Skip to main content

Skip to main content

Tax return deadline looms - avoid a fine!

Were you one of the 4,757 people that filed their tax return on Christmas Day? Or the 12,136 that filed on Boxing Day? It may seem extreme to be doing your tax return over the festive period, but for those diligent people the chore is done for another year – and they have avoided the stress of leaving it too late and risking an automatic penalty of £100. In the 2020/21 tax year around 290,000 were fined.

And it’s not just late filing that can see you paying a penalty. You also have to pay the tax due! In that same tax year a further 1.43 million people were fined for not paying up on time, up from 1.24 million the year before. And that was despite the fact that HMRC waived the late filing and late payment penalties by one month that year, in recognition of the pressures caused by the Covid-19 pandemic.

HMRC has announced that it will only be dealing with priority calls in the lead up to the end of the month, as according to The Times, waiting times to speak to someone for assistance have soared from 5 minutes in 2017 to 20 minutes in 2022.

Who has to send in a tax return

Apparently more than 1 million people will have been drawn into self-assessment for the first time due to the increase in taxes due on everything from savings and dividends to capital gains, because of the freeze in many allowances that was introduced in 2021 and it set to continue until 2028.

And some people could be first timers if the increase to their income, including the State Pension, pushes their income over £100,000.* But there could be other situations too, so, you might be surprised to find that you do need to file a self-assessment tax return.

As there are so many more who may need to do a self-assessment tax return, it could be wise to check if you need to send a tax return if you’re not sure.

According to the gov.uk website, you must send a tax return if, in the last tax year (6 April to 5 April), any of the following applied:

- you were self-employed as a ‘sole trader’ and earned more than £1,000 (before taking off anything you can claim tax relief on)

- you were a partner in a business partnership

- you had a total taxable income of more than £100,000

- you had to pay the High Income Child Benefit Charge

You may also need to send a tax return if you have any untaxed income, such as:

- some COVID-19 grant or support payments

- money from renting out a property

- tips and commission

- income from savings, investments and dividends

- foreign income

What do you need if you have to file a tax return?

If you are filing online you’ll need to have a login to the Government Gateway and you’ll need your Unique Taxpayer Reference (UTR) number.

More information is available on gov.uk, so this is a great reference point especially if you don’t yet have a Government Gateway account. But you really need to get a move on if you want to avoid a penalty.

Remember that HMRC will charge interest on these fines and any unpaid tax and the amount is calculated as base rate plus 2.5% - so currently this is 7.75%. This is bad enough, but if HMRC owes you money because you have overpaid tax, they will only apply base rate minus 1% (4.25%), known as the repayment interest rate! Even more of a reason to make sure you pay up on time and accurately.

*Source: gov.uk

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Reasons for Investors to expect the unexpected

Investing is inherently risky and will always contain uncertainties. However, by taking risk, investors have a greater potential for higher returns, although this also presents the potential for losses. Nobody can predict the future or factor in every possibility to their plans, but careful portfolio construction can help to limit losses. As we continue to live through uncertain times, with raging wars, potentially changing political environment and the effects of an unprecedented pandemic still being felt, it’s little surprise that investors are feeling nervous. Here we look to outline some key sources of uncertainty and talk through the way The Private Office can help clients to mitigate the effects.

Arrange your free initial consultation

1. What are the sources of uncertainty for investors?

Market Volatility

Volatility is an inherent component of financial markets and reflects the ability to rise and fall suddenly in a very short space of time, due to diversity of sentiment and analysis among investors. Some times sentiment swings wildly one way or another, driving volatility. Equally, external events like elections, natural disaster and geopolitical conflicts can cause markets to react in a swift and violent manner. Recent examples include the Russia-Ukraine war and the Covid pandemic. Investors who, in a state of panic, sold when markets dropped missed the subsequent recovery in asset values. A long-term perspective, therefore, is key to avoid unnecessary losses and to ride out the short-term volatility.

Technological Disruption

Changes to technology is a constant through human existence, although it happens in fits and starts. As such, investors can be caught off guard by rapid changes in technology and the impacts on old industries. Not many foresaw how much Amazon would impact retail or how Netflix would impact media distribution. Looking for technological trends can help investors avoid being left behind.

Regulatory Changes

Changes to laws, regulations and government policies can have large impacts on investors and their portfolios. It is, of course, very difficult to predict changes in regulation, but you may choose investments that have a lower regulatory risk level – for example investments in firms that are aiming to reduce environmental impact reduces the risk that they fall foul of future environmental regulation and consequently suffer fines.

Geopolitical Shocks

Markets often undergo significant turbulence during times of acute uncertainty, and geopolitical shocks often raise the spectre of great uncertainty due to the wide degree of possible outcomes, ranging from swiftly negotiated peace all the way through to world war. As such, conflicts increase the price of risk to market participants, thus causing asset prices to decline in the immediate term. This is to say nothing of the impact on supply chains of ongoing wars – the Russia-Ukraine conflict being a good example, with the outbreak of the war causing a spike in energy and grain prices. Geographical diversification is a key to help minimising this risk.

Business Scandals & Contagions

Business scandals, often involving fraudulent accounting and business practices, understandably have serious impacts on the asset values of the involved companies, however investors often tar entire industries with the same brush, causing sector wide selloffs. Enron’s 2001 collapse is a good example, as it resulted in a period of heightened volatility across the energy sector. Avoiding concentrated positions can minimise this risk.

Economic Shocks

Economic data that is wildly out of the consensus expectations often causes sharp moves in financial markets, as investors incorporate this new data into their outlook on the world and thus their asset allocation frameworks. A recent example of this is the flare up in inflation in 2022 and the subsequent interest rate hikes by central banks. Rising costs of financing causes investors to reappraise the fundamentals of many of the companies they invested in and to change investment strategies. Keeping an open mind and assessing a wide variety of outcomes can help partially mitigate this risk.

Black Swan Events

Black Swan events get their name from the Victorian belief that a black swan did not exist, only for explorers to find them living in Australia. As such, events that are incredibly unlikely, but impactful, are called Black Swan events. The outbreak of the Covid pandemic is an example of a Black Swan event. By definition, these events catch investors off guard. Only by creating robust risk-modes and stress testing portfolios can you then help limit the impact of these events.

Overconfidence & Biases

Humans are prone to biases when making decisions: loss aversion, overconfidence and confirmation bias can hurt investors and lead to bad decisions. Remaining disciplined and working with an adviser to understand your own biases can reduce the risk of making poor investment decisions.

