Skip to main content

Skip to main content

The importance of Cash

There’s no getting away from it, costs have risen exponentially. With a growing cost of living crisis throughout the country, the need for cash retention to act as a buffer in these circumstances remains vital for everyone. This increase in costs will likely mean most people will need to try and save money where they can. Nevertheless, while cash is a crucial component of a well-rounded financial strategy, it's essential to strike a balance. Allocating too much cash for an extended period could expose your wealth to inflation risk, where the purchasing power of your money will decrease over time. It is therefore imperative to assess your overall financial goals, time horizon and risk appetite when deciding how much to keep in cash versus how much to invest in other assets.

There are many reasons to hold money in cash, so we look to explore the importance of cash and its inherent benefits within personal finance, whilst also considering the common risks associated with cash investments. Of course, managing your savings is a highly personalised process, and how much you save should reflect your individual circumstances.

Arrange your free initial consultation

Emergency Fund

The term ‘emergency fund’ or ‘buffer’ refers to money set aside for the sole purpose of being used in times of financial distress. The fund provides a financial safety net to cover any unexpected, and typically costly, expenses that may arise such as those following a loss of job or unexpected tax bill. The amount you should target for an emergency fund depends on a number of factors, including your financial situation, expenses, lifestyle, and debts. Typically, consideration may be given between three to six months of normal expenditure in cash, to be drawn from in the event of an emergency. This is considered a prudent financial practice because it helps avoid unnecessary debt and financial stress.

Top Tip: Starting off small is better than not starting at all!

The Stock Market

While investing in the stock market offers great potential opportunities for accumulating wealth and financial growth, it is important to be aware of the fundamental downsides and risks, and striking the right balance between investments and cash has proven particularly relevant over the past few years with investment markets going through a turbulent time.

Although investors are attracted to the idea of growing their wealth through stock market investments, this should always be looked at as a long-term strategy given the risks associated.

Up until November 2021, there were very few options for your lower risk portion of your wealth, as interest rates were extremely low. However, since the recent interest rate hikes many investors are turning their attention towards setting aside some cash into savings account and are benefiting from some of the highest returns in almost two decades. Unsurprisingly, the last few years have witnessed huge inflows of cash into savings, particularly fixed time deposits, with investors looking elsewhere from the stock market in providing safer and guaranteed returns.

Nonetheless, whilst saving rates have risen, cash has been a depreciating asset, after inflation, with ‘real returns’, remaining negative over the long term. So, for many, it is fundamental to have a comprehensive financial plan in place, to ensure your investment and cash allocations are aligned to meet your objectives and goals.

When it comes to investing, however, one particular benefit of holding some money in cash is managing sequencing risk with your investments. This refers to the impact of the timing of investment returns on a portfolio, particularly when withdrawals are made. If an investor needs to sell assets to cover income or emergency expenses, this can significantly affect the overall portfolio value. As such, the benefit of holding some money in cash is that you help reduce the chances of becoming a forced seller during an investment market downturn. By having this safety measure in place, you can help cover some expected or unexpected expenditure without negatively impacting your long-term investment strategy.

If you are interested in exploring what savings accounts have to offer, please check out our best buy tables, which compares the best accounts on the market.

Retirement

Holding cash as you approach retirement plays a vital role in providing financial flexibility, security and peace of mind when we consider aforementioned risks with invested pension provisions.

As we have covered, sequencing risk can be a major issue for investors. This risk is more common during retirement, as you are far more dependent on your retirement income through your invested pension pots. Significant market downturns alongside taking pension income could be detrimental on your long-term retirement goals, where cash reserves are not in place, as you could be realising losses that could impact the value of your future pension provisions.

Furthermore, healthcare costs are increasingly forming a large part of unexpected costs during retirement. Health spending per person steeply increases after the age of 50, so having cash buffers in place to cover immediate healthcare needs is important.

Using cash in place of drawing from your pension can also have tax benefits, as some pensions sit outside the scope of inheritance tax. This means that the assets held within a pension fund may not be subject to inheritance tax when passed on to beneficiaries. However, given the complexity of inheritance tax laws, it is recommended to seek advice from professionals who have the expertise to guide you through your estate and pension planning.

If you’d like to learn more about how cash can best play a part in your wealth strategy, why not get in touch and speak to one of our experts.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Investment returns are not guaranteed, and you may get back less than you originally invested. Past performance is not a guide to future returns.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning or tax advice.

Savings Champion and their associated services are not regulated by the Financial Conduct Authority (FCA).

The value of professional advice isn't just financial

In an era of instant information and digital connectivity, obtaining financial advice has become more accessible than ever. However, it's important to consider the reliability of your sources, particularly on the internet and from individuals lacking the necessary qualifications and expertise to provide advice. Research by the Financial Service Compensation Scheme (FSCS) revealed that 22% of individuals seek advice from friends, family, or colleagues, 31% turn to online forums or tools, and 9% rely on advice from Social Media Influencers.

Arrange your free initial consultation

While the internet offers a plethora of sources for managing finances, the crucial question remains: is it trustworthy? The easy spread of information on social media and the internet has created a risky environment with unregulated content directing financial decisions. Without regulatory oversight, misleading or inaccurate advice can quickly circulate, posing a potential threat to unsuspecting investors.

Additionally, while seeking advice from close relationships can create a comfortable space for discussing financial matters, it's key to exercise caution. The existing trust and comfort within such relationships may foster a sense of security, but it's equally important to evaluate the individual's expertise. Just as you wouldn't turn to your electrician for medical advice, the same principle should apply to decisions impacting your financial well-being.

The FSCS study further delved into the reasons individuals hesitated to enlist the services of a regulated financial advisor, revealing intriguing insight. Specifically, 23% believed the value of their savings and investments fell short of the amount needed, and 38% expressed concerns about associated costs and value for money. These findings highlight a significant gap in understanding regarding the financial and emotional benefits derived from seeking professional financial advice, contributing to the emergence of the Advice Gap.

