Skip to main content

Skip to main content

Six common investment errors

Investing is one of the most effective ways to build long-term wealth, yet even the most experienced investors can fall into common traps that undermine their financial success. Emotional decision-making, cognitive biases, and the lure of quick profits can all lead to costly errors that may take years to recover from. By recognising these pitfalls in advance, investors can make more rational, informed decisions and stay focused on their long-term financial goals.

Arrange a free initial consultation

1 - The danger of familiarity bias

Many investors have a tendency to favour what they know, often concentrating their investments in companies, industries, or markets that feel familiar. This is known as ‘familiarity bias’, and while it may provide a sense of comfort, it can also lead to an unbalanced and risky portfolio.

For example, a UK-based investor may be tempted to allocate most of their portfolio to British companies, simply because they recognise the brands.

However, this overexposure to a single market increases vulnerability to domestic economic downturns, political instability, or sector-specific challenges. A well-diversified portfolio should include exposure to different asset classes, industries, and geographic regions to spread risk more effectively.

2 - Holding on for too long

Another common mistake is becoming too attached to a particular investment, even when the evidence suggests it is time to move on. This often happens when investors refuse to sell a declining asset, hoping it will recover to avoid taking a loss. Unfortunately, this reluctance to accept mistakes can lead to even greater losses in the long run.

The decision to sell should always be based on objective analysis rather than emotional attachment. Investors should periodically review their portfolios with a clear and rational mindset, ensuring that every investment still aligns with their overall strategy and personal risk tolerance.

3 - Rushing into investments without proper research

The fear of missing out (FOMO) can be a powerful force in investing, often leading individuals to rush into opportunities without fully understanding the risks. This is particularly common during market booms when prices are soaring, and everyone seems to be making easy money.

Without thorough research, investors may find themselves exposed to assets that are overvalued or fundamentally unsound. Proper due diligence—reviewing financial reports, understanding industry trends, and assessing long-term growth potential—is essential before making any investment decision. A well-planned approach is far more effective than acting on impulse or social media hype. And remember the old saying, ‘If something appears too good to be true, it probably is!”

4 - Being too influenced by recent performance

One of the most pervasive cognitive biases in investing is ‘recency bias’, where investors place too much weight on recent events while ignoring the bigger picture. This can lead to buying assets at their peak simply because they have performed well in the short term or selling assets after a downturn out of fear that losses will continue.

Financial markets move in cycles, and short-term fluctuations do not necessarily indicate a long-term trend. Investors who make decisions based on recent performance alone often find themselves buying high and selling low—exactly the opposite of a successful investment strategy. A disciplined approach, backed by a long-term perspective, can help investors avoid making knee-jerk reactions based on temporary market movements.

5 - The dangers of cryptocurrency and speculative investments

The rise of cryptocurrency has been one of the most dramatic financial stories of the past decade, attracting millions of new investors with the promise of quick gains. While some have made significant profits, others have lost fortunes by getting caught up in the hysteria and failing to understand the risks.

Unlike traditional investments, many cryptocurrencies lack underlying value or a clear regulatory framework. Prices can be highly volatile, often driven by speculation rather than fundamentals. As cryptocurrency is not regulated in the UK, there are many risks associated with it, and investors should therefore approach it with caution. Due to a lack of broader adoption in the regulated advisory space, there are also a lack of experts that can give appropriate and informed advice in this area. That is why it is crucial to understand the risks before investing any sum of money in the crypto, whether it be Bitcoin or any other virtual currency.

Speculative investments, whether in crypto, meme stocks, or high-risk startups, should never form the foundation of a financial strategy. A strong portfolio is built on stable, well-researched investments with a proven track record of delivering returns over time.

6 - Failing to seek professional advice

Perhaps the most overlooked mistake is assuming that investing is simple enough to do without expert guidance. While self-education is crucial, professional financial advice can help investors navigate complex markets, manage risks effectively, and build a strategy tailored to their personal goals.

A financial adviser can provide an objective perspective, helping investors avoid emotional decision-making and ensuring they stay on track for their own personal long-term success. Whether it's building a diversified portfolio, managing tax-efficient investments, or planning for retirement, professional advice can make a significant difference in overall financial outcomes. And remember, your success is different to the next persons, so using an experienced Adviser helps to define exactly what your financial gaols and success looks like.

At TPO, we help investors make informed decisions, avoid common pitfalls, and build long-term wealth with confidence. If you want to ensure your investment strategy is on the right track, contact us today to see how we can help.

Arrange a free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

Investment returns are not guaranteed, and you may get back less than you originally invested.

Past performance is not a guide to future returns.

Technology turbulence and regional gains

After a pullback in December 2024, we saw global equities resume their move upwards as the MSCI World index returned 3% in January 2025. However, as we discussed recently, investors should be prepared for volatility and we saw a brief but volatile episode towards the end of the month with the emergence of DeepSeek.

Arrange your free initial consultation

DeepSeek, AI and Technology Stocks

DeepSeek – a Chinese AI company – has developed an AI model which reportedly has comparable quality to OpenAI (a US AI company) but at a fraction of the cost. Initial estimates are that DeepSeek spent just $6m dollars developing the model compared to the $5bn that OpenAI is expected to spend this year.

This came as a surprise to investors as export controls have limited the sale of Nvidia’s high powered Graphic Processing Units (GPU’s) to Chinese companies. As a result investors have begun to question the return that will be made on the vast amounts of capital that US technology companies have invested into AI projects.

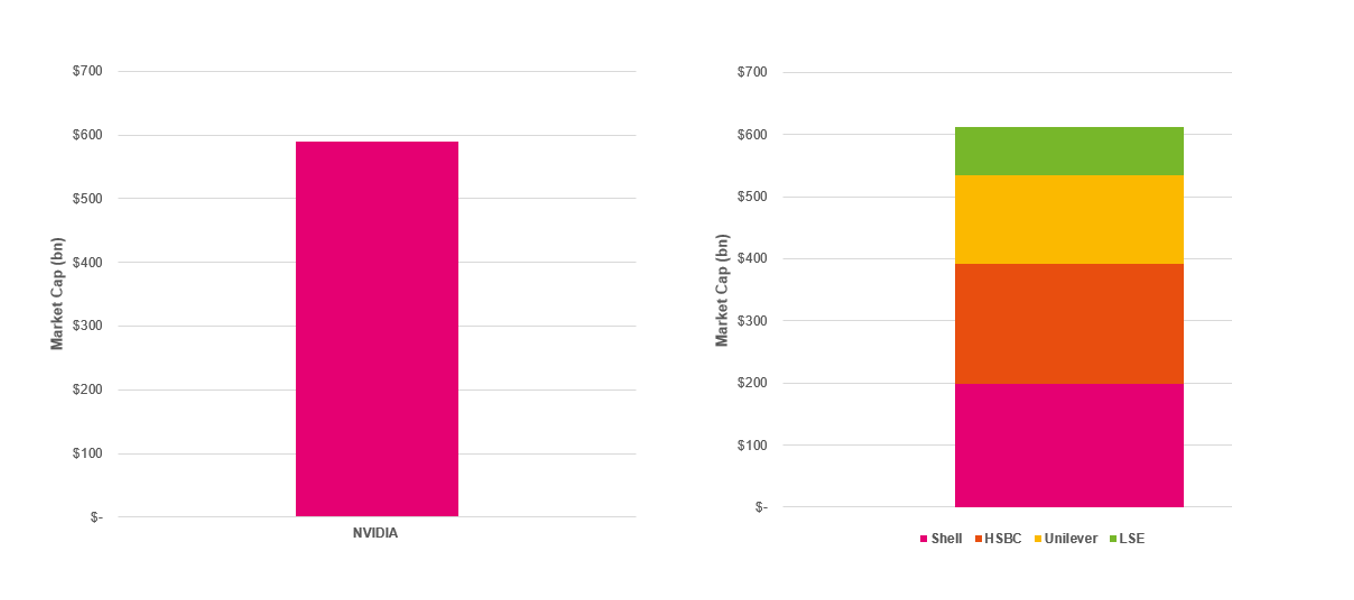

Following this announcement we saw Nvidia post the largest drawdown in US history with the company falling 17% on the news, which was a $600bn loss in market capitalisation. To put this into context, $600bn is the entire market capitalisation of Shell, HSBC, Unilever and the London Stock Exchange (see Figure 1).

Figure 1. The fall in Nvidia’s share price was the equivalent to the market capitalisation of four UK equity market stalwarts (Source: TradingView)

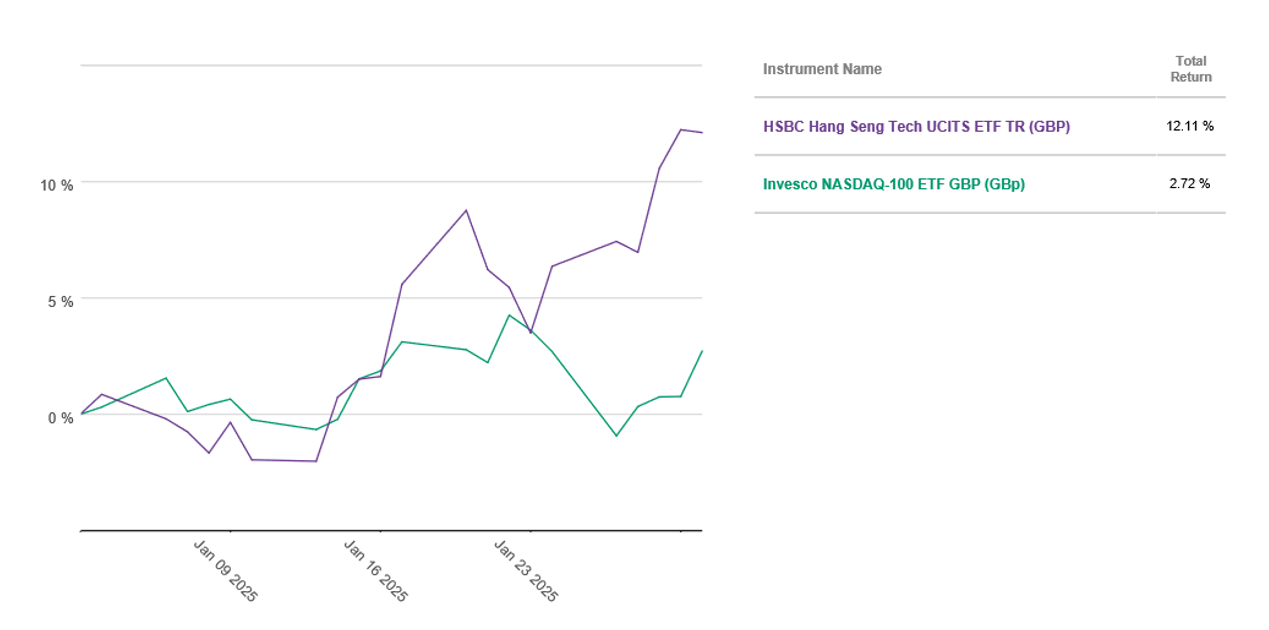

Whilst Nvidia fell we saw Chinese Technology companies rally on the news as investors began to reappraise the outlook for the sector and begin to question the dominance of US technology companies.

