Skip to main content

Skip to main content

The big pension changes in 2024 and how to plan for them

2024 will see some huge changes to pensions, not least the much-publicised abolition of the Lifetime Allowance (LTA). So how do you prepare for a rapidly changing pension landscape? With a general election around the corner and the likelihood of a changing Government how can you plan for changes in legislation that could well be scrapped later down the line?

Arrange your free initial consultation

Lifetime Allowance

Taxation on pension funds has been a hot topic since the 2023 Spring Budget when the Chancellor announced his intention to abolish the ‘Lifetime Allowance (LTA)’. The LTA is the total value that someone can accrue within a pension over their lifetime without incurring certain tax charges. Under LTA rules you could face a tax charge of up to 55% on pension savings above £1,073,100. So, for people with large pension pots, the prospect of abolishing this allowance was welcomed.

The announcement also signposted the introduction of two new allowances which will restrict the amount of tax free lump sums which could be paid under the new pension regime from 6 April 2024.

The new Lump Sum Allowance is the upper limit on the tax-free cash someone can take from their pensions during their lifetime and is capped at 25% of the previous LTA (£268,275).

The second allowance, the Lump Sum and Death Benefit Allowance will restrict the tax free lump sum which can be paid from your pension funds to your beneficiaries if you die before your 75th birthday. The Lump Sum and Death Benefit Allowance is set at £1,073,100 and the new regulation does not have any provision for these to increase over time to keep pace with inflation.

If you had previously registered for one of the many forms of protection against the Lifetime Allowance and have not broken the conditions for maintaining your protection you will benefit from a higher Lump Sum and Lump Sum and Death Benefit Allowance.

To account for benefits taken between 6 April 2006 and 5 April 2024 a transitional calculation has been provided so that individuals can calculate their remaining available Lump Sum Allowance and Lump Sum and Death Benefit Allowance.

There is a secondary calculation which can be undertaken for individuals who did not receive the full tax free cash lump sum entitlement of 25% when pension benefits were taken previously which may enable them to receive an increased Lump Sum and Lump Sum and Death Benefit Allowance. It is advisable to take financial advice when undertaking these calculations as they can be complex.

As soon as the Chancellor announced the abolition of the LTA, Labour announced that they would reintroduce the LTA if they are elected following the impending General Election with the current Prime Minister, Rishi Sunak, suggesting this will happen in the second half of this year.

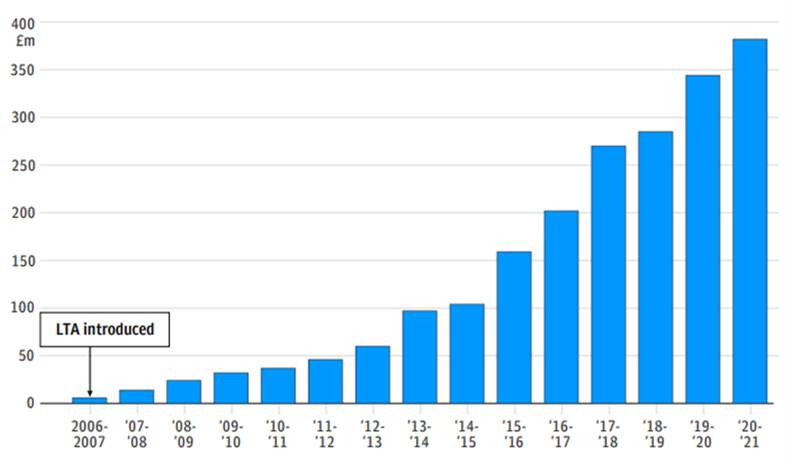

The number of people paying tax for breaching the LTA has been increasing in recent years (See Figure 1) , and the reintroduction of the limit after a period of overcontributing will push this number even higher. If the LTA is reintroduced at its previous level, it is estimated that around 250,000 people will be over the limit.

Figure 1: Tax Paid for breaching lifetime allowance, Source: HMRC, 2024

Many are concerned that bringing back the cap will push senior NHS doctors into an early retirement. One of the key motivations for scrapping the LTA initially was to deter NHS doctors from retiring early to avoid tax bills.

Could a Labour government reverse the rules?

In the run up to the election we could see a sudden flurry of savers rushing to draw down on their pensions before the potential reintroduction of an LTA. To prevent this, Labour may decide not to go ahead with the reversal.

Now that the legislation has been passed and HMRC have almost completed the implementation of the changes, tax experts have said it will be more difficult for policymakers to reverse the rules. This uncertainty leaves savers in a tricky position, as they try to second-guess the next move by a government.

So, do you make the most of the current pension rules or stay cautious in case Labour reverses the changes? In the past when the LTA has been changed HMRC has introduced protections for those who breached the new lower limit. Therefore, if the cap is reintroduced savers who are over the limit might be able to protect their pot. It is hard to predict how a new government might behave but many are hopeful for some form of protection.

If you are thinking about crystalising your pension early to avoid issues with a Lifetime Allowance tax charge, given the complexity of the matter, you should first consult your financial adviser.

Annual Allowance

It is also worth noting that the pension annual allowance changed from £40,000 to £60,000 on the 6th April 2023. Although there is not a limit on the amount that can be saved into pensions each year, there is a limit on the amount that can benefit from tax relief. The ‘Annual Allowance’ is the limit that an individual can contribute to a pension personally in any given tax year, whilst benefiting from tax relief.

For example, someone receiving a salary of £40,000, would only receive tax relief on personal contributions up to £40,000, but someone on a salary of £80,000, would only attract tax relief on contributions up to £60,000. It is important to note that lower limits apply to high earners or individuals who have already accessed some of their pension funds flexibly.

State Pension

The state pension is due to receive an 8.5% rise this month, taking it from £10,600 to £11,502 a year. This is the second largest percentage rise in the last 30 years. It is worth remembering that this isn’t the case for everyone who is entitled to the state pension, and there is no guarantee that the next government will retain the current “triple-lock” status afforded to the State Pension.

You can read more about specific pension details published in the Autumn Statement here.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Simple ways to reduce your tax bill in 2024/25

The age old saying, ‘there are only two things certain in life, death and taxes.’ Well, although we may not always be able to control the former, the good news is we can have greater control on the amount of tax we pay to ensure we are being as tax efficient as possible. Regardless of your age, there are different ways in which you can reduce the amount of money you pay in tax . So, here is a useful refresher on simple ways in which you can save money on your tax bill in the new 2024/25 tax-year (commencing 6th April 2024 through to 5th April 2025).

Arrange your free initial consultation

Firstly, let's look at the taxes most commonly payable:

Income Tax

Income tax is the tax payable on any personal income we receive in a given tax year. This includes any interest received on savings deposits, as well as tax levied on salaries for employed people, or profits for the self-employed.

In England, Wales and Ireland, income tax is levied at 20%, 40% and 45% for basic, higher and additional rate taxpayers respectively. Different rates and tiers apply in Scotland, with 6 tiers of income tax bandings. Here, we will be specifically looking at England, Wales and Ireland.

There are various complexities relating to the personal allowance, however, broadly speaking, you have a personal allowance each tax year, currently £12,570 (frozen until April 2028). Up to this amount, earnings are tax-free. Surplus earnings above this amount are taxed at your marginal rate. It should also be noted that for every £2 you earn over £100,000, your personal allowance decreases by £1. Therefore, the personal allowance is zero if your income is £125,140 or above.

Relating specifically to cash deposits, there is a separate allowance called the personal savings allowance (PSA) which is £1,000 and £500 for basic and higher rate taxpayers respectively. This is used to offset against any interest accrued on our cash savings. Unfortunately, additional rate taxpayers are not entitled to this allowance.

