Skip to main content

Skip to main content

Reeves rules out pension lump sum cut

Rachel Reeves will not reduce the tax-free pension lump sum allowance in this month’s Budget, officials have confirmed.

The Treasury has ruled out any changes to the amount individuals can withdraw from their pension without paying income tax, following reports of a wave of withdrawals from pension funds.

Currently, most savers are allowed to take 25% of their pension pot tax-free from the age of 55, up to a maximum of £268,275.

The Chancellor had been considering a cut to the Pension Lump Sum Allowance as a possible way to help fill a gap of up to £30 billion in the public finances.

The Fabian Society, a well-known think tank aligned with Labour, had recommended reducing the tax-free lump sum to £100,000. This was a proposal Ms Reeves also weighed up ahead of last year’s Budget. Torsten Bell, the Pensions Minister, had previously supported lowering the limit to just £40,000.

The Chancellor’s refusal to rule out changes last year led to a sharp rise in pension withdrawals. In 2024-25, savers withdrew more than £70 billion from their retirement pots, an increase of 36% compared to the previous year.

However, Treasury officials have now confirmed to The Telegraph that Ms Reeves will not make any changes to the limit when the Budget is announced on 26 November.

The confirmation comes after reports that many retirees were acting early to access their funds in fear of a potential tax increase.

What is the Lump Sum Allowance?

The Lump Sum Allowance is one of the three new allowances which were introduced following the abolition of the Lifetime Allowance on 5 April 2024.

In simple terms the Lump Sum Allowance limits the overall amount of tax-free lump sums you can take from your pension funds during your lifetime.

For most people this lifetime limit is £268,275.

This does not mean you can take all of your pension pot as a tax-free lump sum if it is worth less than £268,275, as there are rules in place that limit the tax-free amount you can receive to either 25% of the value of the pension pot you are crystallising, or £268,275 – whichever is the lower figure.

If you’re interested in how to manage you pension withdrawals to ensure the best possible outcome for you and your family, we can help. Give us a call on 0333 323 9065 or book a free non-committal initial consultation with a member of our team to find out more.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

What to expect from the Autumn Budget 2025

Rachel Reeves will deliver her second budget on 26th November 2025, and with speculation mounting regarding the potential changes, it can be hard to cut through the noise and make good decisions about what action to take, and importantly, not to take.

What is likely to be in the Autumn Budget?

Speculation has been rife about potential changes in a number of areas, so what might these changes look like?

Arrange your free initial consultation

Pensions

As has been the case in previous years, a reduction in individuals’ tax free cash entitlements is rumoured once again to be in the Autumn 2025 budget. These rumours have been fuelled by reports that Pensions Minister Torsten Bell, who in 2019 had stated that the tax free lump sum should be limited to £40,000, had been appointed as a key aid for the Chancellor ahead of the budget. However, while a change is of course possible, it is important to note that:

- When tax free cash has been reduced before (by reductions to the then Lifetime Allowance), protections (such as Fixed Protection 2012, 2014 and 2016) were put in place to ensure individuals who had already built up pension savings were not disadvantaged.

- The current Labour government previously tried to reinstate the Lifetime Allowance, which the previous Conservative government had scrapped. However, the government abandoned these plans when they realised it was unworkable to exclude Doctors (who had been retiring due to the high tax rates they were subjected to through a combination of the lifetime allowance and the annual allowance) from the Lifetime Allowance tax charge. Having now finalised legislation around the Lump Sum Allowance, a further change affecting Doctors’ pensions could prove very unpopular.

- Pension legislation notoriously takes months or years to finalise, as was the case with the recent Lump Sum Allowance (LSA) changes and as is currently the case with the legislation which will bring pensions into scope for inheritance tax from April 2027. This could indicate any reduction may come into force at a given date in future, rather than with immediate effect.

To make a change ‘overnight’ would be administratively difficult for pension providers.

Capital Gains Tax (CGT)

Despite the administrative issues associated with implementing an overnight change as outlined above, one change that was brought in with immediate effect in last year’s budget was an increase in the main rate of capital gains tax from 10% to 18% for basic rate tax payers and 20% to 24% for higher rate tax payers. These increases weren’t as substantial as some thought they would be, so there is the possibility of further increases. However, there are question marks over how much revenue such an increase would actually raise given individuals can simply choose to stop selling their assets.

Inheritance Tax (IHT)

This is the area that saw arguably the biggest changes in the 2024 budget with:

- Pensions brought into scope for inheritance tax purposes from April 2027

- Business Relief and Agricultural Relief limited to £1m per person and 50% of the full rate thereafter

- AIM shares Inheritance Tax Relief limited to 50% of the full rate

The government may see the estimated £5.5 trillion of wealth that is expected to be passed down from ‘Baby Boomers’ over the next two decades (known as the ‘Great Wealth Transfer’) as a target for additional taxation. This could include a tax on gifting (currently gifting to individuals is unlimited if the donor lives 7 years from the date of the gift) or a reduction in the tax free allowances available on death (for example the removal of the Residence Nil Rate Band – RNRB). For this reason, those considering making a gift in the not too distant future could consider making the gift before the budget, though only if the implications of this on their overall financial situation are fully understood.

ISAs

There are rumours that there will be a reduction to the Cash ISA allowance. However, a cut to the Stocks and Shares ISA allowance is perhaps less likely given Reeves spoke positively about Stocks and Shares ISAs in her Mansion House speech in July.