The Hang Seng Tech index which is a composite of the 30 largest technology companies listed in Hong Kong and includes companies like Alibaba, JD.com and Tencent, rallied 3% on the day and finished the month 12% up. This compares to the US tech centric NASDAQ index which returned just 2.7% over the same time period.

Figure 2. Chinese technology companies rallied on the news of DeepSeek (Source: Pacific Asset Management)

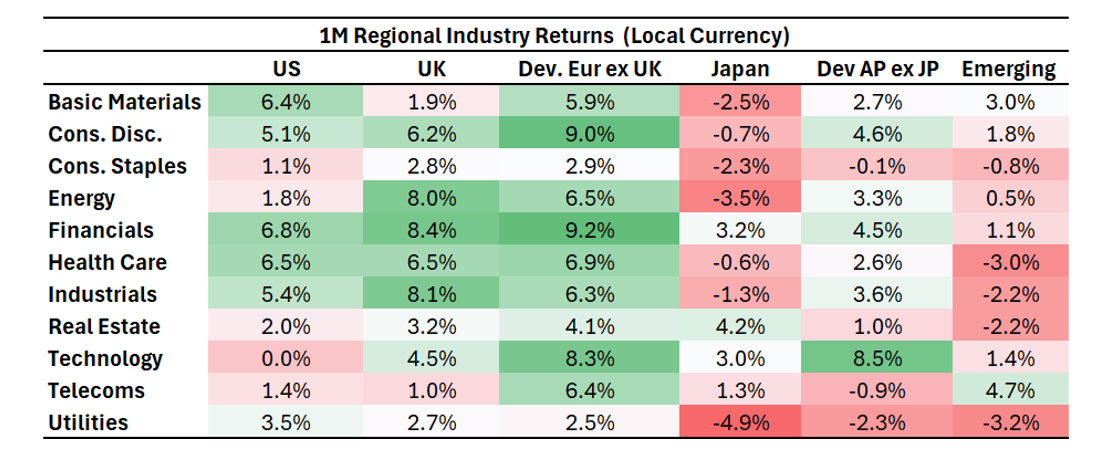

We also observed a broader rotation within the US as the S&P 500 equal weight index – an index where each company has the same weight (0.20%) – outperformed the S&P 500 which has a 35% allocation to just seven (‘Magnificent’) stocks.

Part of this is due to the composition of the equal weight index which has less exposure to technology companies (a 13% allocation compared to the 36% allocation in the S&P 500) and a larger allocation to industrials and healthcare both of which outperformed technology last month (see Figure 3).

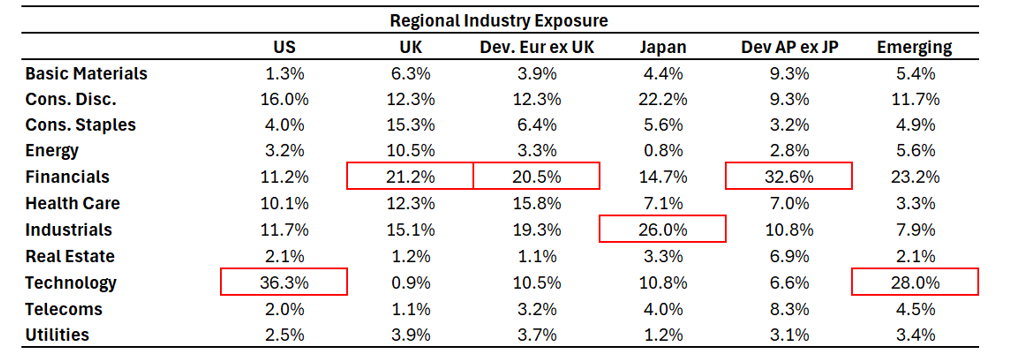

Figure 3. Returns of regional industry sectors (Source: FTSE Russell)

Regional Returns and Sector Rotation

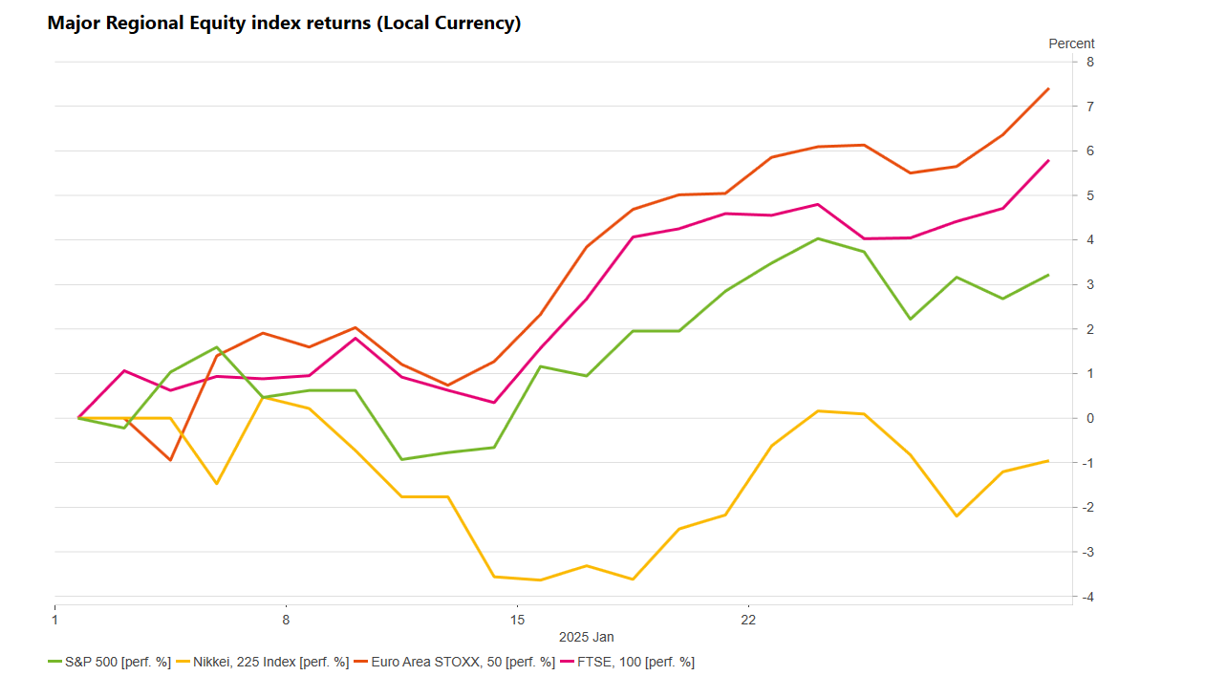

In a rare showing we saw both European and UK equities outperform US equities last month.

Economic growth in Europe continues to be modest. However, an improvement in business activity and ECB interest rates cuts have provided a supportive backdrop for European equities with the Euro Stoxx index up 7.9% last month.

In the UK and Japan we saw moves in the respective countries currency drive equity returns. A weakening pound sterling supported UK equities given that 75% of the revenue generated by companies listed on the FTSE 100 is earned overseas, a weakening pound increases the value of overseas earnings. Meanwhile in Japan we continue to see strong wage growth and the Bank of Japan have indicated that there will be further rate increases which saw the Yen rally against the Dollar. This weighed on the export focused Japanese equity market as Japanese exports became relatively more expensive due to relative Yen appreciation.

Figure 4. Returns of regional equity indices (Source: Macrobond)

Figure 4. Returns of regional equity indices (Source: Macrobond)

Another important consideration for investors is the industry exposure of regional equity markets.

One reason why the US equity market has been so dominant in recent years is due to the index’s exposure to technology companies. Around 36% of the S&P 500 is in technology companies compared to less than 1% in the FTSE 100.

By comparison the UK equity market can be described as the ‘old economy’ with a larger allocation to Industrials such as Financials and Energy. Similarly in Europe there is a larger allocation to Industrials and Healthcare and again a relative underweight to Technology (see Figure 5).

Figure 5. Regional industry exposure (Source: FTSE Russell)

Figure 5. Regional industry exposure (Source: FTSE Russell)

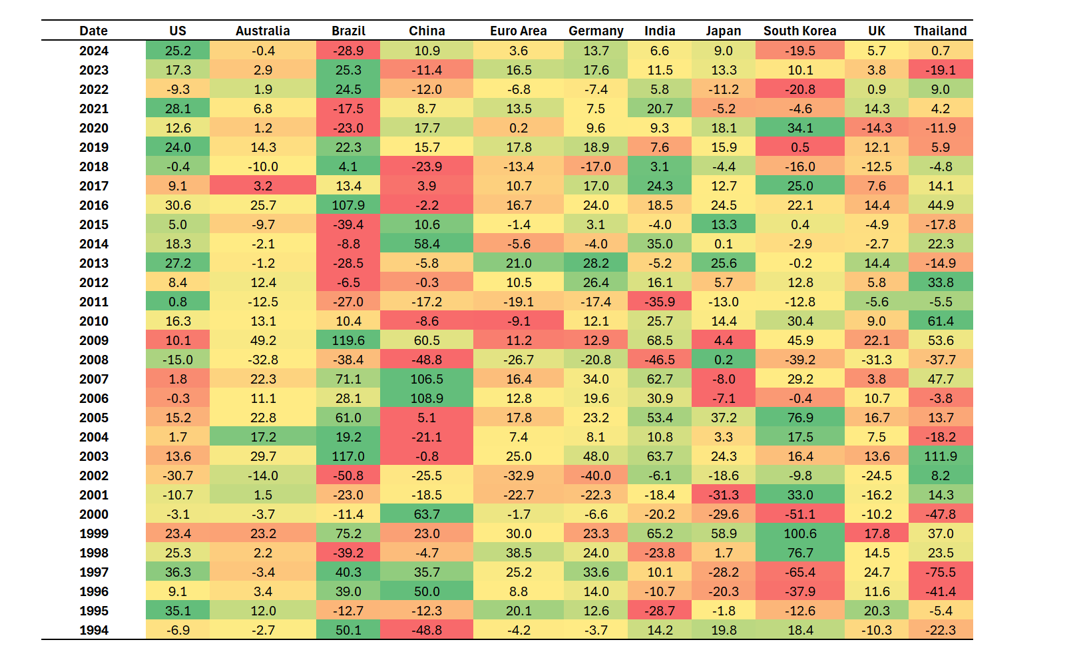

Given the noise in financial markets it can be useful to step back and reassess where we are or what prevailing narratives are on the mind of investors. One of these is the exceptionalism of the US economy (and equity market) and whether this will continue.

We retain a positive outlook for the US given the robustness of the economy and relative strength of US corporates, however we’re mindful that no individual country continuously outperforms.

You can see this when we look at the returns of various equity markets over the last thirty years. It also highlights the potential opportunity that investors have by looking beyond the US and being proactively tactical with their investments (see Figure 6).

Figure 6. Historic equity returns (in sterling) have varied significantly over the last 30 years (Source: Macrobond)

Conclusion

Last month was another example of the benefits of having a diversified portfolio.

Increased volatility in markets typically creates opportunities to buy assets at more attractive valuations or take advantage of short-term trends. By being proactive investors can strategically adjust their allocations to asset classes, regions and sectors to not just reduce overall risk but also potentially improve total returns.

As ever, if you have any questions about navigating your personal investment environment, please don’t hesitate to contact your adviser or one of the TPO team.

