Skip to main content

Skip to main content

Diversify or die - the case for balanced investor portfolios

In our Investment Markets update this month, we’re going to cover the following 2 themes:

-

How April 2024 contrasted to Q1, leading to the benefits of diversification.

-

The impact of the change in monetary policy expectations in April and how this drove returns.

Arrange your free initial consultation

Market Volatility and Investor Sentiment

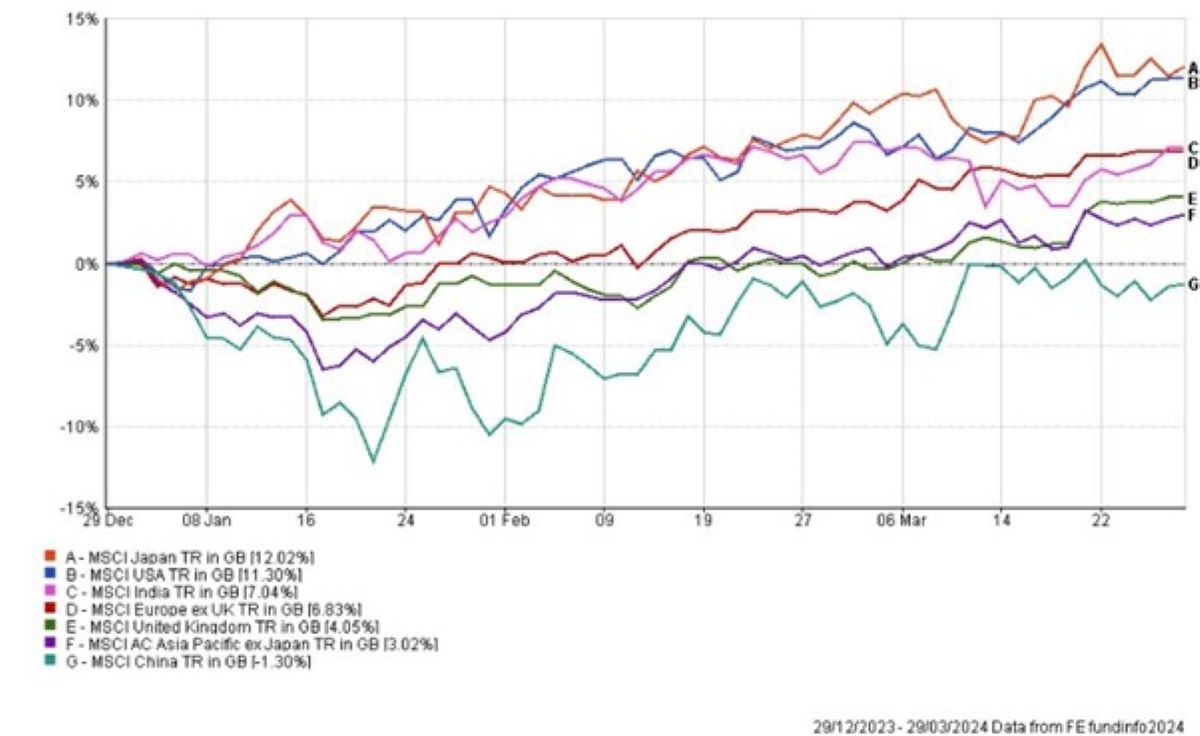

Markets are fickle and are prone to reversing their trends at the drop of a hat. The fundamental forces that underpin them are usually slow moving, but investors animal spirits aren’t easily tamed. They can bolt like a wild beast in response to small disturbances, in the form of economic data releases that don’t conform to expectations. This was the case in April, when markets took slowing US economic growth and sticky inflation data poorly, causing a stampede to exit many of the main regional equity and fixed income markets. That said, there were some regions that maintained their sense of calm and even excelled – reinforcing the value of holding a portfolio diversified across geographies.

Q1 Market Performance

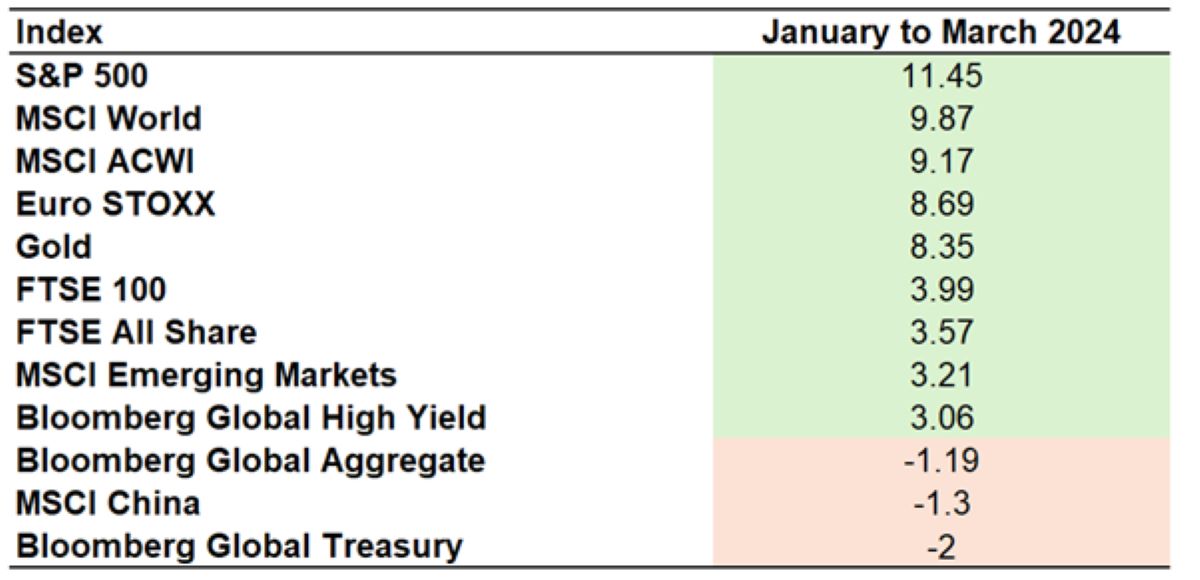

To frame this story we’d like to show you how markets behaved from January to March. The table below provides a brief summary. Figure 1 – Table of returns to key global asset classes – Source: FE Analytics, 2024.

Figure 1 – Table of returns to key global asset classes – Source: FE Analytics, 2024.

US equities, in the form of the S&P 500 index, led the pack and drove global equity returns, represented by the MSCI World and ACWI indices. UK equities, in the form of the FTSE 100 and FTSE All Share indices, posted respectable performance, however lagged their European and US peers. Chinese equities were in the doldrums, pulled down by negative investor sentiment engendered by a deflating property bubble and the overhang of geopolitical tensions. In a few words: the US excelled, the UK did OK, and China saw serious underperformance.

April's Market Reaction

So what happened in April? US inflation and growth data disappointed investors relative to their expectations. Firstly, economic growth slowed, taking some initial wind out of the sails of US equities, but didn’t slow enough to force the Federal Reserve into signalling interest rate cuts. Secondly, US inflation remained more sticky than investors had hoped, with that last mile down to the 2% target being frustratingly elusive. The inability for inflation to make that final leap below 2% caused much consternation among investors, who removed between 1 and 2 expected interest rate cuts from their pricing of bond yields, causing bond yields to rise and subsequently equity prices to fall. US markets, in the main, drive global markets so this trend spread across most developed markets.

Interest Rate Expectations

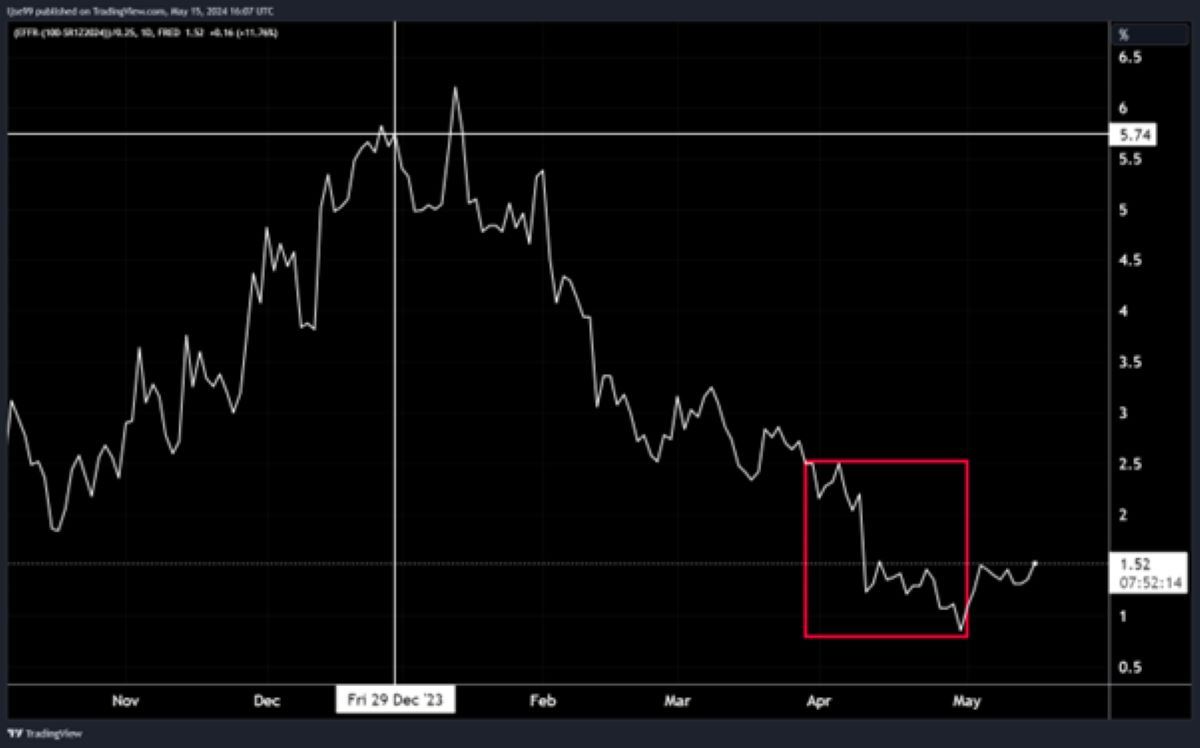

Figure 2 – Number of Federal Reserve interest rate cuts by the end of 2024 expected by markets – Source: TradingView, 2024.

Figure 2 – Number of Federal Reserve interest rate cuts by the end of 2024 expected by markets – Source: TradingView, 2024.

The chart above illustrates the rollercoaster of interest rate expectations through the year. Markets expected nearly 6 interest rate cuts in 2024 at the start of 2024. By the beginning of April this was down to 2.5 cuts and by the end of April, following US GDP and inflation data, this was down further to only 1 interest rate cut. That final move has been boxed in red. This is a return of the so called ‘higher for longer’ interest rate narrative.