The Advice Gap

In the United Kingdom, the Advice Gap refers to a staggering 39 million adults who currently abstain from seeking any form of professional financial advice. Research conducted by the Financial Conduct Authority (FCA) in 2022 sheds light on this issue, revealing that a 60% of individuals with £10,000 or more of investable assets do not consider financial advice, due to the perception that they wouldn't benefit from it. Further insights from the FSCS investigation, revealed interesting thresholds for considering financial advice worthwhile. 13% of respondents believed that a minimum of £100,000 in funds was necessary, while 21% admitted they were uncertain about the financial threshold. This reveals a substantial segment of the population, hesitant to seek advice due to uncertainty about the potential benefits awaiting them.

The real value of Professional Guidance

A study conducted in 2019 by the International Longevity Centre (ILC) in the UK, illuminates the financial impact of seeking professional advice. The research uncovered that those individuals who sought financial guidance during the period from 2001 to 2006, experienced a total wealth boost of £47,706 in their assets over the following decade, compared to those who navigated the financial landscape independently. While the estimated average cost of a one-off independent financial consultation may be approximately £2,000, the benefits accrued over a 10-year period exceed this cost by an impressive 24 times, resulting in a net gain of £4,570 per year. This emphasises that investment in financial advice is essentially an investment in securing a more resilient and prosperous financial future.

The study goes beyond highlighting the importance of a single consultation; it emphasises the significant impact of continuous advice. Individuals who sought financial guidance more than once over the decade, experienced a remarkable 61% improvement in overall financial well-being compared to those who sought advice only once. Achieving financial well-being is not a destination, but a journey. It involves adapting to changing circumstances, making informed decisions, and staying proactive in financial planning. The study's findings highlight the importance of having a trusted advisor who can provide ongoing support, helping individuals navigate the complexities of the financial landscape.

The FSCS study brought to light a common scepticism regarding the minimum asset requirement for benefiting from financial advice. Contrary to the notion that financial advice primarily caters to those with high net worth, the ILC study, mentioned above, demonstrated that individuals who consider themselves in the "just getting by" category experienced a more substantial financial enhancement compared to their wealthier counterparts. For instance, while the affluent group saw an 11% increase in pension wealth, the "just getting by" group experienced an impressive 24% boost in pension income. The key takeaway is quite evident; irrespective of your income level, seeking financial advice can indeed exert a meaningful influence on your financial well-being.

Emotional value of advice

In reference to the ILC study, a whopping 88% of people who have taken advice think it’s good value for money. However, the worth of advice extends beyond financial gains. Amidst the backdrop of market volatility and continuing uncertainty in the political and economic spheres over the past year, it’s good to see that the emotional benefits of advice plays an important role.

A study conducted by Royal London delves into the emotional well-being advantages of seeking advice, revealing that it can offer more than just financial perks. The top three cited benefits include:

- Enhanced confidence in financial plans and the future.

- Heightened control over one's finances.

- Peace of mind and sense of preparedness to navigate life's unforeseen challenges.

Moreover, individuals reported being less anxious about their financial preparedness for retirement, highlighting the emotional impact that sound advice can have at various stages of life.

In conclusion, the studies provided by the FSCS, FCA, ILC and Royal London, paint a compelling picture of the misconceptions around financial advice and the hidden value both for financial and emotional well-being in seeking professional guidance. If you've found yourself questioning the relevance of financial advice in your life, this body of research strongly indicates that taking professional guidance could be a crucial step toward unlocking a more prosperous financial future. So don’t just take our word for it, the research speaks for itself.

If you’d like to learn more about how we can help you achieve the financial future you want, why not get in touch and speak to one our qualified financial advisors for a free initial consultation.

And why not have a look on independent website VouchedFor, to see what our existing clients have to say about us.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Investment returns are not guaranteed, and you may get back less than you originally invested. Past performance is not a guide to future returns.

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax advice.

Who needs to complete a tax return ?

Were you among the 4,757 individuals who completed their tax return on Christmas Day? Or the 12,136 who did so on Boxing Day? Leaving your tax returns to the last minute is unfortunately a common experience for many taxpayers. In the tax year 2020/21, approximately 290,000 individuals incurred fines for late filing and accrued the automatic £100 late filing penalty.

And with more than 1 million people being drawn into self-assessment for the first time due, in the main, to rising inflation and the freeze, by the Government, in many annual allowances until 2028, a larger number of taxpayers are finding themselves at risk of getting hit by the late filing penalties.

Self Assessment Tax Returns

Self Assessment is a system HM Revenue and Customs (HMRC) uses to collect Income Tax.

Tax is usually deducted automatically from wages and pensions known as PAYE (Pay As You Earn). People and businesses with other income must report it in a tax return.

The idea of Self Assessment is that you are responsible for completing a tax return each year if you need to, and for paying any tax due. It is your responsibility to tell HMRC if you think you need to complete a tax return.

If you complete a Self Assessment tax return, you include all your taxable income, and any capital gains. You should also claim any tax allowances or reliefs that you are entitled to on the tax return.

You send the form to HMRC either on paper or online. The information on the tax return is used to calculate your tax liability. This process is called Self Assessment.

What is the deadline for completing a Self Assessment Tax Return?

31st October 2023 - The deadline for submission of tax returns in paper format for the tax year ending 5th April 2023.

30th December 2023 - The deadline to submit your online tax return for automatic payment of owed taxes from your pension and wages.

31st January 2024 - The deadline for online self-assessment tax returns for the 2022/23 tax year to be completed.

For more information about tax dates and thresholds, check out our up-to-date guide.

Who needs to complete a tax return?

According to the gov.uk website, you must send a tax return if, in the previous tax year (6 April to 5 April), any of the following applied:

- You were self-employed as a ‘sole trader’ and earned more than £1,000 (before taking off anything you can claim tax relief on)

- You were a partner in a business partnership

- You had a total taxable income of more than £100,000

- You had to pay the High Income Child Benefit Charge

- You had to pay Capital Gains Tax when you sold or ‘disposed of’ something that increased in value

You may also need to send a tax return if you have any untaxed income, such as:

- Some COVID-19 grant or support payments

- Money from renting out a property

- Tips and commission

- Income from savings, investments and dividends

- Foreign income

What do I need to complete a tax return online?

For those filing online, having a Government Gateway login and a Unique Taxpayer Reference (UTR) number is required. You can find everything you need to know about creating a login on the gov.uk website.

What happens if I don’t complete the self-assessment in time?