Complacency & Herding

Another very common mistake among investors, particularly the inexperienced, is to follow the crowd. “How can this be a bad investment if everyone else is buying?”. As everyone rushes out, it can result in spectacular losses in a short period of time – the late 90s tech bubble crash is a good example. This behaviour can be common in social situations but can be financially damaging as a result of losses when the tide turns. Once again, diversification is a way to help avoid these outcomes.

2. How to deal with uncertainty

Diversification

Diversifying your portfolio across asset classes, geography and sectors is key. Concentrated positions increase investment risk from all those mentioned above, market volatility, regulatory changes, technological disruption and business scandals. By allocating between multiple countries, you help avoid the risks that geopolitical events in one country bring your whole portfolio down. Creating portfolios with equities, fixed income and alternatives lowers correlated risks due to economic shocks and black swan events. Correlated risks are risks that are correlated to each other, for example inflation and interest rate risk are correlated (when inflation rises, often interest rates do too) so if your equity holdings are susceptible to pressures on margins from inflation, as well as suffering from a high debt load that is impacted by interest rate rises, you are exposed to two correlated risks.

Time in the market (not timing the market) is key

A long-term investment mindset stops investors from panic selling at the bottom and herding into the same assets as everyone else. Through history, equity markets have consistently risen over the decades even if they have fallen over short periods. Timing the markets can be a fool’s game with only 18% of hedge fund managers getting it correct the majority of the time.

How we can help

At The Private Office, our investment philosophy is to create long-term, diversified portfolios that benefit from the structural trends shaping society, while mitigating risk through a diversified allocation across geographies and asset classes. We aim to reduce risk by avoiding keeping all eggs in one basket whether those 'eggs' are countries (geography) or types of investment (bonds, stocks, alternatives). Our advisers compliment this with advice that keeps clients-long-term interests in mind with their own tailored investment strategy, to help avoid rash decisions that can harm your financial outcomes.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Investment returns are not guaranteed, and you may get back less than you originally invested.

Past performance is not a guide to future returns.

How to make your child a millionaire before 40!

Most parents would like to ensure their children have a strong financial footing when they are older, but don’t always know the best way to do this. There are many ways to support your children financially throughout their lifetime, but what if there was a way to make them a millionaire before they even reached retirement age? Here we look at the best ways to put money aside for your children and how you can maximise the benefits of compound interest to make your child a “millionaire”!

Arrange your free initial consultation

The first step to saving for your children’s future is understanding your saving options. Here are the most common options that benefit from tax-free growth:

Junior ISA(JISA)

From the day a child is born you can put money into a JISA for them. The current contribution limit is £9,000 per tax year (or £750 per month) and you have the choice of a Junior Investment ISA or a Junior Cash ISA. The most important benefit of a JISA is that any gains made, or interest earned will be tax-free!

If we assume you receive an average annual net return of 5% per year and you save the maximum of £9,000 every tax year, from the day your child is born until they turn 18, you will have contributed a total of £162,000 to their account. However, due to the magic of compound interest (where you earn interest on interest), they will have a pot of over £265,000 saved in a tax-efficient wrapper, what a great 18th birthday present!

At their 18th birthday they can transfer their JISA into an Adult ISA to continue to receive tax-free interest/ investment returns.

Junior Self-Invested Personal Pension (Junior SIPP)

Setting up a pension up for your children may seem like you are overly preparing but this can actually give your children a significant head start. The maximum you can currently save into a Junior SIPP is £2,880 per tax year, and the UK government will add tax 20% tax relief of £720 per tax year, which would bring the total contribution to £3,600. If you can contribute to your child’s Junior SIPP for 18 years and again assuming a 5% growth rate, you will have contributed £51,840 but their pension pot will be worth £106,340 due to the added tax relief. If your child doesn’t contribute to the pension again, by age 57* they could have a pension pot worth around £712,986. Similar to the JISA, any gains made within the SIPP are exempt from tax, and based on current pension rules, you can take up to 25% as a tax-free lump sum upon reaching retirement age.

Recent statistics released by the Office for National Statistics (ONS) stated how the average pension wealth for all persons in the UK is £67,800 at age 57*, highlighting how starting to save early can set your child up for their future and give them a greater opportunity in retirement or even to retire early.

How to make your child a millionaire!

And this is how to do it! If you do the following and assume a 5% growth rate per annum:

- Open a JISA before your child’s first birthday and contribute £9,000 every year until age 18. This results in a total contribution of £162,000 (18 years x £9,000).

- Open a Junior SIPP before your child’s first birthday and contribute £3,600 (including tax relief) to the Junior SIPP every year up to their 18th birthday. This totals 18 years x £2,880 (or £3,600 with tax relief) which equals £51,840 (£64,800)

This would mean you will have contributed a total of £226,800 (including tax relief) to the JISA (£162,000), and Junior SIPP (£64,800). At age 18 when you stop contributing, they could have a total net worth of £372,191 when taking into account compound interest and growth. If they leave this money invested and continue to achieve 5% per year growth, by age 39 they could have a total net worth of just over £1million (£1,036,911), although the funds in the pension would not be accessible until age 57*.

At that point the pension fund could have grown to £712,986, while the ISA, could be worth £1,782,465 if it remained untouched too - an extraordinary total of almost £2.5m. That is a gift worth giving.

The power of starting to save early

Using the same assumptions as above, with a 5% annual growth rate and maximising both Junior SIPP and JISA contributions until age 18:

| Starting from date of birth | Starting at age 5 | Starting at age 10 | |

|---|---|---|---|

| JISA Value at age 30 | £477,430 | £300,604 | £162,056 |

| Junior SIPP value at age 30 | £190,972 | £120,242 | £64,823 |

| Total Value at age 30 | £668,402 | £420,846 | £226,879 |

This shows the benefits you can provide by starting the process of saving early for your child through compounding the interest or investment returns. This is a representation of how you can save for your children and assumes maximum contributions are made at each birthday, but we understand the circumstances for each parent and child will be different and may require different forms of financial planning, such as monthly contributions instead of lump sums.

Despite the examples above, it is never too late to start. If you would like to understand how, The Private Office can structure savings and investments for you and your children to help provide the whole family with a strong financial future. So why not get in touch for a free initial consultation.

* Based on current pension regulation, where the normal minimum pension age is increasing to age 57 from April 2028.

If you would like to know more about this topic, one of our Partners Kirsty Stone appeared on BBC Radio 4 Money Box live, giving her suggestions in a programme all about saving for children.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

All the calculations in this article assume that lump sum contributions are made for 18 years, from birth, unless otherwise stated, to the 17th birthday and are not adjusted for inflation.

The Financial Conduct Authority (FCA) does not regulate tax or cash advice.