Resilience of Diversified Portfolios

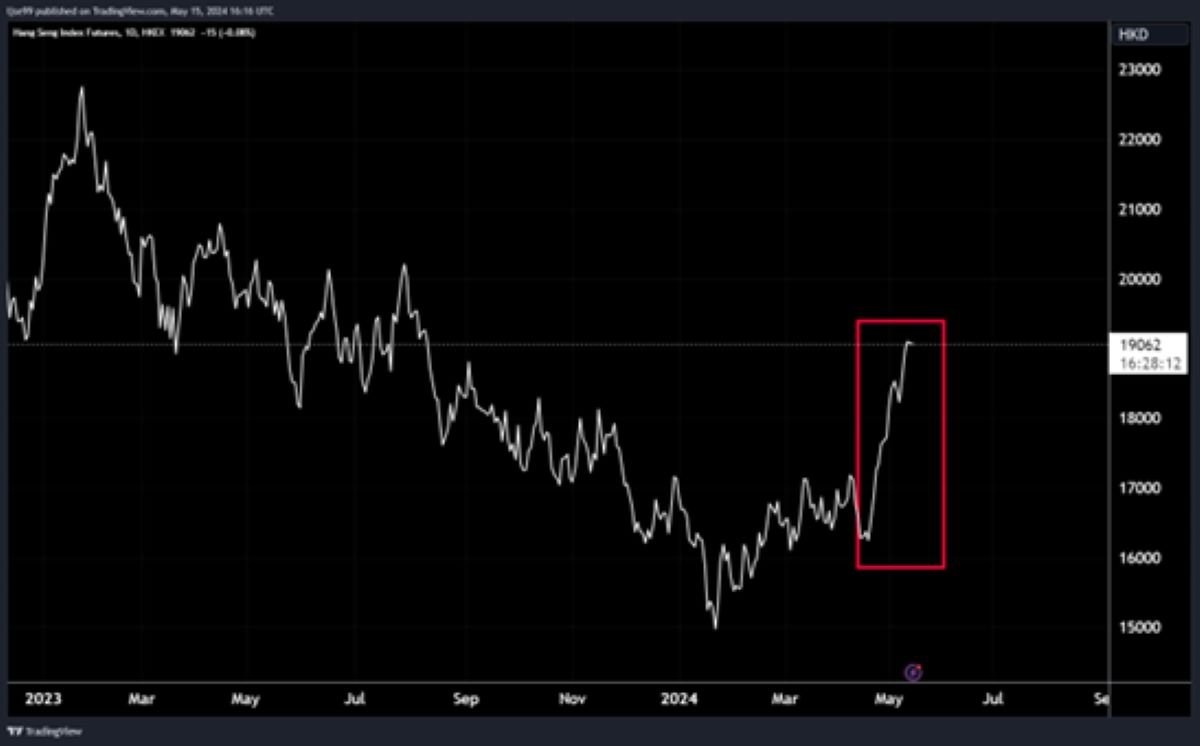

Figure 3 – Hang Seng equity index returns 2023 to date, with recent upwards thrust boxed in red – Source: TradingView, 2024.

Figure 3 – Hang Seng equity index returns 2023 to date, with recent upwards thrust boxed in red – Source: TradingView, 2024.

However, all was not lost, especially for investors with a diversified portfolio. Chinese equities finally made their comeback, following a year of brutal drawdowns – Chinese authorities had engineered a small reversal in price slides through numerous measures (some as extreme as banning onshore fund managers from selling) and this initial price action drew in western investors who had sat on the side lines for the last year. As western investors returned, prices surged upwards , shown in the Figure 3

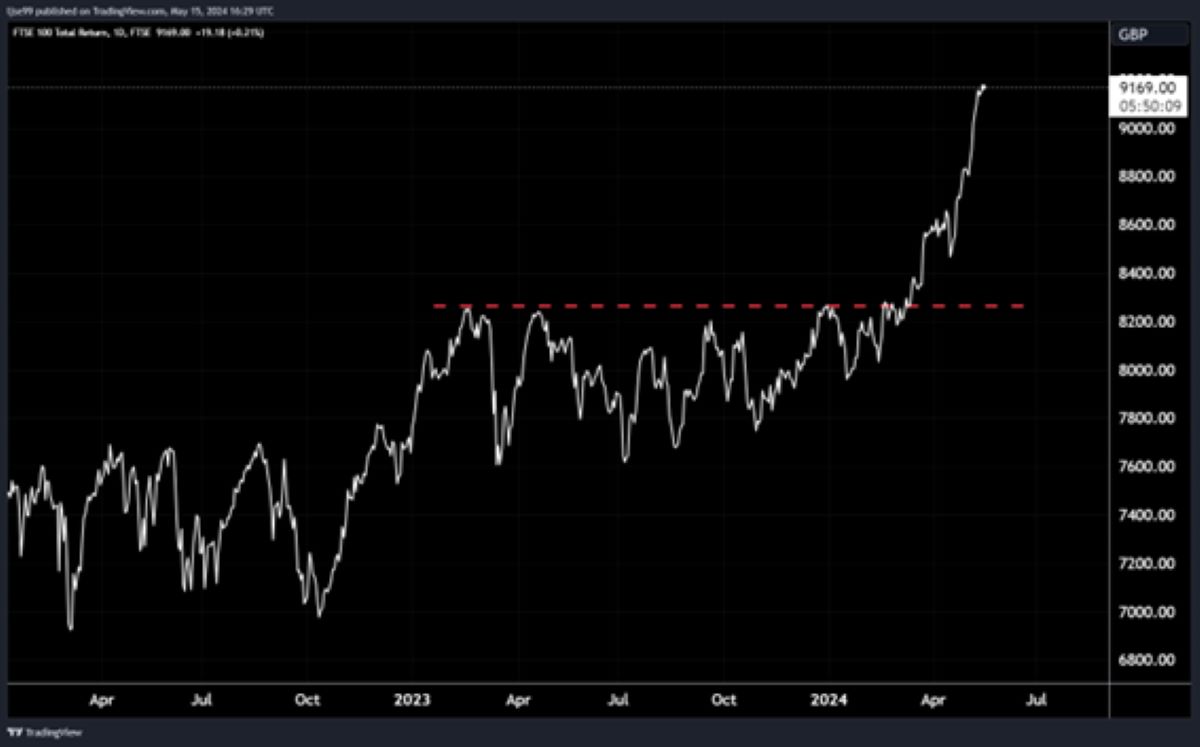

Figure 4 – FTSE 100 Total Returns – Source: TradingView, 2024.

Figure 4 – FTSE 100 Total Returns – Source: TradingView, 2024.

Potentially more relevant to readers in the UK was the performance of UK markets, which broke out from the cage they had been trapped in for 2023 and the start of 2024. The UK has a very different sector composition to US markets: where the US is heavy on high growth technology stocks, the UK has more of the older world industries which have underperformed over the long run but are well suited to periods of rising interest rates and elevated commodity prices (which remain high due to geopolitical tensions).

| Pre-tax profit | |

|---|---|

| Financials | 27% |

| Oil & Gas | 20% |

| Consumer Staples | 13% |

| Mining | 11% |

| Consumer Discretionary | 8% |

| Health Care | 8% |

| Industrial goods & services | 7% |

| Utilities | 3% |

| Telecoms | 2% |

| Real estate | 1% |

| Technology | 0% |

Figure 5 – Sectoral pre-tax profit share of the FTSE 100 – Source: Investor Chronicle, 2024.

The table in Figure 5 shows the sectoral share of FTSE 100 profits. Notable is the high share of financials (mainly banks) and energy and mining companies. Banks benefit from interest rates remaining higher for longer because it extends the period in which they can offer loans at high interest rates, increasing their margins and benefitting their profitability. Energy and mining companies benefitted from elevated commodity prices, which have seen an uplift as geopolitical tensions raise questions over security of supply.

Conclusion

In conclusion, markets at the highest level performed well from January to March, but took a tumble in April as slowing US economic growth and sticky US inflation caused investors to worry about the future path of interest rates – but this pain was not evenly spread, with some of the initial laggards becoming the best performers. This recent experience reinforces the need for a portfolio that is diversified across geographies, economic sectors and asset classes.

If you have any questions about your portfolio please don’t hesitate to contact your adviser.

Arrange your free initial consultation

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions.

Past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.

The investment crystal ball - What do we know so far?

With the first quarter of the year already wrapped up (it feels like Christmas was yesterday!) we thought it would be worth recapping the high-level macroeconomic picture and summarising the notable movements in markets through the quarter. We start with economic growth below.

Arrange your free initial consultation

Macroeconomics - Economic Growth & Inflation

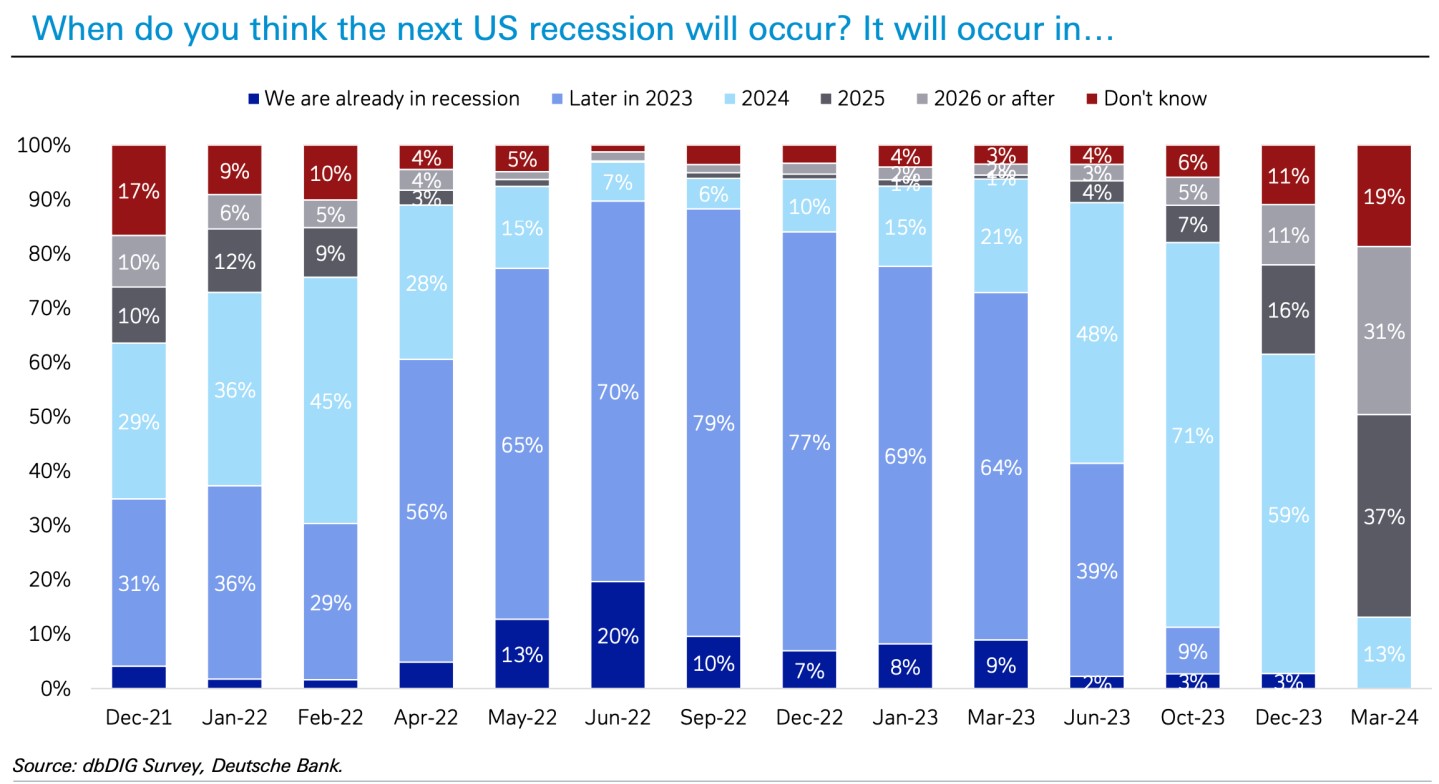

Figure 1 – When do economists think the next US recession will occur?, Source: DeutcheBank, 2024.

Before we dig into the current macroeconomic landscape it’s worth setting the scene by revisiting how macroeconomists expected the economy to perform both in 2023 and 2024’s first quarter. The chart above shows the percentages of economists that expect a US recession in given time periods, surveyed every quarter. Throughout 2023 the date of recession was pushed back ever further, from ‘later in the year’ out to ‘2024’. Now that we have arrived in 2024 expectations have moved out into 2025 and beyond. But why is this?