If you don’t file your tax return correctly by the deadline, you will be sanctioned with a penalty depending on how late you file your return. This penalty will begin at an initial £100 fixed fee and progress as follows:

- After 3 months, daily penalties of £10 will start, up to £900 in total.

- After 6 months, you will be sanctioned for 5% of the total tax due or £300, whichever is greater.

- After 12 months, you will be sanctioned for a further 5% of the total tax due or £300, whichever is greater - in some cases, you may have to pay 100% of the tax you owe

Additionally, the interest rate that HMRC charges on unpaid tax recently rose to the highest it has been in 14 years. The amount is calculated as the base rate plus 2.5% - so currently this is a rate of 7.75%. This is in contrast to the interest rate paid to those that are owed money by HMRC, they will only apply the base rate minus 1% (4.25%), known as the repayment interest rate.

Late filing isn't the only trigger for penalties. Failure to pay the owed tax on time will result in further penalties. In that 2020/21 tax year, 1.43 million people faced fines for overdue payments, up from 1.24 million the previous year. Interestingly, despite HMRC granting a one-month waiver for late filing and payment penalties that year, due to the challenges posed by the Covid-19 pandemic, the numbers continued to rise.

However, seeking assistance over the phone might prove challenging. HMRC announced in January 2024 that it would focus on addressing priority calls leading up to the months end, with reported waiting times increasing from 5 minutes in 2017 to 20 minutes in 2022. Many callers have faced prolonged persistence to connect with the right person for assistance, despite generally positive experiences once contact was established.

That said, HMRC has made it clear that for those that can demonstrate a genuine reason why they cannot make the deadline, they will be ‘lenient’ in their penalty process. The penalties mainly exist to punish deliberate tax evaders and those who persistently fail to complete their tax returns.

There are many ways you can minimise the tax you pay, with some taxes mitigated altogether. For those with higher earnings, check out our free guide on tax planning strategies. Alternatively, give us a call on 0333 323 9065 to book a free non-committal initial consultation with a member of our team to find out how we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Tax return deadline looms - avoid a fine!

Were you one of the 4,757 people that filed their tax return on Christmas Day? Or the 12,136 that filed on Boxing Day? It may seem extreme to be doing your tax return over the festive period, but for those diligent people the chore is done for another year – and they have avoided the stress of leaving it too late and risking an automatic penalty of £100. In the 2020/21 tax year around 290,000 were fined.

And it’s not just late filing that can see you paying a penalty. You also have to pay the tax due! In that same tax year a further 1.43 million people were fined for not paying up on time, up from 1.24 million the year before. And that was despite the fact that HMRC waived the late filing and late payment penalties by one month that year, in recognition of the pressures caused by the Covid-19 pandemic.

HMRC has announced that it will only be dealing with priority calls in the lead up to the end of the month, as according to The Times, waiting times to speak to someone for assistance have soared from 5 minutes in 2017 to 20 minutes in 2022.

Who has to send in a tax return

Apparently more than 1 million people will have been drawn into self-assessment for the first time due to the increase in taxes due on everything from savings and dividends to capital gains, because of the freeze in many allowances that was introduced in 2021 and it set to continue until 2028.

And some people could be first timers if the increase to their income, including the State Pension, pushes their income over £100,000.* But there could be other situations too, so, you might be surprised to find that you do need to file a self-assessment tax return.

As there are so many more who may need to do a self-assessment tax return, it could be wise to check if you need to send a tax return if you’re not sure.

According to the gov.uk website, you must send a tax return if, in the last tax year (6 April to 5 April), any of the following applied:

- you were self-employed as a ‘sole trader’ and earned more than £1,000 (before taking off anything you can claim tax relief on)

- you were a partner in a business partnership

- you had a total taxable income of more than £100,000

- you had to pay the High Income Child Benefit Charge

You may also need to send a tax return if you have any untaxed income, such as:

- some COVID-19 grant or support payments

- money from renting out a property

- tips and commission

- income from savings, investments and dividends

- foreign income

What do you need if you have to file a tax return?

If you are filing online you’ll need to have a login to the Government Gateway and you’ll need your Unique Taxpayer Reference (UTR) number.

More information is available on gov.uk, so this is a great reference point especially if you don’t yet have a Government Gateway account. But you really need to get a move on if you want to avoid a penalty.

Remember that HMRC will charge interest on these fines and any unpaid tax and the amount is calculated as base rate plus 2.5% - so currently this is 7.75%. This is bad enough, but if HMRC owes you money because you have overpaid tax, they will only apply base rate minus 1% (4.25%), known as the repayment interest rate! Even more of a reason to make sure you pay up on time and accurately.

*Source: gov.uk

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Managing the cost of care for you and your family

As a nation we are living longer. According to the Office for National Statistics (ONS) in 2010 there were 4.9 million people aged over 75, fast forward 10 years and this has grown by a huge 24%, to 6.1 million in 2020. The need, therefore, for some form of care in later life is a real fear among most families which is only growing. This fear comes from not only losing your independence but also losing the legacy you may have planned to pass to your loved ones.

Arrange your free initial consultation

A scary fact to add to this concern is the total beds available in care homes as a proportion of the population is decreasing. In 2012 there were 11.3 beds in care homes available per 100 people for those over age 75. Over a 10-year period this has reduced to 9.4 beds per 100 over age 75, this is a 17% decrease.

In a time where emotions are high as well as stress being overwhelming, the last thing you need to worry about is whether your finances are working in the best way for you so you can afford the care you want or need. Taking the time to appropriately plan for potential care costs in good time will remove this financial worry, allowing you to focus on the health and wellbeing of you and your family.

In terms of planning for care costs, a good place to start is to understand what these costs may look like.

Costs of care today

There is a common misconception that the state will pay for your long-term care. However, in reality only a few people will meet the eligibility criteria which prevents them paying the costs of care themselves.

In 2023 the average cost for residential care in the UK was is £1,078 per week (£56,056 per year), according to the AgeUK Charity. However, figures will vary significantly depending on your location and the individual circumstances surrounding your care requirements. The first step in your plan would be to research care homes around you and what the typical costs for these are. In most cases, the preferred care home isn’t based on cost but on the distance from family members, so costs can sometimes be unexpectedly high.