The growth rates provided are for illustrative purposes only. Investment returns can fall as well as rise and are not guaranteed. You may get back less than you originally invested. Investments may be subject to advice fees and product charges which will impact the overall level of return you achieve.

Autumn Statement – what the announcements mean for your finances

Chancellor Jeremy Hunt promised to ‘reduce debt, cut taxes and reward work’ in his ‘Autumn Statement for growth’, but what might the changes he announced mean for your personal finances?

In the lead up to the Autumn Statement, we discussed the changes that were rumoured to have been announced in this article.

Arrange your free initial consultation

These speculated changes included:

- Reducing Inheritance tax

- Announcing an additional ISA allowance for investment into UK companies

- Changing the state pension triple lock calculation to limit next year’s state pension increase

In the end, none of these changes were introduced, with shadow chancellor Rachel Reeves claiming Hunt wanted to reduce inheritance tax but that he “couldn’t get away with it in the middle of a cost of living crisis”. Instead, the headline grabbing change was the 2% reduction to employee national insurance contributions between £12,571 and £50,271. This will equate to an annual saving of c. £754 p.a. to those earning over £50,270 p.a. with effect from January 2024. Additionally, there were National Insurance reductions for the self-employed, with Class 2 contributions effectively abolished and Class 4 contributions reduced from 9% to 8% between £12,571 and £50,271 with effect from April 2024.

However, this will only go part of the way to make up for the impact of the continued freezing of the income tax bands, which will remain frozen until 2028. Indeed, as a result of higher inflation, higher interest rates and frozen tax bands, the Office for Budget Responsibility (OBR) states “Living standards, as measured by real household disposable income per person, are forecast to be 3.5 per cent lower in 2024-25 than their pre-pandemic level.”

Separately, the speculated ISA allowance increase for investments into UK companies did not materialise and pensioners will be pleased to hear Mr Hunt state the government will “honour our commitment in full” as the state pension rises by 8.5% next year.

Regarding pensions, workers will hope a new legal right for their new employer to pay into their previous defined contribution pension scheme will simplify pension planning going forward and will mean an end to the accumulation of multiple schemes as individuals move between companies.

This was an Autumn Statement with half an eye on an upcoming general election, with announcements that should put more money in the pockets of workers and pensioners alike. Mr Hunt repeatedly referred to the OBR’s forecasts during his announcement as he tried to rebuild credibility, a little over a year after Liz Truss and Kwasi Kwarteng’s ‘mini-budget’, prior to which the OBR was not asked to run forecasts. Overall, Mr Hunt will have been grateful that he was able to use some of the fiscal headroom provided by then Chancellor, now Prime Minister, Rishi Sunak’s decision to freeze income tax bands back in 2021 to offer a national insurance cut and significant state pension rise to the voting public.

Arrange your free initial consultation

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

Will 2024 see another recession?

The economy faces potential risks of a recession in 2024, indicated by negative economic trends, reduced investment in real estate and non-residential sectors, and potential weaknesses in global trade and labour market conditions.

Core inflation has remained above the Federal Reserve's target, prompting a more hawkish stance and increased attention to tackling inflationary pressures. The market's response to this is reflected in rising US bond yields, while the NASDAQ 100 continues to climb, driven by the AI revolution and increased retail investor participation. However, the labour market is strong, evident through robust job creation and low unemployment claims.

Looking Back: 2023 Market Roundup

We take a look back at market activity from the last six months, to help form future predictions in the economy.

Labour Market Strength and Inflation

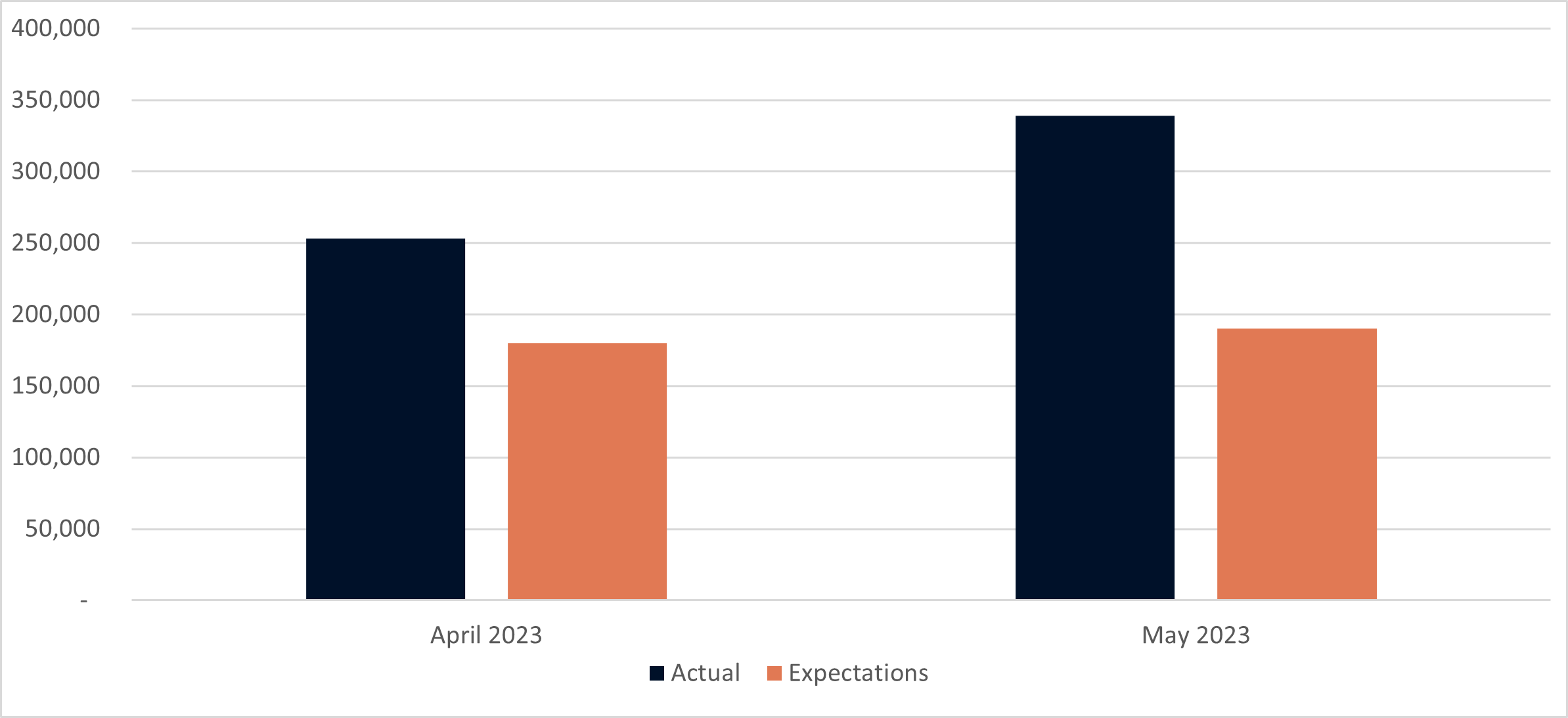

The labour market is a key indicator of economic health. A robust labour market implies sustainable employment, allowing the Federal Reserve to focus more on controlling inflation. Recent data shows that US job creation (nonfarm payrolls) exceeded expectations in April and May, signalling strength in job creation. Additionally, unemployment claims remain relatively low, indicating a resilient labour market.