Capital Gains Tax

Capital Gains tax (CGT) is the tax you pay upon the disposal of an asset that has increased in value. These might include the selling of stocks and shares, personal chattels and more. In the 2024/25 tax year, the annual exempt amount has been reduced from £6,000 to £3,000.

The Annual Exempt Amount is the amount you can use to offset against any CGT liability you may incur within that given tax year. Any CGT liability in excess of the annual exempt amount (£3,000), will be taxable at either 10% or 20% depending on if you are a basic rate or higher/additional rate taxpayer.

When disposing of property however, the associated tax is levied at 18% and 28% for basic and higher/additional rate taxpayers respectively. This is not applicable to your primary residence, but to additional properties such as a buy-to-let property of a second home.

Dividend Tax

When investing in stocks and shares of public companies, dividends are usually paid (which is a portion of the company profits distributed to shareholders) on a regular basis (monthly, quarterly, annually etc). There is a tax levied on dividends received - at the rate of 8.75%, 33.75% and 39.35% for basic, higher and additional rate taxpayers respectively.

Each tax year, similar to the annual exempt amount, you have a dividend allowance which is currently a measly £500. This can be offset against dividends received in the 2024/25 tax year, where any excess above the dividend allowance is taxed at their respective rates.

Maximising Tax-Efficiency

Now we have discussed taxes which many of us pay, lets discuss the various ways in which you can help prevent your hard-earned money from going to the tax man!

Utilising ISA Allowances

This is a commonly thought-of solution to investing in a tax-efficient manner. Let’s explore how it works:

- Each tax year you are able to invest an amount into an Individual Savings Account (ISA), currently £20,000. For children aged under 18, they have a Junior ISA (JISA) available to them which currently provides an allowance of £9,000 per tax year.

- Monies held within an ISA can be deposited in cash and/or invested in stocks and shares

- ISAs receive tax-free growth and income.

What does this mean for you?

It means each tax year; you have £20,000 to invest into an ISA. Upon disposal of assets within the ISA, there is no CGT liability generated which saves you money if you continue to utilise your ISA allowances over the long-term. This can avoid an unpleasant tax bill if your investments perform well and generate a capital gain. In addition, if you hold a Stocks and Shares ISA with regular receipt of dividends from the underlying companies, you do not need to worry about any form of dividend tax liability. With the dividend allowance being a measly £500, this could be a crucial difference between generating a sizable tax bill.

If you hold a cash ISA, it also means you do not need to pay income tax on the interest received on the deposit accounts you are holding within the ISA wrapper. Given the increase in savings rates in recent years, especially the high rates which are being offered on some fixed term accounts (see more at Savings Champion), it is considerably easy to accumulate interest in excess of your personal savings allowances than it would have been before rates started to climb.

Making additional Pension contributions

Each tax year, you can tax efficiently contribute into a registered pension scheme the maximum of either £3,600 (gross) or 100% of your relevant UK earnings, up to the annual allowance, currently £60,000 (gross), providing tax relief at your marginal rate. This means if you’re a 20%, 40% or 45% taxpayer, you may be able to claim tax relief, matching your personal tax band, on contributions made up to the annual allowance. There is also an opportunity for further pension contributions in excess of the annual allowance through a carry-forward rule. This allows up to a maximum of 3 previous tax year unused allowances to be used.

Please note: If you are a high earner, then your annual allowance may be subject to tapering. If you are unsure or believe you are in this position, you should speak to your adviser.

To encourage savings for retirement, the Government pays tax relief on the allowable contributions you make. This means that your pension provider can claim tax back from HMRC and add that amount to each contribution you make. Tax relief can be claimed through various ways such as the net pay arrangement, relief at source or salary sacrifice.

Pension savings are typically free to grow without generating any form of tax liability. Furthermore, when you begin drawing down on your pension, typically 25% of the pension pot will be paid tax-free, with the remaining amount being taxable at your marginal rate.

All the above-mentioned points mean that contributing into our pension can be extremely tax efficient.

For those who have relevant earnings above £100,000, there could be further benefit to contributing considerable amounts into your pension as you could be paying an effective rate of up to 60% income tax.

How does it work?

- As mentioned before, we all receive a personal allowance of £12,570. For earnings above £100,000, this personal allowance tapers by a rate of £2 per £1 over £100,000.

- This means you can earn £125,140 before completely losing any entitlement to the personal allowance.

- However, if you were to contribute into a pension, it reduces your taxable income and therefore, you can begin to reclaim your personal allowance.

Case Study example:

Sally, has relevant UK earnings of £120,000 and as a result, is a higher rate taxpayer. Due to her high salary, she only has a personal allowance of £2,570 (£20,000 earnings over £100,000. Therefore £20,000 / 2 = £10,000 of personal allowance lost. Personal allowance = £12,570 - £10,000 = £2,570).

Sally has decided it is affordable for her to make a gross pension contribution of £20,000 that tax year. As a result, not only has she successfully managed to reclaim her full personal allowance by lowering her taxable income. In doing so, Sally has also contributed to a tax efficient investment vehicle, obtained 40% tax relief from the government, all of which is able to grow tax free for her retirement provision.

As with all things, there comes a downside to specific strategies in saving tax. An example of this would be that you can only access your pension from age 55, increasing to 57 in 2028, as per the normal minimum pension age. There may be exceptions for those in critical illness or for the terminally ill. It is important to ensure affordability of pension contributions due to the inaccessibility of the investments. You should speak to a financial adviser when contemplating aspects of your retirement including affordability of a pension contribution.

Use it or lose it – Utilising all allowances in the household

As mentioned above, we have discussed the main types of tax which people might be liable to pay, including Capital Gains Tax, Dividend Allowance, Personal Allowance and the Personal Savings Allowance.

At the end of the tax year, these allowances will be reset, whether you have used them or not and most cannot be carried forward. As such, to help maximise tax efficiency, it is also worthwhile to consider the allowances available as a household and not just on an individual basis.

If you have utilised your current years allowances, there may be someone in your household who has not. In this instance, funding their contributions or allowances might be a useful way to spread the tax liability across multiple people to maximise tax efficiency.

Case Study example:

Rebecca, age 45, earns £185,000 per annum while her husband, David, earns £20,000. They have two children, James and Josh. Rebecca has currently utilised all her allowances in a tax-efficient manner as well as maximised her pension contributions for the current tax-year – however the remainder of her family have not. Rebecca holds some cash and some shares which are outside of her ISA and Pension. David has also contributed an affordable amount to his workplace pension arrangement to claim basic-rate tax relief.

Rebecca could:

- Gift some of the shares to her husband, David, if she believes that the gain on these assets is likely to generate a capital gain in excess of £3,000. Between them, they have £6,000 allowance to use.

- Minimise her cash holdings and maximise David’s cash holdings, as Rebecca does not have any personal savings allowance to offset against any interest earned as she is an additional rate taxpayer.

- Contribute £3,600 into each of her children’s pensions as well as £9,000 into their JISAs to utilise their current allowances.

- Contribute to David's pension on his behalf if affordable. Knowing how much is affordable should be done with the assistance of a financial adviser.

- Gift £20,000 to David for him to make an ISA contribution in the current tax year, if affordable.

The culmination of utilising your own allowances as well as your loved one's allowances, can be a great way for high earners to maximise their own tax efficiency as well as their families.

If this or anything you see in this article is something you would rather discuss with an adviser, please get in touch with us. We’re offering anyone with £100,000 or more in pensions, savings or investment a free initial review worth £500.