For the current tax year 2023/24, in England, you currently need to be below the savings threshold of £23,250 in savings and/or assets before part of the cost of care will be covered by the state and below £14,250 before all costs are paid (£28,500 in Scotland, £50,000 in Wales and £23,250 in Northern Ireland). This limit includes the value of your home unless you have a spouse or dependent occupying the property. This limit has not been increased to take into account the effects of inflation over the years, therefore fewer individuals are able to benefit from state support each year.

If your assets are above these limits, then you will need to fund your care costs personally, which may even include your home.

What is the social care cap?

It is not all bad news, in 2021 the UK government proposed a price cap on care costs of £86,000, known as the ‘social care cap’, meaning this will be the maximum an individual would pay towards their care costs in their lifetime. The cap was originally due to come into effect as of October 1st, 2023, but has been postponed to October 2025 following Jeremy Hunt’s Autumn statement of 2023. Of course, with the prospect of a changing government on the horizon it’s easy to see that a lot could happen before the postpone social care gap would be implemented.

Although there is the care cap this only covers the care costs, if you were to be in a residential care home you would still be liable to pay additional costs such as ‘hotel’ costs and luxury costs.

Building your plan

If you’ve identified that you will need to pay for care or you’d like to plan for the possibility and you’ve researched to understand what the costs look like in your area, you’re half way there in terms of building your plan. The next step is ensuring your current savings, investments and pensions are working hard and tax efficiently for you to ensure you have the best chances to meet this expense.

If you are retiring and planning for care costs is important to you, a common mistake most individuals make is holding too much wealth as cash in your bank account. Although cash is very safe and won’t, in theory, go down in value, interest rates on bank accounts have historically been lower than inflation. Therefore, your wealth could be deteriorating in real terms. It is important to have a conversation with a financial adviser to build an initial plan and check if the overall assets you are holding are appropriate.

If you are much closer to needing care, it is still important to plan the potential expenses out. This will help you to understand how long you would be able to sustain care costs until your wealth is below the threshold for the council to start making contributions. For a short-term solution, your plan may focus around cash accounts, which although may not provide the best return year on year, will provide certainty and peace of mind in the short term.

If you are in a position where the majority of your wealth is locked away in your home, and you are single and living alone, this will keep you above the threshold. In this situation you will likely need to use this wealth in some way to cover the costs. You will have a few options open to you, which include:

-

Renting the house out.

-

Taking out a mortgage or equity release.

-

Have the council take the costs from the house (typically on death).

-

Selling your home outright.

Each of these options presents potential benefits and drawbacks. For example, selling your home may provide you with a lump sum of cash that you can put towards care costs. However, you may lose your Residence Nil Rate Band (RNRB) on your property, which is an increase to the threshold for inheritance tax. Therefore, it’s important to assess each in turn and discuss with a financial professional.

At The Private Office we look at your overall financial picture and discuss what is important to you. Our first step is to always build your bespoke financial plan, which will include potential care costs, and how you may be able to pay for these.

To understand the features and risks of equity release, please ask for a personalised illustration.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning or tax advice.

How to make your child a millionaire before 40!

Most parents would like to ensure their children have a strong financial footing when they are older, but don’t always know the best way to do this. There are many ways to support your children financially throughout their lifetime, but what if there was a way to make them a millionaire before they even reached retirement age? Here we look at the best ways to put money aside for your children and how you can maximise the benefits of compound interest to make your child a “millionaire”!

Arrange your free initial consultation

The first step to saving for your children’s future is understanding your saving options. Here are the most common options that benefit from tax-free growth:

Junior ISA(JISA)

From the day a child is born you can put money into a JISA for them. The current contribution limit is £9,000 per tax year (or £750 per month) and you have the choice of a Junior Investment ISA or a Junior Cash ISA. The most important benefit of a JISA is that any gains made, or interest earned will be tax-free!

If we assume you receive an average annual net return of 5% per year and you save the maximum of £9,000 every tax year, from the day your child is born until they turn 18, you will have contributed a total of £162,000 to their account. However, due to the magic of compound interest (where you earn interest on interest), they will have a pot of over £265,000 saved in a tax-efficient wrapper, what a great 18th birthday present!

At their 18th birthday they can transfer their JISA into an Adult ISA to continue to receive tax-free interest/ investment returns.

Junior Self-Invested Personal Pension (Junior SIPP)

Setting up a pension up for your children may seem like you are overly preparing but this can actually give your children a significant head start. The maximum you can currently save into a Junior SIPP is £2,880 per tax year, and the UK government will add tax 20% tax relief of £720 per tax year, which would bring the total contribution to £3,600. If you can contribute to your child’s Junior SIPP for 18 years and again assuming a 5% growth rate, you will have contributed £51,840 but their pension pot will be worth £106,340 due to the added tax relief. If your child doesn’t contribute to the pension again, by age 57* they could have a pension pot worth around £712,986. Similar to the JISA, any gains made within the SIPP are exempt from tax, and based on current pension rules, you can take up to 25% as a tax-free lump sum upon reaching retirement age.

Recent statistics released by the Office for National Statistics (ONS) stated how the average pension wealth for all persons in the UK is £67,800 at age 57*, highlighting how starting to save early can set your child up for their future and give them a greater opportunity in retirement or even to retire early.

How to make your child a millionaire!

And this is how to do it! If you do the following and assume a 5% growth rate per annum:

- Open a JISA before your child’s first birthday and contribute £9,000 every year until age 18. This results in a total contribution of £162,000 (18 years x £9,000).

- Open a Junior SIPP before your child’s first birthday and contribute £3,600 (including tax relief) to the Junior SIPP every year up to their 18th birthday. This totals 18 years x £2,880 (or £3,600 with tax relief) which equals £51,840 (£64,800)

This would mean you will have contributed a total of £226,800 (including tax relief) to the JISA (£162,000), and Junior SIPP (£64,800). At age 18 when you stop contributing, they could have a total net worth of £372,191 when taking into account compound interest and growth. If they leave this money invested and continue to achieve 5% per year growth, by age 39 they could have a total net worth of just over £1million (£1,036,911), although the funds in the pension would not be accessible until age 57*.