Salary Sacrifice

This is the ability for employees’ pension contributions to be paid directly into their workplace pensions, reducing both employer and employee national insurance contributions. Limiting or removing the ability to do this could raise significant revenue for the government without them needing to renege on their manifesto commitment not to increase tax on working people (income tax, national insurance or VAT).

Other rumours

Other recent rumours include:

- An increase in tax with a corresponding reduction in National Insurance. This could in theory raise revenue without raising tax on ‘working people’, with landlords and pensioners instead footing the bill.

- A further freezing of income tax bandings. Though this is described by many as a stealth tax as it means more and more individuals will move into higher tax bandings over time, these have been frozen since 2021/22 until 2028 and an extension of this freeze to 2029/30 could raise an estimated £7bn p.a.

- A tax on Limited Liability Partnerships (LLPs) favoured by Solicitors, Accountants and Doctors, as such arrangements allow individuals to be self-employed and not subject to employer’s national insurance contributions.

- A windfall tax on banks, though the Chief Executive of Lloyds Banking Group Chalie Nunn argued this would impact banks’ ability to lend.

An increase in gambling taxes, though the Chairman of Betfred Fred Done has stated all its shops on UK high streets could close if the rumoured changes were implemented.

When does the Autumn budget take effect?

Though the budget will take place on 26th November 2025, most changes are expecting to come into effect from the next tax year on 6 April 2026 and beyond.

What can you do to protect your wealth?

In an environment where taxes are increasing, it is becoming more and more important to:

Utilise the various tax allowances that are available to you and your family, for example:

- Your ISA allowances

- Your pension contribution allowances

- Your capital gains tax, savings and dividend allowances

- Your personal income tax allowance.

Have a plan in place with diversified sources of income and investments. This way you can adapt your plan as a result of any changes in the budget.

In summary, it is clear that the state of public finances mean taxes will need to increase in the upcoming budget and Labour’s manifesto commitment not to increase tax on ‘people working’ has led to mounting speculation that changes will be made to a number of different areas. These headlines are usually followed by a quote from a leader within the industry in question stating how the tax increase would be devastating for that industry and how the government should look elsewhere. As Private Eye’s headline from September rightly stated: ‘Raise taxes for other people’, agrees everyone, so some difficult decisions will need to be made.

To consider the potential impact of the budget on your overall financial situation, please get in touch or contact your TPO Adviser.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning or tax advice.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age).

The value of your investments (any income derived from them) can go down as well as up, so you could get back less than you invested. This could also have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.

Autumn Budget 2025: your go to guide

When is the Autumn Budget?

As we head into the final months of the year, attention is turning towards one of the key economic milestones, the Autumn Budget. Scheduled for 26th November this year, the Budget is an essential part of the financial calendar, not just for policymakers and economists, but for households, businesses and advisers to understand the direction of travel.

Arrange your free initial consultation

While every Budget matters, the stakes feel especially high this year. The economic outlook remains uncertain, government borrowing costs have rocketed, and a growing number of taxpayers are already feeling the pain from continued frozen allowances and the changes announced in last year's Budget.

So, what exactly is the Autumn Budget for, and why is it such an important event?

Understanding the Budget’s role

The Autumn Budget is the government’s main opportunity each year to set out its plans for taxation, public spending and economic strategy. It’s when the Chancellor outlines how the government will raise and allocate money in the year ahead, usually supported by economic forecasts from the Office for Budget Responsibility (OBR).

These forecasts cover everything from inflation and interest rates to borrowing, debt levels, and projected economic growth, all of which shape the decisions being made in the Budget itself.

The Autumn Budget is often accompanied by a Spending Review, which sets departmental budgets for the medium term, though not necessarily every year. In contrast, the Spring Statement, usually delivered in March, tends to be lighter, more of an economic update than a full fiscal event, though it can include policy changes when needed.

In recent years, the Autumn Budget has become the main fiscal moment of the year. The Spring Statement, while still useful, is generally more reflective in tone. Some recent commentary has suggested that the government may be considering a move to just one formal fiscal event per year, but as of now, the current two-event framework remains firmly in place.

Raising revenue by stealth

One of the most effective tools for raising revenue in recent times has been the simple decision to freeze tax thresholds and allowances, rather than increase them in line with inflation. This is often referred to as “fiscal drag” or stealth tax.

The concept is straightforward. When income tax thresholds stay fixed, but wages rise, even modestly, more people are pulled into higher tax bands. Likewise, with allowances reduced for capital gains or frozen for inheritance tax, for example, more estates and investments gains become taxable over time.

These quiet changes can bring in billions in additional revenue without altering headline tax rates, and they’ve become a central part of the government’s fiscal approach. The freeze on the personal allowance and higher-rate income tax threshold began in 2021 and is currently extended to at least 2028, with rumours this could be further extended in the coming Budget.

For financial planning, this makes the Autumn Budget a critical event. It’s not just about new taxes or reliefs being introduced or withdrawn; it’s about understanding how existing policies evolve by, some cases, staying exactly the same.

How will the Autumn Budget affect me?

With the Autumn Budget fast approaching, attention is turning to what the Chancellor might announce this time around.

While nothing is confirmed, early speculation includes:

- An extension of existing tax band freezes, particularly income tax and inheritance tax thresholds

- Restrictions on pension tax reliefs or changes to contribution limits

- Restrictions on the tax-free cash available from pensions, though it is important to remember when the tax-free lump sum has been reduced before, protections were put in place to ensure individuals who had already built up savings in their pensions were not disadvantaged.

