Skip to main content

Skip to main content

What is the average retirement income in the UK?

On face value the question of ‘what is the average’ is a simple one, the answer is £595 per week (£30,940 p.a.) for a retired couple and £282 per week (£14,664 p.a.) for a single retiree as per the most up to date Government Pensioners’ Income figures.

However, these figures do not take into account that everyone’s retirement looks different and so the question of ‘what is the average retirement income in the UK’ shouldn’t be boiled down to a static annual figure and should be looked upon through a more personal lens - by its nature, an average will not be the right amount for everyone.

Arrange your free initial consultation

Retirement Living Standards in the UK

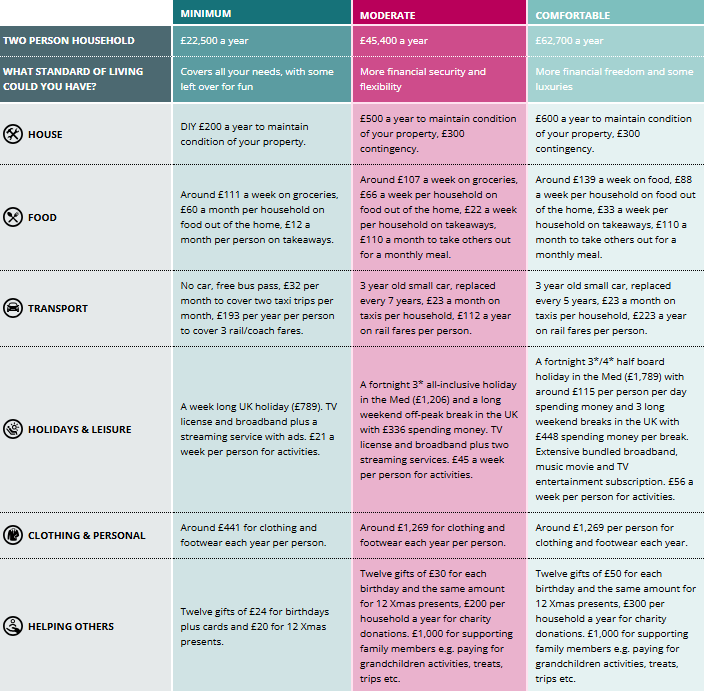

The Pensions and Lifetime Savings Association have conducted a study using independent research provided by Loughborough University which looks into Retirement Living Standards in the UK. The study looks at average retirement income in a more lifestyle focused manner by outlining examples of what specific retirement income groups could look like in more tangible ways. The groups are split into Minimum, Moderate and Comfortable and can be seen below for both single retirees and couples.

Figure 1 - Types of expenditure - Single, Source: Pensions and Lifetime Savings Association, 2026

Figure 2 - Types of expenditure - Couple, Source: Pensions and Lifetime Savings Association, 2026

*The figures shown are the amounts of annual expenditure required to achieve the living standard (i.e. they are not gross income figures).

These tables suggest possible lifestyles which could be achieved at different levels of income in retirement. Although this is an attempt to address the average retirement income through real world examples of expenditure, the truth is that retirement income is subjective and truly depends on the individual’s circumstances and desires.

Retirement income has become a bigger personal concern, especially in today’s environment of rising living costs and unpredictable investment markets. Everyone is feeling the pressure on their standard of living, but it’s especially challenging for those who are nearing or already in retirement. Those who are used to living a ‘comfortable’ retirement may now be in a position more aligned to a ‘moderate’ retirement.

What is a ‘good’ monthly retirement income?

A ‘good’ monthly retirement income will depend on the lifestyle you want to maintain and the financial commitments you expect to have once you stop working.

For some people this may mean covering only essential living costs such as housing, food and utilities, while others may want enough income to support travel, hobbies and regular leisure spending.

Using the Retirement Living Standards as a guide, a single person may need the equivalent of around £1,158 per month for a minimum standard of retirement living and up to roughly £3,783 per month for a more comfortable lifestyle. For couples, the required income is typically higher overall but lower per person due to shared household costs. These figures provide a useful benchmark, but the most appropriate monthly retirement income will always depend on your personal circumstances and long-term financial goals.

What is the average retirement income for a single person?

As shown in the table above, the amount that needs to be saved for retirement depends on the lifestyle you want to achieve. For a single person, this varies from an income of £13,900 a year for a minimum retirement to £45,400 a year for a comfortable retirement. These figures are just estimates, intended to give you an idea of the kind of lifestyle you might expect with each level of retirement income.

What is the average income for a retired couple?

The figures for a retired couple start at £22,500 and rise to £62,700, according to the Retirement Living Standards tables, with £44,900 considered ‘moderate’.

Whether you are a couple or single, there are additional factors that can impact the level of income you may need. For instance, those with dependents may have further financial commitments and a different lifestyle to those with no dependents.

Factors that influence retirement income

There are a number of factors that can influence the level of income you may require in retirement. Your housing situation can play a significant role, as those who have fully paid off their mortgage may have fewer regular expenses than those who are still renting or repaying borrowing.