Arrange your free initial consultation

The information in this article is correct as at 14/02/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

Why we all need a digital death file

Who deals with the finances in your household? Would your family know where to look should something happen to you?

In the past, having a Will would be how your final wishes were granted for the distribution of your assets after death…

Arrange your free initial consultation

But is it enough in the new digital world?

As the financial industry transitions towards increasingly using technology, your loved ones are unlikely to unearth your financial information by searching through a physical filing cabinet. Finder, a global fintech, estimates that in the UK alone, 47 million people use some form of online or remote banking – that’s 87%! In the last decade especially, each of our digital footprints has grown exponentially. With multiple logins, passwords, usernames and accounts held across different websites and portals it’s hard to keep track yourself. The question is, how would your loved ones cope with this should you pass away?

No one can dispute that navigating the death of a loved one is one of life’s biggest challenges. To further complicate things, a recent survey by consumer group Which? has indicated that 76% of members surveyed had left no plan for what to do with their digital assets should they die.

Removing the additional complexity of trying to locate relevant documents to settle your estate can only be of benefit to those you leave behind. Although you can name a ‘digital executor’ in your will, this does not extend to consolidation of your financial affairs into one accessible place. TPO Wealth solves this problem for you.

What is TPO Wealth?

At The Private Office, all our clients have access to a digital filing cabinet, at no additional cost, through our secure online portal TPO Wealth. As with a physical filing cabinet, here documents can be stored safely and securely. By leaving behind instructions for family members on how to access this, the painful process of settling your estate can be expediated and enhanced.

With your consent, your solicitors and accountants can also access information you deem appropriate, such as tax returns. This capability allows for a seamless and effortless experience for you. You can have confidence that your information is safe, whilst allowing trusted contacts to have access to relevant documents.

Our clients use TPO Wealth to file personal financial documents and those they choose to share with professional contacts, such as their:

- Tax Information

- Will

- Details of any trusts they may have

- Invoices

- Details of professional contacts

- In case of emergency details

This can be particularly useful for the self-employed. As of October 2024, the statistical agency Statista estimates that 4,383,000 people in the UK are self-employed. That’s 13.1% of the workforce! Granting your accountant access to secure documents on TPO Wealth could substantially speed up the arduous process of filing tax returns and completing annual accounts.

With all the information neatly stored in one place, the need for time consuming back-and-forth is reduced. You’re free to get on with life’s more important things.

What about if you become incapacitated?

Beside from the death of a loved one, information may be required, in other instances. Consider critical illness or incapacity. Should something happen to you, access to your TPO Wealth account and those within the remit of your Power of Attorney rights can be granted. Ministry of Justice data from 2024 indicates just how slow the Lasting Power of Attorney process can be – in fact, one application was finally processed in 2024 after a total of 2,777 working days!

Would you like to take control of your finances?

Beyond secured storage of important files, with TPO Wealth you can track investment performance and the growth of your savings, across various accounts with different providers, all in one place. Using clear graphics, our clients can track the value of their net-worth in real time. Features such as an in-built property value calculator contribute towards overall peace of mind, as you can get a clear picture of the state of your finances, all at your fingertips.

If you’d like to learn more about how TPO Wealth can help to consolidate your financial affairs into one simple, easy-to-use place, we would be happy to help.

So why not get in touch?

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

TPO Wealth is only available to clients of The Private Office.

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

Higher bond yields spike investor interest

In last month’s update we spoke about two prominent themes we see evolving over the course of this year. The first was regarding the diverging and contrasting growth outlook for the US compared to the rest of the world. The second relating to inflation and the challenge that Central Banks face in bringing inflation down to target and what this means for interest rate policy.

Arrange your free initial consultation

Interest Rate Cuts: A Non-Uniform Picture

Our base case would be one where we continue to see cuts in interest rates, however we do not expect this to be uniform. We’ve seen a stark revision to the outlook of interest rates with the market now pricing in just two cuts in the US compared to the six cuts that were priced in back in October. This is in contrast to the UK where weakening economic growth and uncertain outlook is likely to necessitate more rate cuts from the Bank of England.

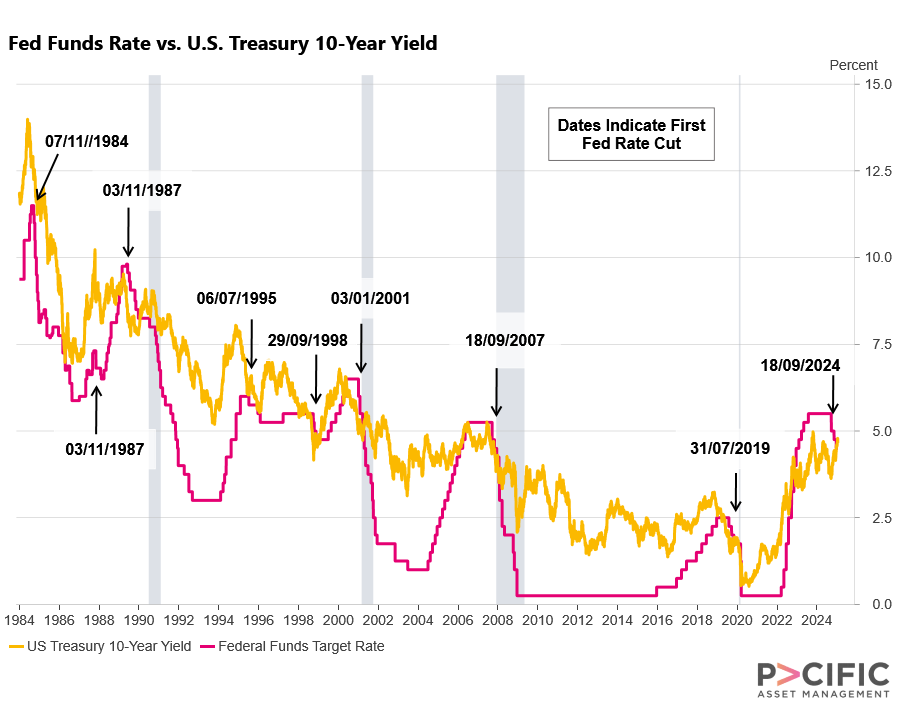

An Unusual Trend in Yields

This backdrop has created a somewhat unusual occurrence where interest rates have fallen (and are expected to fall further) but long-term yields have increased (see Figure 1.).

In the US, historically, when the Federal Reserve have first cut interest rates, the 10-year yield declined causing bond prices to rise. However, since the Federal Reserve cut rates back in September, we’ve seen a marked move up in yields which has been a painful experience for investors holding longer duration (more interest rate sensitive) bonds, as their prices have fallen.

Figure 1. Fed Funds Rate vs US Treasury 10-year yield 1984-2025 (Source: Macrobond)

Figure 1. Fed Funds Rate vs US Treasury 10-year yield 1984-2025 (Source: Macrobond)

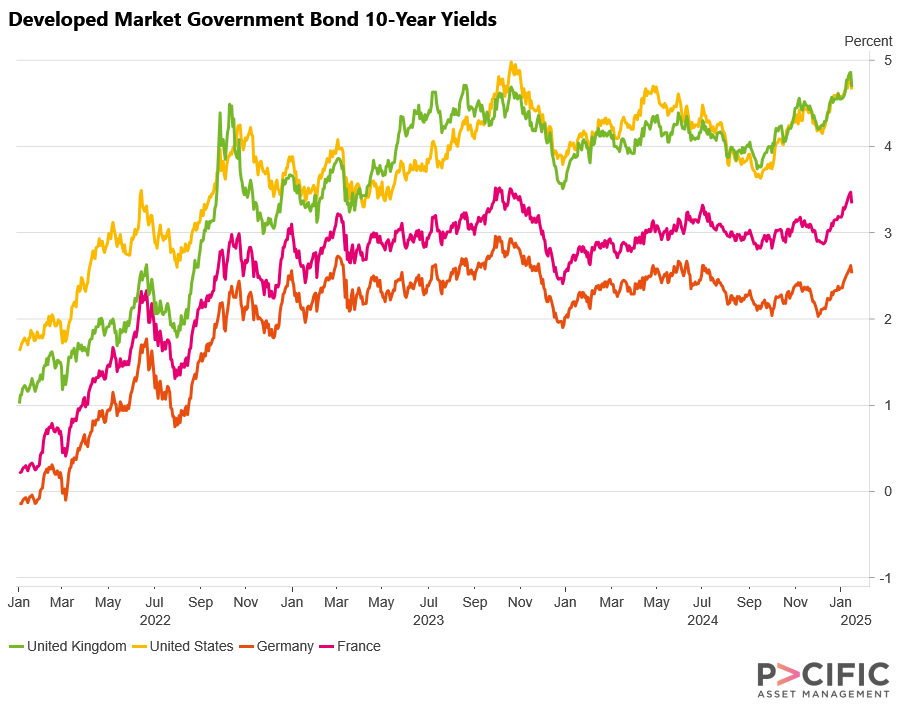

It’s important to note that this is not just a US phenomenon as we’ve seen a move up in long-term Government Bond yields in the UK and Europe as well (see Figure 2).

Figure 2. UK vs Developed Market 10-year Government Bond yields (Source: Macrobond)

Figure 2. UK vs Developed Market 10-year Government Bond yields (Source: Macrobond)

Factors Driving Higher Long-Term Yields

It has been well publicised that UK borrowing costs are now at a high not seen since 1998, however whilst there is uncertainty regarding the outlook of the UK economy there’s little to suggest at this stage there’s a broader issue in the UK Government Bond market.

Instead, the rise in long-term yields can be explained by the prospect of interest rates remaining higher for longer, concerns around inflation and the expected increase in the supply of bonds as Governments look to continue with expansionary fiscal policies.

Looking ahead we expect there to be continued volatility in yields, however with inflation falling and real yields now positive we think investors can be opportunistic in this space.

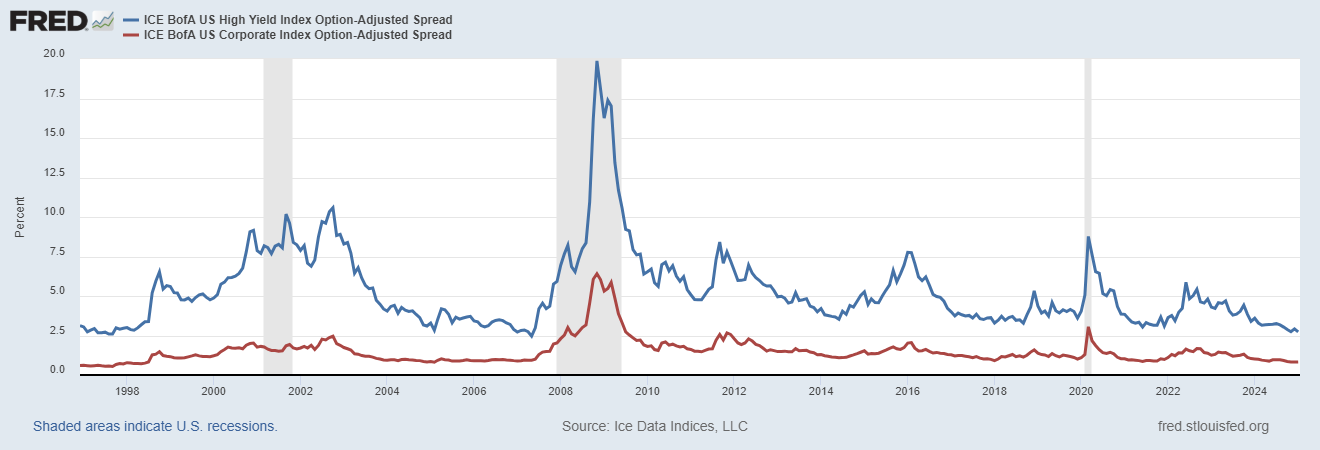

Corporate Bonds: Balancing Risks and Opportunities

For corporate bonds the overall yield remains high but come into the year trading at a rich valuation given that the spread (the compensation one gets for investing into corporate debt) on Investment Grade and High Yield bonds are heading towards historic lows (see Figure 3.)

