Skip to main content

Skip to main content

Transitional arrangements for NI top up extended to 31 July 2023

In 2016, the Basic State Pension changed to the New State Pension and the rules about the number of years credit needed to get the full benefit also changed. The new rules state that you need 35 years full credits to be eligible for full state pension and that if you have less than ten years’ service you won’t get any State Pension.

However, there are also transitional protections to ensure that no one who has earned credits under the old system is worse off, but this adds additional levels of complexity. The starting point should always be getting a State Pension statement, which can very easily be obtained using the Government Gateway. Sign up and access only take minutes.

Part of the transitional protection, because of the need to have more than the previous 30 years credits and because many people were contracted out of the State Pension prior to 2012 allows the purchase of missing years. This protection, if eligible, allows the purchase of full or part years that are missing all the way back to 2006. This option is being removed on 31 July 2023 and will revert to the standard six years as per legislation.

Now is the time to consider if there are gaps that need filling and make the most of the option to go back to 2006. Not everyone needs to fill gaps, even if they currently don’t have full State Pension entitlement and care needs to be taken to avoid buying years unnecessarily.

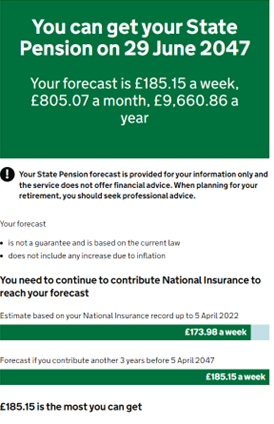

When looking at the State Pension forecast then the first thing to consider is the projected pension figure, and then what you have already earned based on the current records and how many more years you need to get the full amount.

If the forecast shows, as in the example shown, that only three more years are needed, and you intend to work full time or receive credits for three years, then there is no need to do anything more. In addition, with just three years to accrue before retirement, then buying additional years should you decide to cease work shouldn’t be a problem because there are plenty of years until State Pension Age. There are other ways in which to accrue State Pension credits some of which are automatic and some need to be claimed.

More consideration is required where the numbers are more challenging if there is a disparity between what you can hope to accrue before you reach State Pension Age.

In some cases, the forecast may seem too low. This can be for a number of reasons. For example, contracting out of the State Second Pension or SERPS. This could have resulted in a Contracted Out Pension Equivalent (COPE) deduction being made to the forecast. The COPE deduction is already included in the forecast, so there is no need to try and factor this additional information in. However, because the New State Pension accrues at a flat rate of 1/35th for each year of credits under the new system, if you work longer then you can still get the full New State Pension at State Pension Age. However, it is worth noting Class 1 and Class 2 National Insurance contributions cease at State Pension age even if you work beyond State Pension Age.

The article is for general information only, does not constitute individual advice and should not be used to inform financial decisions.

This information is correct as of 16/03/2023