Figure 1. US Nonfarm Payrolls. (Source: BLS, 2023.)

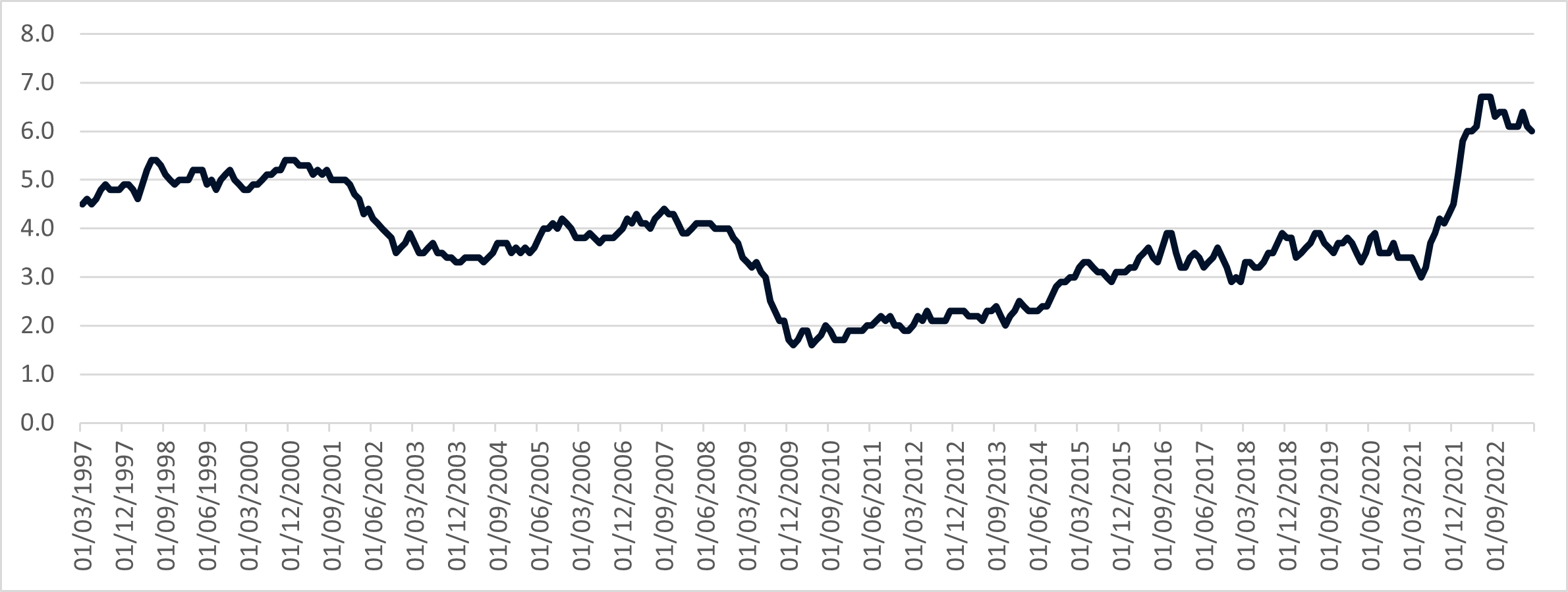

Wage growth is another factor closely monitored by the Federal Reserve. Currently, it stands at around 6% year-on-year. Higher wages translate to increased consumer spending, thereby driving inflation. Personal spending has also witnessed a notable increase, contributing to elevated inflation levels within the US.

Figure 2. US Wage Growth. (Source: Atlanta Fed, 2023.)

Core Inflation and Federal Reserve's Focus

Core inflation, which excludes volatile sectors like energy and food, remains above the Federal Reserve's target of 2%. This persistent elevation in core inflation prompts the Federal Reserve to adopt a more hawkish stance. With a strong labour market, their attention is primarily directed towards tackling inflationary pressures.

Federal Reserve Members' Outlook

Several Federal Reserve members expressed their views in May, providing insights into the future direction of monetary policy. Christopher Waller, a voting member of the Federal Reserve Committee, suggested further hikes in July. Federal Reserve members updated their June “dot plot” projections of monetary policy and revised their interest rate expectations upwards. The growing hawkish sentiment among Federal Reserve members indicates their commitment to addressing inflationary concerns among a backdrop of strong consumer spending.

Bond Yields, Equity Markets, and the Tech Revolution

The market response to the Federal Reserve's outlook can be observed in the movement of yields. As expectations of rate hikes increased, US bond yields, such as the US 2-year and 10-year, started moving up. This shift in yields reflects market participants' belief that the Federal Reserve will prioritise controlling inflation.

Interestingly, despite rising yields, the NASDAQ 100, a technology-focused growth index, continued to climb. This divergence from the conventional expectation, where rising discount rates lead to underperformance in growth stocks, can be attributed to the AI revolution. Companies like Microsoft, Apple, Amazon, Nvidia, Meta, and Alphabet, which contribute significantly to the NASDAQ 100, have been capitalizing on the potential of artificial intelligence (AI) and witnessing substantial growth. This trend has attracted retail investors, driving their increased participation in US equities.

Figure 3. US 2-Year Treasury Bond Yield. (Source: MarketWatch, 2023.)

Figure 4. US 10-Year Treasury Bond Yield. (Source: MarketWatch, 2023.)

Narrow Market Breadth and Retail Investor Sentiment

The performance of the S&P 500, the benchmark index, reveals a narrower breadth, with a few dominant companies outperforming the rest. This divergence from historical patterns indicates that the market is currently driven by a handful of large-cap stocks. Retail investors, driven by the fear of missing out, are keen to tap into the growth potential of these AI-focused companies, leading to increased investment in US equities.