In our recent webinar: How to escape the tax raid on your Wealth, experts Christie Tillett and David Gruenstein talked about smart tax planning and how it has become essential to retain as much of your wealth as possible.

Watch it back here!

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Investment returns are not guaranteed, and you may get back less than you originally invested.

Tax rates and allowances mentioned in this article are based upon current limits and allowances, but are subject to change.

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax advice.

Savings Champion and their associated services are not regulated by the Financial Conduct Authority (FCA).

Navigating changes to UK tax 2024

The Chancellor, Jeremy Hunt, recently delivered his ‘Budget for Long-Term Growth on 7th March 2024, announcing the latest raft of tax changes to contend with, many of which will come into effect from 6th April 2024. This all follows huge pension change announcements last year and the continued effects of the stealth taxes hitting us all. Navigating all of these can be hard so here’s a look at some of the key changes that might affect you this coming new tax year.

Arrange your free initial consultation

National Insurance Changes

The national insurance rate for employees had previously been cut from 12% to 10%, with this change coming into effect on 6th January 2024. This is being further reduced by 2% to 8% from 6th April 2024, with both cuts applying to earnings between £12,570 and £50,270 per tax year.

The Treasury says the average worker on £35,400 per year will save more than £900 a year as a result of both of these cuts in January and April. This figure rises to over £1,500 for anyone who is employed and a higher rate taxpayer.

For the self-employed, the Government will reduce the main rate of Class 4 national insurance contributions from 9% to 6% from April 2024. This is an increase on the 1% cut that was previously announced at the 2023 Autumn Statement from 9% to 8%. Class 4 national insurance contributions apply to earnings between £12,570 and £50,270 per tax year. This could result in a potential saving of over £1,100 if you are self-employed with earnings over £50,270 per tax year.

The Government is also scrapping Class 2 national insurance contributions for the self-employed. Prior to 6th April 2024, you pay Class 2 national insurance contributions at £3.45 a week (£179.40 per year) if your self-employed profits are £12,570 or more for a tax year.

Abolition of the Lifetime Allowance, what does this mean?

The lifetime allowance, a limit on how much you can build up in pension benefits over your lifetime while still enjoying full tax benefits, is being scrapped from 6th April 2024. The lifetime allowance for the 2023/24 tax year is £1,073,100.

This removal of the lifetime allowance follows the removal of the lifetime allowance tax charge from 6th April 2023. Prior to 6th April 2023, any withdrawals above the lifetime allowance limit were subject to 55% if taken as a lump sum, or 25% plus your marginal rate of income tax if taken as income. From 6th April 2023 up to 5th April 2024, any excess over the lifetime allowance (whether taken as a lump sum or income) is subject to your marginal rate of income tax.

From 6th April 2024, the tax-free lump sum which can be taken from a pension pot (after the age of 55) will remain at 25% of the current lifetime allowance, equivalent to £268,275. This tax-free lump sum limit will be known as the Lump Sum Allowance (LSA). Any withdrawals above your LSA will be subject to your marginal rate of income tax.

Transitional protections may continue to apply, so it is worth checking whether the changes to the lifetime allowance may impact your tax-free cash entitlement.

An additional complication is Labour have indicated that should they be elected in the next general election, they plan to reverse the removal of the lifetime allowance. As ever, it is critical to keep on top of current legislation.

Changes to Capital Gains Tax

If you hold investments outside of tax-efficient wrappers such as ISAs and pensions, or are planning to sell a second property, you should be aware of the cut to the capital gains tax (CGT) annual exemption.

Within the 2022/23 tax year, the annual CGT exemption below which you would pay any tax on capital gains was £12,300 per tax year. This was cut to £6,000 from 6th April 2023, and will be reduced further to £3,000 from 6th April 2024, less than a quarter of what the exemption was in the 2022/23 tax year.

Capital gains tax on second property sales

The higher rate of CGT on residential property sales (excluding your main residence which is not subject to CGT typically) for higher and additional rate taxpayers will be reduced from 28% to 24% from 6th April 2024. This is in a move to try and encourage property sales in order to generate further tax revenue despite the cut in the tax rate.

The rate of CGT on residential property sales for basic rate taxpayers will remain at 18%.

The CGT rates for any other asset sales will remain at 10% for a basic rate taxpayer and 20% for higher and additional rate taxpayers.

What is happening to the dividend allowance?

Whilst the tax rates on dividend income will remain unchanged in the new tax year, similar changes are being made to the dividend allowance (as per the CGT allowance) which is being halved. The dividend allowance (below which no tax is payable on dividends) stood at £2,000 per individual per tax year, was reduced to £1,000 from 6th April 2023 and will be halved once again to £500 from 6th April 2024.

These changes make it even more important to be making use of your annual tax-efficient allowances, to reduce any potential tax liability on capital gains and investment income.

One implication of these changes is more individuals will fall above these tax-free thresholds, resulting in the potential need to complete a self-assessment tax return if not doing so already.

Please do get in touch if you are unsure whether you will be affected by the reduction in these allowances.

High Income Child Benefit Charge (HICBC)

In order to support working families, the threshold to start paying back Child Benefit will be increased from 6th April 2024 from £50,000 to £60,000 per tax year. This applies to the highest earning partner for a couple.

The rate at which the Child Benefit is taxed away completely is being made more favourable, with 1% of the benefit taxed away for every extra £200 you earn above the threshold (instead of 1% for every extra £100 above the threshold in the 2023/24 tax year).

This means that the upper income threshold, where the Child Benefit is effectively taxed in full, is rising from £60,000 to £80,000.

From April 2026 (subject to consultation), the Government is planning to move to a household income system for administering the tax charge, rather than on an individual basis, so single earner families are not disadvantaged.

Further investment in UK businesses?

A new “British ISA” was announced in the Spring Budget following widespread speculation. This will be a further £5,000 tax-free ISA allowance for investments into British companies, and will be in addition to the standard £20,000 ISA allowance which is remaining unchanged.

Further details to follow including when this will be available.

“Stealth Taxes” – what are they?

Although the freezing of some tax allowances not mentioned above may look like a ‘neutral’ move with limited impact on your situation going into the new tax year, it is important to be aware of “stealth taxes”. While income tax bands, which are frozen until 2028, will remain unchanged from 6th April 2024, if your wage is increasing year on year (for example to account for inflation), you will be subject to a greater tax liability.

Similarly, the Savings Allowance for savings interest, as well as the Inheritance Tax threshold (Nil Rate Band), are remaining at the same levels going into the new tax year, pulling more and more people into paying these taxes.

These stealth taxes, if left unattended, will be a drag on your income and accumulated wealth.

Do I need to take any action?

With widespread changes across the tax landscape, it is as important as ever to ensure you are making use of the key allowances applicable to your personal situation, and minimising the amount of tax you pay on your income and/or wealth.

If you’d like to learn more about what the changes will mean to you in the new tax year, why not get in touch and book in a free initial consultation with one of our expert advisers.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

Spring Budget 2024

The Spring Budget 2024 confirmed some rumours, such as the introduction of a British ISA, and at the same time, contained a few surprises too.

The main points are summarised below along with a reminder of some of the other changes coming into effect in April 2024.

Some measures are potentially subject to change until enacted into legislation.

If you have any questions or would like to speak to one of our expert financial advisers about the changes announced, contact us to arrange a free initial consultation.

Arrange your free initial consultation

Pensions

Abolition of Lifetime Allowance (LTA) from 6 April 2024

A further Pension Schemes Newsletter / Lifetime Allowance Guidance Newsletter is expected this week but no further detail was issued as part of the Budget itself. Further information will be issued once it’s available.