At that point the pension fund could have grown to £712,986, while the ISA, could be worth £1,782,465 if it remained untouched too - an extraordinary total of almost £2.5m. That is a gift worth giving.

The power of starting to save early

Using the same assumptions as above, with a 5% annual growth rate and maximising both Junior SIPP and JISA contributions until age 18:

| Starting from date of birth | Starting at age 5 | Starting at age 10 | |

|---|---|---|---|

| JISA Value at age 30 | £477,430 | £300,604 | £162,056 |

| Junior SIPP value at age 30 | £190,972 | £120,242 | £64,823 |

| Total Value at age 30 | £668,402 | £420,846 | £226,879 |

This shows the benefits you can provide by starting the process of saving early for your child through compounding the interest or investment returns. This is a representation of how you can save for your children and assumes maximum contributions are made at each birthday, but we understand the circumstances for each parent and child will be different and may require different forms of financial planning, such as monthly contributions instead of lump sums.

Despite the examples above, it is never too late to start. If you would like to understand how, The Private Office can structure savings and investments for you and your children to help provide the whole family with a strong financial future. So why not get in touch for a free initial consultation.

* Based on current pension regulation, where the normal minimum pension age is increasing to age 57 from April 2028.

If you would like to know more about this topic, one of our Partners Kirsty Stone appeared on BBC Radio 4 Money Box live, giving her suggestions in a programme all about saving for children.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

All the calculations in this article assume that lump sum contributions are made for 18 years, from birth, unless otherwise stated, to the 17th birthday and are not adjusted for inflation.

The Financial Conduct Authority (FCA) does not regulate tax or cash advice.

The growth rates provided are for illustrative purposes only. Investment returns can fall as well as rise and are not guaranteed. You may get back less than you originally invested. Investments may be subject to advice fees and product charges which will impact the overall level of return you achieve.

Autumn Statement – what the announcements mean for your finances

Chancellor Jeremy Hunt promised to ‘reduce debt, cut taxes and reward work’ in his ‘Autumn Statement for growth’, but what might the changes he announced mean for your personal finances?

In the lead up to the Autumn Statement, we discussed the changes that were rumoured to have been announced in this article.

Arrange your free initial consultation

These speculated changes included:

- Reducing Inheritance tax

- Announcing an additional ISA allowance for investment into UK companies

- Changing the state pension triple lock calculation to limit next year’s state pension increase

In the end, none of these changes were introduced, with shadow chancellor Rachel Reeves claiming Hunt wanted to reduce inheritance tax but that he “couldn’t get away with it in the middle of a cost of living crisis”. Instead, the headline grabbing change was the 2% reduction to employee national insurance contributions between £12,571 and £50,271. This will equate to an annual saving of c. £754 p.a. to those earning over £50,270 p.a. with effect from January 2024. Additionally, there were National Insurance reductions for the self-employed, with Class 2 contributions effectively abolished and Class 4 contributions reduced from 9% to 8% between £12,571 and £50,271 with effect from April 2024.

However, this will only go part of the way to make up for the impact of the continued freezing of the income tax bands, which will remain frozen until 2028. Indeed, as a result of higher inflation, higher interest rates and frozen tax bands, the Office for Budget Responsibility (OBR) states “Living standards, as measured by real household disposable income per person, are forecast to be 3.5 per cent lower in 2024-25 than their pre-pandemic level.”

Separately, the speculated ISA allowance increase for investments into UK companies did not materialise and pensioners will be pleased to hear Mr Hunt state the government will “honour our commitment in full” as the state pension rises by 8.5% next year.

Regarding pensions, workers will hope a new legal right for their new employer to pay into their previous defined contribution pension scheme will simplify pension planning going forward and will mean an end to the accumulation of multiple schemes as individuals move between companies.

This was an Autumn Statement with half an eye on an upcoming general election, with announcements that should put more money in the pockets of workers and pensioners alike. Mr Hunt repeatedly referred to the OBR’s forecasts during his announcement as he tried to rebuild credibility, a little over a year after Liz Truss and Kwasi Kwarteng’s ‘mini-budget’, prior to which the OBR was not asked to run forecasts. Overall, Mr Hunt will have been grateful that he was able to use some of the fiscal headroom provided by then Chancellor, now Prime Minister, Rishi Sunak’s decision to freeze income tax bands back in 2021 to offer a national insurance cut and significant state pension rise to the voting public.

Arrange your free initial consultation

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

Inheritance tax planning – Strategies to protect your wealth

Former Labour Chancellor, Roy Jenkins, famously described Inheritance Tax (IHT) as a “voluntary levy paid by those who distrust their heirs more than they dislike the Inland Revenue”. While that statement may divide opinion, there is no doubt methods exist in order to mitigate or avoid completely an IHT liability on your estate on death.

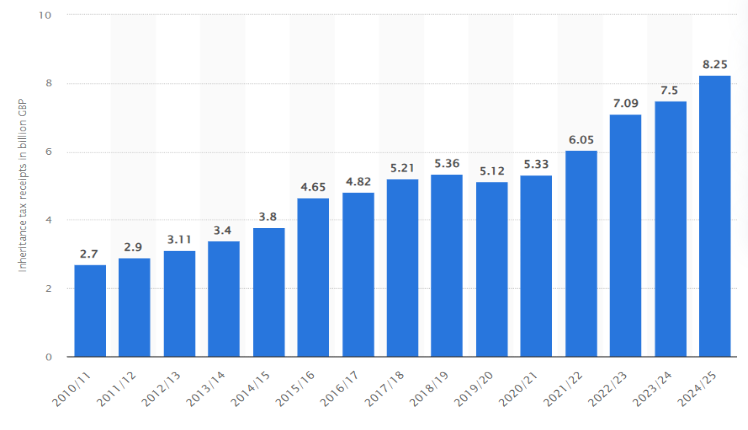

Inheritance tax receipts

IHT receipts in the UK amounted to £8.25bn in the 2024/25 tax year, a staggering increase of over £700m from the previous tax year which was a previous peak.

Figure 1 - Inheritance tax Receipts 2020-2025, Source: Statista

This can be in part attributed to a ‘stealth tax raid’ from the Government, as allowances have been frozen for a number of years, with the chancellor, Rachel Reeves, also announcing in her Autumn Budget last year that the current IHT thresholds would be frozen until at least April 2031.