- Property tax reforms, potentially around stamp duty or council tax

- ISA reforms, possible reduction in the Cash ISA allowance

This is purely speculation at this point so it’s advisable not to make rash decisions before knowing exactly what the outcome will be. However, given the current economic environment, including sluggish growth and high debt interest costs, the government has limited room to manoeuvre, so sadly it’s wise to be prepared. Potentially, if there were financial decisions you were planning to make anyway, that could possibly be impacted by the Budget, now could be the time to make them.

How we can help

Whether you're a business owner, investor, retiree or employee, the Autumn Budget can affect you in ways both obvious and subtle. Whether through active policy changes or passive revenue generation via fiscal drag.

We’re following developments closely now and in the run-up to November’s announcement. We’ll be keeping these pages updated with the latest news, including on the day of the Budget with a full run down of all the announcements

In the meantime, if you’re concerned in anyway how the Budget may affect your finances, why not get in touch and see if we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

FAQs

No, the money you receive through equity release is not classed as income, so it is not subject to income tax. However, using equity release could affect your entitlement to means-tested state benefits, and it’s important to consider the wider impact on your finances.

When you die or move into permanent long-term care, the equity release loan becomes repayable. This is typically settled from the sale of your home. Any remaining value after the loan and interest have been repaid will go to your estate and be passed on to your beneficiaries.

Should I withdraw money from my pension before the Budget?

A growing number of pension savers are taking action ahead of the Budget in November 2025 as concerns mount that Chancellor Rachel Reeves may target pensions in a bid to raise revenue. The most significant fear being a reduction—or even scrapping—of the 25% tax-free lump sum.

New figures from the Financial Conduct Authority (FCA) showed that £70bn was withdrawn from pension pots in the tax year 2024/2025 which was an increase of 36% on the previous tax year. But it was tax free cash that saw the biggest jump in withdrawals, with £18.3bn withdrawn, up 62% on the previous year. While some are taking early action as part of planned retirement or inheritance strategies, others may be reacting to speculation and that may carry its own risks.

Arrange your free initial consultation

So, what’s really happening, and what should pension savers consider before making any, potentially rash, decisions?

Is 25% tax-free cash under threat?

One of the most cherished benefits of pension saving is the ability to withdraw 25% of your pension pot tax-free from the age of 55 (rising to 57 from April 2028). This feature is often a key part of retirement planning, offering a welcome financial boost in early retirement years.

However, there has been much speculation in the media that this benefit could be in the Chancellor’s sights. Given the growing cost pressures on the Treasury and the need to balance the books, the Government may see this as a politically tolerable way to raise funds, especially if positioned as a move to make the system “fairer” or to close “tax loopholes.”

Some rumours have hinted that the allowance could be capped or means-tested, while others believe it could be scrapped altogether for higher earners. Though nothing has been confirmed, it has been enough to make many savers act early.

Why are people withdrawing pension money now?

A major driver of this accelerated activity is likely inheritance tax planning. Many people have used pensions as estate planning vehicles because, under current rules, unused defined contribution pensions can often be passed on to beneficiaries tax-free if the saver dies before age 75 (and pre-2027), or at their beneficiaries’ marginal income tax rate after that age.

Whilst pensions were not designed to be passed on tax-free, this became a feature only with the pension freedoms introduced in 2015. It would appear that the Government now sees this an unintended generosity hence changing the rules from April 2027.

Major factors potentially driving this trend:

- ‘Lock in’ current rules: By taking their tax-free cash early, even if they didn’t need the money immediately.

- Support for adult children: In a cost-of-living crisis, many parents are using their pension pots to help their children buy homes, support education, clear debts, or simply get by.

- Impending legislation: Known changes are coming in April 2027 that will bring most pensions into a person's estate for inheritance tax purposes making their longer-term benefit less tax efficient, as such some are accelerating inheritance tax planning through gifting.

- Desire to see the benefits: More people may be choosing to gift during their lifetime to witness the impact their money can have, rather than waiting until after death.

The HMRC crackdown: Watch out for re-contributions

However, pension savers must tread carefully. HMRC have confirmed that they are now targeting people who have withdrawn pension funds and then tried to re-contribute the money. This often happens when people access cash “just in case” and later realise they didn’t need it.

HMRC is treating these “recycling” activities as unauthorised payments, and in some cases is issuing penalties of up to 70% of the amount re-contributed.

This crackdown should act as a serious warning: pension planning must be done properly and ideally with advice. Knee-jerk decisions based on speculation or panic can come at a very high price.

So, should you withdraw your tax-free cash now?

Plan, don’t panic, is the key. The temptation to act quickly in light of Budget rumours is understandable but the best outcomes come from measured, strategic financial planning, not reacting to headlines.

Yes, the landscape may change. But making major pension decisions without understanding the long-term impact could create bigger problems down the line, particularly if HMRC penalties counteract any tax saving you set out to achieve. The smarter move? Review your financial and estate plan now, not later. If you’ve already been considering gifting or restructuring your assets, this could be the right time. Equally if you were planning to take your tax-free cash soon, anyway, now could be a good time. But don’t make a move based on speculation and what might happen. Ideally, speak to a qualified financial adviser who understands your full situation.