State pension

Triple lock means new state pension and basic state pension will increase by 8.5% in April 2024. Full new state pension figure will be £221.20 per week.

Investments

Individual Savings Accounts (ISA)

The annual subscription limits all remain at their current levels in 2024/25, i.e.

- £20,000 ISA

- £4,000 Lifetime ISA

- £9,000 Junior ISA (and Child Trust Fund)

A new British ISA is to be introduced from a date to be confirmed. This will give investors an additional £5,000 ISA allowance each tax year, so on top of the current £20,000. There is a consultation paper in place to obtain feedback from ISA managers, but the idea is for allowable investments to include UK equites and potentially UK corporate bonds, gilts, collectives.

As previously announced at the Autumn Statement, the government is to make changes to ISAs to simplify the scheme and widen the scope of investments that can be included in ISAs. To simplify the scheme the government will:

- Allow multiple subscriptions in each year to ISAs of the same type, from 6 April 2024

- Remove the requirement to make a fresh ISA application where an existing ISA account has received no subscription in the previous tax year, from 6 April 2024

- Allow partial transfers of current year ISA subscriptions between providers, from 6 April 2024

- Harmonise the account opening age for any adult ISAs to 18, from 6 April 2024

- Digitise the ISA reporting system to enable the development of digital tools to support investors

Reserved Investor Fund

The Reserved Investor Fund is a new type of investment fund designed to complement and enhance the UK’s existing funds rule. This meets the industry demand for a UK-based unauthorised contractual scheme, with lower costs and more flexibility than the existing authorised contractual scheme. The introduction date is still to be confirmed.

Taxation

Income tax

All income tax rates and bands remain at their current levels in 2024/25. See our latest tax tables 2024/25.

National insurance (NI)

National Insurance is paid by people between age 16 and State Pension age who are either an employee earning more than £242 per week from one job or self-employed and making a profit of more than £12,570 a year.

Following on from the NI cuts made in the Autumn Statement when the 12% rate of employee NI reduced to 10% from January 2024, the government is cutting the main rate of employee NI by 2p from 10% to 8% from 6 April 2024.

They are also cutting a further 2p from the main rate of self-employed National Insurance on top of the 1p cut announced at Autumn Statement and the abolition of Class 2.

This means that from 6 April 2024 the main rate of Class 4 NICs for the self-employed will now be reduced from 9% to 6%.

Child Benefit charge

The adjusted net income threshold for the High Income Child Benefit Charge (HICBC) will increase from £50,000 to £60,000, from 6 April 2024.

For individuals with income above £80,000, the amount of the tax charge will equal the amount of the Child Benefit payment. For those with income between £60,000 and £80,000, the rate at which HICBC is charged is halved, and will equal one per cent for every £200 of income that exceeds £60,000.

New claims to Child Benefit are automatically backdated by three months, or to the child’s date of birth (whichever is later). For Child Benefit claims made after 6 April 2024, backdated payments will be treated for HICBC purposes as if the entitlement fell in the 2024/25 tax year if the backdating would otherwise create a HICBC liability in the 2023/24 tax year.

In his Budget speech, the Chancellor announced that the plan is to move assessment for the HICBC to a system based on household income from April 2026. This is to remove the current unfairness meaning that a couple who each have income below the threshold, so could in 2023/24 have £49,000 pa each (£98,000 pa in total), wouldn’t be subject to the HICBC whereas another household with one person with income of £51,000 for example would.

Dividend allowance

As we are already aware, the dividend allowance reduces from £1,000 to £500 on 6 April 2024. Dividend tax rates remain the same at 8.75% in basic rate band, 33.75% in higher rate band and 39.35% in additional rate band (and 39.35% for discretionary trusts).

Arrange your free initial consultation

Capital gains tax (CGT)

Annual exemption reduces from £6,000 to £3,000 on 6 April 2024 (a maximum of £1,500 for discretionary/interest in possession trusts – shared between all settlor’s trusts subject to a minimum of £600 per trust).

CGT rates remain as they currently are apart from the higher CGT rate for residential property gains (the lower rate remains at 18%):

- 10% for any taxable gain that doesn’t fall above the basic rate band when added to income and 20% on any gain (or part of gain) that falls above the basic rate band when added to income

- For residential property gains these rates increase to 18% and 24% (formerly 28%) respectively

- Discretionary/interest in possession trustees and personal representatives pay at the higher rates (20%/24% (formerly 28%))

Simplifications for trusts and estates

From April 2024 trustees and personal representatives of estates will no longer have to report small amounts of income tax to HMRC and taxation of estate beneficiaries will be simplified, as shown below:

- Trusts and estates with income up to £500 will not pay tax on that income as it arises

- The £1,000 standard rate band (effectively basic rate band) for discretionary trusts will no longer apply

- Beneficiaries of UK estates will not pay tax on income distributed to them that is within the £500 limit for the personal representatives

Stamp duty land tax (SDLT)

SDLT Multiple Dwellings Relief is being abolished from 1 June 2024. This applies to purchasers of residential property in England and Northern Ireland who acquire more than one dwelling in a single transaction or linked transactions.

Changes to the taxation of non-doms

The concept of domicile is outdated and incentivises individuals to keep income and gains offshore. The government is therefore modernising the tax system by ending the current rules for non-UK domiciled individuals, or non-doms, from April 2025. A new residence-based regime will take effect from April 2025.

From April 2025, new arrivals, who have a period of 10 years’ consecutive non-residence, will have full tax relief for a 4-year period of subsequent UK tax residence on foreign income and gains (FIG) arising during this 4-year period, during which time this money can be brought to the UK without an additional tax charge.

Existing tax residents, who have been tax resident for fewer than 4 tax years and are eligible for the scheme, will also benefit from the relief until the end of their 4th year of tax residence.

Liability to inheritance tax (IHT) also depends on domicile status and location of assets. Under the current regime, no inheritance tax is due on non-UK assets of non-doms until they have been UK resident for 15 out of the past 20 tax years. The government will consult on the best way to move IHT to a residence-based regime. To provide certainty to affected taxpayers, the treatment of non-UK assets settled into a trust by a non-UK domiciled settlor prior to April 2025 will not change, so these will not be within the scope of the UK IHT regime. Decisions have not yet been taken on the detailed operation of the new system, and the government intends to consult on this in due course.

Furnished holiday lets (FHL)

The FHL tax regime, which relates to short-term rental properties, is to be abolished from April 2025.

Currently, if an individual lets properties that qualify as FHLs:

- The profits count as earnings for pension purposes

- They can claim Capital Gains Tax reliefs for traders (Business Asset Rollover Relief, relief for gifts of business assets and relief for loans to traders)

- They’re entitled to plant and machinery capital allowances for items such as furniture, equipment and fixtures

Raising standards in the tax advice market

A consultation has been issued to discuss the government’s intention to raise standards in the tax advice market through a strengthened regulatory framework. It sets out three possible approaches to strengthening the framework: mandatory membership of a recognised professional body, joint HM Revenue and Customs (HMRC) – industry enforcement, and regulation by a separate statutory government body. The consultation also explores approaches to strengthen the controls on access to HMRC’s services for tax practitioners.