Liquidity and the US Debt Ceiling Crisis

The recent uptick in liquidity in the market is another notable trend. Despite the US debt ceiling crisis, where the government faced borrowing limitations, liquidity has increased. This unexpected outcome can be attributed to the counterbalance between government spending and bond issuance. As the government continues to spend while facing borrowing constraints, liquidity injections occur, impacting market dynamics.

Figure 5. Liquidity Driving Markets. (Source: StenoResearch, 2023.)

Looking Forward: 2024 Recession Risk

Leading Economic Indicators and Investment Patterns

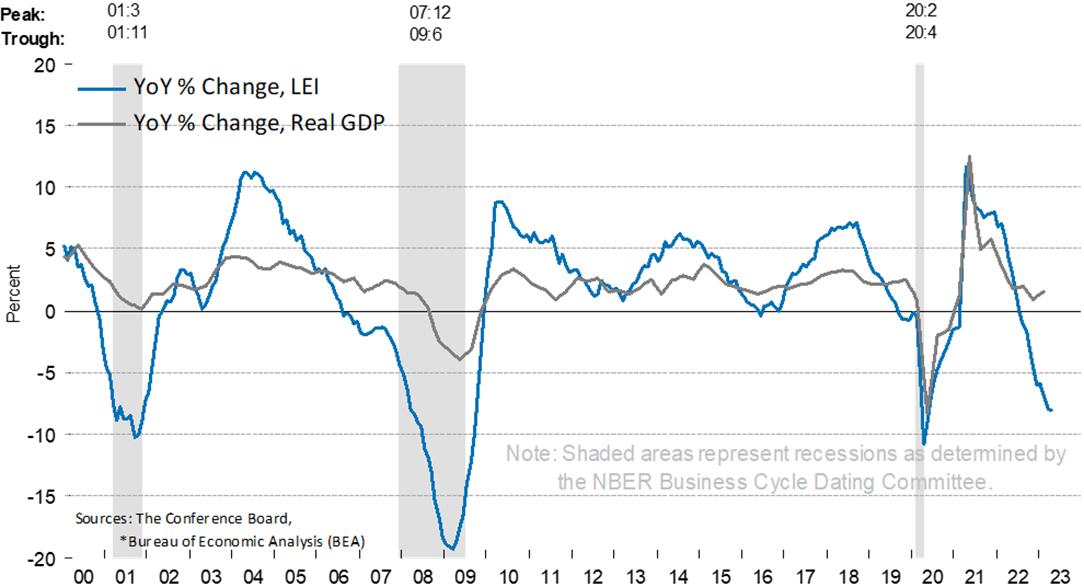

The Conference Board's Leading Economic Indicator, comprising various variables, serves as a reliable measure of economic growth and recessionary signals. Currently, the leading indicator exhibits a deep negative trend, indicating a possible recession in the near future.

Figure 6. Leading Economic Indicator. (Source: Conference Board, 2023.)

Examining specific segments of the economy, such as private residential fixed investment, reveals a significant relationship between investment in real estate and economic downturns. As interest rates rise, demand for mortgages and housing decreases, resulting in reduced investment in the construction sector. Given that residential real estate investment peaked about six months ago, it aligns with the 6 to 12 months timeline for a potential recession. Non-residential investment, which includes spending on factories and machinery, is also a critical indicator. The Goldman Sachs Capital Expenditure (CapEx) tracker suggests a potential decline in non-residential fixed investment, further emphasising the possibility of an economic slowdown.

Global Trade Labour Market Conditions

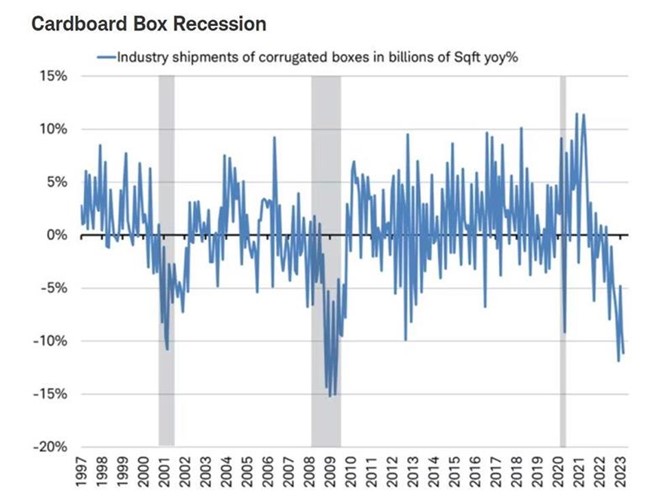

To gauge the demand for goods in the economy and the global market, alternative indicators such as cardboard box shipments and firm expenditures on freight provide valuable insights. Declines in these indicators during previous recessions demonstrate the interconnectedness between global trade and economic downturns.

Figure 7. Cardboard Box Demand. (Source: DisruptorStocks, 2023.)

Labour Market Conditions

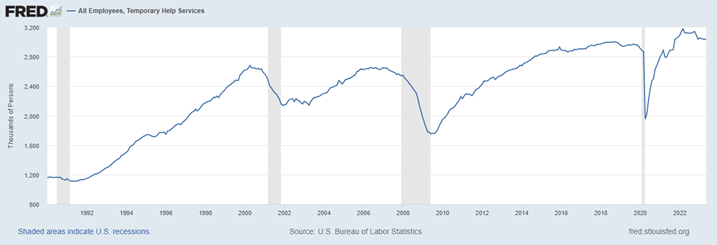

Analysing the labour market, employment in temporary help services serves as an effective leading indicator. Historically, peaks in temporary employment have preceded recessions, and negative year-over-year growth in this sector has consistently been followed by a recession. While the labour market remains robust, initial jobless claims have recently ticked up, signalling potential weakness in the future.

Figure 8. Employment of Temporary Help Services. (Source: Federal Reserve, 2023.)

Consumer Strength and Financial Stress

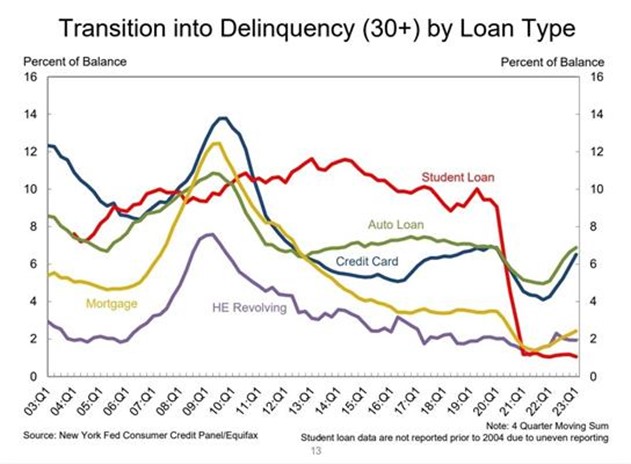

Consumer spending, driven by excess savings accumulated during the pandemic, has been a significant factor supporting the economy. However, the estimated excess savings are gradually being depleted, indicating a potential decline in consumer spending within the next 6 to 12 months. Rising delinquencies on credit cards and auto loans indicate rising financial stress, and restarting student loan payments could further strain consumer finances and lead to reduced spending in various sectors, negatively impacting economic growth.