The most consequential data release was the Q4 2023 GDP data for the US, which surprised economists and investors, growing at an annualized rate of 3.4% . This has been reinforced by labour market data showing that hiring and wage growth remains strong, with the expectation that this will continue to support household consumption through 2024. The OECD now estimate the US economy to grow 1.5% in 2024, a far sight from the recession expected last year.

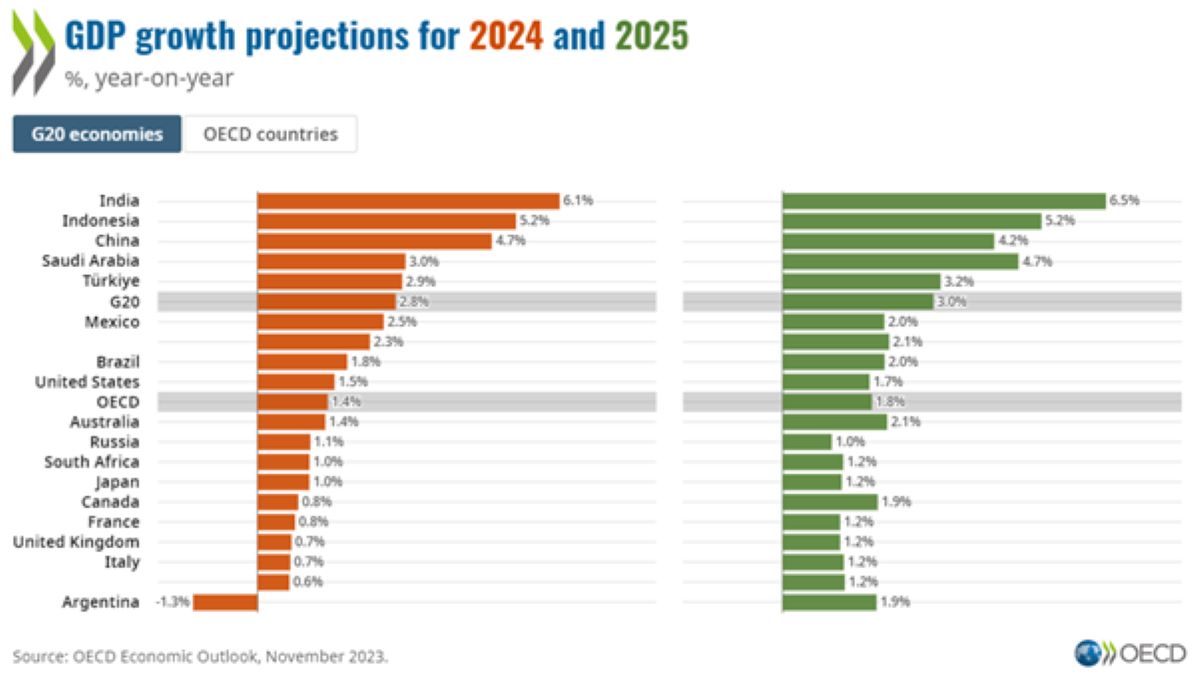

Economic growth outside of the US has been more sluggish, particularly in developed markets. Higher debt burdens in Europe have held governments back from the level of government investment seen in the US, while developed Asian economies are yet to see the full benefits of Chinese stimulus efforts. The OECD’s forecasts of economic growth in 2024 and 2025 for G20 economies can be seen below:

Figure 2 – GDP Growth projections for G20 and OECD countries, Source: OECD, 2024.

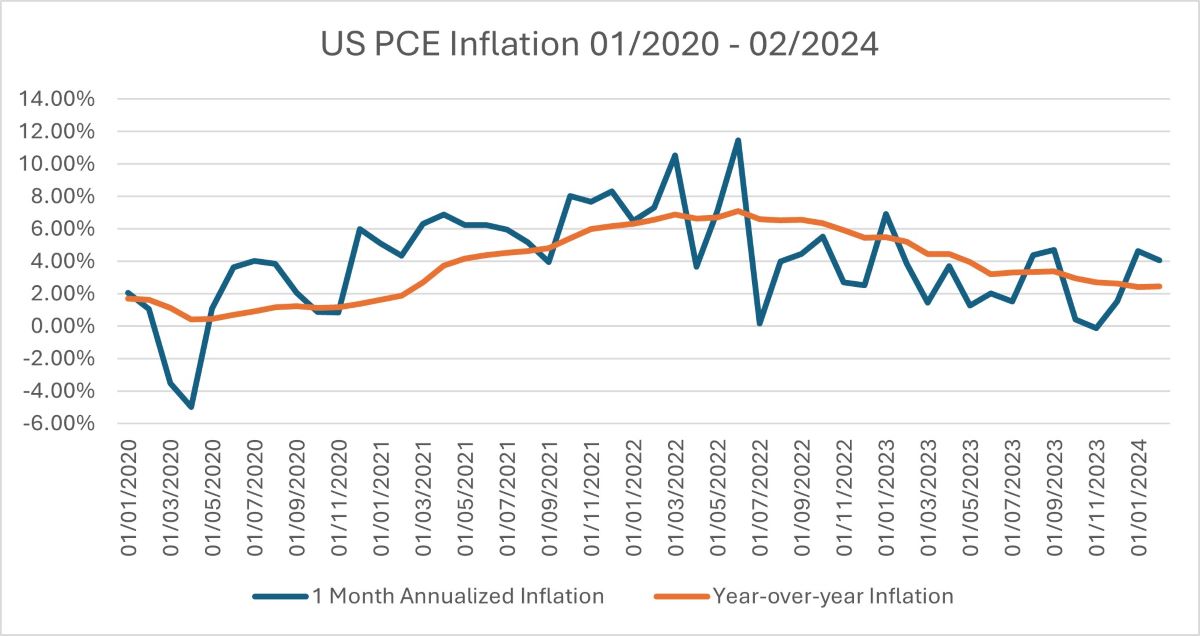

Figure 3 – US Inflation from 2020 – 2024, Source: Bureau of Economic Analysis, 2024.

The chart above shows the US inflation rate from 2020 through to the latest data release for February 2024. The orange line shows year-on-year inflation, while the blue line shows the inflation in a given month at an annualised rate, i.e. showing what the inflation rate would be for a whole year if it stayed at the pace of that month. Inflation data is fairly volatile from month to month, so the year-on-year figures are important in establishing trends, while the monthly data is useful in spotting where those trends may be changing course.

Two things stand out in the graph. Firstly, there has been a clear downward trend in inflation since July of last year. This has supported the Federal Reserve in guiding markets towards interest rate cuts in 2024. Secondly, inflation in the first two months of this year has accelerated above the year-on-year rate, running at an annualised rate of 4-4.5%. This second point has caused consternation among investors, who are becoming less certain that central banks will be able to cut interest rates in the first half of this year.

Markets – Fixed Income

That final point leads into the market performance of fixed income securities.

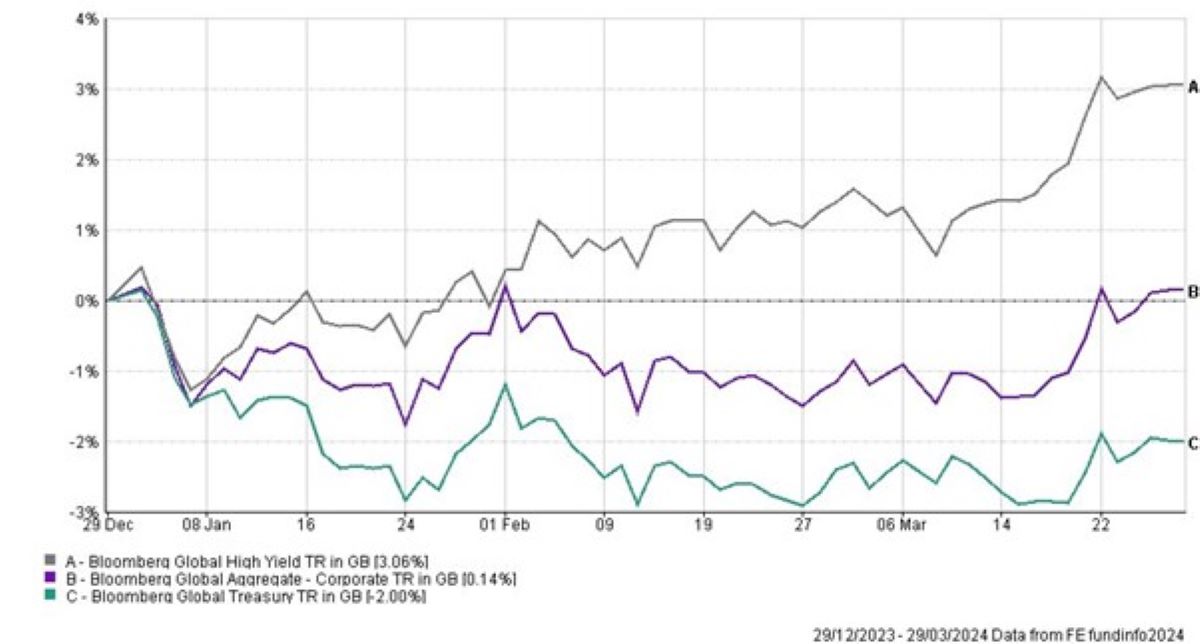

The price of a bond is inverse to the yield it pays, meaning rising bond yields cause falling bond prices (and thus capital values) and vice versa. As interest rate cut expectations are pushed further into the future and become less probable, the yield on bonds rises. This effect, of changes in interest rates and their expected future path on bond prices is called ‘duration risk’, and the effects of this risk are greater when a bond’s maturity is longer and the coupon (yield) it pays is smaller. Government bonds tend to have longer maturities, and owing to their security, tend to pay a smaller coupon (yield), making them highly susceptible to changes in interest rate expectations. At the other end of the spectrum, you find high yield corporate bonds, which tend to have a short maturity, and owing to their lower credit quality (i.e. higher credit risk) they pay a higher coupon. Thus, government bonds are more exposed to duration risk, high yield corporate bonds are more exposed to credit risk, and investment grade corporate bonds tend to sit in the middle on both risks.

Figure 4 – High Yield, Investment Grade and Government Bond returns in Q1 2024, Source: FE Analytics, 2024.

The first quarter saw high yield corporate bonds (grey line) outperform both investment grade corporate bonds (purple line) and government bonds (turquoise line). Going back to the macroeconomics, we had strong economic growth and some signs of inflation ticking up, meaning economic growth can sustain corporate cashflows and stave off credit risks, while inflation worries cause interest rate expectations to rise and thus longer duration bonds to selloff. Investment grade corporate bonds and government bonds were those longer duration bonds that sold off.

Markets – Equities

Figure 5 – Regional Equity Market Returns in Q1 2024, Source: FE Analytics, 2024.

Equity markets shrugged off the losses in government bonds and posted a strong quarter, with China being the only major region to see losses – a deflating property sector continues to weigh on corporate investment and household consumption. The strongest performance on a country basis was seen in Japan, propelled by a combination of robust corporate profit growth and favourable international investor sentiment. An interesting picture emerges when equity returns are broken down by sector, shown below.

Leading contributors

Time period: 01/01/2024 to 31/03/2024

| Rescaled weight | Return | Contribution | |

| Semiconductors | 7.28 | 34.53 | 2.32 |

| Software | 10.03 | 9.83 | 0.96 |

| Banks | 7.08 | 9.89 | 0.70 |

| Interactive media | 4.81 | 14.64 | 0.70 |

| Retail - Cyclical | 5.31 | 12.46 | 0.65 |

| Insurance | 3.97 | 13.50 | 0.52 |

| Oil & Gas | 4.33 | 10.59 | 0.46 |

| Drug manufacturers | 5.01 | 8.87 | 0.44 |

| Industrial products | 2.47 | 10.94 | 0.27 |

| Aerospace & defense | 1.56 | 15.64 | 0.24 |

| Credit services | 1,74 | 11.59 | 0.20 |

| Medical devices & Instruments | 2.03 | 9.52 | 0.19 |

| Media - Diversified | 0.99 | 19.57 | 0.18 |

| Retail - Diversified | 1.57 | 10.97 | 0.17 |

| Farm & Heavy construction machinery | 0.74 | 16.96 | 0.12 |

Figure 6 – Sector level contributions to global equity returns in Q1 2024, Source: Morningstar Direct, 2024.