This has relevance to anyone who may receive or provide tax advice or offers services to third parties to assist compliance

with HMRC requirements. For example, accountants, tax advisers, legal professionals, payroll professionals, bookkeepers, insolvency practitioners, financial advisers, customs intermediaries, charities and other voluntary organisations that help people with their tax affairs, software providers, employment agencies, umbrella companies and other intermediaries who arrange for the provision of workers to those who pay for their services, people who engage workers off-payroll, promoters, enablers and facilitators of tax avoidance schemes, professional and regulatory bodies, and clients, or potential clients, of all those listed above.

The consultation runs until 29 May 2024.

VAT

The VAT threshold is increasing from £85,000 to £90,000 from 1 April 2024, the first increase in seven years. See our tax tables 2024/25 for more details. See our tax tables 2024/25 for more details.

If you’d like to discuss any of the changes announced in the Budget or would simply like to explore ways that you can minimise the amount of tax you pay on your wealth, why not get in touch and speak to one of our expert team of advisers. We’re offering anyone with £100,000 in savings, investments or pensions a free financial review worth £500.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Income needed for a comfortable retirement reaches new highs

The latest update to the Pensions and Lifetime Savings Association’s (PLSA) ‘Retirement Living Standards’ has revealed that a ‘moderate’ standard of living in retirement could now require over a third more income to account for the rising cost of living.

This means that for the ‘moderate’ retirement, which many savers aim for, a single person would need roughly £8,000 more in 2023/24 than they did in 2022/23. A total of £31,300 in 2023/24 is required, up 34% from £23,300 the year prior.

The thresholds for ‘minimum’ and ‘comfortable’ retirements also increased from the previous year, with a ‘minimum’ retirement living standard costing 13% more, up from £12,800 to £14,400, and a ‘comfortable’ retirement living standard costing 16% more, up from £37,000 to £43,100.

Arrange your free initial consultation

The table below displays the exact updated figures for each threshold. It’s important to note that these figures only represent the cost of retirement living now and do not account for future changes. If you don’t plan to retire for years, it’s important to consider how these thresholds may increase with future inflation.

| PSLA Retirement Living Standards | SINGLE | COUPLE | ||||

| 2024 level of income | Previous level | % Increase | 2024 level of income | Previous level | % Increase | |

| Minimum | £14,400 | £12,800 | 13% | £22,400 | £19,000 | 18% |

| Moderate | £31,300 | £23,300 | 34% | £43,100 | £34,000 | 27% |

| Standard | £43,100 | £37,300 | 16% | £59,000 | £54,400 | 8% |

Figure 1 - PSLA Retirement Living Standards, Source: Pensions and Lifetime Savings Association, 2024

With the state pension potentially rising to 71 by 2050, it’s more important than ever to seek professional financial advice to ensure you’re prepared as retirement living costs continue to increase.

How do the thresholds work?

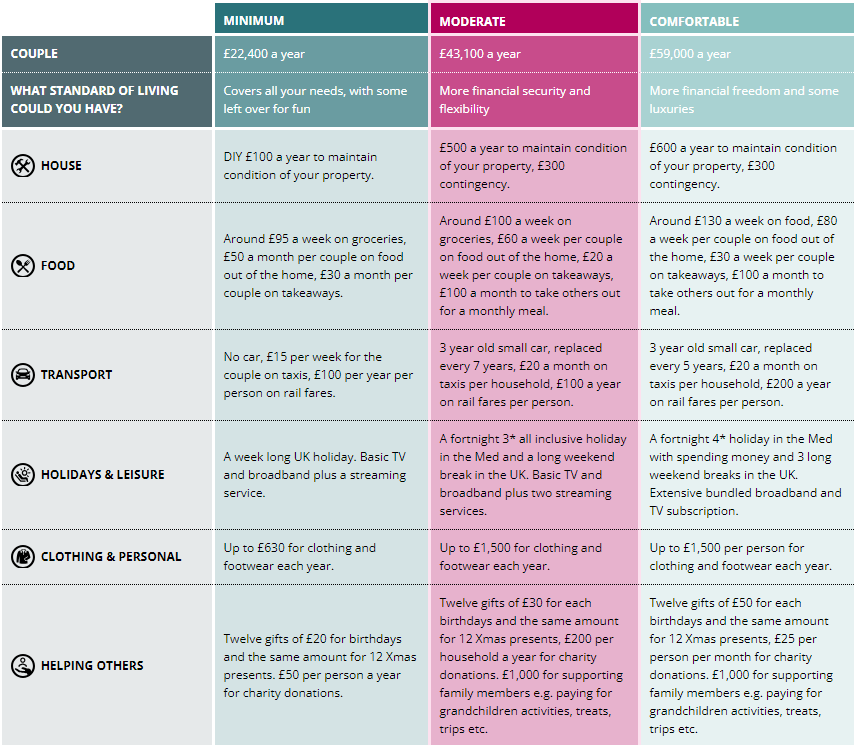

The thresholds, called the ‘Retirement Living Standards’, are intended to provide a very rough guide to how much different retirement lifestyles might cost and what they would generally allow for in terms of budget. The ‘minimum’, ‘moderate’ and ‘comfortable’ categories attempt to convey a realistic picture of life by assuming that everyone, including those targeting a ‘minimum’ standard of living, will want to at least have some kind of social life and the occasional takeaway while still being able to pay essential bills.

For example, the ‘minimum’ living standard assumes one weeklong UK holiday per year. By contrast, the ‘comfortable’ living standard, budgets for a fortnight 4 star holiday in the Mediterranean with spending money and three long weekend breaks in the UK. The moderate living standard assumes a more realistic 3 star all-inclusive fortnight holiday in the Mediterranean and a long weekend break in the UK.

Some of the key assumptions that inform the Retirement Living Standards are detailed in the table below. These living standards assume no mortgage or rental costs.

Figure 2 - Types of expenditure, Source: Pensions and Lifetime Savings Association, 2024

*The figures shown are the amounts of annual expenditure required to achieve the living standard (ie they are not gross income figures).

With the cost of living in retirement on the rise, it’s more important than ever to manage your retirement plans carefully to ensure you don’t get caught out. If you want to find out more about how you can navigate these changes, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our chartered advisers to find out how we might be able to help you.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

How the Budget could affect your finances

Chancellor Jeremy Hunt will unveil his Spring Budget on 6 March, which is likely to be his last fiscal announcement before the upcoming General Election.

Before the Autumn Statement in November 2023, there were rumours of Inheritance Tax being scrapped, a change in the calculation of the State Pension, and an ISA aimed at boosting investment into the UK. Instead, pensioners received a boost as the calculation of the State Pension remained unchanged, so they will receive the full 8.5% increase in April. Additionally, instead of the other changes we were expecting, National Insurance was reduced, resulting in an annual saving of up to £754 p.a. for workers.

The Prime Minister, Rishi Sunak, is under pressure personally with the Conservatives still trailing Keir Starmer's Labour Party significantly in the polls, so there is an expectation that big changes need to be announced to change the minds of voters. So, what can we expect?

Arrange your free initial consultation

Inheritance Tax

After opting to cut National Insurance rather than Inheritance Tax in the Autumn Statement, it would seem unlikely that the Chancellor would opt to cut Inheritance Tax now, especially given the relatively small number of voters any change would affect, relative to a further cut in National Insurance or Income Tax.

By way of reminder, Inheritance Tax is payable at 40% when the estate of an individual exceeds £325,000 (though there are increased allowances when main residences are left to direct descendants) and gifts, both directly and into trust, must also be accounted for. Please speak to your TPO adviser for further information.

Additionally, there could be unintended consequences if Inheritance Tax were to be scrapped as previously reported. An example of this could be the impact on some small UK companies, as investors into these can potentially benefit from inheritance tax relief (although these investments are high risk and not suitable for all investors), so the removal of this relief could reduce their appeal to investors.