Because while Budget speculation may be out of our control, how we plan for our financial future isn’t.

Inheritance planning tips

If you're considering how to manage your pension and reduce your estate for IHT purposes, here are a few strategies to consider:

- Use spouse exemptions: Transfers between spouses are free from IHT. Consider aligning pension and estate planning as a couple.

- Gift excess income: Regular gifts from excess income (not just capital) can be IHT-free if documented properly and as part of a regular pattern

- Use other allowances: Don’t overlook the £3,000 annual gifting exemption or small gift allowances.

- Lifetime gifting: Gifts survive the 7-year rule for IHT purposes if you live long enough, so starting earlier has advantages.

- Consider life insurance: A whole-of-life policy written in trust can provide a tax-free lump sum on death to help cover an IHT bill.

- Don’t rely solely on pensions: A balanced approach using ISAs, property, other tax incentivised products, and trusts may be more resilient against future rule changes.

For this any many more tips on how we can improve you and your family’s financial future, why not get in touch for free initial consultation.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The value of your Investments and the income derived from them can fall as well as rise and you may get back less than you originally invested.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

HMRC responds to surge in pension withdrawals with cautionary warning

HM Revenue & Customs (HMRC) has warned savers not to act impulsively with pension withdrawals ahead of the upcoming November Budget.

This message is aimed at those savers who might look to take advantage of the 30-day cooling-off periods to request withdrawals but with the option of putting them back again within 30 days, should the Budget leave the current rules unchanged.

Now HMRC have said pensioners who took out their lump sum after December 5 2024 and put the money back in, within the 30 days, could be pursued by the tax man with each cash reviewed on a "case-by-case" basis.

They clarified that once a tax-free lump sum has been paid, it cannot be reversed, even if the cancellation period is still open.

In its latest update, HMRC has reiterated that these 30-day windows do not provide any tax exemptions, meaning those who took and then returned their tax-free lump sums since December 5 last year are potentially facing charges of 55% in most cases, and up to 70% in others.

“Once lump sums are paid, the associated tax consequences (including the use of the individual’s lump sum allowance and lump sum death benefit allowance) cannot be undone, even if the payment is returned or cancellation rights are exercised” said HMRC.

62% rise in those accessing tax free cash lump sum?

Most pension savers have the option of withdrawing up to 25% of their pension, tax free. Many pensioners choose to take a lump sum to clear mortgages or help children with university costs, but after reports last year that Chancellor Rachel Reeves was considering reducing the tax-free allowance to £100,000, many savers rushed to access their money early, with tax-free pension lump sum withdrawals rising significantly amid fears this allowance could be reduced or scrapped completely.

Figures from the Financial Conduct Authority (FCA) show pension withdrawals rose by nearly £20 billion in the 2024/25 tax year compared with the previous year.

The amount of money withdrawn from pensions jumped by almost 36% in 2024/25, with savers taking out £70.9bn compared to £52.2bn the previous year, according to the FCA’s latest Retirement Income Market Data. Of this, £18.3bn was tax-free cash, an increase of 62% on the £11.3bn the previous year.

The latest data showed that just shy of one million pension plans (961,575) were accessed for the first time during the year, up 8.6% on the amount accessed in 2023/24.