Figure 3. US Investment Grade and High Yield spreads (Source: FRED, January 2025)

At face value this can seem counterintuitive given the outlook for global growth which we discussed in last month’s update and the uncertainty around inflation and interest rates, which brings to mind the adage that the economy is not the market and the market is not the economy.

The absence of a hard landing, along with corporates issuing debt at low interest rates, has left them well-positioned to meet their ongoing financial obligations. We have witnessed some softening in interest coverage ratios - a measure of a company's capacity to pay its debt - in recent months, but we do not expect a significant widening in spreads given the current strength of corporate balance sheets.

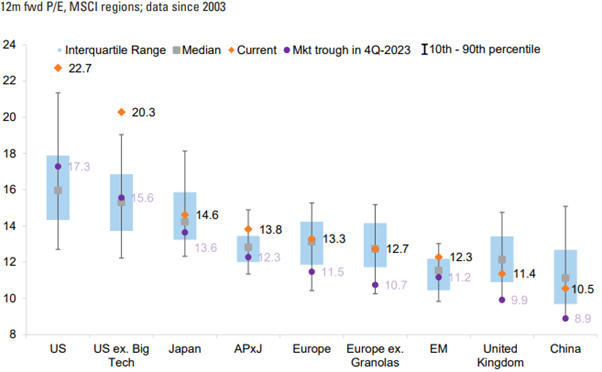

Equity Valuations: Optimism or overreach?

The strength of corporates has also been a contributor to a continued increase in equity valuations. Since the trough in Q4 2023 valuations have moved up across regions with the forward price-to-earnings ratio in the US now trading above its 20-year high (see Figure 4.)

Figure 4. Regional Forward Price-to-Earnings (Source: Goldman Sachs GIR)

This has seen another remarkable period for US equities and the S&P 500 has trounced the return of other regional markets. This reflecting the strength of the US economy and corporate earnings which have far exceeded their regional peers.

Conclusion

Amid volatility, investors should adopt a prudent, diversified approach, focusing on regional, sectoral, and company-specific factors. Companies with lower valuations, robust earnings, and manageable debt levels are likely to perform well over the next year. While US markets continue to dominate, global diversification could yield significant benefits as economic and earnings growth shifts across regions.

As ever, if you have any questions about navigating your personal investment environment, please don’t hesitate to contact your adviser or one of the TPO team.

Arrange your free initial consultation

The information in this article is correct as at 17/01/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

A Christmas Slaying for the Magnificent Seven

Reflecting on a resilient market year

As we approach the end of the year I find myself experiencing déjà vu.

It has been another remarkable period for risk assets. Fears of a ‘hard landing’ or recession did not materialise and investors were able to ignore the noise of the largest ever global election cycle as c. 50% of the world’s population took to the polls this year.

Arrange your free initial consultation

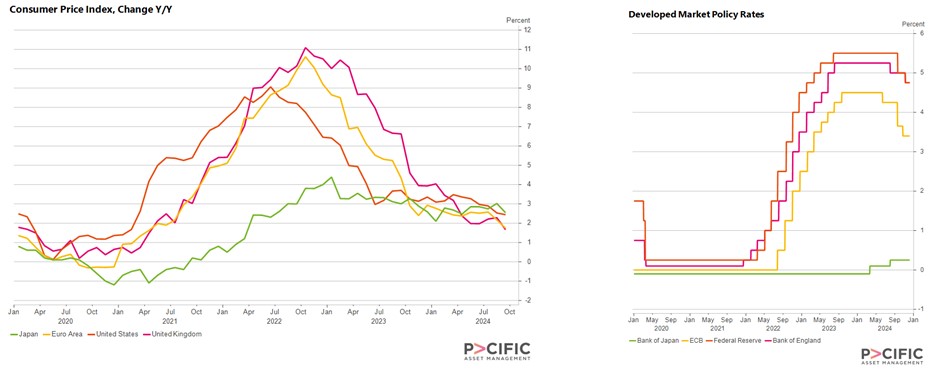

Stable growth and declining inflation

Global growth remained stable and this coincided with headline inflation continuing to fall across the US, UK and Europe and with that, Central Banks in the respective economies have now begun to cut interest rates (see Figure 1.).

Figure 1: Consumer Price and Interest Rates (Source: Macrobond)

Figure 1: Consumer Price and Interest Rates (Source: Macrobond)

Diverging growth prospects for 2025

Moving forward I expect the global economy and financial markets to be something of a mixed picture.

The OECD expects Real Global GDP to be 3.3% next year, however we see growth prospects differing significantly between countries. The US economy is forecasted to grow 2.8% next year whereas Germany (the world’s third largest economy) - which faces a combination of political risk home and abroad and an anaemic manufacturing sector - is expected to grow just 0.7% next year1 .

Inflation trends and labour market shifts

Another consideration is the path of inflation as this will be a key determinant as to how many interest rate cuts we see next year.

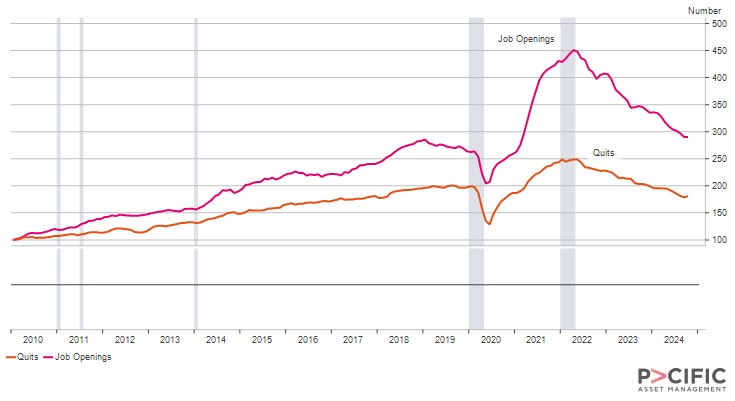

Headline inflation, as mentioned above, has fallen meaningfully, however there are other measures of inflation that Central Banks monitor. One of these is Services inflation which is the measure of prices in the service and hospitality sector. Post- pandemic we saw a distortion in labour markets where there were too few people for the number of jobs available, which saw wage growth in the western world increase as individuals leveraged their position in a limited pool of labour.

However, as the number of job openings has decreased from those post-pandemic highs and the unemployment rate has started to rise, we have started to observe a slowing of pay growth, which has also coincided with some weakening of labour markets.

Additionally, the number of "job quits" in the US has decreased, which offers additional insight into the labour market because, generally speaking, people only want to change professions when there are better roles/openings and when they can earn more money elsewhere (see Figure 2).

Figure 2. US Job Openings and Quits (Source: Macrobond)

Figure 2. US Job Openings and Quits (Source: Macrobond)

Positive outlook for corporate earnings

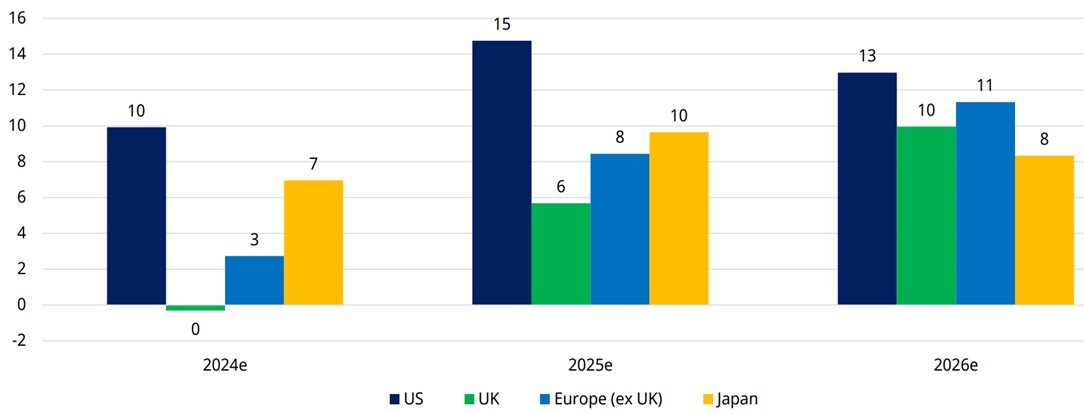

Corporate earnings are expected to improve next year with US corporates (once again) forecasted to produce the highest level of earnings growth.

Figure 3: Corporate Earnings: Consensus YoY EPS growth forecasts % (Source: Schroder Equity Lens – December 2024)

Figure 3: Corporate Earnings: Consensus YoY EPS growth forecasts % (Source: Schroder Equity Lens – December 2024)

The question as to whether this level of earnings growth will materialise will be key for investors.

US equity market performance and valuations

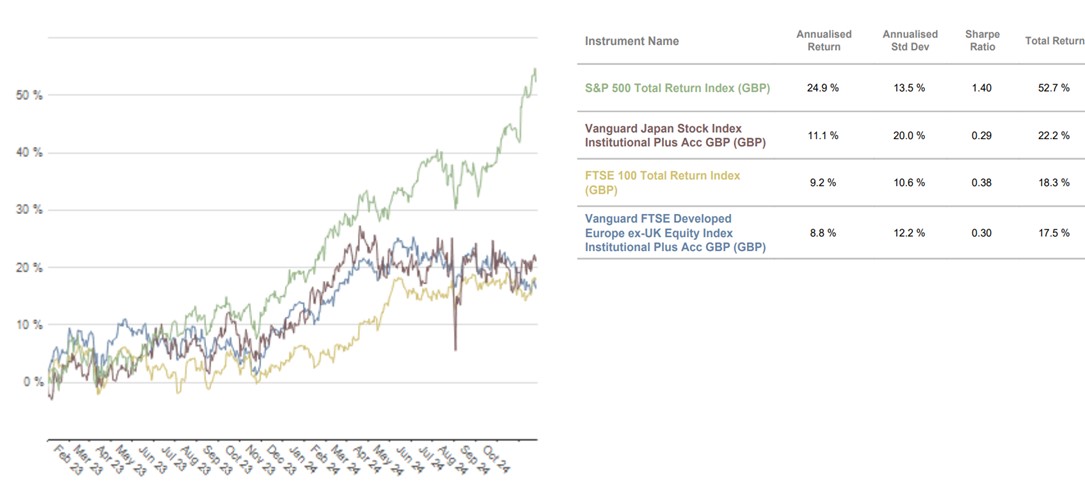

To the end of November, the S&P 500 – an index of the 500 biggest companies in the US – was up c.28% since the start of the year and this followed the less - but still impressive - return of c.19% in 2023. This means (when considering the benefit of compounding) the index is up 53% since January 2023 which is in stark contrast to other regional equity markets where UK, European and Japanese equities returned 17-23% over the same time period (see Figure 4.)