Income Tax / National Insurance

For the reasons mentioned above, it’s likely Income Tax or National Insurance may be cut rather than Inheritance Tax, in a move that can be framed as a pre-election giveaway. However, as was widely reported after the National Insurance reduction in the Autumn Statement, any reduction’s impact is likely to be minimal when compared with the combined impact of frozen tax bandings and high inflation over the past few years.

This theory is supported by The Resolution Foundation, who have calculated, “Cutting the basic rate of Income Tax by 1p while maintaining the personal allowance freeze next year would mean anyone earning less than £38,000 would see their personal tax bills rise rather than fall.”

Child Benefit Threshold

Another option for the Chancellor could be to raise or scrap the current £50,000 earnings threshold above which Child Benefit starts to reduce.

This would prove popular with some voters, but it would be expensive and would benefit a smaller percentage of the voting public than an outright reduction to Income Tax or National Insurance.

Conclusion

A study by Capital Economics calculates Chancellor Jeremy Hunt has about £15bn in headroom with which he can cut taxes. It will be interesting to see which areas any pre-election giveaways are targeted at and how far Mr Hunt’s tax cuts will go. If he does not go far enough, the Conservative Party could face a wipeout at the next election, but if he goes too far and bond markets view the tax cuts as unfunded, we could have a repeat of Kwasi Kwarteng’s “Mini-Budget’ which caused chaos in bond markets in September 2022.

Mr Hunt has sought to gain market confidence through financial discipline during his tenure as Chancellor and he will not want to jeopardise this in what could be his final budget, he will be under pressure to give Conservative candidates a budget upon which they can build an election campaign.

If you’d like to learn more about how you can minimise the amount of tax you pay on your wealth, why not get in touch and speak to one of our experts for a free initial consultation.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Inheritance tax receipts headed for record high

The latest figures from HM Revenue & Customs showed that inheritance tax (IHT) receipts have reached £5.7bn, £400m higher than during the same period last year.

At the current rate, the previous year’s record high £7bn in inheritance tax receipts is on track to be beaten come tax year end, continuing a concerning upwards trajectory. According to the Office of Budget Responsibility, total IHT intake could reach or exceed £8.4bn in the 2027/28 tax year.

Additionally, in a bid to boost IHT receipts further, HMRC has launched an investigation into more than 2,000 households between April and November 2023 that they believe may not be paying enough IHT. Often, a sizable portion of IHT recovered comes from HMRC investigations that were opened months or even years previously.

With rumours around the Government reducing or even scrapping IHT, despite the record highs, and with Labour saying that they would reverse any abolition should they win the next general election, the hot topic of IHT is leaving many with more questions than answers.

Arrange your free initial consultation

What is IHT?

Inheritance Tax (IHT) is a tax levied by the Government on the estate of a deceased person in the UK. This includes all of their assets including property, personal belongings, and investments.

However, this levy only applies to the total value of the estate that exceeds the IHT threshold or ‘nil-rate band’. As of the 2023/24 tax year, the threshold is set at £325,000. Anything above £325,000 could be subject to up to 40% inheritance tax and anything below this threshold is tax-free.

Following the introduction of the residence nil-rate band (RNRB) in April 2017, you can also add an extra £175,000 to the total tax-free threshold, provided you are passing down your assets and property to direct descendants.

Why are IHT receipts continuously on the rise?

The number of estates across the UK that are being pulled into the IHT net are increasing each year.

Total IHT receipts collected by the Government have been steadily on the rise with the situation accelerating since the IHT tax free threshold was frozen at current levels. This was initially announced by the then Chancellor, Rishi Sunak, in his 2021 Budget. The Budget outlined that the IHT threshold, along with many thresholds and allowances, would be frozen for five years until 2026. However, this was further extended for two more years until April 2028.

However, due to the rising rate of inflation coupled with ever increasing property values across the UK, the freeze essentially means that a greater number of people will cross the inheritance tax threshold each year. Many have been calling this move an example of ‘shadow tax’, as the simple act of freezing allowances rather than upping tax rates means the Government will have collected billions in extra tax.

The inheritance tax allowance of £325,000 was increased from £312,000 on 6 April 2009. This means the IHT nil rate band has been frozen for over 14 years now and will keep allowances frozen until at least 5 April 2028. That’s a staggering 19 years of higher taxes on death.

With the Government cracking down on thousands of households that owe money who might not even realise they have breached the allowance, it’s more important than ever to seek professional advice to help navigate the threshold and avoid any possible penalties. Inheritance tax is often referred to as a voluntary tax as there are many ways you can mitigate it, with the right amount of time and planning. If you’re interested in learning more about how to manage IHT on your estate, to ensure the best possible wealth protection for you or your family, we can help. Give us a call on 0333 323 9065 or book a free non-committal initial consultation with a member of our team to find out more.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

Inheritance Tax, not just a concern for the wealthy

Often referred to as the ‘death tax’, Inheritance Tax (IHT) is a financial levy imposed on a deceased person’s estate that determines the distribution of wealth to their beneficiaries. Despite popular belief, IHT is not exclusive to the wealthy; its impact resonates across a wide spectrum of society.

IHT is calculated on the total value of the deceased’s estate, with a headline rate of 40% applied to estates that exceed the £325,000 nil-rate band (NRB). The misconception that only the wealthy need concern themselves with IHT is ousted, as longer life expectancies and changes in demographics bring the impact of this tax closer to home.

Arrange your free initial consultation

The current landscape

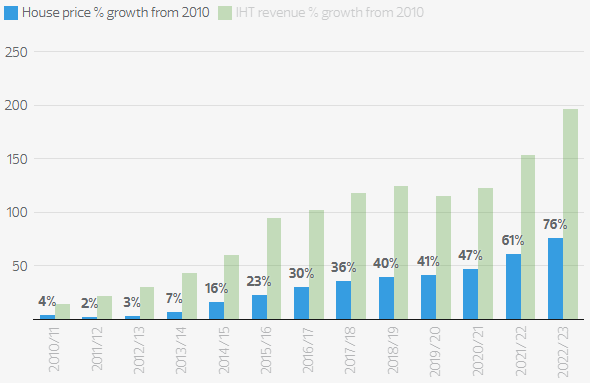

The Office for Budgeting Responsibility (OBR) are predicting that IHT receipts in the UK will rise sharply from the record-breaking £7.1 billion collected in 2022-2023 to £8.4 billion by 2027-2028. According to HMRC data, one in every 25 estates are subject to IHT, meaning that this tax is no longer exclusive to the wealthy. Recent data from HMRC reveals a staggering £2.6 billion in IHT receipts were collected in just 13 weeks between April and July of 2023, which is more than the total IHT bill for 2009. Based on projections, the average IHT bill is expected to rise to £304,567 in 2025-2026 and £345,084 in 2027-2028.

With its tax-free allowance, known as the NRB, remaining unchanging at £325,000 since April 2009, IHT may be considered as one of the longest-standing stealth taxes. Over the past decade there has also been no increase to the £3,000 gifting allowance. Rising house prices and frozen allowances are drawing more households into the IHT net, debunking the common misconception that IHT is solely for the wealthy.