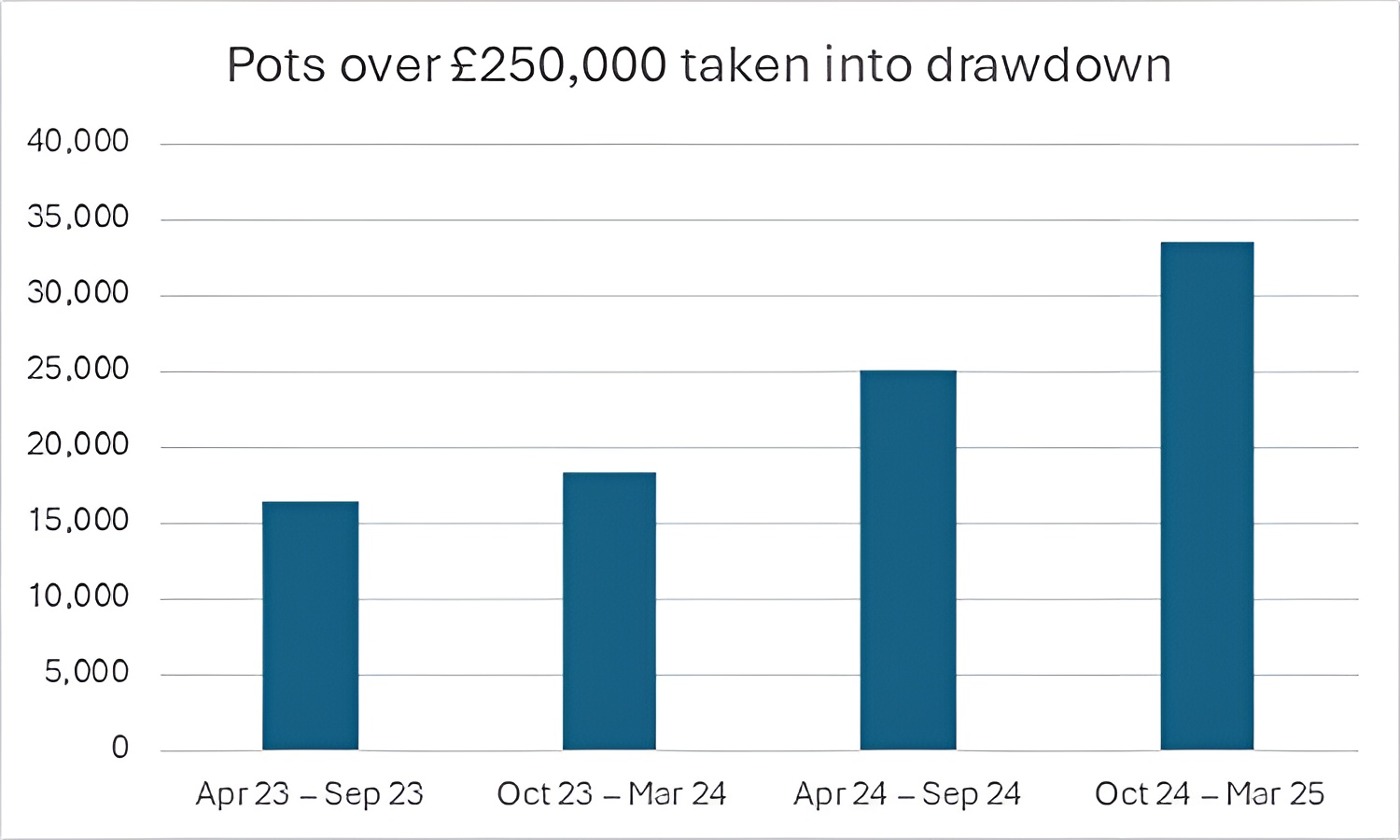

Figure 1: Pots over £250k taken into drawdown, Source: FCA, 2025

The FCA data also showed that the number of pensions being accessed without regulated advice had grown, with only 30.6% of pension plans accessed for the first time in 2024/25 being taken with regulated advice, slightly down from 30.9% the previous year.

If you’re concerned about the Budget or simply want to discuss the best way to plan for your retirement, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our qualified and regulated financial advisers to find out how we might be able to help you.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.

HMRC makes it tougher to claim pension tax relief

The UK tax authority is increasing scrutiny of pension tax relief claims made by higher earners in an effort to “protect taxpayers’ money,” as part of a broader initiative to boost revenue collection.

HM Revenue & Customs (HMRC) announced on Thursday that starting September 1st, it has “lowered the threshold” at which claimants must provide evidence to support their pension tax relief requests. In addition, claims can no longer be made by phone and must instead be submitted online or by post.

Last year, the Labour government pledged an additional £555 million annually in HMRC funding, aiming to generate an extra £5 billion in yearly tax revenue by the end of this parliament.

HMRC said it is reducing the evidence threshold for personal pension tax relief claims following a review that found “many claims below the current evidence threshold were incorrect.” The move, it said, is intended to “protect taxpayers’ money.”

Each year, around 80,000 personal pension relief claims are submitted. HMRC’s review of claims under £10,000 showed that one in three required the claimant to amend the amount claimed.

What is pension tax relief?

Pension tax relief is a government incentive that helps you save more efficiently for retirement by reducing the tax you pay on your pension contributions. When you pay into a pension, some of the money that would have gone to HMRC is instead added to your pension pot.

If you're a basic-rate taxpayer (20%), contributing £80 means the government tops it up with £20, so £100 goes into your pension. Higher-rate taxpayers (40%) and additional-rate taxpayers (45%) can claim back even more through their self-assessment tax return, reducing the real cost of saving even further. It’s one of the most tax-efficient ways to build your retirement fund.

Tax relief is often financially beneficial, but it is important to remember that there are limits and restrictions. For more information, check out our article on how to be tax efficient with your pension contributions.

What’s changed?

HMRC has made a few changes to claims for tax relief on personal pension contributions which came into effect on 1st September. Below are some of the key changes.

- All pay as you earn (PAYE) claims for pension tax relief must be made online or by post and must be supported by evidence from the pension provider or employer.

- HMRC will not accept claims made via the telephone.

- All claims must be made using HMRC’s online service or by letter; and all claimants need to provide evidence in support of their claim.

Prior to 1 September 2025, only those claimants who met the conditions set out in HMRC’s guidance were required to provide evidence. The evidence required is a letter or statement from the pension provider or a payslip from the employer showing:

- The claimant’s full name;

- Details of the pension contributions paid and the tax year they relate to; and

- Where the claim relates to a workplace pension, that the claimant received 20% tax relief automatically from their employer.

- Evidence needs to be provided for each tax year that a claim is made for.

For more information please read further on gov.uk.

If you want to find out more about how you can make the most your pension tax reliefs and allowances, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our chartered advisers to find out how we might be able to help you.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash planning or tax advice.

Pension uplift as triple lock holds

Millions of pensioners across the UK are expected to receive a state pension rise of 4.7% next April, a figure that exceeds inflation and could place further strain on public finances just as Chancellor Rachel Reeves considers potential tax increases in the upcoming Autumn Budget.

Labour has pledged to maintain the state pension triple lock, which ensures payments rise each year by whichever is highest out of 2.5%, inflation in September, or average earnings growth over the three months to July.

New data released this week shows that average weekly earnings, including bonuses, were 4.7% higher between May and July compared to the same period last year. With September’s inflation figure currently sitting at 3.8%, experts believe the earnings growth measure will set next year’s state pension increase.