Figure 4. Regional equity returns (Source: Pacific Asset Management)

Figure 4. Regional equity returns (Source: Pacific Asset Management)

Given this relative outperformance of US equities, if you were to look at the MSCI World index which is made up of the largest c. 1,500 public companies in developed markets based on size (the technical term being market ‘capitalisation’) you would see that US equities make up over 70% of the index. This is why investors should be cognisant that when investing into ‘global equities’ they are in turn (and perhaps inadvertently) investing a significant amount into the US stock market.

What this means from a valuation perspective is that US equities are considered expensive, not just compared to other regional equity markets like the UK, but also relative to its own history.

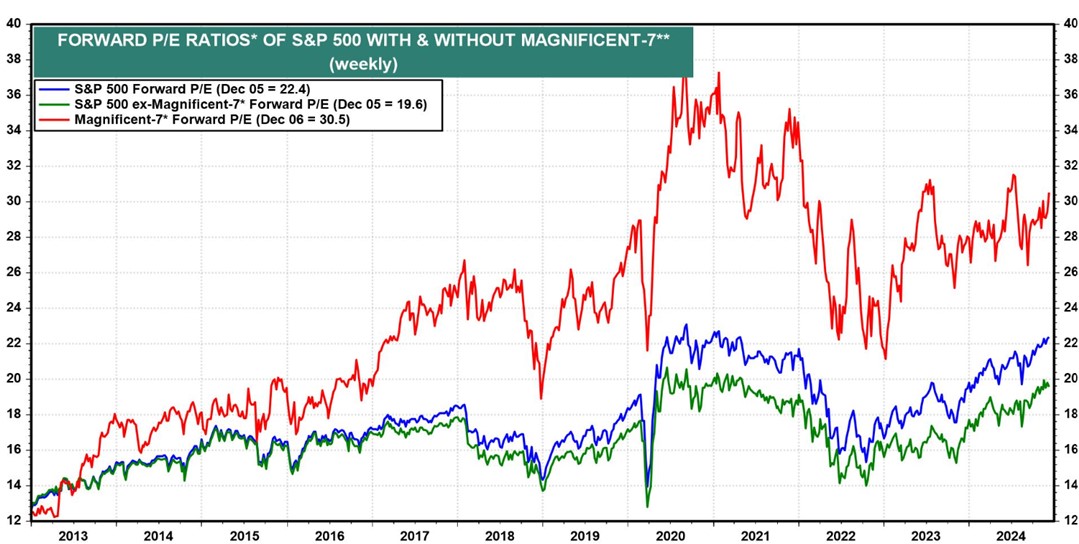

One could have made this comment several times over the last decade and if you were a valuation purist then you would have missed out on a significant return. That said, when you consider the valuation of the ‘Magnificent 7’ - which collectively represent approximately 30% of the S&P 500 - and compare it with the broader index otherwise known as the S&P 493, then it does raise the question of how much of that future earnings growth is already priced in and whether these companies can continue to produce sales growth in excess of 20% per annum2.

The divergence in valuation between the Magnificent 7 and the broader S&P 500 can be seen below where we are comparing their respective forward price-to-earnings ratios i.e a measure of how much an investor must pay for a company’s forecasted earnings in 12 months’ time.

Figure 5. US equity price-to-earnings ratio (Source: Yardeni – December 2024)

Figure 5. US equity price-to-earnings ratio (Source: Yardeni – December 2024)

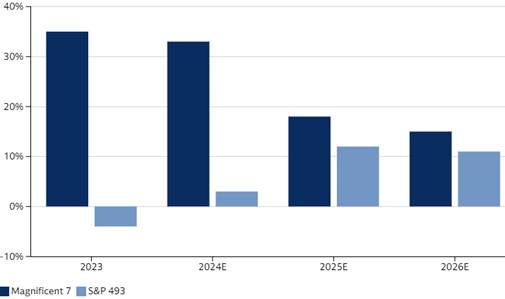

Looking ahead we are certainly not calling an end to the exceptionalism of the US economy and equity market, but we do see a broadening out of this feature.

In 2023 the ‘Magnificent 7’ outperformed on an earnings growth basis and they benefited accordingly, however it is expected that we will see an improvement in earnings for companies in the ‘S&P 493’ which when you consider the relatively cheap valuation compared to their ‘magnificent’ peers could represent an opportunity for investors.

Figure 6. US earnings expectations (Source: Goldman Sachs research – December 2024)

Figure 6. US earnings expectations (Source: Goldman Sachs research – December 2024)

Looking ahead to 2025

We will return to the outlook for 2025 in January. However, reflecting on 2024 suggests that next year will be a year where investors should reacquaint themselves with the fundamentals of investing, for instance, companies that are improving their earnings whilst trading at a cheap valuation should do well over the long-term. Having a diversified portfolio will continue to reduce risk but will also provide the opportunity for returns in markets which some investors have (up until recently) neglected.

As ever, if you have any questions about navigating your personal investment environment, please don’t hesitate to contact your adviser or one of the TPO team.

Arrange your free initial consultation

Notes:

1 Figures referenced are from the OECD’s latest economic outlook which was released on 4 December 2024

2 The Magnificent 7 refers to Apple, Microsoft, Amazon, Alphabet (Google), Tesla, Nvidia and Meta Platforms.

The information in this article is correct as at 13/12/2024.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

Trump's return - investment boom or inflationary timebomb?

The US election has dominated headlines and markets over the recent past, with each upwards swing in Trump’s odds driving the dollar and US government bond yields higher. Now that the US election has delivered a new President, we can consider how markets have reacted and the broader economic implications.

Arrange your free initial consultation

Trump's Consolidation of Power

It is now clear that Donald Trump and the Republicans have won a resounding victory, sweeping the Presidency, the Senate, and the House of Representatives. Additionally, the Republicans retain a majority in the Supreme Court and are expected to ‘pack the benches’ of the lower courts at the beginning of the Trump presidency. This result gives Trump almost complete control over the three arms of US government, making it likely that he will be able to push forward with his agenda relatively unimpeded.

What does the 47th President intend to do with this power? Separating rhetoric from policy can be difficult with Trump, as exaggerated rhetoric is often used as a negotiating tactic and is part of Trump’s ‘Art of the Deal’. A sense of what really matters to Trump can be gleaned from his most frequent public utterances on certain policy issues.

Key Economic Priorities Under Trump

The three most consistent issues with economic implications have been:

- Reductions in immigration and closing of the loopholes in the asylum system

- The China trade threat

- The use of tariff policy to rebalance American trade

US Equity Market Response

In recent years he has also flipped his script on the need for a balanced government budget, from a fiscal hawk in the 80s and 90s to ‘the great protector’ of social security programs in the 2024 election. Continued lavish government spending in combination with his proposed tax cuts creates inflationary pressure.

At a headline level the pursuit of these aims has two primary economic impacts, the first being upwards pressure on medium-to-long term inflation, the second being an increased incentive to bring goods manufacturing back to the US.

The inflationary aspect causes rising government bond yields (investors must be compensated for the risk of rising inflation over the period they hold a bond), which, in combination with the direct appreciation impact of tariffs and the smaller trade deficits they produce, have resulted in upwards pressure in the value of the dollar. The manufacturing onshoring aspect has been a boon to the stock prices of medium and smaller sized US companies that are more exposed to domestic US supply chains and will therefore see the most benefit from a rejuvenation in those supply chains.

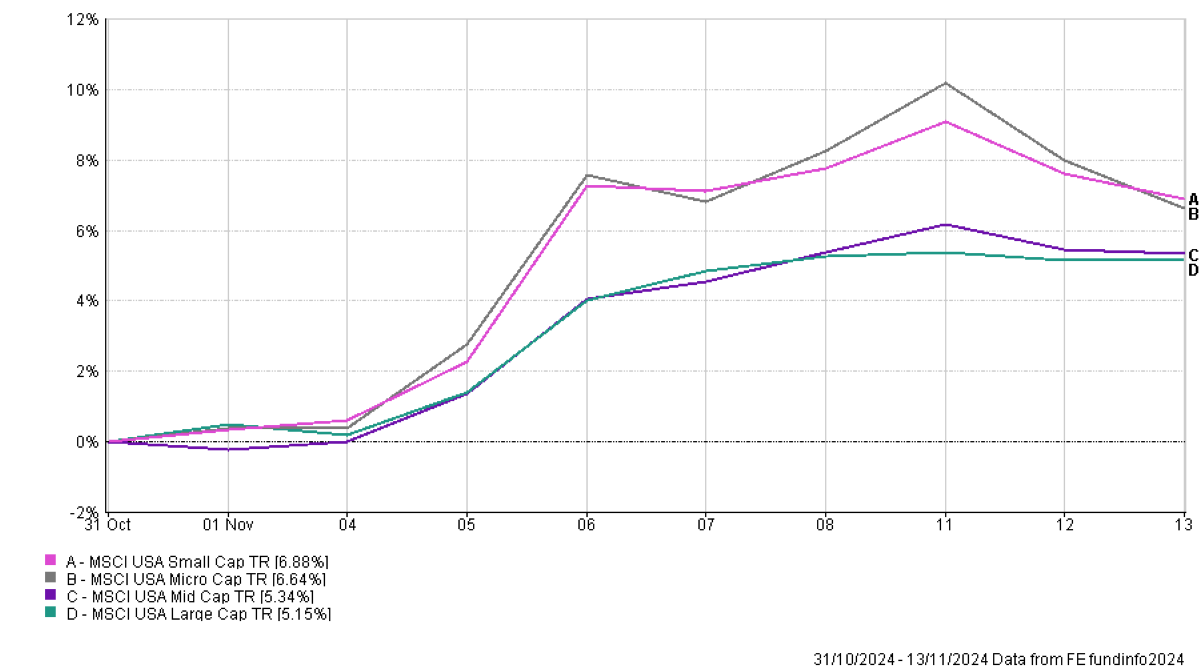

Figure 1 – US equity market returns split by market capitalization – Source: FE Analytics, 2024.

Figure 1 – US equity market returns split by market capitalization – Source: FE Analytics, 2024.

Once Trump’s election victory became clear to markets on the 6th of November there was a rapid surge in US equity prices. Smaller companies, which have lagged their larger counterparts over recent years, surged ahead of the wider market.

Small companies, at least conceptually, are set to benefit in multiple ways:

- Trump has consistently pushed for the Federal Reserve to lower interest rates and small companies are more dependent on borrowing, so more responsive to lower rates;

- Onshoring of manufacturing should benefit the companies most exposed to domestic US supply chains, as smaller companies are;

- Deregulation is likely to benefit smaller companies, as the costs of regulation are more easily borne by the largest companies and so create barriers to market entry for small firms.

Global Equity Market Trends

Casting our net a little wider into the global equity ponds we can get a feeling for how investors expect the Trump regime to impact the key trading partners of the US.

