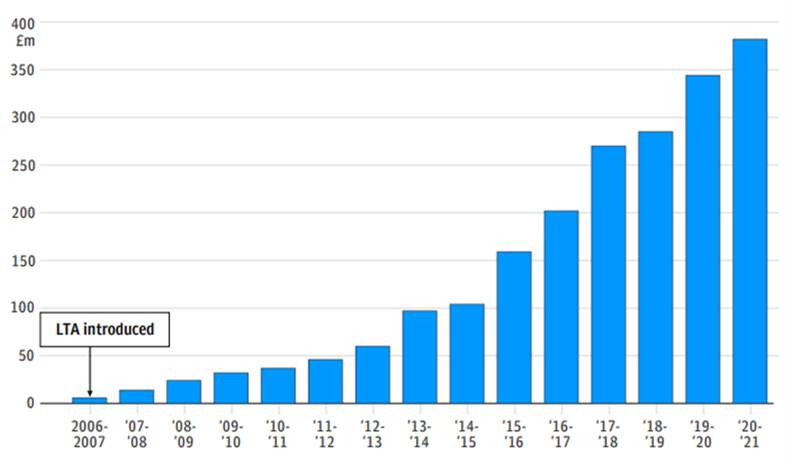

The number of people paying tax for breaching the LTA has been increasing in recent years (See Figure 1) , and the reintroduction of the limit after a period of overcontributing will push this number even higher. If the LTA is reintroduced at its previous level, it is estimated that around 250,000 people will be over the limit.

Figure 1: Tax Paid for breaching lifetime allowance, Source: HMRC, 2024

Many are concerned that bringing back the cap will push senior NHS doctors into an early retirement. One of the key motivations for scrapping the LTA initially was to deter NHS doctors from retiring early to avoid tax bills.

Could a Labour government reverse the rules?

In the run up to the election we could see a sudden flurry of savers rushing to draw down on their pensions before the potential reintroduction of an LTA. To prevent this, Labour may decide not to go ahead with the reversal.

Now that the legislation has been passed and HMRC have almost completed the implementation of the changes, tax experts have said it will be more difficult for policymakers to reverse the rules. This uncertainty leaves savers in a tricky position, as they try to second-guess the next move by a government.

So, do you make the most of the current pension rules or stay cautious in case Labour reverses the changes? In the past when the LTA has been changed HMRC has introduced protections for those who breached the new lower limit. Therefore, if the cap is reintroduced savers who are over the limit might be able to protect their pot. It is hard to predict how a new government might behave but many are hopeful for some form of protection.

If you are thinking about crystalising your pension early to avoid issues with a Lifetime Allowance tax charge, given the complexity of the matter, you should first consult your financial adviser.

Annual Allowance

It is also worth noting that the pension annual allowance changed from £40,000 to £60,000 on the 6th April 2023. Although there is not a limit on the amount that can be saved into pensions each year, there is a limit on the amount that can benefit from tax relief. The ‘Annual Allowance’ is the limit that an individual can contribute to a pension personally in any given tax year, whilst benefiting from tax relief.

For example, someone receiving a salary of £40,000, would only receive tax relief on personal contributions up to £40,000, but someone on a salary of £80,000, would only attract tax relief on contributions up to £60,000. It is important to note that lower limits apply to high earners or individuals who have already accessed some of their pension funds flexibly.

State Pension

The state pension is due to receive an 8.5% rise this month, taking it from £10,600 to £11,502 a year. This is the second largest percentage rise in the last 30 years. It is worth remembering that this isn’t the case for everyone who is entitled to the state pension, and there is no guarantee that the next government will retain the current “triple-lock” status afforded to the State Pension.

You can read more about specific pension details published in the Autumn Statement here.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.