The Government will confirm the final uplift ahead of the Budget, but Work and Pensions Secretary Pat McFadden reiterated Labour’s commitment to the triple lock on Tuesday.

“That’s a commitment from the Labour government to the UK’s pensioners,” he said. “It’s something that we said we’d do at the election and something that we will keep to.”

The confirmation that the triple lock will be upheld has come as a relief to many as there had been rumours that it might be abandoned as another part of Labour’s tax campaign.

The ‘Triple Lock’ explained

The ‘triple lock’ refers to a well-known state pensions policy that ensures state pensions rise every year by either the average earnings growth, inflation (as measured by the Consumer Prices Index) or a flat 2.5% - whichever is highest that year, hence the name ‘triple’ lock.

It was designed in principle to make sure that state pension value would always have the best growth outcome each year for pensioners. The guarantee that the highest of the three will be what pensions grow against ensures that savers have three layers of protection against inflation, hence the name ‘triple lock’. This is incredibly important in maintaining a level of healthy financial security for those relying on their pensions, as it guarantees growth irrespective of how volatile the economy becomes.

If you want to find out more about retirement planning, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our chartered advisers to find out how we might be able to help you.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Advice or Guidance? Why it matters

The terms advice and guidance are often used interchangeably when it comes to financial matters, but in reality, they are very different. And in today’s fast-changing financial landscape, understanding this difference is essential.

Since the introduction of the Pension Freedoms in 2015, individuals have had greater control over how and when they access their defined contribution (DC) pension pots. In response, the government established services to offer free, impartial guidance aiming to help people aged 50+ understand their options and avoid costly mistakes.

Arrange your free initial consultation

One such service is the MoneyHelper platform, provided by the Money and Pensions Service (MaPS), previously known as Pension Wise. The idea was (and still is) to ensure people receive basic, unbiased information before making decisions about their retirement income.

As UK Pensions Minister Guy Opperman put it, “We will introduce new provisions requiring trustees of occupational pension schemes to nudge members to appropriate guidance when they seek to access their pension through the pension freedoms.”

This “nudge” while helpful, begs the question: is general guidance really enough when you're making decisions about what could be hundreds of thousands of pounds of lifetime savings?

What’s the difference between guidance and advice?

Guidance

Guidance is all about information rather than recommendations that are specifically tailored to your situation. It helps you better understand the options available, but the responsibility to decide and act lies entirely with you.

Government services like MoneyHelper for example, or your pension provider’s website may offer generalised content, online tools, or telephone support to guide you through the basics of pensions, investments, or budgeting.

In fact, anyone, including friends or colleagues, can technically give “guidance”. But remember, they aren’t liable for the outcome, and you're not protected if things go wrong.

What you won’t get from guidance:

- Personalised recommendations

- Product suggestions

- A risk assessment of your circumstances

- A regulated professional who is accountable for their advice

Advice

Advice, by contrast, is personal, specific, and regulated. When you take financial advice, you're working with a qualified and authorised Financial Adviser who assesses your entire financial situation, whether that be your goals, risk tolerance or future plans, then recommends a course of action tailored to you.

You’re also protected. Advisers are regulated by the Financial Conduct Authority (FCA) and must adhere to strict standards. If something goes wrong, you may have access to the Financial Ombudsman Service and Financial Services Compensation Scheme.

What about the cost? And is it worth it?

Guidance is usually free and is offered by government-backed services or your pension/investment provider, for example. It’s a good starting point, especially if you just want to understand your options or educate yourself.

Advice, however, is a paid professional service, and like any other expert service, the cost reflects the time and complexity involved.

There are two main types of advisers:

- Independent Financial Advisers (IFAs), who offer whole-of-market advice across a full range of products and providers. All our advisers at The Private Office are Independent Financial Advisers.

- Restricted Advisers, who are limited in the scope of advice they can give, often tied to a particular provider or product range.

Choosing the right type of adviser can significantly impact your financial outcomes. Independent advice means you're more likely to get the best solution for you rather than for the adviser’s institution.

The rise and possible risks of AI in financial guidance

A key change in the advice landscape is the increasing use of Artificial Intelligence (AI), particularly Large Language Models (LLMs) like ChatGPT and other advanced systems.

Using LLMs as a substitute for regulated financial advice carries several risks. To be balanced, however, on one hand, there are benefits, including speed, ease of access and lower (or no) cost. But the pitfalls are real and therefore need to be carefully considered.

Here are some of the potential risks:

- Inaccuracy & outdated / partial information

LLMs may rely on data that is not fully up to date, or doesn’t reflect recent regulatory, tax or product changes. They also generate plausible‑sounding but false or misleading information, known as hallucinations, from time to time. - Lack of holistic view

AI tools typically only see what you tell them. They can’t pick up life‑events you haven’t mentioned, emotional preferences, long‑term goals, or unexpected future needs. A human adviser can ask probing follow‑up questions to uncover things you may not have thought to tell them. - No regulatory protection

Advice from AI tools is not regulated in the way financial advice from an FCA‑authorised adviser is. If things go wrong, there is no ombudsman to make claims, no compensation scheme, and no requirement that those giving the advice act in your “best interests.” - Overconfidence & misplaced trust

Because LLMs are good at generating fluent, confident text, people may overestimate their reliability. - Potential for financial loss

Applying generic or inappropriate advice could cost money e.g. picking wrong investment vehicles or mismanaging tax implications.