The table above show industries, their weightings in global equity markets, the returns generated by those industries in Q1, and by multiplying their weight and returns shows their contribution to global equity market performance.

AI and semiconductors have driven market performance through 2023 and the first quarter, shown by semiconductors and software ranking top two in sector contribution. What has been interesting is the catchup of many of the ‘cyclical’ sectors that are sensitive to changes in economic conditions, these are the likes of banks, oil and gas producers, discretionary retailers, and industrial product manufacturers. These sectors had been fairly flat for the first two months of the year but staged a comeback in March following the release of data suggesting an upturn in the global manufacturing cycle and inflationary pressures.

Summary

Economic growth has been better than expected so far this year, particularly in the US.

Strong growth has underpinned rising inflation, which has held back government bond performance but supported returns in high yield corporate bonds.

Equity markets have been largely unphased by recent inflation data, with semiconductor and AI related stocks continuing to gain. However, towards the end of the quarter there has been a notable rotation into cyclical stocks that benefit from an economy that is heating up, both in terms of inflation and manufacturing growth.

As a client of either our discretionary or advisory portfolio service, your portfolios are positioned to capture remaining upside in the AI/semiconductor space, while retaining significant allocations to cyclical sectors through UK & European equities. Similarly, we remain vigilant to developments in bond (fixed interest) markets. Our asset class and sector/industry diversification aims to smooth out returns and ensure that our investors benefit from different investment opportunities throughout the economic cycle. If you have any questions about your portfolio please contact your adviser.

Arrange your free initial consultation

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions.

Past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.

The question is when rather than if

This month we explore how investors might be rewarded for holding a diversified portfolio and whilst one cannot time the markets the outlook for asset prices remains positive this year.

Arrange your free initial consultation

Global Equity Performance

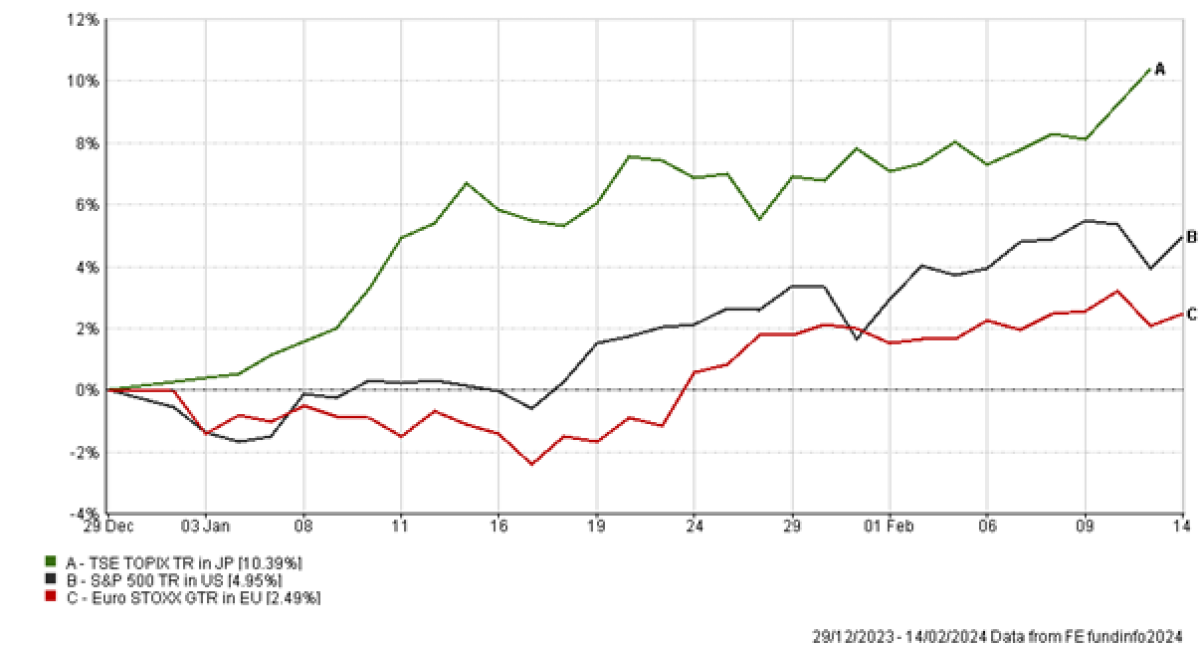

Last month was another strong month for equity markets with the S&P 500 reaching a record high as earnings for the “Magnificent 7” did not disappoint investors, a (long awaited) rebound in Chinese equities supported broader Asia, the Nikkei index in Japan reached a high not seen since December 1989 and European equities whilst underperforming relative to their US equity peers produced positive returns in the month (see Figure 1.).

Figure 1. World Equity returns, Source: JP Morgan, 29th February 2024

In fixed income we saw positive returns from high yield (a form of riskier corporate debt and less sensitive to interest rate expectations given its low duration) which is no surprise considering the positive return in risk markets such as equities. US and European Government bonds were down in the month as stronger inflation data saw investors push back their expectations of a cut in interest rates, meanwhile continued strength in UK wage data saw the price of Gilts fall as investors also revised their expectations of when the Bank of England will cut interest rates (see Figure 2.).

Figure 2. World Fixed Income returns, Source: JP Morgan, 29th February 2024

Diversification importance

Some of you reading this will have already noted that with equities going up in price and bonds falling in price, it means that the two asset classes exhibited negative correlation and offered investors the opportunity of diversification. That word (diversification) which has eluded investors in recent years as equities and bonds moved in tandem, going up together (most recently in October of last year) and falling together with the most notable example being in January 2022 when Central Banks reopened the quantitative tightening policy playbook and began to hike interest rates from historic lows.

As we move through this year the feature of ‘diversification’ and the idea that having exposure to multiple asset classes and regions is an optimal approach to one’s investment journey is something I expect to continue and will look to substantiate in this update. I’m cognisant though and to plagiarise the widely used quote that “history does not repeat but it rhymes”, it’s not as simple as to suggest simply repeating what was successful last time.

Interest rate expectations

Interest rates are expected to be cut this year as inflation data in the developed world has fallen materially from the highs of 2022. UK inflation in October 2022 was 11.1% and recently came in 4% year on year (which was even below analyst forecasts) and whilst the US - which has been the poster child for the soft-landing narrative - saw its most recent inflation print increase, this was to 3.2% which is a long way from the 9.1% inflation rate that was recorded in June 2022.

This sets the stage for a cut in interest rates which the market is anticipating will occur in Q2 of this year and with it the potential for bonds to reassume their rightful place as a diversifier in portfolios along with offering investors a positive return.

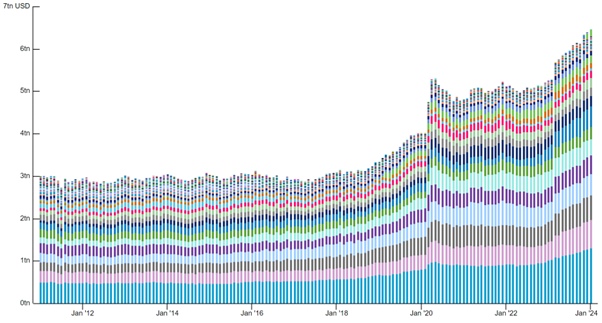

A fall in interest rates will also have implications for other asset classes. Money market funds which have attracted significant flows in recent times and have seen the Assets Under Management (AUM) in US money market funds reach c. $6.5tn (see figure 3.) will see their relative return fall as the interest on the funds is directly linked to the interest rate set by Central Banks.

Figure 3. Total assets in US Money Market funds, Source: OFR Analysis, 31st January 2024

The question then posed is will the prospect of reinvestment risk (reinvesting one’s income at a lower rate than previously invested) see increased inflows in equity markets as investors look to achieve a higher return.

Research by Schroders showed that since 1928 there have been 22 interest rate cutting cycles in the US and that on average, equities have outperformed cash by 9% in the 12 months after the first cut in interest rates. Bonds have also typically outperformed cash with an average outperformance of 3%.

Regional opportunities

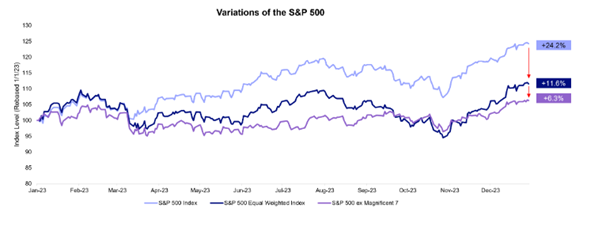

Referring to my earlier point about not repeating exactly what worked previously. Much has been made about the recent performance of the ‘Magnificent 7’ (see figure 4.) and the rich valuation of US equities compared to the broader US equity market. Whilst there are reasons to support the continued outperformance of these companies (high free cash flows, low levels of debt and durable business models) this is not the same as saying that all the other 493 listed companies in the S&P 500 or more broadly non-US equites will underperform.

Figure 4. Performance of the ‘Magnificent 7’, S&P 500 index, S&P 500 equally weighted index last year, Source: OFR Analysis, 31st January 2024

US exceptionalism – the idea that the US economy has better relative growth, more dynamic financial markets and a strong currency – has long been touted as a reason for the continued outperformance of the US equity market and whilst this is certainly one reason, there are a number of reasons to think we may see this exceptionalism wane at least in the short term.

This is in part due to the fact that the market is pricing in a soft landing in the US and that the Federal Reserve has been able to implement the ‘perfect policy’ (I remain sceptical) but also that investors remain pessimistic on the outlook for other regions.

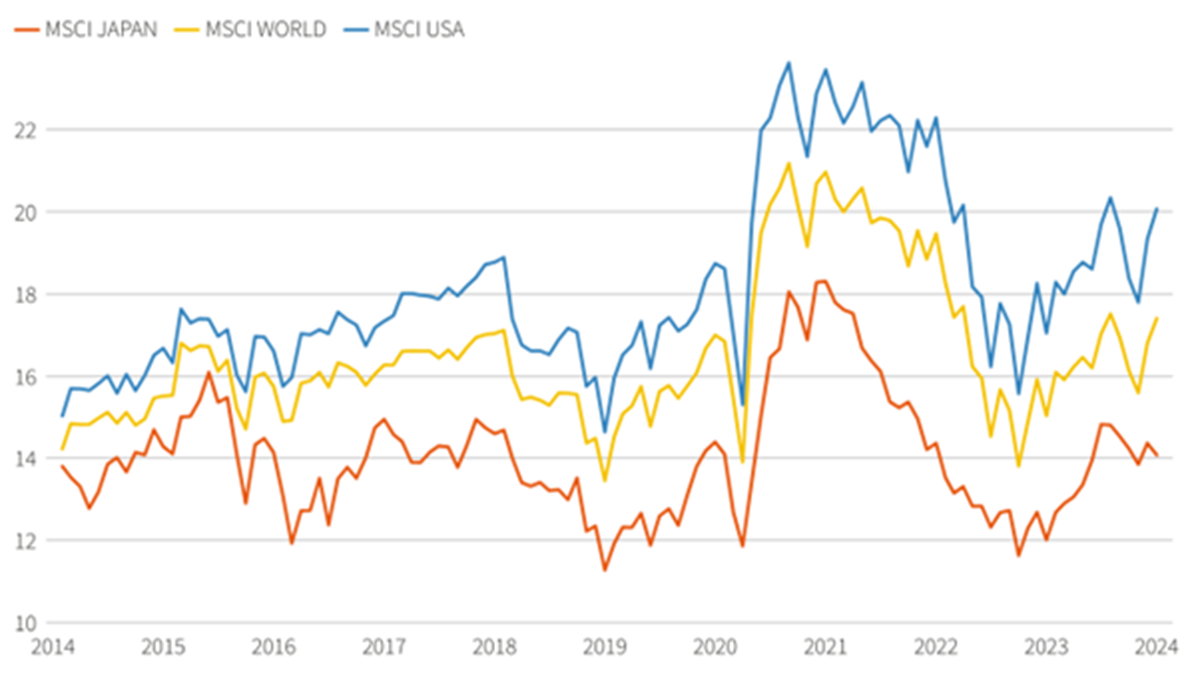

Leading economic indicators in Europe are beginning to trend up, global factory activity is increasing, and investors are beginning to reassess their view on equities outside of the US specifically given the divergence of European equities compared to US equities. Another potential opportunity lies in Japan where corporate governance reforms and interventions from the regulator will likely see continued support for Japanese equity markets and there looks to be continued price upside considering that the market trades on a cheaper valuation to its global peers (see Figure 5.).