Your lifestyle choices will also have a considerable impact on your income needs. Some retirees prefer a quieter lifestyle focused on home and family, while others may wish to travel regularly, pursue hobbies or provide financial support to children and grandchildren. Each of these choices can affect the amount of income required to maintain your preferred standard of living.

Health considerations and life expectancy can also influence retirement planning. Longer retirements may require savings to stretch further, while potential healthcare or care costs later in life can place additional demands on your finances. Taking these factors into account early can help create a more realistic and sustainable retirement income plan.

How much income do I need in retirement?

For many people, private and state pensions could go a long way to building up retirement income. The full state pension for 2026/27 is £12,547 per year, up from £11,973 in 2025/26. Additionally, adopting the right tax-efficient strategy for your situation could make all the difference. It could be that different pots of savings and pensions are drawn down on at different stages to get your target income to fund the lifestyle you are looking for. Everyone's “need” in retirement will be different, but it should be reflective of what is achievable and affordable within the savings and pensions you have amassed.

Planning your retirement

The key to peace of mind and a stress-free retirement is planning. Planning allows you to spend the money you have saved without fear that you’ll run out. Knowing how much you’ll need and how long your money will last as well as how much you can afford to spend is vital. That switch from using income to build capital to using capital to provide income can be daunting.

It’s essential to make sure you plan as early as you can, to forecast if the money and assets you have set aside for your retirement will be enough to see you through. At TPO we use a tool called Cash Flow Forecasting. It gives you control over your finances so you can live comfortably now, be prepared for unexpected expenses or changes in circumstances, and still have a secure future to look forward to.

Retirement Calculator

A useful tool to get a basic understanding of this is our retirement calculator. From your own inputs, you will be able to forecast an estimate of the pension income you will get when you retire and receive a target retirement income to aim for based on your choices, taking into account your salary.

How to increase your retirement income

Increasing your retirement income is certainly achievable with appropriate planning and foresight; we are massively incentivised by the government to save for retirement through the tax relief on pension contributions and the legal obligation for your employer to pay into a workplace scheme. Taking advantage of these reliefs and putting money aside as early as possible for your retirement can have a real tangible impact on your retirement income.

Additionally, pension funding is the only allowance which can be backdated for up to three tax years, known as 'Carry Forward' rule, this means any of your unused allowance from previous tax years can be brought forward and invested into your pension.

Furthermore, to fund whatever retirement income your lifestyle needs, you don’t need to solely rely on pension savings and the State Pensions. ISAs, cash and other investment vehicles can also be used to fund your retirement. ISAs are particularly useful with their tax-free status, allowing you to draw tax free income when you need it.

We are lucky that we now have more information and more choice on how we plan for the future. A good starting point is to try and envisage what a good retirement will look like you for. This will in turn enable you to ensure you are maximising the relief and allowances which are inherently designed to increase the level of retirement income you can enjoy. Starting retirement saving late shouldn’t be disregarded, as any effort to put away money can have a noticeable difference and impact the retirement you can look forward too.

How does the average retirement income compare to average earnings?

Pre-retirement expenditure needs can vastly differ from your income requirements in retirement. The median gross salary for full-time workers in the UK (male and female) in 2025, according to the Office for National Statistics, was £35,828 p.a. As we have investigated, this is significantly higher than the average retirement income for a single individual of £14,664 p.a.

In retirement people often face different expenses compared to their working years. While some costs like commuting may decrease, healthcare and long-term care costs can rise. Furthermore, one of the largest outgoings individuals face whilst working is mortgages - retirees will generally have paid off their mortgage liability as they begin to transition towards their sources of retirement income to fund their lifestyle. Therefore, the income needed in retirement will inevitably differ from working years.

A standard measure that can be used to assess retirement needs is the replacement ratio, which is the percentage of pre-retirement income that is replaced by retirement income. As a rule of thumb, most people may need to replace between 60%-80% of their pre-retirement household income, before tax, in order to maintain their lifestyle in retirement. However, the average retirement income is far lower than 60% of the average income for full-time workers in the UK (60% of £35,828 is £21,497). Therefore, this serves to reinforce the notion that retirement income is circumstantial for each individual, depending on their unique needs and objectives.

How to plan for your retirement income

Retirement is personal and not just as straightforward as an average number given to you.

By considering what your retirement might look like in advance, you can plan, utilise allowances and the tax reliefs granted to you by the government to build your wealth, which you can later draw on to fund your retirement.

Here at TPO we use cash flow modelling to visualise your retirement and track the progress towards your goals. This process maps out your financial future and shows you the difference even small changes can make. We will assist you in constructing a tax-efficient strategy to achieve the level of retirement income you hope to gain. If you would like to have an initial free consultation to discuss your retirement plan, please get in touch.

Arrange your free initial consultation

The value of investments can fall as well as rise. You may not get back what you invest.

The Financial Conduct Authority (FCA) do not regulate estate or cash flow planning, or tax advice.