The value of advice is still stronger than ever

It can often be a daunting task for individuals to think about their financial futures. Working with a qualified financial adviser can help to alleviate the burden of worry, become better educated on their finances and receive actionable advice on how to improve their situations.

An update to the International Longevity Centre’s research showed the long-term value of advice:

- Advised individuals can be up to 24% better off after a decade compared to those who don’t take advice.

- The benefits are especially strong for those with modest wealth, proving that advice isn't just for the wealthy.

- Those who seek advice regularly (e.g. annually) see even stronger outcomes over time.

In Summary – Guidance vs Advice

| Guidance | Advice | |

|---|---|---|

| Cost | Free | Fee-based |

| Personalised? | No | Yes |

| Regulated? | No | Yes (FCA) |

| Recommendations? | No | Yes |

| Protection? | None | Yes - Ombudsman Compensation Scheme |

| Provided by? | Government, websites, AI, providers | Regulated Financial Advisers |

You get what you pay for, and when it comes to your lifetime savings and financial future, that advice could make all the difference.

Start with a free, no-obligation consultation

If you’re thinking about the next stage in your financial journey and want trusted, independent advice, get in touch to arrange your free consultation with a qualified adviser.

At The Private Office, we offer chartered, independent, whole-of-market advice, recognised as the gold standard in the industry. If you have £100,000 or more in pensions, savings or investments, you can start with a free initial consultation (worth £500) with one of our regulated Financial Advisers.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice or cashflow modelling.

Living to 100 years - are you financially prepared?

The prospect of living to 100 is a concept that has evolved from a distant dream into a tangible reality for a growing number of people. While modern medicine and healthier lifestyles have made it possible to live longer, the question of whether our finances can keep pace with our longevity is a critical one. For many, the traditional notion of retirement at 65 followed by a relatively short period of relaxation is a thing of the past. The increasing life expectancy coupled with the complexities of the modern world are prompting us to rethink our financial futures. The challenge is not just to live a long life, but to ensure that it is a comfortable one, free from financial worry.

Arrange your free initial consultation

The changing landscape of retirement

The traditional retirement we all plan for is undergoing a significant change. The dual factors of increasing life expectancy and the recent rising cost of living have turned the conventional wisdom on its head. Retirement is no longer a fixed point in time but a new phase of life that could span thirty or even forty years. This extended period requires a more robust financial plan than was previously necessary. The era of retiring and simply living off a single fixed income for life is fading, as we all look forward to a longer and in many cases more active retirement.

Instead, individuals are seeking a diverse stream of incomes from various sources to support a new, longer retirement. This could include a combination of pensions, investments, and even part-time work to supplement savings. The rise of the gig economy and flexible working arrangements has also enabled more people to continue earning a living well into what would have traditionally been considered their retirement years. This shift in mindset is not just about necessity; it is also about a desire to remain active and engaged with society.

What you need to live on

The figures from the Office for National Statistics* reveal that the number of centenarians in England and Wales has reached a record high. This demographic shift has important implications for financial planning. It means that the pension pot we build during our working lives may need to stretch for an additional two decades or more. Consider the difference a single decade can make. Our calculations highlighted that a couple needing an income of £25,000 per year from their pension pot only may need a pension value of around £425,000 for a retirement that lasts 20 years, but that same couple would need an additional £159,000 just to last them until the age of 100. The reality for many is that the state pension alone provides a basic safety net but falls well short of supporting a comfortable lifestyle in retirement.

As we look at the latest Retirement Living Standards** data from the Pensions and Lifetime Savings Association, or PLSA, it becomes clear that building your own wealth is crucial. For a single person to achieve a minimum standard of living, which covers all their basic needs with some left over for fun, they would require an income of £13,400 a year. To reach a moderate standard, allowing for more financial security and flexibility, the figure rises to £31,700 a year, while a comfortable lifestyle requires an annual income of £43,900. For a two-person household, the figures are £21,600 for a minimum standard, £43,900 for a moderate one, and £60,600 for a comfortable lifestyle. This is a clear reminder that we need to take control of our financial futures and ensure that we are saving enough for the lifestyle we desire in retirement.

The family factor

As financial pressures grow, an increasingly common phenomenon is the 'bank of mum and dad'. While it might seem like a simple way to help a child get onto the property ladder or pay for a grandchild's education, the financial support offered to the younger generation is putting a significant strain on the retirement savings of their parents. Many well-meaning parents are using their own hard-earned pension pots to assist their children and in doing so are affecting their own financial security.

This act of generosity can inadvertently create a new layer of risk for their own retirement plans. The money that was carefully set aside for their later years is being used for immediate family needs, reducing the total wealth available to them when they stop working. This places even greater importance on having a comprehensive and forward-looking financial plan that accounts for both your own needs and the needs of your family, without compromising your own long-term wellbeing. This intergenerational financial pressure highlights the need for a holistic approach to financial planning, one that considers the entire family's financial health and requirements, not just that of the individual.

Planning for the future

For most people, the idea of living to 100 is intimidating from a financial standpoint. The question of whether you can afford to live that long often feels like a difficult one to answer. This is where the true value of financial planning comes into its own. At its heart, financial planning is not just about numbers; it is about providing peace of mind. A good financial plan will provide a clear and concise visual picture of your financial future, helping you to understand the impact of your decisions on your wealth over time.