Figure 5. Forward Earnings of equity markets, Source: LSEG & Reuters, 23rd February 2024

Conclusion

Putting all of this together suggests that investors will be rewarded for holding a diversified portfolio and whilst one cannot time the markets the outlook for asset prices remains positive this year.

If you would like to speak to your adviser about this, or have any other questions please don’t hesitate to get in touch.

Arrange your free initial consultation

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions.

Past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.

Spring Budget 2024

The Spring Budget 2024 confirmed some rumours, such as the introduction of a British ISA, and at the same time, contained a few surprises too.

The main points are summarised below along with a reminder of some of the other changes coming into effect in April 2024.

Some measures are potentially subject to change until enacted into legislation.

If you have any questions or would like to speak to one of our expert financial advisers about the changes announced, contact us to arrange a free initial consultation.

Arrange your free initial consultation

Pensions

Abolition of Lifetime Allowance (LTA) from 6 April 2024

A further Pension Schemes Newsletter / Lifetime Allowance Guidance Newsletter is expected this week but no further detail was issued as part of the Budget itself. Further information will be issued once it’s available.

State pension

Triple lock means new state pension and basic state pension will increase by 8.5% in April 2024. Full new state pension figure will be £221.20 per week.

Investments

Individual Savings Accounts (ISA)

The annual subscription limits all remain at their current levels in 2024/25, i.e.

- £20,000 ISA

- £4,000 Lifetime ISA

- £9,000 Junior ISA (and Child Trust Fund)

A new British ISA is to be introduced from a date to be confirmed. This will give investors an additional £5,000 ISA allowance each tax year, so on top of the current £20,000. There is a consultation paper in place to obtain feedback from ISA managers, but the idea is for allowable investments to include UK equites and potentially UK corporate bonds, gilts, collectives.

As previously announced at the Autumn Statement, the government is to make changes to ISAs to simplify the scheme and widen the scope of investments that can be included in ISAs. To simplify the scheme the government will:

- Allow multiple subscriptions in each year to ISAs of the same type, from 6 April 2024

- Remove the requirement to make a fresh ISA application where an existing ISA account has received no subscription in the previous tax year, from 6 April 2024

- Allow partial transfers of current year ISA subscriptions between providers, from 6 April 2024

- Harmonise the account opening age for any adult ISAs to 18, from 6 April 2024

- Digitise the ISA reporting system to enable the development of digital tools to support investors

Reserved Investor Fund

The Reserved Investor Fund is a new type of investment fund designed to complement and enhance the UK’s existing funds rule. This meets the industry demand for a UK-based unauthorised contractual scheme, with lower costs and more flexibility than the existing authorised contractual scheme. The introduction date is still to be confirmed.

Taxation

Income tax

All income tax rates and bands remain at their current levels in 2024/25. See our latest tax tables 2024/25.

National insurance (NI)

National Insurance is paid by people between age 16 and State Pension age who are either an employee earning more than £242 per week from one job or self-employed and making a profit of more than £12,570 a year.

Following on from the NI cuts made in the Autumn Statement when the 12% rate of employee NI reduced to 10% from January 2024, the government is cutting the main rate of employee NI by 2p from 10% to 8% from 6 April 2024.

They are also cutting a further 2p from the main rate of self-employed National Insurance on top of the 1p cut announced at Autumn Statement and the abolition of Class 2.

This means that from 6 April 2024 the main rate of Class 4 NICs for the self-employed will now be reduced from 9% to 6%.

Child Benefit charge

The adjusted net income threshold for the High Income Child Benefit Charge (HICBC) will increase from £50,000 to £60,000, from 6 April 2024.

For individuals with income above £80,000, the amount of the tax charge will equal the amount of the Child Benefit payment. For those with income between £60,000 and £80,000, the rate at which HICBC is charged is halved, and will equal one per cent for every £200 of income that exceeds £60,000.

New claims to Child Benefit are automatically backdated by three months, or to the child’s date of birth (whichever is later). For Child Benefit claims made after 6 April 2024, backdated payments will be treated for HICBC purposes as if the entitlement fell in the 2024/25 tax year if the backdating would otherwise create a HICBC liability in the 2023/24 tax year.

In his Budget speech, the Chancellor announced that the plan is to move assessment for the HICBC to a system based on household income from April 2026. This is to remove the current unfairness meaning that a couple who each have income below the threshold, so could in 2023/24 have £49,000 pa each (£98,000 pa in total), wouldn’t be subject to the HICBC whereas another household with one person with income of £51,000 for example would.

Dividend allowance

As we are already aware, the dividend allowance reduces from £1,000 to £500 on 6 April 2024. Dividend tax rates remain the same at 8.75% in basic rate band, 33.75% in higher rate band and 39.35% in additional rate band (and 39.35% for discretionary trusts).

Arrange your free initial consultation

Capital gains tax (CGT)

Annual exemption reduces from £6,000 to £3,000 on 6 April 2024 (a maximum of £1,500 for discretionary/interest in possession trusts – shared between all settlor’s trusts subject to a minimum of £600 per trust).

CGT rates remain as they currently are apart from the higher CGT rate for residential property gains (the lower rate remains at 18%):

- 10% for any taxable gain that doesn’t fall above the basic rate band when added to income and 20% on any gain (or part of gain) that falls above the basic rate band when added to income

- For residential property gains these rates increase to 18% and 24% (formerly 28%) respectively

- Discretionary/interest in possession trustees and personal representatives pay at the higher rates (20%/24% (formerly 28%))

Simplifications for trusts and estates

From April 2024 trustees and personal representatives of estates will no longer have to report small amounts of income tax to HMRC and taxation of estate beneficiaries will be simplified, as shown below:

- Trusts and estates with income up to £500 will not pay tax on that income as it arises

- The £1,000 standard rate band (effectively basic rate band) for discretionary trusts will no longer apply

- Beneficiaries of UK estates will not pay tax on income distributed to them that is within the £500 limit for the personal representatives

Stamp duty land tax (SDLT)

SDLT Multiple Dwellings Relief is being abolished from 1 June 2024. This applies to purchasers of residential property in England and Northern Ireland who acquire more than one dwelling in a single transaction or linked transactions.

Changes to the taxation of non-doms

The concept of domicile is outdated and incentivises individuals to keep income and gains offshore. The government is therefore modernising the tax system by ending the current rules for non-UK domiciled individuals, or non-doms, from April 2025. A new residence-based regime will take effect from April 2025.

From April 2025, new arrivals, who have a period of 10 years’ consecutive non-residence, will have full tax relief for a 4-year period of subsequent UK tax residence on foreign income and gains (FIG) arising during this 4-year period, during which time this money can be brought to the UK without an additional tax charge.

Existing tax residents, who have been tax resident for fewer than 4 tax years and are eligible for the scheme, will also benefit from the relief until the end of their 4th year of tax residence.

Liability to inheritance tax (IHT) also depends on domicile status and location of assets. Under the current regime, no inheritance tax is due on non-UK assets of non-doms until they have been UK resident for 15 out of the past 20 tax years. The government will consult on the best way to move IHT to a residence-based regime. To provide certainty to affected taxpayers, the treatment of non-UK assets settled into a trust by a non-UK domiciled settlor prior to April 2025 will not change, so these will not be within the scope of the UK IHT regime. Decisions have not yet been taken on the detailed operation of the new system, and the government intends to consult on this in due course.

Furnished holiday lets (FHL)

The FHL tax regime, which relates to short-term rental properties, is to be abolished from April 2025.

Currently, if an individual lets properties that qualify as FHLs:

- The profits count as earnings for pension purposes

- They can claim Capital Gains Tax reliefs for traders (Business Asset Rollover Relief, relief for gifts of business assets and relief for loans to traders)

- They’re entitled to plant and machinery capital allowances for items such as furniture, equipment and fixtures

Raising standards in the tax advice market

A consultation has been issued to discuss the government’s intention to raise standards in the tax advice market through a strengthened regulatory framework. It sets out three possible approaches to strengthening the framework: mandatory membership of a recognised professional body, joint HM Revenue and Customs (HMRC) – industry enforcement, and regulation by a separate statutory government body. The consultation also explores approaches to strengthen the controls on access to HMRC’s services for tax practitioners.

This has relevance to anyone who may receive or provide tax advice or offers services to third parties to assist compliance

with HMRC requirements. For example, accountants, tax advisers, legal professionals, payroll professionals, bookkeepers, insolvency practitioners, financial advisers, customs intermediaries, charities and other voluntary organisations that help people with their tax affairs, software providers, employment agencies, umbrella companies and other intermediaries who arrange for the provision of workers to those who pay for their services, people who engage workers off-payroll, promoters, enablers and facilitators of tax avoidance schemes, professional and regulatory bodies, and clients, or potential clients, of all those listed above.

The consultation runs until 29 May 2024.

VAT

The VAT threshold is increasing from £85,000 to £90,000 from 1 April 2024, the first increase in seven years. See our tax tables 2024/25 for more details. See our tax tables 2024/25 for more details.

If you’d like to discuss any of the changes announced in the Budget or would simply like to explore ways that you can minimise the amount of tax you pay on your wealth, why not get in touch and speak to one of our expert team of advisers. We’re offering anyone with £100,000 in savings, investments or pensions a free financial review worth £500.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Hunt’s politically charged budget

Hunt’s politically charged budget gives the voting public a second National Insurance cut in six months, but will it be enough to save the Tory party in the upcoming General Election?

Chancellor Jeremy Hunt delivered what could be his last Spring Budget (on 6 March 2024), with a further 2% National Insurance cut making the headlines, but there were other measures introduced which could have an impact on your finances. So, what was announced?

Arrange your free initial consultation

National Insurance

Following the 2% National Insurance reduction announced in the Autumn Statement last November, a further 2% National Insurance reduction was announced. This will again affect earnings between £12,570 and £50,270 p.a. and will take effect in April 2024 in the pre-election giveaway that was widely anticipated following speculation in the press. This will save workers up to a further £753 p.a., on top of the up to £753 p.a. saving as a result of the reduction announced in the Autumn Statement.

Child Benefit

It was announced that the High Income Child Benefit Charge (HICBC) will be replaced by a household income based system in April 2026 following a consultation. In the meantime, from April 2024 the threshold above which the HICBC starts to apply on a tapered basis will increase from £50,000 to £60,000 and the top of the taper will increase from £60,000 to £80,000 in a move that Mr Hunt will hope will please working families.