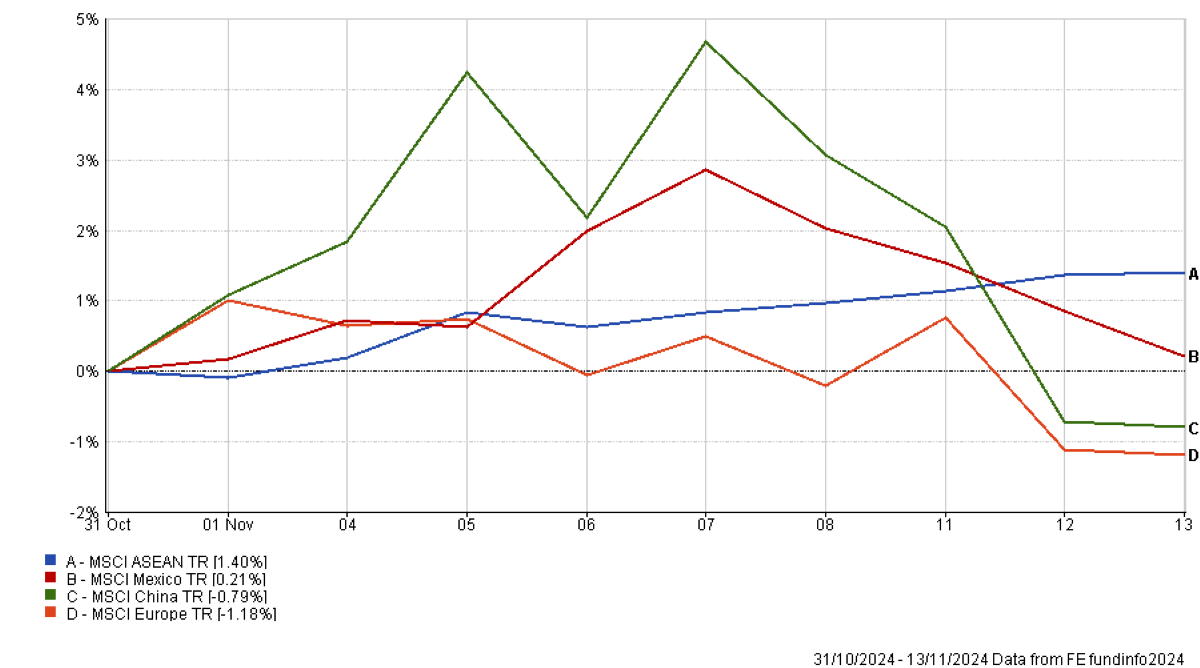

Figure 2 – Regional equity market returns for key US trade partners – Source: FE Analytics, 2024.

Figure 2 – Regional equity market returns for key US trade partners – Source: FE Analytics, 2024.

Starting with the clearest loser of the situation, Europe. With an increasingly domineering US to the west, growing China to the east and a deindustrialising Germany at the centre the EU is facing pressures last seen during the 2012 Euro crisis, although arguably more existential. Sentiment towards the European economy and equity market was weak to start with and Trump’s election has only reinforced this.

The reaction in Chinese equity markets has been more mixed, but ended in pessimism. On election day equities fell as the prospect of a full blown trade war rose, the day after election equities rose on the narrative of a ‘grand bargain’ between the US and China – a deal that only Trump “the dealmaker” could make unimpeded by the Democrat’s ideological red-lines over human rights and the Chinese system of government. This optimism soon petered out and Chinese equities fell from the 8th onwards.

Where the reaction has been far more positive is in countries that have been the biggest beneficiaries of the shift in trade patterns away from direct ‘China to US’ trade to indirect ‘China to intermediary country to US’ trade. The Association of South East Asian Nations (ASEAN) and Mexico have benefitted a great deal from this so far and markets expect this trend to continue.

Fixed Income Market Response

Finally, we’ll take a look at the response of the fixed income markets. Since September, when Trump’s victory probability began to rise, so did government bond yields as markets began to price in the potential inflationary impact of Trump’s policy mix, meaning that by election day much had already been priced in. Even so, there was a spike in the 10-year US government bond yield, a fall in yields from the 7th-11th and then a rise back to the election day levels – investors remain concerned with Trump’s inflationary impact.

Conclusion

So, where does that leave us in terms of portfolio allocations? While at first sight Trump’s tariff policy seems set to benefit US firms at the expense of non-US firms, the positive equity market response in Mexico and ASEAN show that it still pays to hold a portfolio that is diversified across multiple regions – in the event that one region is negatively impacted this can be balanced by positive impacts to other regions. Additionally, it has paid, and is likely to continue to pay, to diversify US equity allocations out from the largest companies in the S&P 500 – to that end our Managed portfolios maintain a direct allocation to mid and smaller sized US companies.

As the investment landscape becomes increasingly complex the benefits of a portfolio constructed by investment professionals and run by experienced managers increase – please contact your adviser to discuss how a risk appropriate portfolio can be constructed for you.

Arrange your free initial consultation

The information in this article is correct as at 15/11/2024.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

Autumn Budget 2024

In one of the longest ‘Budget’ speeches in memory, Chancellor Rachel Reeves gave the first Labour Budget speech for nearly 15 years on 30 October 2024.

Here we’ve summarised the main elements of interest for financial planning, with further details on tax rates and allowances for 2025/26 (to compare to 2024/25) available on the government website.

If you have any concerns or questions about any of the announcements and would like to speak to one of our expert financial advisers, contact us for a free initial consultation to see how we can help.

Arrange a free initial consultation

Non- domicile changes

The non-domicile tax regime is to be abolished from 6 April 2025. Domicile will no longer be a feature of the UK tax system and will be replaced by a system based on residency.

The government will:

- Introduce a new 4-year foreign income and gains regime for new arrivals who have not been UK tax resident in the previous 10 years

- Allow individuals previously taxed on the remittance basis to remit pre-6 April 2025 foreign income and gains using a new Temporary Repatriation Facility

- Reform Overseas Workday Relief

- Replace the domicile-based system for inheritance tax with a residence-based system

VAT on private school fees

From January 2025, 20% VAT will apply to private school fees across the UK and the business rates charitable rates relief for private schools in England will be removed.

Income tax and personal National Insurance (NI)

Income tax bands and personal NI thresholds remain frozen until April 2028. This time period hasn’t been extended and from 2028/29 these bands/thresholds will increase with inflation.

Capital gains tax (CGT) changes

Investors’ Relief

Investors’ Relief (IR) provides for a lower rate of CGT to be paid on the disposal of ordinary shares in an unlisted trading company where certain criteria are met, subject to a lifetime limit of £10 million of qualifying gains for an individual.

This measure reduces the lifetime limit from £10 million to £1 million for IR qualifying disposals made on or after 30 October 2024.

CGT rates

The main rates of Capital Gains Tax (that apply to assets other than residential property and carried interest), will increase from 10%/20% to 18%/24% respectively for disposals made on or after 30 October 2024.

The main rate of Capital Gains Tax that applies to trustees and personal representatives will increase from 20% to 24% for disposals made on or after 30 October 2024.

The rate of Capital Gains Tax that applies to Business Asset Disposal Relief and Investors’ Relief is increasing to 14% for disposals made on or after 6 April 2025 and from 14% to 18% for disposals made on or after 6 April 2026.

Carried interest

Carried interest, which is a form of performance-related reward received by fund managers, primarily within the private equity industry, will be subject to a CGT rate of 32% from April 2025 (current rates are 18% and 28%). From April 2026, carried interest will be subject to a revised regime within the income tax framework.

Inheritance tax (IHT) changes

Freezing of IHT thresholds

The Inheritance Tax thresholds were already fixed at their current levels until April 2028. This time period has been extended to April 2030. This measure will fix the:

- Nil-rate band at £325,000

- Residence nil-rate band at £175,000

- Residence nil-rate band taper, starting at £2 million

Inherited pensions

From 6 April 2027, when a pension scheme member dies with unused funds or without having accessed all of their pension entitlements, those unused funds and death benefits will be treated as being part of that person’s estate and may be liable to Inheritance Tax. The current distinction in treatment between discretionary and non-discretionary schemes will be removed.

The change will apply to both DC and DB schemes. It will apply equally to UK registered schemes and QNUPS. This will ensure that most pension benefits are treated consistently for Inheritance Tax purposes, regardless of whether the scheme is discretionary or non-discretionary, DC or DB.

A small number of specified pension benefits will remain outside scope for Inheritance Tax, including where funds can only be used to provide a dependants’ scheme pension. These are currently out of scope in non-discretionary schemes and so will remain out of scope under this change.

Pension scheme administrators will become liable for reporting and paying any Inheritance Tax due on pensions to HMRC. This will require pension scheme administrators and personal representatives to share information with one another.

A technical consultation has been issued on the processes required to implement these changes for UK-registered pension schemes. After the consultation, the government will publish a response document and carry out a technical consultation on draft legislation for these changes in 2025.

The government will continue to incentivise pension savings for their intended purpose of funding retirement, supported by ongoing tax reliefs on both contributions into pensions and on the growth of funds held within a pension scheme.

Agricultural relief and business relief

From 6 April 2025, the existing scope of agricultural relief will be extended to include land managed under an environmental agreement with, or on behalf of, the UK government, devolved governments, public bodies, local authorities, or relevant approved responsible bodies.

From 6 April 2026, agricultural relief (AR) and business relief (BR) will be reformed, as summarised below:

- The 100% rate of relief will continue for the first £1 million of combined agricultural and business property to help protect family farms and businesses, and it will be 50% thereafter.

- The rate of business relief will reduce from 100% to 50% in all circumstances for shares designated as “not listed” on the markets of recognised stock exchanges, such as AIM.

The reforms are expected to only affect around 2,000 estates each year from 2026/27, with around 500 of these claiming agricultural relief and around 1,000 of these holding shares designated as “not listed” on the markets of recognised stock exchanges.

The government will publish a technical consultation in early 2025. This will focus on the detailed application of the allowance to lifetime transfers into trusts and charges on trust property. This will inform the legislation to be included in a future Finance Bill.

More detail is available at gov.uk.

National insurance

Employer NI is to increase to 15% (from 13.8%) from April 2025 and the secondary threshold will reduce to £5,000 (from the current £9,100), i.e. employer NI will become payable on an employee’s earnings above £5,000pa.

The Employment Allowance, a National Insurance exemption for smaller businesses, will increase to £10,500 (from £5,000).

Pensions

Qualifying recognised overseas pension scheme (QROPS)

The Overseas Transfer Charge (OTC) is a 25% tax charge on transfers to QROPS, unless an exclusion from the charge applies.

The government has announced that they are removing the exclusion from the OTC for transfers made on or after 30 October 2024 to QROPS established in the EEA and Gibraltar.

Also, from 6 April 2025, the conditions of OPS and ROPS established in the EEA will be brought in line with OPS and ROPS established in the rest of the world, so that:

- OPS established in the EEA will be required to be regulated by a regulator of pension schemes in that country

- ROPS established in the EEA must be established in a country or territory with which the UK has a double taxation agreement providing for the exchange of information, or a Tax Information Exchange Agreement

From 6 April 2026, scheme administrators of registered pension schemes must be UK resident.