Currently, the ‘nil rate band’ allows you to pass on £325,000 of your estate without paying IHT, and an additional ‘residence nil rate band’ of £175,000 is potentially available if your main residence is passed on to direct descendants, giving an IHT allowance of £500,000 per individual or £1m for a married couple/ civil partners. Any value of your estate above these thresholds will typically be subject to IHT at 40% (as noted in more detail below, the latter allowance can be tapered if your estate value exceeds £2m).

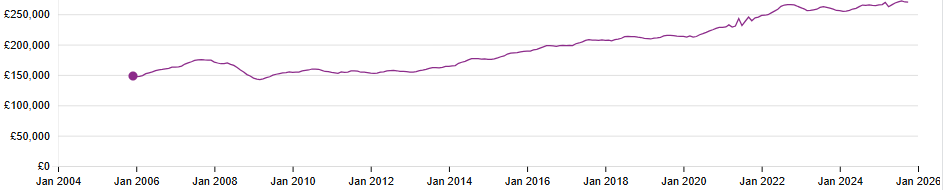

Although an IHT-free threshold of £1m may seem quite generous, the number of people caught in the IHT net has been increasing for several years, due in the main to the rapid increase in property prices. In the 20 years running up to October 2025, which is the latest stats from the Land Registry, the average UK house price has almost doubled to nearly £270,000.

Figure 2 - Average price by property in UK, Source: Land Registry

The residence nil rate band taper

Inheritance tax planning becomes increasingly valuable for estates exceeding £2 million, where the potential tax savings can be most significant. For every £2 of your estate value over £2m, the residence nil rate band is reduced by £1. Therefore, the full residence nil rate band is lost if the value of your estate exceeds £2.35m for an individual or £2.7m for a married couple.

What this means in practice is that for a married couple with an estate value of £2.7m the IHT-free allowance can be reduced from £1m down to £650,000, potentially resulting in an additional IHT liability of up to £140,000 (£350,000 @ 40% IHT) due to the loss of this valuable additional allowance.

What can I do to reduce my Inheritance tax bill?

Whilst inheritance tax planning can take the form of complex trust arrangements where appropriate, below are some of the key IHT mitigation strategies to consider:

Spend more – an often overlooked but simple and effective method of reducing the value of your estate, which you will also hopefully get some personal enjoyment from!

Gifting – as shown below, there are certain types of gifts that will fall outside of your estate immediately for IHT purposes. Any gifts that are not immediately tax exempt or within the annual allowances are treated as either potentially exempt transfers (PETs) or chargeable lifetime transfers (CLTs). PETs allow you to make gifts of unlimited value which will be exempt from IHT if you survive for a period of 7 years, subject to the 14 year rule not applying. If you don’t survive the gift by 7 years, the PET becomes chargeable and is added to the value of your estate.

Certain gifts, most commonly gifts into trust, may instead be treated as CLTs and could give rise to an immediate IHT charge, depending on the circumstances. Specific rules may apply to any gifts made into trusts. Please do get in touch if you require information in this regard.

IHT gifting strategies

Annual gifts

Individuals can give up to £3,000 each tax year free of inheritance tax, and any unused allowance from the previous year can be carried forward one year, allowing up to £6,000 to be gifted in a single year.

Small gifts

You can give as many gifts of up to £250 per person each year, provided each recipient is different. These small gifts are separate from and additional to the annual £3,000 exemption. However, they can't be in addition to the £3,000 given to one individual.

Wedding gifts

Certain gifts made in anticipation of a wedding or civil partnership are exempt. The limit is:

- £5,000 to a child

- £2,500 to a grandchild or great-grandchild

- £1,000 to any other person.

Gifts from income

Regular gifts can be made from surplus income without triggering inheritance tax, as long as these payments are genuinely from income rather than capital and do not reduce your normal standard of living. They must also form a pattern.

Gifts to charities and political parties

Gifts to registered charities and qualifying political parties are free from inheritance tax, whether made during your lifetime or on death.

Lifetime gifts

Gifts that do not fall under a specific exemption are treated as potentially exempt transfers or a chargeable lifetime transfer (CLT). These may become fully exempt if you survive seven years, but they can be brought into account if death occurs within that period.

How to reduce your IHT rate from 40% to 36%

Another benefit of gifting to charity is if 10% of your net estate (i.e. the value of your estate above the tax-free allowances) is gifted to charity on death, the rate at which IHT is charged on your taxable estate falls from 40% to 36%. This can significantly reduce any ‘cost’ of a gift to charity and ultimately the amount of your estate that is paid to the taxman.

Life insurance to reduce IHT

Set up a life insurance policy – although not mitigating IHT, a life insurance policy can ensure that your beneficiaries have sufficient capital to cover the IHT liability. It is important to consider writing the policy in trust, so it doesn’t form part of your estate and the payment on death is accessible for your beneficiaries prior to any required IHT payment.

Investing in business relief assets to reduce IHT

Invest in Business Relief (BR) assets- originally designed to allow family businesses to be passed through generations without the need to be sold or broken up to meet an IHT liability, Business Relief can apply to certain qualifying investments, such as shares in unquoted qualifying companies. While most lifetime gifts are subject to the seven‑year rule, qualifying Business Relief assets can be transferred free of IHT once they have been owned by the donor for at least two years.

There are two tax points for IHT that the donor should be aware of on a gift of Business Relief assets. One is at the point of making a gift and the other is at the point of death of the donor, if death occurs within seven years of the gift. The gift of BR shares should provide relief from IHT, provided they were held for at least two years. It is important to note that once an asset has been gifted, control over that asset cannot be retained by the donor. On death, the recipient needs to hold the shares for seven years or, if earlier, at the time the donor dies, for the gift to continue to provide relief from IHT in the donor’s estate. If the recipient disposes of the shares before the donor’s death or before seven years have elapsed, the relief may be lost and the value could become subject to IHT in the donor’s estate.

From April 2026, the combined allowance for Business and Agricultural Property Relief will be capped at £2.5 million per individual (transferable between spouses), with any excess qualifying for relief at 50%. This allowance will refresh every seven years for lifetime gifts and will be indexed to CPI from 2031. In addition, unquoted shares listed on recognised exchanges such as AIM will only qualify for 50% relief under the new rules.