Figure 9. Loan Delinquencies. (Source: NY Fed, Equifax, 2023.)

Summary

Despite the potential risks, several factors may help mitigate the impact of a recession. Household leverage (personal debt) is currently low, with debt service payments as a percentage of disposable income at multi-generational lows. This provides households with flexibility to borrow and spend, potentially bolstering economic activity. Additionally, business debt as a percentage of GDP, while reasonably high, is manageable, with a significant portion of debt not coming due until later years and borrowings locked in at low rates.

Government spending remains substantial, which historically has injected demand into the economy. The government's current deficit of ~5% of GDP suggests a level of support that can cushion the impact of an economic downturn. Moreover, the Federal Reserve's policy space, with room to lower interest rates if necessary, and the demonstrated ability of the Fed and Treasury Department to respond swiftly during the 2020 crisis provides additional reassurance.

In summary, there are some worrying indicators of recession. However, a combination of resilient consumers with low levels of personal debt and Governments willing to step in when necessary might keep a full-blown recession at bay.

Please contact your adviser if you require assistance, or if you're looking to get started and have £100k or more in investable assets, arrange your free initial consultation.

Arrange a free initial consultation

Note: This Market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Additionally, past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.

First Republic – Another Banking Collapse. Should we be worried?

The recent collapse of First Republic, the second-largest bank failure in US history following the 2008 demise of Washington Mutual, has sent tremors through the financial sector. This article aims to delve into the causes and implications of the collapse, while providing a comparison to previous banking crises. Analysing the factors leading to First Republic's downfall will shed light on the challenges faced by the US banking sector and the subsequent ripple effects on the broader economy.

Comparing First Republic to Past Banking Collapses

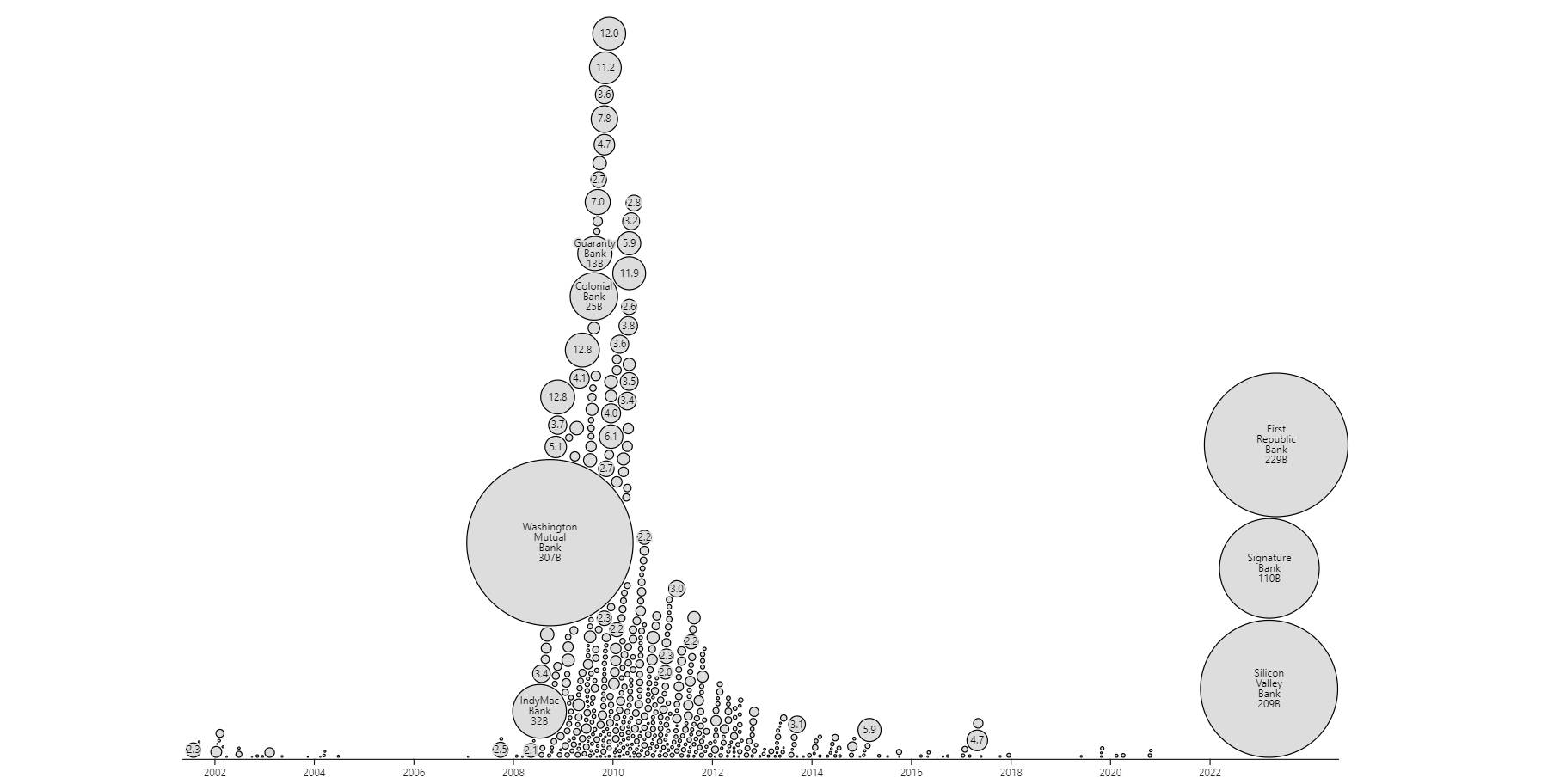

Figure 1. Bank Collapses. (Source: Observable, 2023.)

The magnitude of First Republic's collapse cannot be underestimated. Using a chart ranking US banking collapses by both date and size, it becomes apparent that the absolute impact of First Republic and its predecessor, Silicon Valley Bank (SVB), is significant. However, when considering the sheer number of collapsed banks, the recent events pale in comparison to the numerous failures experienced from the 1950s to the 1980s.