Aligning the treatment of transfers to QROPS established in the EEA and Gibraltar with that of transfers to QROPS established in the rest of the world will help to ensure that some UK residents do not benefit from a double tax-free allowance whilst remaining in the UK and reduces the risk of around £1 billion of UK tax-relieved pension savings being transferred overseas across the scorecard.

Changing the conditions EEA schemes need to meet in order to become an OPS or ROPS will mean that they will have to meet the same conditions as those which are established anywhere else in the world.

Requiring scheme administrators of registered pension schemes to be UK resident will mean that all administrators of registered schemes will need to meet the same conditions.

Further details are available at gov.uk.

Employee Ownership Trusts and Employee Benefit Trusts

Targeted reforms are to be made to the Employee Ownership Trust tax reliefs to ensure that the reliefs remain focused on the intended purpose of encouraging and supporting employee ownership, whilst preventing opportunities for the reliefs to be abused to obtain tax advantages outside of these intended purposes.

Details are available at gov.uk

Stamp Duty Land Tax (SDLT)

The higher rates of Stamp Duty Land Tax (SDLT) for purchases of additional dwellings (second properties) and for purchases by companies is increasing from 3% to 5% above the standard residential rates of SDLT.

This measure also increases the single rate of SDLT payable by companies and other non-natural persons purchasing dwellings over £500,000, from 15% to 17%.

Both changes apply to transactions with an effective date on or after 31 October 2024.

National Minimum Wage

The National Living Wage will increase from £11.44 to £12.21 an hour from April 2025. The National Minimum Wage for 18 to 20-year-olds will also rise from £8.60 to £10.00 an hour.

State benefit and state pension increases

From April 2025, a 4.1% increase to the basic and new State Pension meaning the full new State Pension will rise from £221.20 to £230.25 a week, while the full basic State Pension will increase from £169.50 to £176.45 per week.

The Pension Credit Standard Minimum Guarantee will increase by 4.1% from April 2025, meaning an annual increase of £465 in 2025/26 in the single pensioner guarantee and £710 in the couple guarantee.

Working-age state benefits and the Additional State Pension will rise by 1.7% in April 2025, in line with inflation.

Furnished holiday lettings (FHL)

As previously announced, the furnished holiday lettings (FHL) tax regime will be abolished from April 2025, removing the tax advantages that landlords who offer short-term holiday lets have over those who provide standard residential properties.

The current rules provide beneficial tax treatment for furnished holiday lettings compared to other property businesses in broadly four key areas:

- Exemption from finance cost restriction rules (which restrict loan interest to the basic rate of Income Tax for other landlords)

- More beneficial capital allowances rules

- Access to reliefs from taxes on chargeable gains for trading business assets

- Inclusion as relevant UK earnings when calculating maximum pension relief

The abolition of the FHL regime will mean that income and gains will then:

- Form part of the person’s UK or overseas property business

- Be treated in line with all other property income and gains

If you’d like to discuss any of the changes announced in the Autumn Budget or would simply like to explore ways that you can minimise the amount of tax you pay on your wealth, why not get in touch and speak to one of our expert team of advisers. We’re offering anyone with £100,000 in savings, investments or pensions a free financial review worth £500.

Arrange a free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning or tax.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Labour’s first Budget in 14 years - What's the impact?

Nearly 4 months after the general election, Chancellor Rachel Reeves finally delivered her eagerly anticipated Budget this afternoon.

It had been widely reported that there would be tax rises and speculation had been rife that pensions, capital gains tax and inheritance tax could be targeted to raise tax revenue following Labour’s manifesto commitment not to increase taxes on “working people”.

In the end, changes to all three of these areas were announced as Reeves looks to raise taxes by £40bn, though the changes were not to the extent that many had feared.

Arrange your free initial consultation

Capital Gains Tax

The main rate of Capital Gains Tax will increase for basic rate tax payers from 10% to 18% and for higher rate tax payers from 20% to 24%. This change will take effect immediately. Capital Gains Tax on second properties will remain unchanged.

There had been rumours that capital gains tax rates would be equalised with income tax rates, so the changes could be viewed as relatively modest compared to potential increases of this level.

Pensions

Investors will have been pleased to see that no changes were announced to the maximum tax free cash that can be taken from pensions or the tax relief available on pension contributions. However, it was announced that unused pension funds and death benefits payable from a pension will be included in the value of estates for inheritance tax purposes from 6 April 2027. This will affect individuals who were previously planning to leave their pensions to beneficiaries rather than to spend them in their lifetimes, though income taken from pensions in excess of tax free cash entitlements is subject to income tax and will then form part of the estate for inheritance tax purposes if not spent, so careful planning will be needed to ensure funds are not taxed twice.

Inheritance Tax

Aside from inherited pensions entering the estate for inheritance tax purposes in 2027, there were a couple of additional changes to inheritance tax rules.

Firstly, the freezing of the nil rate band (£325,000) and Residence Nil Rate Band (£175,000) until 2030 was announced. For reference, the Residence Nil Rate Band is generally available when a main residence is passed to direct descendants and this, combined with the nil rate band, generally gives married couples £1m which can be passed to direct descendants inheritance tax free on the second death of them both.

Additionally, there had been rumours that the inheritance tax break on shares listed on the Alternative Investment Market (AIM), if held for two years before death, would be scrapped. However, the Chancellor instead took a ‘half way’ approach by introducing a 20% inheritance tax rate in respect of these shares.

The Chancellor also announced changes to two lesser-known inheritance tax reliefs, Business Relief and Agricultural Relief, which will now be subject to a 20% inheritance tax charge on qualifying asset values over £1 million.

Income Tax, Employee’s National Insurance and VAT

As expected there were no increases in these three areas given they affect “working people”. However, with income tax bandings already frozen until 2028, there was an expectation the Chancellor may extend this date, but this did not prove to be the case, as the Chancellor confirmed the freezing of these bandings would end in 2028.

Given the above changes were not to the level expected, how has the Chancellor raised £40bn?

Employer’s National Insurance

A large proportion of this £40bn (an estimated £25bn) will be funded by a large increase in employer’s National Insurance contributions from 13.8% to 15% and a reduction in the threshold from which these are paid from £9,100 to £5,000.

Stamp Duty on second properties

Landlords will be disappointed to see the stamp duty surcharge on second properties increasing from 3% to 5% with effect from 31 October.

Non-Dom tax status abolished

As expected, the Chancellor confirmed Labour’s plans to abolish “non-dom” tax status.

Overall, after weeks of speculation, the tax rises announced in the budget were not to the extent that many had feared. Individuals with pensions will be relieved to see no reduction in their maximum tax free cash entitlement and no change to the tax relief they can receive on pension contributions. Investors may also feel increases in capital gains tax rates could have been worse. Instead, businesses were left to fund the majority of the tax rises through their National Insurance contributions.

However, these changes to inheritance tax, pensions and capital gains tax rules will mean financial plans will need to be revisited. To discuss the implications of the budget for your personal financial situation, please contact your TPO Independent Financial Adviser.

Arrange your free initial consultation

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

This article is intended as information only and does not constitute financial advice.

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Federal Reserve and Chinese central bank – unusual bed fellows or fiscal allies?

In our last Investment Market Update we covered the recovery in markets following early August’s volatility and the beginning of a slowdown in US technology equities.

Since then, policymakers from both sides of the Pacific have provided stimulus measures to markets, with the US starting their interest rate cutting cycle with a bang, delivering two rate cuts in one meeting, followed by the announcement by Chinese authorities of new fiscal and monetary stimulus measures.

In this month’s update we will take a closer look at Chinese stimulus, it’s expected economic effectiveness and ongoing market impacts, along with the impact of these initial US rate cuts on markets.

Arrange your free initial consultation

US Rate Cuts

The US Federal Reserve (Fed) chose to cut rates by 0.5% at their September 18th meeting. Interest rate rates are typically changed by 0.25% at a time, so this ‘double cut’ was a surprise to some investors. Fed Chairman Jerome Powell cited falling inflation, as well as emphasising initial signs of weakness in job markets that he would like to get ahead of with pre-emptive interest rate cuts.

Markets at this point were expecting a further weakening in jobs figures and anticipated two more ‘double cuts’ at the November and December Fed meetings. In equity markets investors crowded back into the ‘Magnificent 7’ technology stocks, with these 7 accounting for 55.2% of S&P 500 returns in September, owing to their high-quality business models and perceived resilience to potentially slowing economic conditions.

In early October, just as markets were reflecting upon the direction of economic travel, the very same labour market data investors were so vigilantly watching showed a pickup in job creation, pushing unemployment down and wage gains up. Markets turned, with only a 0.25% rate cut now expected in November versus 0.5% previously, and government bond yields moving upwards in unison. Within equity markets there was a renewed rally in cyclical industries like industrials and financials.

Where to from here? Markets have begun to increase their probabilities of market volatility following the presidential election on November 5th, with the Federal Reserve meeting the following day to choose interest rate policy (0.25% cut expected). All eyes will be on the results of the election and Fed policy.

Fed rate cuts have also been supportive of asset markets globally, in particular with increased dollar liquidity spilling into emerging markets, allowing Chinese authorities to bring forward stimulus measures without putting undue depreciation pressure on the Yuan.

Chinese Stimulus

That brings us to the other main story in markets: Chinese stimulus. As mentioned, China had been waiting for the US monetary policy easing to provide large stimulus measures, with the People’s Bank of China (PBOC) Governor Pan Gongsheng previously emphasising currency stability in messages over the summer. With that US roadblock out of the way, China has announced their first large round of fiscal and monetary supports, summarised as follows:

1. Monetary Policy

a. Cut in central bank base rates by 0.2%.

b. Cut in commercial bank reserve requirements, releasing $160bn in new credit.

2. Property Market Policy

a. Cut in mortgage rate by 0.5%.

b. Cut in down-payment requirement.

3. Stock Market Support

a. $80bn central bank borrowing facility for brokers, dealers and funds to fund stock purchases.

b. $50bn central bank borrowing facility for companies to fund share repurchases.

4. Household Consumption Support

a. Continued funding for household goods & automotive trade-in schemes (cash-for-clunkers).

b. Initial pilots of cash-handouts to the deeply impoverished.

So, what’s the assessment of all this? Given the total value of support is around 1.6% of GDP this stimulus is substantial, but not as significant as the huge 30% of GDP credit stimulus seen in the post-financial crisis 2008-9 period.

Points 1 and 2 are unlikely to move the needle, having been tried last year to little effect – the demand for credit, both by households for property and businesses for capacity expansion, is fairly subdued, so falling interest rates may have little impact on credit growth.

Point 3, on the other hand, is already having an impact. This has increased investor confidence in Chinese domiciled assets and those assets that are most correlated with rising wealth and economic activity in China; Chinese equities have skyrocketed, gaining 25% in two weeks, while commodities and emerging market equities have rallied. The “ripple effect” has seen the Asia-focused UK bank Standard Chartered rally by over 9% and European luxury goods group LVMH rise over 8%. It should be noted that these improvements in market liquidity and investor confidence lay relatively brittle foundations for this rally that will need stiffening with improvements in corporate and economic fundamentals.