These types of assets are however typically very high risk and can be difficult to sell, hence should be approached with caution. Therefore, this will not be appropriate for all clients.

Changes in pension legislation

One of the most significant recent changes in the IHT space is the change in pension regulation, expected to come into force from 2027. From 6th April 2027, the Government is planning a significant shift in how pensions are treated for IHT. Under the new rules, most unused pension pots and death benefits will count as part of your estate, meaning they could be taxed at up to 40% if they push the total value of your estate over your available thresholds. This is a significant change from current treatment, where pensions have generally been exempt from IHT and therefore used as an estate‑planning tool.

Looking ahead, pensions will play a much bigger role in estate planning than before. With upcoming changes to the IHT rules, it is important to review how your pension fits into your overall strategy. This could open up new opportunities to protect wealth, manage tax efficiently, and ensure your assets are passed on in the way you intend

With these changes in mind, it is important to keep pension funding as a key part of your wealth building strategy before retirement. Pensions don’t just help you prepare for later life, they also provide valuable tax advantages, such as tax relief on contributions and tax efficient growth. Making the most of these benefits now can give you greater flexibility and security in the future. What’s more, recent changes have made pensions even more attractive as the standard annual allowance for contributions has increased from £40,000 to £60,000, and the lifetime allowance has been removed, giving you more scope to invest for the long term.

Can I just gift my main residence to my children?

In simple terms, no. If you continue to live in the property after the gift was made, this will be treated as a ‘gift with reservation of benefit’ and the property would remain in your estate. In order for this strategy to be effective, you would need to pay your children the full market rate rent after gifting the property to them, which can result in additional tax consequences.

How we can help

A starting point for estate planning is ensuring you have a valid Will in place. This will ensure that your estate is distributed as per your wishes and could reduce the potential IHT liability payable on your death.

Thereafter, whilst mitigating IHT may seem like a key objective, a balance needs to be struck between tax efficiency and retaining sufficient assets to meet your own needs in later life.

One method in which we can assess the viability of different IHT mitigation methods is through cash flow modelling, whereby your financial future is mapped out so you can see what wealth you need for the life you want, so why not get in touch today to arrange a free no obligation initial discussion with one of our expert advisers

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

This article is also based upon our understanding of current law, HM Revenue and Custom's practice, tax rates and exemptions which are subject to change.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, will writing, tax or trust advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Gifting to charity and reducing your Inheritance tax bill? It’s a win-win!

There is no denying the charity sector is feeling the strain. Running costs, declining government support and demand for services are rising, while disposable incomes are being squeezed by increasing taxes, frozen allowances and an uncertain economic climate.

As a result, organisations are being forced to think differently about how they raise money in the current climate. Some are placing a greater emphasis on “legacy fundraising” i.e. when someone designates part of their estate to a chosen charity in their will. Nevertheless, this method of fundraising could face future challenges.

Additionally, multiple news outlets are reporting that Prime Minister Keir Starmer is considering plans to increase inheritance tax revenue by tightening rules around the gifting of assets, among other suggestions, at the next budget. This could mean that charitable tax incentives would become less prominent as a way to mitigate tax for high-value estates, which could have an impact on the number of people who leave assets to charity in their will. While we await the outcome of the impending budget, for now, those looking to minimise their tax bill while doing good for the world have a golden opportunity.

Arrange your free initial consultation

How can I reduce Inheritance tax by giving to charity?

Currently, gifts to registered charities are exempt from inheritance tax (IHT). This can either be done through donating during your lifetime, or on death through your will.

As a reminder, everyone has a ‘nil rate band’ exemption for IHT, (currently at £325,000 per person). Furthermore, if you are passing your main residence to your direct descendants, you can also benefit from an additional exemption of up to £175,000 – this is known as the “residence nil rate band”.

Case Study 1 Example:

Mr A has an estate valued at £550,000 including a £300,000 main residence that he is planning to pass on to his children. He also utilises his annual gifting allowance every tax year. As a result, Mr A will benefit from £500,000 of allowances, as per below:

- £325,000 nil rate band

- £175,000 residence nil rate band

The excess (i.e. £50,000) would ordinarily be taxed at 40%, leading to a £20,000 tax liability. However, if Mr A left £50,000 to charity, his estate (now £500,000) would fall within the respective nil rate bands, which means there would be no inheritance tax to pay.

Bequeath on death

Further to the above, you also have the potential to reduce the rate of inheritance tax to 36% if you leave at least 10% of your net estate to charity. This is typically achieved by leaving a charitable gift via your will.

The net estate "baseline amount" is calculated by deducting IHT exemptions, reliefs and nil-rate band from the total estate value (however this does not include the deduction of the residence nil-rate band).

If the value of the gift is at least 10% of the "baseline amount", the reduced 36% rate of inheritance tax will be applicable.

You could also consider a charitable trust; gifts to charities placed in trust are free of IHT.

Case Study 2 Example:

Ms B has an estate valued at £1,000,000 including a £400,000 main residence that she is planning to pass on to her children. She also utilises her annual gifting allowance every tax year and was planning to leave £40,000 of her estate to charity.

To keep things simple, we are going to assume that she has her full nil rate band and residence nil rate band, as per Case Study 1.

This means we would calculate Ms B’s inheritance tax liability as follows:

| Estate | £1,000,000 |

| Net estate/ baseline value (Estate - NRB) taxable estate | £675,000 |

| Charitable gift | (£40,000) |

As the value of gift is below 10% of the baseline value (£67,500), IHT will be chargeable at 40%.

| Estate | £1,000,000 |

| Less nil rate band & residence nil-rate band | (£500,000) |

| Less Charitable gift | (£40,000) |

| Tax to be calculated using... | £460,000 |

| IHT @40% | (£184,000) |

| Distribution to MS B's beneficiaries | £776,000 |

Nevertheless, if Mrs B gifted 10% of her net estate (calculated at £67,500 - detailed above) instead of £40,000, it would have the following impact:

| Estate | £1,000,000 |

| Less nil rate band and residence nil rate band | (£500,000) |

| Less Charitable gift | (£67,500) |

| Tax to be calculated using... | £432,500 |

| IHT @ 36% | (£155,700) |

| Distribution to Ms B’s beneficiaries | £776,800 |

As shown above, the planning in this scenario has not only slightly increased the amount the beneficiaries receive, but also the charity has received a further £27,500. This represents a win-win situation for both parties.