Savings/Investments

Following speculation prior to the Autumn Statement, a British ISA was announced. This will be a further £5,000 tax free ISA allowance for investments into British companies, which will be available in addition to the standard £20,000 ISA allowance.

A new British Savings Bond will also be made available through National Savings and Investments (NS&I), which will offer a fixed rate over three years, though the rate payable has not been announced.

Pensions

Regarding the lifetime allowance, currently 0% and due to be scrapped in April 2024, there were no further changes announced. However, Mr Hunt did not miss the opportunity to reference Labour’s plans to reintroduce the allowance, stating “Ask any Doctor what they think about Labour’s plans to bring it back, and they will say “don’t go back to square one'.”

There were also new rules announced requiring Defined Contribution and Local Government pension funds to disclose how much UK equity exposure they have relative to their international equity exposure. This could prove controversial given the funds’ mandates will be to produce the best risk adjusted return they can for investors, irrespective of their asset allocation.

Property

It was announced that higher rate Capital Gains Tax (CGT) rates on property sales will be reduced from 28% to 24% in April 2024, in a move that the government claims will be revenue generating. The Furnished Holiday Lettings (FHLs) regime will also be abolished.

‘Non-doms’

The current ‘non-dom’ rules, a tax advantageous regime for those who are non-UK domiciled (their ‘permanent home’ is outside the UK), will be replaced by a residency based system from 2025.

Inheritance Tax

After strong rumours that Inheritance Tax would be scrapped before last year’s Autumn Statement, it was not mentioned in the Chancellor’s budget statement.

Conclusion

In what was always going to be a politically charged speech given the proximity to the general election, Chancellor Jeremy Hunt will hope he has done enough to convince voters to give the Conservative Party another term in office in his Spring Budget. In what the Labour Party leader Keir Starmer described as a ‘Last Desperate Act’; the speech was filled with warnings about the potential implications of a future Labour government (the budget speech transcript on the gov.uk website has ‘political content removed’ 27 times!).

However, workers, families, those selling second homes and those already benefitting from last year’s Lifetime Allowance changes may see themselves as in a better position than they were previously, and they could see a future Labour Government as a risk to the longevity of the recently announced changes.

If this is to be the case, there could be a limited opportunity to plan over the next few months. So now is the time to seek advice, to make sure you are doing all you can to protect you and your family’s wealth. If you'd like to learn more about how you can minimise the amount of tax you pay on your wealth, why not get in touch and speak to one of our experts for a free initial consultation or please speak to your adviser if you would like to discuss any of the changes detailed above.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Arrange your free initial consultation

Is the inflation yo-yo and US big-tech distorting investment returns?

As 2024 has started, two key themes have been driving markets. The first is the change in market expectations of the future path of interest rates and the second is the results of the most recent US corporate earnings season. The reason we focus on the US corporate earnings season is the dominance of US markets, which are around 60-70% of the global equity market by market capitalisation.

Arrange your free initial consultation

Interest Rate Expectations

In the fourth quarter of 2023, following a string of monthly inflation data releases that pointed to Central Banks, particularly the US Federal Reserve, imminently achieving their goal of 2% inflation, there was a sharp move in market expectations of interest rate policy. Markets started to expect interest rate cuts to begin in March and continue through the year, culminating in 7 interest rate cuts. Fast forward to the Federal Reserve’s January press conference where Chairman Powell told the press “I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting to identify March is the time to [cut interest rates]”. This language had immediate effect – where markets had expected a 62% probability of a March rate cut before the speech, afterwards markets only assigned an 18% probability. This view was further reinforced by the release of labour market data that points to continued strength in employment, along with the release of December’s US inflation data in which inflation ticked up marginally.

In the UK the picture has been a little more complicated, as markets came into the year far more uncertain over the path of inflation and economic growth in the UK. This is important because Bank of England interest rate policy is set based on minimising inflation and maximising growth, so uncertainty over future inflation and growth makes central bank policy less easily predicted by markets.

Taking inflation first, the UK like the rest of the world has benefitted from the reopening of supply chains and falls in commodity prices previously inflated by Russia’s invasion of Ukraine. Domestically though, inflationary pressures remain high, primarily through high wage growth sustained by a mismatch between the type of job vacancies and the skills of available applicants.

With economic growth, the conundrum is between the ‘hard data’, typically collected by governmental agencies and based on activity that has already happened, like economic growth, and the ‘soft data’, typically survey based and forward looking. The Office for National Statistics (ONS) hard data shows the UK entering a mild recession in 2023 along with sharply declining retail sales in December, however the soft data, such as S&P Global’s Purchasing Managers Index point to UK GDP growth moving up % in 2024 (to an annualised rate of 1-1.5%). Taken together, this had made it difficult for investors to predict how the Bank of England will implement policy through 2024. Fortunately for investors, a great deal of certainty has been gained upon the release of January’s inflation data – prices fell -0.6% from December ‘23 to January ’24, taking the annual figure from January ’23 to January ’24 to 4%. It now appears much more likely that the Bank of England will be able to cut interest rates in the near future given that the inflationary threat appears weaker.

Earnings Season

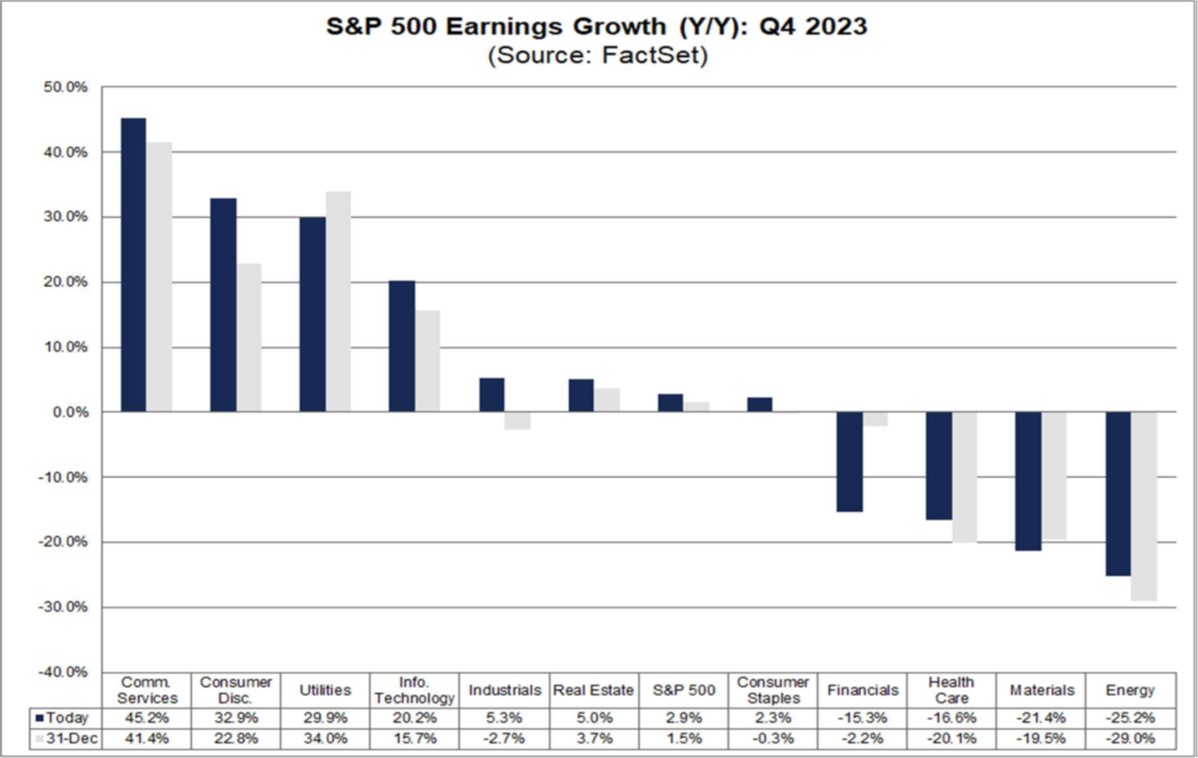

This US earnings season has been a bit of a rollercoaster, starting off weak and rapidly strengthening, leading market sentiment to become increasingly optimistic. Earnings season starts in mid-January with banks and financial firms, who made a poor start and put a negative framing on the season. Following weak earnings releases by cyclical sectors such as energy and basic raw materials these expectations continued. In late January and early February there was a sharp move upwards in aggregate earnings estimates, as the large tech firms (including the so called ‘Magnificent 7’) that comprise 30% of the S&P 500 reported earnings growth far outstripping other sectors. This resulted in an S&P 500 wide earnings growth rate of 2.9%. Conventions over sector can be a little confusing – Amazon and Tesla are classed as Consumer Discretionary businesses, Meta is classed as Communications Services, while Nvidia, Google and Microsoft are in the expected Information Technology sector. This results in the following sectoral earnings growth:

Figure 1 – Sectoral S&P 500 Earnings Growth, Source: FactSet 2024

This will be important when we look at equity market returns by sector.

A quick note on the international picture – European earnings declined at an aggregate level in Q4, US earnings grew 2.9%, while Japanese earnings grew even more rapidly.

Market Reactions

So, how have markets reacted to changes in interest rate expectations and the most recent US corporate earnings season?

Starting with the former, the asset class that had seen the swiftest price gains in November and December was small-cap equities. Small-cap equities have a high sensitivity to interest rate expectations for two reasons, firstly they tend to be more financially fragile and reliant on borrowing at prevailing interest rates, secondly their value often derives from their growth of cashflows far in the future, which is sensitive to interest rates. The result is that small-caps outpaced the wider market as interest rate expectations fell at the end of 2023, but have lagged at the start of this year as interest rate expectations have risen. Government bonds are also sensitive to interest rate expectations, and have seen a similar return profile. Figure 2 below shows the S&P 500 large cap index, MSCI USA Small Cap index and the Bloomberg US Government Bond index over November and December 2023, while the Figure 3 shows those same instruments year-to-date.

Figure 2 – US Small Cap Equity, US Large Cap Equity & US Treasury Bond returns in November and December 2023, Source: FE Analytics 2024.

Figure 2 – US Small Cap Equity, US Large Cap Equity & US Treasury Bond returns in November and December 2023, Source: FE Analytics 2024.

Figure 3 – US Small Cap Equity, US Large Cap Equity & US Treasury Bond returns year-to-date, Source: FE Analytics 2024

Figure 3 – US Small Cap Equity, US Large Cap Equity & US Treasury Bond returns year-to-date, Source: FE Analytics 2024

Now, moving to the effects of the most recent corporate earnings season. The big-tech sectors were the leaders this earnings season, while the cyclical energy and Materials sectors were the laggards. These results have translated through to equity market returns, and have resulted in the big tech names leading the stock market upwards:

Figure 4 – US Sectoral equity returns year-to-date, Source: FE Analytics 2024.

Figure 4 – US Sectoral equity returns year-to-date, Source: FE Analytics 2024.

Similarly, when comparing regional equity markets, Japanese equities have outperformed US equities, which have outperformed European equities. This follows the pattern of regional earnings growth.

Figure 5 – Regional equity returns, Source: FE Analytics 2024.

Figure 5 – Regional equity returns, Source: FE Analytics 2024.

Conclusion

In summary, we came into 2024 with expectations of imminent interest rate cuts, which had driven strong performance in interest rate sensitive assets like small-cap equities and government bonds, however the tempering of these expectations has caused a reversal in these returns. Equity markets have broadly followed the pattern of corporate earnings, inter-regionally this has played out through stronger market returns to regions with stronger earnings growth, and intra-regionally has played out through stronger market returns to sectors with stronger earnings growth.