Point 4, while a good start, is just too small to effectively redress the structural imbalance at the heart of China’s economy – of weak domestic consumer demand, owing to a low household share of national income, and the subsequent need for high rates of questionable Government funded property & infrastructure investment to prop-up otherwise weak demand in the economy. Further announcements are scheduled in the coming weeks of additional fiscal measures, expected to be targeted at households, which hopefully will start to enact rebalancing. Unfortunately, without a comprehensive set of such reforms, rallies in China’s equity market are unlikely to turn into long-term positive trends, as businesses continue to deal with the pressures of a deflationary economy.

Conclusion

In summary, asset markets have been supported by increasingly supportive policy in both China and the US, with China enacting wide ranging, but fairly shallow, stimulus and the US Fed starting their interest rate cutting cycle with a bang.

Markets have been buoyed by this increase in liquidity and investor confidence, however questions remain over the effectiveness of Chinese stimulus and the medium-term health of the American labour market. In the shorter term, politics is likely to be a driver of market volatility. Investors are therefore advised to allocate to diversified portfolios and maintain their nerve through short-term rough patches in the pursuit of long-term returns.

Please contact your advisor if you have any questions.

Arrange your free initial consultation

The information in this article is correct as at 11/10/2024.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

Market Horizon: Smooth Sailing or Rough Waters?

In last month’s TPO Investment Market Update we spoke about the market volatility seen in early August, caused by a sharp decrease in risk taking due to the combination of:

-

An abrupt change to Japanese monetary policy,

-

The release of weak US labour market data, and

-

Concerns over the ability of large tech firms to turn AI investments into bottom-line profits.

Arrange your free initial consultation

Since then, global equity markets have broadly recovered, although worries remain over both the health of the US labour market going forward and the ability of the largest technology companies to deliver on the promised profits of their AI investments. These worries have resulted in a minor selloff of tech stocks at the start of September, flattening global equity returns.

For September’s investment market update we will take a closer look at the recovery in markets and the previously mentioned factors causing ongoing concern amongst investors.

Market Recovery

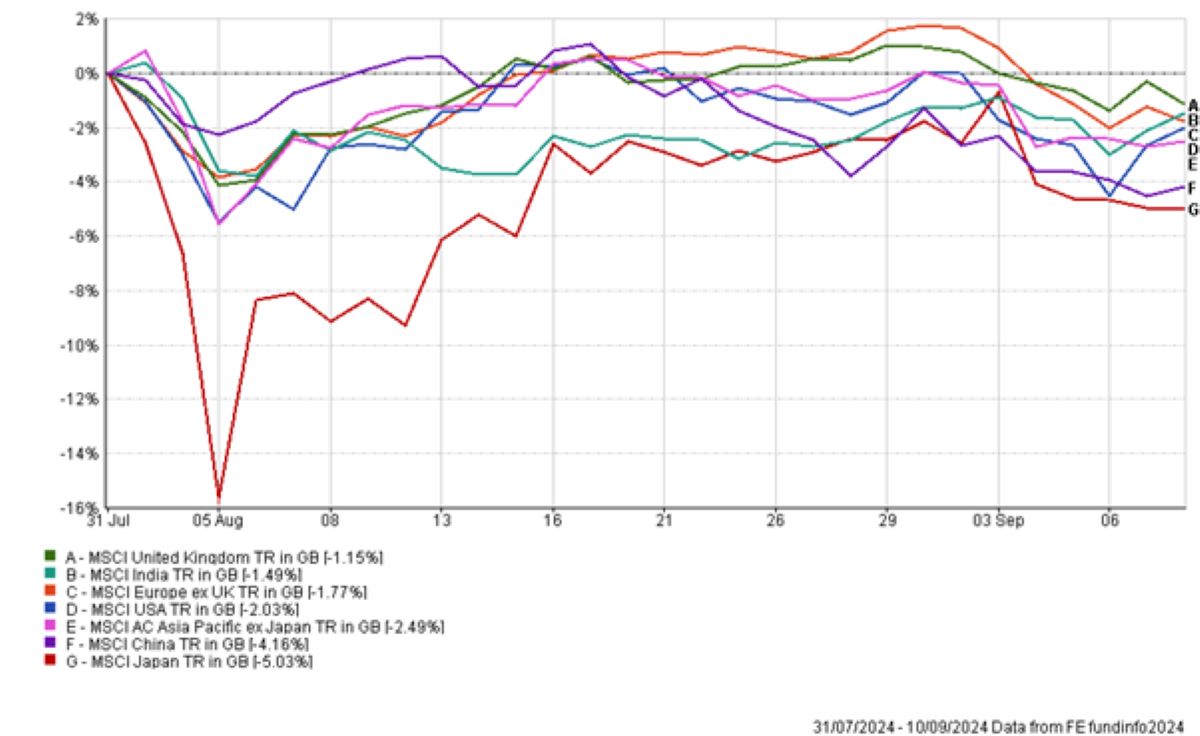

Figure 1 – Returns of major regional equity indices from August to early September – Source: FE Analytics, 2024.

Figure 1 – Returns of major regional equity indices from August to early September – Source: FE Analytics, 2024.

Figure 1 shows the returns of major regional equity markets to a sterling denominated investor from August through to early September. The major bout of volatility, hitting Japanese equities the hardest, can be seen in the first week of August – for an explanation of the factors causing this please read last month’s market update, available here. Markets recovered through August, as investors came to the conclusion that the moves in early August were an overreaction. Market volatility reduced and the hardest hit regional markets and sectors/industries saw the swiftest recovery. This meant a strong rebound in Japanese equities and large technology companies.

The beginning of another, hopefully smaller, selloff

What we also see in Figure 1 is the beginnings of another selloff in equity markets at the start of September. While this has not been nearly as violent as the August selloff, it has nonetheless pulled many regional indices down close to their levels seen in August. The background causes remain similar to last time, excluding the Japanese monetary policy factor – primarily concerns over a weakening US labour market and the high stock prices of US tech firms relative to the profits they are currently delivering from their AI investments.

So, what are the US labour market concerns? These concerns stem from slowing job creation and a rising unemployment rate. The most recent market-moving data releases were the reports on job openings and new job creation, both of which are down significantly versus a year ago, or even a few months ago. Whilst neither measure is at the level indicating a recession, the direction of travel indicates a slowing economy. You can be fairly sure a recession is signposted when total employment declines outright from month-to-month. The most recent data showed 142,000 jobs added in August 2024, so no recession, but down significantly from the 210,000 jobs added in August of 2023 and below the roughly 200,000 jobs needed to keep up with population growth.

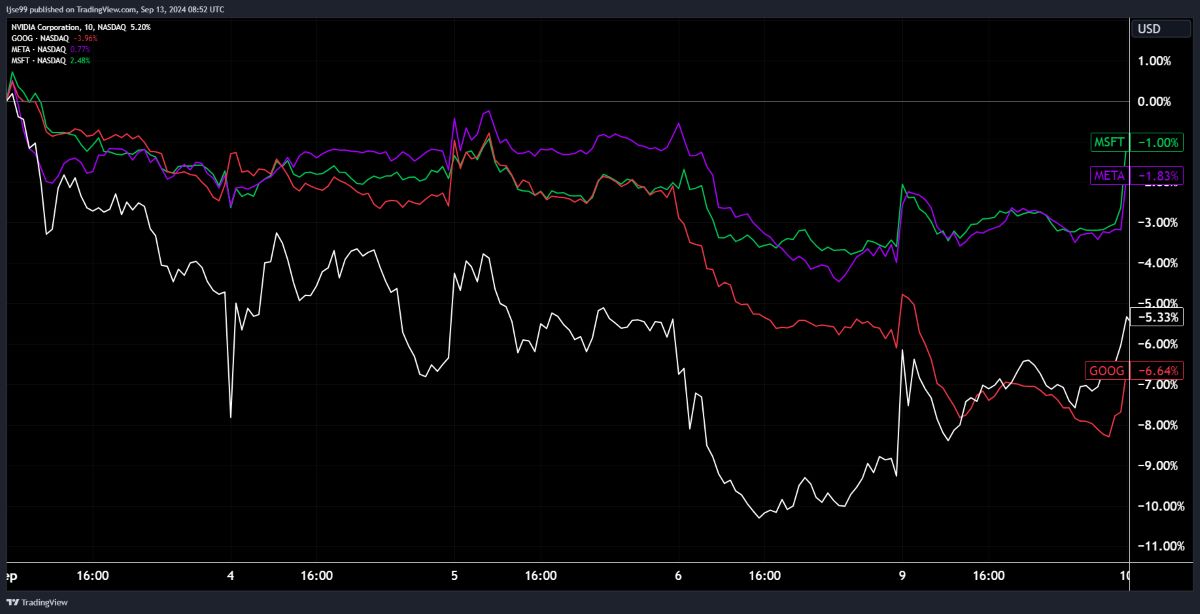

Figure 2 shows the returns of the most prominent AI-related technology companies in early September. Nvidia, the most linked to AI, fell as much as 11% by 06/09/24 but has since recovered around 6% of that drop. Similarly, Google (Alphabet) is down over 7% so far this month.

But what has caused this selloff? Outside of the general risk-averse sentiment caused by weakening labour market data, investors are becoming increasingly sceptical of tech firms ability to turn their large AI investments into near-term profits. Whilst AI models like ChatGPT have wowed us with their innovation, they have not yet found sufficient commercial uses to generate revenues that cover the costs of building out vast data centres and research teams. Despite this, tech firms steam ahead, with Mark Zuckerberg commenting in a recent interview that they must continue to invest heavily in AI for fear of falling behind others and becoming ‘irrelevant’ in years to come.

This sentiment came to a head upon the release on Nvidia’s most recent quarterly earnings report, along with the forward guidance for the next quarter that comes with it. While Nvidia recorded substantial revenue growth from the first to the second quarter, growing in one quarter what the average company would be envious of growing in a whole year, their forward guidance pointed to slowing revenue growth in coming quarters. They cited issues with the production of their next generation Blackwell chips. While revenues are expected to continue growing, the expectation of just a slowing of that rate of growth rattled markets because of the very steep growth assumption baked into Nvidia’s high share price. Markets have reacted to this and applied the sentiment to other AI-related stocks, along with research suggesting Microsoft may only be bringing in profits in the single digit billions from their ownership of OpenAI (the creator of ChatGPT), a drop in the bucket for a firm generating profits of $72bn in 2023. AI-related stocks have therefore seen the price declines shown in Figure 2.

What next?

Given the importance that markets have recently attached to US labour market data, the next month’s figures will be pivotal to market narratives, meaning another month of weak job growth will confirm a slowdown and could lead to further equity market volatility. Conversely, more positive figures should push investors back to the ‘soft landing’ camp.

Additionally, politics will continue to be an important factor. Kier Starmer’s first Budget will be unveiled on October 30th and the US election will take place 6 days later on November 5th. While the former is unlikely to surprise capital markets – save for some speculation about removal of the inheritance tax breaks given to investors in the London AIM equity market – there is far more uncertainty surrounding the latter, with neither US presidential candidate having fully fleshed out their economic policies, leaving a wide range of policy uncertainty for investors to navigate.

Given the potential for political uncertainty and volatility ahead, we recommend a portfolio that is spread across regions, as well keeping a patient approach to remain invested through volatile periods.

If you have any questions about navigating such an environment, please don’t hesitate to contact your adviser.

Arrange your free initial consultation

The information in this article is correct as at 12/09/2024.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.