The Role of SVB and Uninsured Deposits

The troubles for First Republic began with the collapse of SVB, which caused investors to panic and raised concerns about the stability of the US banking sector. One crucial aspect that exacerbated the situation was the fact that 67% of First Republic's deposits were uninsured. While the Federal Deposit Insurance Corporation (FDIC) provides coverage up to $250,000 per person, amounts exceeding this threshold are left unprotected. As SVB crumbled, investors withdrew their funds from perceived risky regional banks, seeking to diversify their uninsured deposits. This mass movement of capital triggered a degree of panic within the US banking system.

Asset Liquidation Attempts and the Struggle of First Republic

Following a pattern similar to SVB, First Republic attempted to sell its assets to mitigate the crisis. However, the majority of the bank's net interest income and asset base consisted of government bonds, municipal securities, and real estate loans. The latter, being less liquid, presented challenges in meeting deposit requests, rendering the bank unable to fulfill its obligations.

The Wider Context

In this section, we will delve into the current state of the banking system and explore the conditions that have contributed to the challenges faced by financial institutions. By examining Q1 earnings reports from major banks, analysing deposit and loan trends and evaluating the impact of unrealised losses on securities, we can gain insights into the overall health of the banking sector and identify areas of concern.

Q1 Bank Earnings and Performance

When reviewing the Q1 earnings of prominent banks, it becomes evident that, on the whole, they have remained relatively healthy. JP Morgan emerges as a standout performer, experiencing substantial growth with a 50% increase in net income and a 25% rise in revenue compared to the previous year. With improved margins and positive performance across the board, most major banks have fared well in the first quarter.

Interest Rates and Income

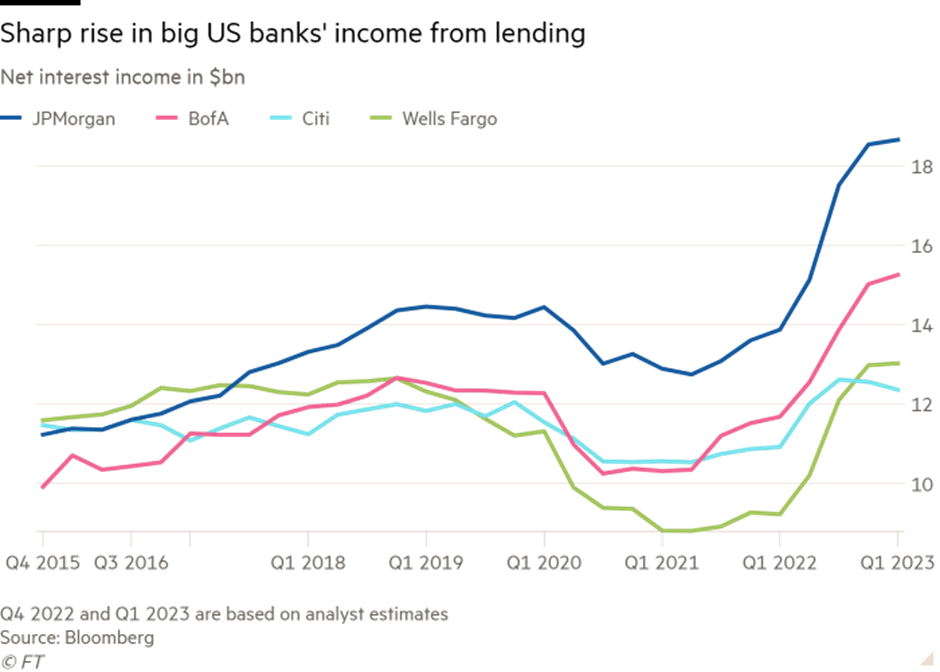

Figure 2. Bank Interest Income. (Source: FT, 2023.)

The increase in interest rates has played a significant role in boosting banks' profitability. As interest rates rise, banks charge higher rates on new loans, resulting in increased interest income as they can achieve greater margins on their loans. Notably, JP Morgan's shorter term loan book has allowed them to take advantage of the higher interest rates more swiftly.

Deposit and Loan Trends

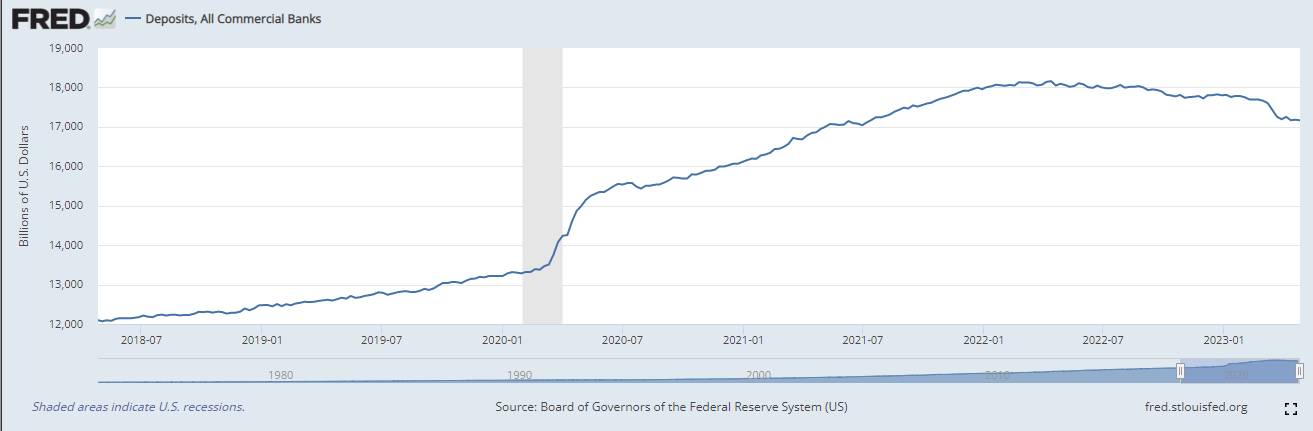

Figure 3. US Commercial Bank Deposits (top) and Loans (bottom). (Source: St Louis Fed, 2023.)

Traditionally, there is a positive correlation between deposits and loans, with deposits often created through loan extensions. However, since mid-2022, deposit levels have been declining and in recent weeks they have accelerated. in deposits made. This decline can be attributed to flows into money market funds. Despite the decline in deposits, loans extended to the real economy have remained relatively strong, although there has been a slight slowdown. This divergence raises concerns about the future impact on banks' liquidity and ability to lend.