The pattern of returns described above has been beneficial to our discretionary portfolios, which have an agile asset allocation and have been able to skilfully surf the US tech wave by maintaining an overweight position to these winning names. The discretionary nature of these portfolios also means that exposures can be rapidly changed if the investment thesis changes. Although the asset allocation of our advisory services is, by design, not as nimble, we have positioned them to take advantage of the structural themes that have played out in this most recent corporate earnings season, by adding a structural overweight position to Japanese equities, where we have identified the potential for long-term earnings growth outperformance.

If you would like to speak to your adviser about this, or have any other questions please don’t hesitate to get in touch.

Arrange your free initial consultation

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions.

Past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.

The importance of Cash

There’s no getting away from it, costs have risen exponentially. With a growing cost of living crisis throughout the country, the need for cash retention to act as a buffer in these circumstances remains vital for everyone. This increase in costs will likely mean most people will need to try and save money where they can. Nevertheless, while cash is a crucial component of a well-rounded financial strategy, it's essential to strike a balance. Allocating too much cash for an extended period could expose your wealth to inflation risk, where the purchasing power of your money will decrease over time. It is therefore imperative to assess your overall financial goals, time horizon and risk appetite when deciding how much to keep in cash versus how much to invest in other assets.

There are many reasons to hold money in cash, so we look to explore the importance of cash and its inherent benefits within personal finance, whilst also considering the common risks associated with cash investments. Of course, managing your savings is a highly personalised process, and how much you save should reflect your individual circumstances.

Arrange your free initial consultation

Emergency Fund

The term ‘emergency fund’ or ‘buffer’ refers to money set aside for the sole purpose of being used in times of financial distress. The fund provides a financial safety net to cover any unexpected, and typically costly, expenses that may arise such as those following a loss of job or unexpected tax bill. The amount you should target for an emergency fund depends on a number of factors, including your financial situation, expenses, lifestyle, and debts. Typically, consideration may be given between three to six months of normal expenditure in cash, to be drawn from in the event of an emergency. This is considered a prudent financial practice because it helps avoid unnecessary debt and financial stress.

Top Tip: Starting off small is better than not starting at all!

The Stock Market

While investing in the stock market offers great potential opportunities for accumulating wealth and financial growth, it is important to be aware of the fundamental downsides and risks, and striking the right balance between investments and cash has proven particularly relevant over the past few years with investment markets going through a turbulent time.

Although investors are attracted to the idea of growing their wealth through stock market investments, this should always be looked at as a long-term strategy given the risks associated.

Up until November 2021, there were very few options for your lower risk portion of your wealth, as interest rates were extremely low. However, since the recent interest rate hikes many investors are turning their attention towards setting aside some cash into savings account and are benefiting from some of the highest returns in almost two decades. Unsurprisingly, the last few years have witnessed huge inflows of cash into savings, particularly fixed time deposits, with investors looking elsewhere from the stock market in providing safer and guaranteed returns.

Nonetheless, whilst saving rates have risen, cash has been a depreciating asset, after inflation, with ‘real returns’, remaining negative over the long term. So, for many, it is fundamental to have a comprehensive financial plan in place, to ensure your investment and cash allocations are aligned to meet your objectives and goals.

When it comes to investing, however, one particular benefit of holding some money in cash is managing sequencing risk with your investments. This refers to the impact of the timing of investment returns on a portfolio, particularly when withdrawals are made. If an investor needs to sell assets to cover income or emergency expenses, this can significantly affect the overall portfolio value. As such, the benefit of holding some money in cash is that you help reduce the chances of becoming a forced seller during an investment market downturn. By having this safety measure in place, you can help cover some expected or unexpected expenditure without negatively impacting your long-term investment strategy.

If you are interested in exploring what savings accounts have to offer, please check out our best buy tables, which compares the best accounts on the market.

Retirement

Holding cash as you approach retirement plays a vital role in providing financial flexibility, security and peace of mind when we consider aforementioned risks with invested pension provisions.

As we have covered, sequencing risk can be a major issue for investors. This risk is more common during retirement, as you are far more dependent on your retirement income through your invested pension pots. Significant market downturns alongside taking pension income could be detrimental on your long-term retirement goals, where cash reserves are not in place, as you could be realising losses that could impact the value of your future pension provisions.

Furthermore, healthcare costs are increasingly forming a large part of unexpected costs during retirement. Health spending per person steeply increases after the age of 50, so having cash buffers in place to cover immediate healthcare needs is important.

Using cash in place of drawing from your pension can also have tax benefits, as some pensions sit outside the scope of inheritance tax. This means that the assets held within a pension fund may not be subject to inheritance tax when passed on to beneficiaries. However, given the complexity of inheritance tax laws, it is recommended to seek advice from professionals who have the expertise to guide you through your estate and pension planning.

If you’d like to learn more about how cash can best play a part in your wealth strategy, why not get in touch and speak to one of our experts.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Investment returns are not guaranteed, and you may get back less than you originally invested. Past performance is not a guide to future returns.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning or tax advice.

Savings Champion and their associated services are not regulated by the Financial Conduct Authority (FCA).

The value of professional advice isn't just financial

In an era of instant information and digital connectivity, obtaining financial advice has become more accessible than ever. However, it's important to consider the reliability of your sources, particularly on the internet and from individuals lacking the necessary qualifications and expertise to provide advice. Research by the Financial Service Compensation Scheme (FSCS) revealed that 22% of individuals seek advice from friends, family, or colleagues, 31% turn to online forums or tools, and 9% rely on advice from Social Media Influencers.

Arrange your free initial consultation

While the internet offers a plethora of sources for managing finances, the crucial question remains: is it trustworthy? The easy spread of information on social media and the internet has created a risky environment with unregulated content directing financial decisions. Without regulatory oversight, misleading or inaccurate advice can quickly circulate, posing a potential threat to unsuspecting investors.

Additionally, while seeking advice from close relationships can create a comfortable space for discussing financial matters, it's key to exercise caution. The existing trust and comfort within such relationships may foster a sense of security, but it's equally important to evaluate the individual's expertise. Just as you wouldn't turn to your electrician for medical advice, the same principle should apply to decisions impacting your financial well-being.

The FSCS study further delved into the reasons individuals hesitated to enlist the services of a regulated financial advisor, revealing intriguing insight. Specifically, 23% believed the value of their savings and investments fell short of the amount needed, and 38% expressed concerns about associated costs and value for money. These findings highlight a significant gap in understanding regarding the financial and emotional benefits derived from seeking professional financial advice, contributing to the emergence of the Advice Gap.

The Advice Gap

In the United Kingdom, the Advice Gap refers to a staggering 39 million adults who currently abstain from seeking any form of professional financial advice. Research conducted by the Financial Conduct Authority (FCA) in 2022 sheds light on this issue, revealing that a 60% of individuals with £10,000 or more of investable assets do not consider financial advice, due to the perception that they wouldn't benefit from it. Further insights from the FSCS investigation, revealed interesting thresholds for considering financial advice worthwhile. 13% of respondents believed that a minimum of £100,000 in funds was necessary, while 21% admitted they were uncertain about the financial threshold. This reveals a substantial segment of the population, hesitant to seek advice due to uncertainty about the potential benefits awaiting them.

The real value of Professional Guidance

A study conducted in 2019 by the International Longevity Centre (ILC) in the UK, illuminates the financial impact of seeking professional advice. The research uncovered that those individuals who sought financial guidance during the period from 2001 to 2006, experienced a total wealth boost of £47,706 in their assets over the following decade, compared to those who navigated the financial landscape independently. While the estimated average cost of a one-off independent financial consultation may be approximately £2,000, the benefits accrued over a 10-year period exceed this cost by an impressive 24 times, resulting in a net gain of £4,570 per year. This emphasises that investment in financial advice is essentially an investment in securing a more resilient and prosperous financial future.

The study goes beyond highlighting the importance of a single consultation; it emphasises the significant impact of continuous advice. Individuals who sought financial guidance more than once over the decade, experienced a remarkable 61% improvement in overall financial well-being compared to those who sought advice only once. Achieving financial well-being is not a destination, but a journey. It involves adapting to changing circumstances, making informed decisions, and staying proactive in financial planning. The study's findings highlight the importance of having a trusted advisor who can provide ongoing support, helping individuals navigate the complexities of the financial landscape.

The FSCS study brought to light a common scepticism regarding the minimum asset requirement for benefiting from financial advice. Contrary to the notion that financial advice primarily caters to those with high net worth, the ILC study, mentioned above, demonstrated that individuals who consider themselves in the "just getting by" category experienced a more substantial financial enhancement compared to their wealthier counterparts. For instance, while the affluent group saw an 11% increase in pension wealth, the "just getting by" group experienced an impressive 24% boost in pension income. The key takeaway is quite evident; irrespective of your income level, seeking financial advice can indeed exert a meaningful influence on your financial well-being.

Emotional value of advice

In reference to the ILC study, a whopping 88% of people who have taken advice think it’s good value for money. However, the worth of advice extends beyond financial gains. Amidst the backdrop of market volatility and continuing uncertainty in the political and economic spheres over the past year, it’s good to see that the emotional benefits of advice plays an important role.

A study conducted by Royal London delves into the emotional well-being advantages of seeking advice, revealing that it can offer more than just financial perks. The top three cited benefits include:

- Enhanced confidence in financial plans and the future.

- Heightened control over one's finances.

- Peace of mind and sense of preparedness to navigate life's unforeseen challenges.

Moreover, individuals reported being less anxious about their financial preparedness for retirement, highlighting the emotional impact that sound advice can have at various stages of life.

In conclusion, the studies provided by the FSCS, FCA, ILC and Royal London, paint a compelling picture of the misconceptions around financial advice and the hidden value both for financial and emotional well-being in seeking professional guidance. If you've found yourself questioning the relevance of financial advice in your life, this body of research strongly indicates that taking professional guidance could be a crucial step toward unlocking a more prosperous financial future. So don’t just take our word for it, the research speaks for itself.

If you’d like to learn more about how we can help you achieve the financial future you want, why not get in touch and speak to one our qualified financial advisors for a free initial consultation.

And why not have a look on independent website VouchedFor, to see what our existing clients have to say about us.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Investment returns are not guaranteed, and you may get back less than you originally invested. Past performance is not a guide to future returns.

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax advice.

Stealth tax raid on your wealth

Although many could be forgiven for believing the tax year 23/24 has been a fairly quiet year from a tax perspective, the simple act of freezing tax brackets and freezing or reducing allowances means these are likely to be the biggest tax raising measures since the 1970s. This statement continues to ring true even after taking into account the announcements made in the Autumn Statement back in November. As we now move closer to the Budget, due on the 6th March, with the current government looking at all options to keep them in power in an election year, one thing is for sure, we’re all feeling the effects of stealth taxes. So, will this change?

Arrange your free initial consultation

Stealth tax refers to government policies that increase tax revenue without directly or explicitly labelling them as tax hikes. These taxes often take the form of adjustments to existing taxes and allowances, fees, or other government charges, rather than the introduction of new higher taxes.

The term stealth taxes implies that these changes are designed to be less noticeable to the general public. Bluntly, the Government may look to introduce these less obvious changes, or indeed make no changes at all, so as to avoid criticism, potentially relying on blind siding taxpayers.

However, some would argue that such measures can be necessary for funding government programs and services or indeed paying back the mountain of debt the UK is now faced with, while avoiding public backlash. One thing is certain however, there are currently many different types of stealth taxes, which means few people are immune from paying much more tax now and potentially in the coming years. Even those not normally concerned are starting to sit up and notice; with the impact of fiscal drag on their finances, it’s hard not to feel the pinch.

Latest figures from HM Revenue and Customs (HMRC) show that total tax receipts for April 2023 to November 2023 are £515.9 billion, which is £24.0 billion higher than the same period last year.