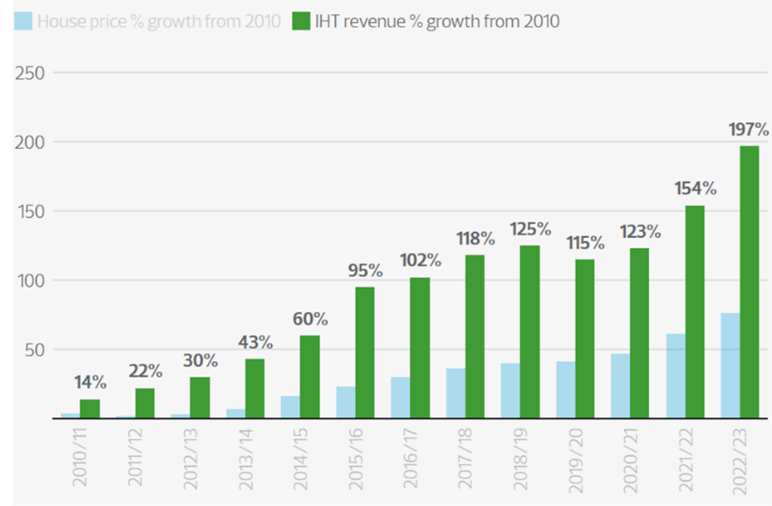

The Office of National Statistics has released figures showing a 73% increase in house prices in the ten years from 2013 to 2023. This consistent rise in house prices over the last decade has contributed significantly to the rise in IHT receipts. Although an individual’s property value is not the sole contributor to the value of their entire estate, it accounts for a substantial proportion of it, therefore expanding the number of households within the scope of IHT. To help somewhat offset IHT, there is an additional threshold, the residence nil-rate band (RNRB), which was introduced in 2017. If an individual leaves their main residence to a direct descendant, they are able to pass on an additional £175,000 IHT free.

Figure 1: House price growth vs IHT revenue % growth from April 2010, Source: RSMUK, 2023.

The political elephant in the room

Rumours around Government changes to IHT?

Navigating potential changes to IHT and political uncertainties is essential, as rumours concerning the possible elimination of IHT, or introduction of a wealth tax continue to circulate ahead of the next Budget on 6th March. In an effort to win over votes, reports indicate that the Conservative Party may abolish IHT, while a wealth tax on the wealthiest individuals is also being considered, however, with the potential of a changing government with an impending General Election, how long any changes stay in place is impossible to call. To effectively plan and reduce IHT, individuals should instead concentrate on the rules and regulations currently in place, rather than basing their decisions on rumours and speculation.

How can you ensure as much as possible of your estate goes to your loved ones?

In order to mitigate IHT, a thorough strategy combining strategic financial planning and maximising available allowances is needed.

Some key strategies include:

Increase your spending - Spending additional cash to lower the value of your estate is a straightforward yet effective tactic. While this may seem straightforward, individuals should aim to strike a balance between reducing their estate, whilst ensuring they don’t compromise their long-term financial security. For this, putting in place a robust financial plan is key.

Responsible financial planning – IHT encourages individuals to engage in financial planning. It is key for this to be updated each year to ensure individuals can enjoy their desired lifestyle whilst also maximising various allowances. Working with a qualified financial adviser can help you comprehend the potential effects of IHT and encourage you to look into mitigation techniques.

Annual gifting – Making use of the £3,000 annual gifting allowance per person offers an opportunity to reduce the taxable estate. If you have not used your annual exemption in the previous tax year, then you are eligible to combine this to your current tax year to make an allowance of £6,000. Utilising additional exemptions above the £3,000 yearly allowance can also be achieved by making use of small gifting of up to £250 to different individuals, although not to anyone who has already received a gift of your whole £3,000 annual exemption.

Regular gifting - A less known allowance is gifting out of surplus income. If individuals can demonstrate that their regular income can comfortably meet their lifestyle expenditure with surplus income remaining, this can be gifted to one beneficiary or split across several. It is important that this gifting has a regular pattern as it is supposed to come out of surplus income. Given that these requirements are met, these gifts out of surplus income would not be subject to IHT.

It is very important to ensure that these gifts would not be classified as a gift out of capital.

As a reminder, any capital gifts over the annual allowance of £3,000, will be classified as Potentially Exempt Transfer (PET). This means that 7 years need to pass following the capital gift, so it is IHT exempt. Careful financial planning can help to determine, if regular gifting out of surplus income is affordable.

Gifts to charities – Gifting to charities can lower the net value of your estate whilst simultaneously giving to a charity you wish to help. Furthermore, charitable donations are free from IHT, offering a strategic way to reduce the total IHT obligation. If you leave 10% of your estate to a charity, then IHT payable above the £325,000 threshold will reduce from 40% to 36%.

Contribute to a defined contribution pension – Since the introduction of pension freedoms in 2015, pensions have emerged as one of the most tax-efficient means of wealth transfer as they do not form part of your estate for IHT purposes. Most pensions are written under a form of trust, meaning the entire pot, including tax relief, can be passed down to loved ones without incurring IHT. Older defined contribution pensions might not be written into trust, which can mean that they might still be paid into the individual’s estate, therefore this should be checked. Since most defined contribution pensions do not form part of your estate on death, pension savings aren’t usually covered in a Will. It is essential to ensure expression of wish forms are set up and kept up to date with pension providers, so they know who to pay out the benefits.

What can you do as the Budget and Tax Year end draw near?

Making the most appropriate use of the above exemptions and annual allowances can help to reduce the taxable value of your estate. These need to be tailored to your individual needs and it is key that a bespoke gifting strategy is put in place without compromising your own lifestyle. Early engagement with a financial adviser plays a key role in ensuring you are making an informed decision in the ever-changing financial landscape. With careful financial planning, individuals can make sure their hard-earned assets are protected for their chosen beneficiaries.

Key dates to have in mind: The Budget on 6th March and the end of the current tax year on 5th April.

If you’d like to learn more about how you can minimise the tax bill on your estate, why not get in touch for a free initial consultation with one of our experts.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

This article is also based upon our understanding of current law, HM Revenue and Custom's practice, tax rates and exemptions which are subject to change.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning or tax advice.

Top up your pension with National Insurance cut

Announced by Chancellor Jeremy Hunt in the November 2023 Autumn Statement, the National Insurance (NI) cuts are now in effect as of 6 January 2024, with further cuts for self-employed taxpayers scheduled to arrive 6 April 2024.

For those who can afford it, these cuts to National Insurance rates could present a perfect opportunity to increase your pension over time. A basic-rate taxpayer will in theory see their income rise by up to £62.83 a month, as a result of the NI reduction. If they pay this straight into their pension, it will be worth £78.53 a month because of the 20% tax relief from the Government on contributions. Over time, these contributions could quickly compound into something significant for your future financial security.

Arrange your free initial consultation

What are National Insurance Contributions?

National Insurance (NI) is an umbrella term for universal health care, unemployment benefits and the public pension program.

National Insurance Contributions (NICs) are a form of tax that employees and employers pay to the Government through payroll deductions. NICs are paid automatically through the PAYE (Pay As You Earn) system, which deducts an amount based on a percentage of your income, and this generally continues until you reach retirement age. Employees are able to make additional voluntary payments to increase the pension amount that they will be entitled to receive.

NICs are collected in order to fund various state benefits, such as the NHS and state pensions.

The changes to National Insurance rates

There are three changes to NICs which were announced in the 2023 Autumn Statement. These changes are:

- A cut in the main rate of NICs paid by employees (‘primary Class 1 NICs’) from 12% to 10%. This rate cut applied from 6 January 2024

- A cut in the main rate of NICs paid by the self-employed (‘Class 4 NICs’) from 9% to 8%. This rate cut would apply from 6 April 2024.