Shifts in Deposit Distribution

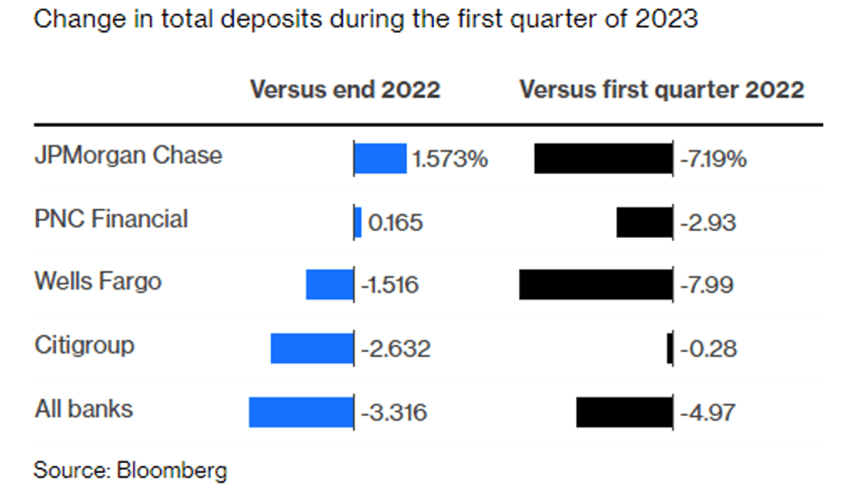

Figure 4. Q1 2023 Deposit Change by Bank. (Source: Bloomberg, 2023.)

Examining the changes in deposits among the 150 largest banks, it becomes evident that deposit flight has not affected all banks uniformly. JP Morgan, in particular, has benefited significantly from this shift. Deposits have moved away from weaker and smaller banks, flowing into larger and stronger institutions.

Why Are Depositors Nervous? Unrealised Losses on Securities and Capital Adequacy Ratios

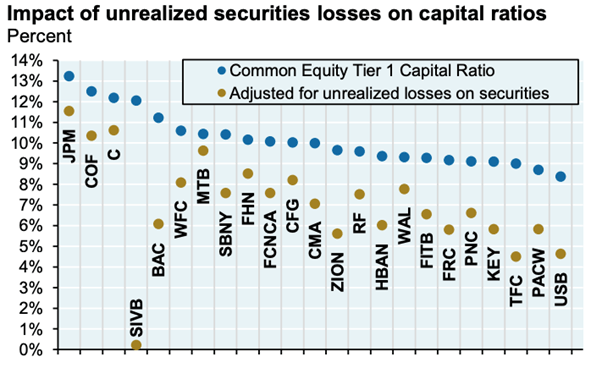

Figure 5. Impact of unrealised losses on securities holdings on banks capital adequacy ratios. (Source: SeekingAlpha, 2023.)

Unrealised losses on securities have impacted banks' capital adequacy ratios to varying degrees. While smaller banks have experienced more significant impacts, larger, institutionally important banks have weathered the storm relatively well. The fact that larger banks have maintained safer leverage ratios provides some reassurance regarding their stability compared to smaller banks.

Why Are Depositors Nervous? Challenges in Commercial Real Estate

Figure 6. Rise in US office vacancy. (Source: FDI Intelligence, 2023.)

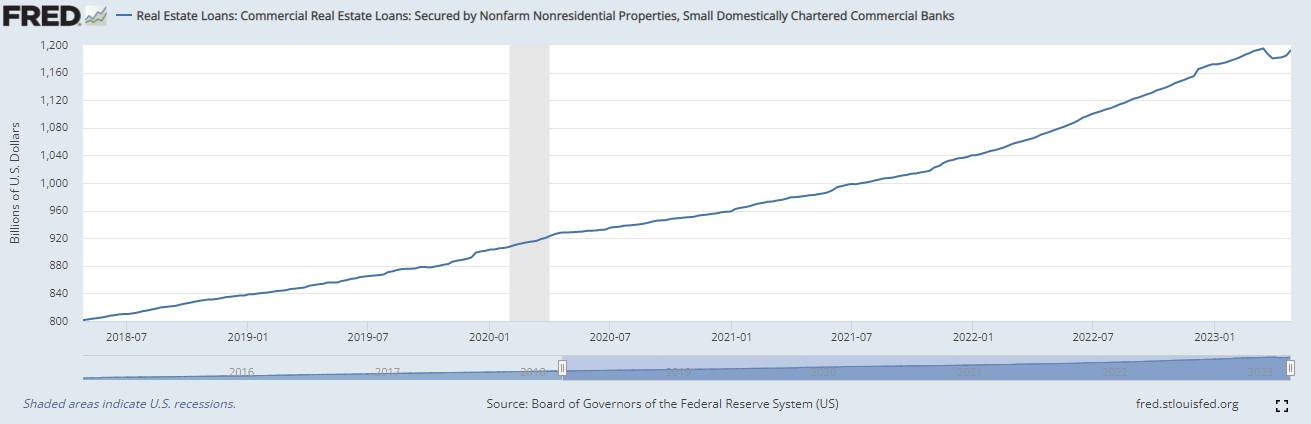

Figure 7. Rise in small US Bank lending to commercial real estate. (Source: St Louis Fed, 2023.)

Commercial real estate, particularly office spaces, has become an area of concern for banks. With the rise in remote work and increased office vacancies, tenants are struggling to make payments, impacting the loans tied to these properties. Small banks have a higher exposure to commercial real estate loans and this exposure has contributed to depositors' nervousness and their concerns about the value of their deposits.

Why Are Depositors Nervous? Funding Mix and Profitability

Figure 8. Proportion of US Small Bank funding themselves through deposits. (Source: St Louis Fed, 2023.)

The funding mix of banks has shifted, with a notable move away from deposits and toward borrowing from capital markets. While deposits are generally considered safer and more stable, capital market borrowing carries higher risks and interest costs. Banks face increased scrutiny from capital market investors, who can swiftly withdraw funding. This shift in funding mix poses challenges to profitability for banks due to higher funding costs in capital markets.

Conclusion

The health of the banking system is multifaceted and impacted by various factors. While major banks have displayed overall stability and positive performance, concerns regarding deposit flight, commercial real estate, and funding mix pose challenges for smaller banks. The continued relative strength of larger banks, such as J P Morgan, will be an important factor in preventing a crisis amongst smaller regional US banks becoming a more significant broader, economic crisis.

Please contact your adviser if you require assistance, or if you're looking to get started and have £100k or more in investable assets, arrange your free initial consultation.

Arrange a free initial consultation

Note: This Market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Additionally, past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.

Alternative Investing Guide

Shhh Insiders Guide to Wealth Management