Can I pay a lower rate of inheritance tax after someone has died?

This may be possible through a Deed of Variation. This is a legal document that allows the distribution of the estate to be altered by the named beneficiaries in the will.

A Deed of Variation can be used to re-direct 10% of the net estate to charity, which means the estate would pay a reduced rate of inheritance tax (36%).

A Deed of Variation needs to be carried out within two years from the date of death for it to be effective from a tax perspective. Furthermore, the relevant paperwork must be signed by all executors and the beneficiaries who may be disadvantaged because of the change.

To help you visualise these numbers, we've put together this Inheritance Tax calculator:

For individuals with large estates, our specialist high-net-worth financial advisers can integrate charitable giving into an overall tax minimisation strategy

If you are concerned about inheritance tax, or how this relates to charitable giving, why not get in touch with The Private Office and give us a call on 0333 323 9065 or book a free non-committal initial consultation.

Arrange your free initial consultation

This article is for information only and does not constitute individual advice. The information provided in this article is based on the current allowances and legislation and is subject to change.

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

Increasing reliance on the Bank of Mum and Dad & the Bank of Gran and Grandad!

The financial support provided by parents and grandparents has long played a role in family life, but in recent years, it has become almost essential in defining the financial future of younger family members of and the wider economy. Dubbed the ‘Bank of Mum and Dad’, this intergenerational flow of wealth is increasingly crucial in helping younger people buy their first homes, fund their education, and establish financial security.

As house prices have surged far beyond wage growth, saving for a deposit has become an uphill battle. The average first-time buyer in the UK now often faces a deposit hurdle of over £65,000, a sum that would take years to accumulate without external support. In high-cost areas such as London and the South East, these figures frequently exceed £100,000. Faced with this reality, over 50% of young homebuyers now rely on financial help from family to get onto the property ladder. Without parental contributions, home ownership is increasingly out of reach for those without inherited wealth, effectively making family support a structural necessity rather than a bonus.

A similar pattern is evident in higher education. Recent media coverage and parliamentary discussions have highlighted the growing "multigenerational burden" of student debt. The Government may be capping student loans at 6% from September, which is good news for those currently paying much more, however many graduates will continue to see their balances grow faster than they can repay them. While some rely on these loans, we are seeing an increasing number of parents and grandparents stepping in to cover fees or living expenses outright. This financial head start provides a significant long-term advantage, allowing graduates to begin their careers without the burden of high-interest debt that would otherwise delay their ability to save, invest, or move into their own homes.

Arrange a free initial consultation![]()

What does this mean for society?

Beyond individual families, the ‘Bank of Mum and Dad’ has wider economic implications. As wealth is increasingly passed down through gifting, it alters patterns of financial security and social mobility. Those who receive help enjoy an advantage not only in property ownership but in long-term financial stability.

Research from the Institute for Fiscal Studies confirms that parental earnings are now a stronger predictor of young people’s future income than in previous generations, reinforcing economic divides between those with access to family capital and those without.

The shifting landscape of Inheritance Tax

For wealthier families, gifting money to children has always served a strategic purpose. Under current UK tax laws, financial gifts made more than seven years before the giver’s death typically fall outside of inheritance tax (IHT) calculations. In addition, parents can pass down most defined contribution pensions free of inheritance tax, in addition to their nil rate band allowance.

However, the strategy behind this is evolving. From April 2027, unused pension funds are set to be included within the value of a person’s estate for IHT purposes. Historically, pensions were a protected way to pass on wealth, but this change looks to already be accelerating a “giving while living" approach. Many grandparents are now choosing or considering choosing to pass down wealth earlier in their lifetime, utilising surplus pension income or lump sums now, to support their grandchildren’s immediate needs while simultaneously reducing the potential 40% tax on their future estate.

Given that IHT is charged at 40% on estates above the £325,000 nil rate band (or £500,000 with the residence nil rate band when passing down your main home to direct descendants), proactive legacy planning is becoming more essential as we approach the 2027 deadline.

The risk of overextending

Despite the clear benefits to the younger generation, parental generosity is not without its risks. As life expectancy increases and the cost of living remains a factor, many parents or grandparents must carefully balance their desire to support their children with their own financial security.

Rising care costs and later-life expenses mean that some retirees could deplete their savings too quickly. A recent survey suggests that over half of UK adults expect to financially support their own parents as they age, illustrating how wealth flows in complex and sometimes unpredictable ways. It is vital that "The Bank of Mum and Dad" does not compromise their own retirement to fund the next generation's present.

The risk of waiting too long - the cognitive ‘timebomb’

While many families focus on the "when" of passing down wealth, we must also consider the risk of waiting too long. One increasingly discussed issue is the potential for assets to become effectively "locked" due to cognitive decline. As we live longer, conditions such as dementia can make it difficult for parents or grandparents to make the very gifts they intended to provide.

We can look to countries like Japan to see the impact of this, where vast sums of personal wealth have become inaccessible because the owners no longer have the capacity to manage them. While the UK is at an earlier stage of this challenge, the trend is clear. Without proactive planning, including the use of Lasting Powers of Attorney, families may find themselves unable to access or manage assets just when they are needed most.

The future of the ‘Bank of Mum and Dad’

The influence of family lending is unlikely to diminish anytime soon. With housebuilding targets continuing to be a challenge and real wages struggling to keep pace with property prices, the need for support shows no signs of easing. Families will continue to navigate the challenges of intergenerational transfers, seeking to strike a balance between supporting their children and securing their own futures.

If you’re considering passing on wealth, early planning is key, especially with the 2027 pension changes coming in next year. Seeking professional financial advice can help structure gifts in the most tax-efficient way, ensuring wealth is preserved and ideally kept in the family.

If you’re looking for advice on the best way to support your loved ones while protecting your own future, why not get in touch for a free initial consultation to see how we can help.

Arrange a free initial consultation

The information contained within this article is for guidance only and does not constitute advice which should be sought before taking any action or inaction. The information is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.