- Cancelling the requirement of the self-employed to pay the flat rate NICs charge (‘Class 2 NIC's’), which applies when someone’s annual profit exceeds a set threshold (the ‘lower profits threshold’). This threshold is currently £12,570. This change would take effect from 6 April 2024.

These measures extend and apply to the whole of the UK. All workers earning over the annual national insurance threshold of £12,570 have seen a fall in their national insurance tax bill as of January 2024.

| Annual Salary | NIC's in 2021/2022 | NIC's in April 2022/23 | NIC's in July 2022/2023 | NIC's in 2023/2024 | NIC's in 2024/2025 |

|---|---|---|---|---|---|

| £20000 | £1,251 | £1,340 | £984 | £892 | £743 |

| £30000 | £2,451 | £2,665 | £2,309 | £2,092 | £1,743 |

| £40000 | £3,651 | £3,990 | £3,634 | £3,292 | £2,743 |

| £50000 | £4,851 | £5,315 | £4,959 | £4,492 | £3,743 |

| £60000 | £5,078 | £5,667 | £5,311 | £4,719 | £3,965 |

| £70000 | £5,278 | £5,992 | £5,636 | £4,919 | £4,165 |

| £80000 | £5,478 | £6,317 | £5,961 | £5,119 | £4,365 |

| £90000 | £5,678 | £6,642 | £6,268 | £5,319 | £4,565 |

| £100000 | £5,878 | £6,967 | £6,611 | £5,519 | £4,765 |

Source: Blick Rothenberg.

How the NI cut could boost your pension?

We have calculated that a 25-year-old basic-rate taxpayer who works and saves until they are 67 years old could end up with as much as £118,900 extra in their pension pot. And even if you’re later in life, for a 55-year-old the uplift could be an extra £15,405. So still worth it, no matter at what point you start to make the extra saving. Although clearly the younger you are the bigger the increase to your pension pot.

For higher-rate taxpayers, the figures are substantially higher. The original £62.83 contribution turns into £104.72 because of the 40% tax relief they get. This means that, for example, a 25-year-old higher-rate taxpayer could be as much as £158,550 better off by age 67. For a 55-year-old, there could be an extra £20,543.

There are some caveats to these calculations. The figures assumes no further changes to NI contributions and that these pots grow by 5% before any fees are deducted.

There are also other factors to consider that could increase the final figures such as employers matching or partly matching extra contributions made by employees, resulting in an even bigger pot over time.

Instead of continuing to work until they reach their planned retirement age, if you divert the extra cash into your pension, you could in theory retire from work a few years earlier as an alternative but feasible strategy, giving you more time to enjoy the best years of your retirement.

Due to the NI reduction involving “class 1” contributions made on earnings received by anyone between the age of 16 and state pension age who is getting more than £242 a week from one job, it means that employees now pay 10% on earnings between £242 and £967 a week.

If you’re thinking about your retirement plans, we’re offering anyone a free initial consultation and cash flow analysis worth up to £500 for those with £100 000 or more in pensions, investments and savings to help with retirement planning. Why not get in touch for a free non-committal initial consultation where you can discuss your savings plans with one of our accredited advisers who will be happy to guide you through the process. Alternatively, you can give us a call on 0333 323 9065 to get in touch with a member of our team to find out more.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

The Financial Conduct Authority (FCA) does not regulate tax advice.

New pension opportunities, but you may need to act fast!

In the 2023 Spring Budget, Chancellor of the Exchequer Jeremy Hunt took many by surprise with his chosen policy changes, particularly in regard to pension allowances. Not only was the Annual Allowance increased from £40,000 to £60,000 and the more restrictive Tapered Annual Allowance increased from £4,000 to £10,000, but it was also announced that the Lifetime Allowance would be abolished.

Consequently, and taking into account a looming election and possible change of government, now could be an opportune time to consider whether you are aiming to maximise your pension contributions prior to the end of the current tax year to take advantage of these tax benefits.

Arrange your free initial consultation

What is the Annual Allowance?

The annual allowance is the maximum amount of pension savings an individual can make each tax year without an annual allowance allowance charge applying.

As noted above, from the start of the current tax year, the annual allowance was increased to £60,000, and you can receive tax relief on your personal contributions up to 100% of your relevant UK earnings (including salary, bonuses, commission).

However, high earners could be subjected to a tapered annual allowance, which gradually reduces their annual allowance to a minimum of £10,000 for those with taxable income over £260,000.

Personal pension contributions are eligible for tax relief at an individual’s marginal rate of income tax. This means that a basic rate taxpayer will receive a 20% uplift on the money they contribute to their pension. A higher or additional rate taxpayer can then also claim an additional 20% or 25% via their self-assessment tax form, resulting in an overall potential tax saving of 40% or 45%!

Employer or Company contributions are also paid gross and can receive corporation tax relief as a business expense.

What is ‘Carry Forward’ and does it apply to me?

Unlike with an ISA, whereby if you do not contribute the full ISA allowance of £20,000 by the 5th of April in a given tax year then this unused allowance is lost forever, this rule does not apply to pensions. The Government introduced the carry forward rules in April 2011, allowing individuals to utilise any unused pension annual allowance from the previous three tax years.

Those with a tapered annual allowance can also still use carry forward if they have any unused annual allowances remaining in previous three tax years.

In order to carry forward any unused annual allowance from these tax years, you must:

- Be a member of a UK-registered pension scheme and had a qualifying pension (this does not include the state pension) since the 2020/21 tax year.

- Have used up your entire annual allowance in the current tax year.

- Have remaining unused annual allowance in previous tax years.

- Have sufficient relevant UK earnings in the current tax year for a personal contribution.

Lifetime Allowance & Transitional Protections

Due to the tax advantages of making pension contributions, the Government previously placed a limit on the amount of pension benefits an individual could accumulate over their lifetime, without incurring a tax charge. This tax charge is known as the Lifetime Allowance (LTA) charge and applied to individuals with pensions valued over £1,073,100.

However, with the UK Government announcing that the LTA charge would be removed from 6 April 2023 and then the LTA abolished from 6 April 2024, this means there is an opportunity for those who are near to or who have exceeded the £1,073,100 threshold to consider recommencing pension contributions.

Historically, the Government has provided individuals with the opportunity to apply to protect their LTA before any changes in legislation. Certain types of transitional protection were introduced with the stipulation that you could no longer make any further pension contributions, but this restriction was then also lifted for those with existing protection before 15 March 2023.

Therefore, this has presented another potential opportunity, as those previously unable to make any contributions due to the risk of losing their protection, may have a significant level of unused annual allowance from previous tax years.

Use it or lose it

With wage growth reaching 7.3% for the period between August to October 2023 (according to the ONS), the tax band freeze means people are technically paying more income tax than ever before. Therefore, it would be prudent to look for ways to maximise the tax-efficient legalisation currently on offer.

Aside from the fact that any unused annual allowance from the 2020/21 tax year will be lost after 5th April 2024, there is no predicting if or when changes will be made again to this legislation. It seems as if the UK population collectively hold their breath at the sign of any Budgets which have seen a vast array of changes to pension rules over the years.

Whilst the most recent changes were positive for pension savers, it is important to consider the implications of the impending election in the next 6-12 months; if there is a change in government then this policy change could be reversed. With that and all the above in mind, it is worth exploring your options and taking appropriate action concerning your carry forward allowance; use it before you lose it!

Pensions can be a complicated and daunting matter to navigate, from obtaining the relevant information from your pension providers to a thorough understanding of ever-changing UK legislation. Therefore, please do reach out to a financial adviser if you would like help making the best use of your savings and pension allowances.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

The Financial Conduct Authority (FCA) does not regulate tax advice.