In ‘normal’ times the Government has typically pursued a policy to increase tax allowances with the rate of inflation. However back in in 2021 the Government announced plans to freeze allowances and thresholds until 2026. This was later extended to 2028. A clever and rewarding move by the Government. The impact of this is staggering and continues to grow, for example, according to the BBC, simply freezing Income Tax bands until 2028 will create an additional 3.2 million new taxpayers and mean 2.6 million more people will pay higher rate tax. In fact, the Institute for Fiscal studies has stated that by 2027/28 one in eight nurses and one in four teachers will pay higher rate tax.

Even pensioners aren’t immune. According to HMRC an additional 800,000 pensioners will be paying income tax this year due to higher inflation pushing up state pension, which will take many of them over the frozen personal allowance.

Added to this, in the spring Budget early in 2023, the Chancellor announced a reduction in the amount you could earn before paying additional rate tax at 45%. Previously you would have breached the additional rate tax band once your earnings exceeded £150,000 per year, however, from April 2023 it was cut to £125,000, dragging many more people into the additional rate tax net.

Impacts of the Autumn Statement 2023

Following the Autumn Statement delivered by the Chancellor, Jeremy Hunt, in November last year, it should be noted that despite some changes designed to give the public back some money in their pocket, by reducing National Insurance payments, stealth taxes continue to be ever present. My colleague Alex Shields wrote a great article summarising the changes outlined in the Autumn Statement.

The first area of note is the changes to National Insurance (NI) payments - as a result of higher inflation, higher interest rates and frozen tax bands, the Office for Budget Responsibility (OBR) states “Living standards, as measured by real household disposable income per person, are forecast to be 3.5 per cent lower in 2024-25 than their pre-pandemic level.” With this in mind even the 2% reduction for employee NI contributions only results in a £754 p.a. for anyone earning over £50,270, which is a relatively small amount given the increasing day to day costs driven by inflation over the last 12-18 months.

What Stealth Taxes are the biggest earners?

Income Tax Freeze

The stealth tax which is arguably the most prominent and takes in the largest receipts are the income tax bands, which are frozen until 2028. Given that on average UK wages increase year on year, and even more so while inflation rocketed, individuals have been moving up the income tax bands, potentially without realising, just by receiving routine pay increases each year. Some 5.59 million people in the UK currently pay higher rate tax, official HMRC figures show, with an additional 310,000 dragged into it in the year 2022 alone. Over the last few years inflation and interest rates have been in a constant battle in order to try and bring inflation back to its 2% target, while wage inflation had been steadily increasing in the background. Although inflation had been falling in recent months, this month saw a surprise small uptick from 3.90% to 4%, meaning it’s stickier than expected and certainly well above the target 2%, so it’s little wonder that demand from the UK labour force for higher wages continues to increase. This, in tandem, drives up the impact of this particular stealth tax – as wages increase over the frozen income tax bands.

Furthermore, as mentioned above, pensioners received a boost as the Government remained committed to the State Pension triple lock; it was announced in the Autumn Statement 2023 that the full State Pension will be increasing to £11,501 per annum from April 2024. But, this in turn leads to many pensioners having to pay more tax than the year before given the freeze on income tax bands. In fact, those on low pension incomes are in risk of paying tax for the first time as they breach the personal allowance of £12,570. This could squeeze the finances of those pensioners on lower incomes more than they were previously, while also pushing others into a higher tax bracket – pointing to the benefit of ongoing financial planning.

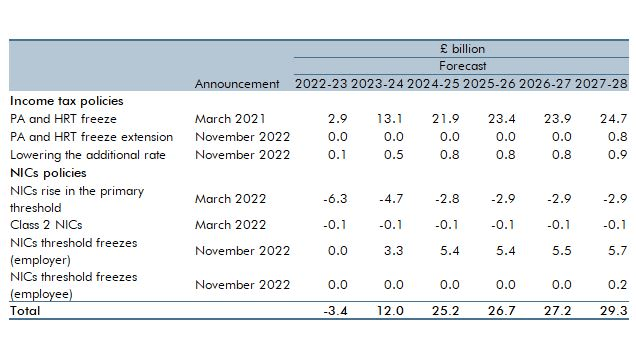

Latest costings of personal tax threshold measures

Source: Office for Budget Responsibility

Savings Allowance Freeze

Another potential stealth tax to be aware of is the tax on savings interest. A basic rate taxpayer can earn up to £1,000 interest outside an ISA without facing a tax bill. This is known as your Personal Savings Allowance (PSA). The allowance is £500 for those paying higher rate tax, and additional rate taxpayers have no allowance at all. Due to very low interest rates in previous years, this tax allowance has been all but forgotten about, with the majority of savers accumulating savings interest tax free.

However, given the Bank of England base rate rose 14 times consecutively from December 2021 in an attempt to combat inflation, cash savings rates became much more attractive as a result (see Savings Champion best buys). Many savers will now accrue significant taxable interest, which in turn takes them over their Personal Savings Allowance and they will therefore need to pay tax.

To put this into context, back in December 2021 a saver could deposit over £133,000 in a best buy account before breaching the basic rate taxpayers PSA. Fast forward to October 2023, when interest rates were peaking, if you saved in the top easy access account, you would breach the PSA on a balance of just over £19,000.

In fact, it’s been reported that the number of people paying tax on their savings income in the 2022/23 tax year has almost doubled to 1.77 million compared to the 0.97 million people the year before. And the amount collected has more than doubled from £1.2 billion to £3.4 billion.

Inheritance Tax

In a similar light to the Income Tax freeze, the Inheritance Tax (IHT) nil rate band (NRB) and residence NRB have also been frozen until 2028. Worst still, however, the current NRB hasn’t changed since 2009, so has remained the same for 14 years. As it stands for the current tax year 2023/24, you will have to pay Inheritance Tax if the value of your estate exceeds £325,000. Anything below this threshold is tax free. Anything above this threshold would be charged at 40%. Those who are passing down their main home to direct descendants are also entitled to an additional allowance of £175,000, known as the residence nil rate band (RNRB), however this allowance actually starts to be withdrawn where the value of the estate exceeds the £2 million taper threshold.

Due to the rising rate of inflation coupled with increasing property values across the UK, the freeze essentially means that a greater number of people will cross the inheritance tax threshold each year, as the value of their total assets have increased, whilst the allowance has remained the same. In the 22/23 tax year a record £7.1 billion in IHT receipts was raised, which was up £1 billion from the previous tax year. With freezing this allowance and estates growing, IHT receipts are expected to increase consistently. In fact, figures from HM Revenue & Customs (HMRC) show a record breaking £2.6bn of inheritance tax receipts were collected in just the 13 weeks between April and July 2023.

The latest figures from HMRC show Inheritance Tax receipts for April 2023 to November 2023 were £5.2 billion, which is £0.4 billion higher than the same period last year.

Why should there be more awareness of these stealth taxes?

Given the current economic climate, it’s wise to ensure your hard-earned money, whether that’s income, investments or savings, are working for you in the most tax efficient way possible. These stealth taxes, if left unattended, will drag on your accumulated and accumulating wealth. The good news is, there are simple ways of mitigating the impact of stealth taxes by being aware of and using the allowances available to you (but be conscious not to creep over them). Moreover, ensuring you are investing, saving, and contributing to tax efficient savings and investments with tax free wrappers will also help to mitigate some of these stealth taxes.

A few examples include:

Use your ISA Allowance

- Saving money into an ISA (the most common being Stocks and Shares or Cash); everyone gets a £20,000 per tax year allowance and any growth within an ISA is totally tax free.

Fund your pension

- If you find yourself entering a new tax bracket, whether that is higher or additional rate, by funding a pension you will receive tax relief at your marginal rate, so are effectively given a tax boost by contributing. For example, a basic rate taxpayer would receive tax relief at 20%, a higher rate by 40% and additional rate by 45%.

- Added to the fact, by contributing to a pension you could even reduce your income as the money is taken at source, so therefore you could change the income tax bracket you fall into.

Watch out for the 60% tax trap

If you earn over £100,000 you begin to lose your personal allowance and could find yourself effectively paying 60% income tax as you lose it – this makes pension funding in this bracket especially attractive.

High Income Child Benefit tax charge

- For parents claiming child benefit, if you or your partner have an income of more than £50,000 a tax charge applies. One way you may avoid the tax charge is if a personal pension contribution is made. If the contribution is enough to reduce your income below £50,000, the High Income Child Benefit tax charge will be avoided.

Use allowances before they are cut

- From 6th April 2024 both the Capital Gains Tax and Dividend Allowance are being halved, £6,000 to £3,000 and £1,000 to £500 respectively.

Whatever side you’re on, working through the political landscape right now can be hard. Therefore, having regular financial planning sessions with a professional independent financial adviser could help mitigate against many of the stealth taxes, so why not get in touch and see how we can help you.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

This article is also based upon our understanding of current law, HM Revenue and Custom's practice, tax rates and exemptions which are subject to change.

Savings Champion and their associated services are not regulated by the Financial Conduct Authority (FCA).

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

A great end to 2023 but will there be a New Year hangover?

This month we take a look at some of the big factors we believe will influence the markets in 2024.

Inflation is falling towards the 2% target, but the risk remains to this aspirational target. In particular, the labour market will need to weaken further, and supply chain disruptions - such as the Red Sea 'crisis', could cause a flare up.

Interest rates are likely to be cut, although markets have been a bit too ambitious with their expectations.

Corporate earnings expectations are too high. Earnings are likely to grow, but it is more likely to be mid-single digits rather than low double digits growth.

Stocks in the US are expensive at an aggregate level, however there is a large divergence between the most and least expensive stocks. Equally, there are large gaps between how expensive the stocks of regional equity markets and sectors are. These differences in valuation could be a source of additional returns to skilled investment managers.

Economic growth will slow down in the US as excess savings - accumulated during Covid times and beyond - are spent. European and UK growth may be buoyed by remaining excess savings. Therefore, growth prospects are likely to converge.

Geopolitics will continue to be a large - and growing - factor. If the world continues to split into factions or spheres of influence then this is likely to increase costs for businesses, which creates an upside risk to inflation.

Arrange a free initial consultation

Inflation outlook remains uncertain despite recent falls

Inflation has declined notably in major economies such as the US and UK over recent months, largely driven by falling goods prices. For example, in the US, goods inflation is near zero whilst services inflation remains sticky around 5%. Chinese export prices have been falling, lowering input costs for companies globally and pulling down inflationary pressures on consumer goods – this has had a large impact and is likely to continue as Chinese industrial production continues to grow rapidly. However, risks remain that inflation may persist. The labour market will need to further weaken to bring down wage growth from around 4%, reducing consumer spending power. Supply chain disruptions also pose an upside risk if shortages re-emerge or shipping lanes are further disrupted, increasing costs.

Currently, US pay growth remains around 4%, enabling higher consumer spending that can drive further price increases. As wages and prices rise in tandem, it creates a self-reinforcing inflationary cycle. Resolving this dynamic requires labour market weakness to lower wage growth momentum. We have seen progress in reducing wage growth, as higher wages have pulled workers into the labour force, increasing the participation ratio, however wage growth of around 3% is more consistent with inflation at the central bank target of 2%, according to JP Morgan.

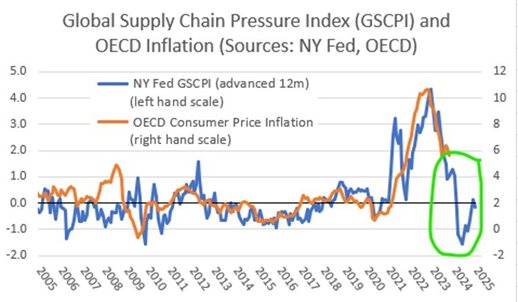

Figure 1: OECD Inflation & NY Fed Global Supply Chain Pressure Index, Source: NY Fed, OECD, 2023.