For us at The Private Office, cash flow planning is central to how we work with our clients. We begin by gaining a deep understanding of your current financial situation, including all your sources of income, capital and your expenditures. We use this detailed information to create a dynamic cash flow model that illustrates what your financial future might look like for you under different scenarios. This approach allows us to test your wealth against potential events like a market downturn, higher than expected inflation, a long-term health issue, or unexpected expenses. It also gives us the opportunity to see how your wealth can support you to achieve your life goals such as funding your children’s education, renovating your home, or retiring earlier than planned. By providing this comprehensive visual overview, we can work together to ensure you have the financial freedom to live a long and fulfilling life.

Use our retirement calculator

No one has a crystal ball. But what you do have is a range of tools that can help you understand whether your plans are on track. Our retirement calculator is one of the most useful, especially if you’re hoping to retire at 55.

By inputting your current savings, your target retirement age, and the income you’d like to receive, our retirement calculator can provide an estimate of how long your money might last – and what you’d need to contribute to reach your goal.

Retirement Calculator

A useful tool to get a basic understanding of what your future retirement plans look like is our retirement calculator. From your own personal circumstances , you will be able to forecast an estimate of the pension income you will get when you retire and receive a target retirement income to aim for based on your choices.

It’s important to remember that these tools are only as accurate as the assumptions they’re based on. Investment growth, inflation, life expectancy and future tax rules are all variables. But using a calculator is an excellent way to create a picture of what your retirement might look like – and how close you are to achieving it. This is not guaranteed and is for illustrative purposes only.

How we can help you

A comprehensive financial plan allows you to make informed decisions about your future with confidence and clarity. Living to 100 may seem like a distant challenge, but with the right financial planning and advice, it is a future you can look forward to. We’re offering anyone with £100,000 or more in savings, pensions or investment a free retirement review, worth £500. Why not get in to speak to one of our team for a free initial consultation.

Sources:

* Office for National Statistics

** Retirement Living Standards

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

The Financial Conduct Authority (FCA) does not regulate tax advice or cashflow modelling.

How much should you save for retirement?

For many people, retirement is no longer a fixed date, but a gradual process shaped by lifestyle choices, financial goals, and personal wellbeing. There’s no one-size-fits-all answer to how much you should save for retirement, but with thoughtful planning and the right strategy, you can move forward with clarity and confidence.

Understanding your future financial needs and the options available for building a retirement fund is essential, particularly if you hope to maintain a moderate or comfortable standard of living in your later years.

Arrange your free initial consultation

While the concept of retirement has evolved, the fundamentals remain the same, at some point, you will need to replace your employment income with alternative sources. These might include a personal pension, workplace pensions, savings, investments, or property income. For those who are already financially secure or moderately wealthy, retirement planning is not about meeting basic needs but maintaining current standard of living, financial independence and, in some cases leaving a legacy.

What lifestyle do you want in retirement?

One of the most personal aspects of retirement planning involves envisioning the lifestyle you hope to enjoy once you stop working. You may be considering whether to remain in your current home or downsize, whether to travel more frequently, spend additional time with family, or pursue hobbies that could come with added costs. These lifestyle choices will significantly influence the level of income you will require in retirement and should be central to any long-term financial planning.

The Pensions and Lifetime Savings Association (PLSA) provides useful guidelines through its Retirement Living Standards, which outline three levels of retirement living: minimum, moderate, and comfortable. According to the most recent figures, a single person would need around £13,400 per year for a minimum standard of living, £31,700 for a moderate one, and £43,900 for a comfortable retirement. For couples, these figures rise to £21,600, £43,900 and £60,600 respectively. These figures include essentials such as food and utilities, as well as extras like holidays and leisure activities, depending on the lifestyle level.

If your retirement plans include enjoying leisure activities, occasional travel, maintaining a comfortable lifestyle, or supporting family, you may be aiming for a retirement standard that goes beyond simply meeting basic needs. Planning for this level of financial independence requires a considered approach to saving, investing, and managing financial assets effectively over time.

How much will you need to retire?

Translating lifestyle aspirations into a target retirement fund can be challenging. Many people underestimate how long they will live or how much income they will need to maintain their lifestyle. While the commonly cited guideline of needing two-thirds of your pre-retirement income can offer a useful starting point, it should be treated as a general reference rather than a definitive rule. A personalised approach, based on your unique circumstances and aspirations, is essential for effective retirement planning.

Cash flow planning is a core element of retirement preparation and a key tool we use at TPO. It provides a detailed view of how your finances are expected to evolve over time by projecting income sources alongside anticipated expenses. This allows you to identify potential shortfalls, prepare for significant future costs, and ensure your savings and investments are structured to support you throughout retirement.

By modelling different scenarios, cash flow planning helps clarify complex decisions, such as how, when and where to begin drawing down on your wealth, how to adjust spending as your needs and circumstances change. It offers a dynamic framework for making informed choices and adapting your financial strategy over time.

In essence, cash flow planning acts as a financial roadmap. It gives you visibility and control, helping you maintain stability and confidence while pursuing the lifestyle you want in retirement.

At TPO, cash flow planning is a vital part of retirement preparation, and our models are designed to be ultra cautious. They account for realistic, but conservative rates of return on investments, inflation, potential long-term care costs, and a contingency fund for unexpected expenses. By using conservative modelling, our cash flow planning provides a realistic and resilient framework to help ensure your savings last, your lifestyle is supported, and your financial future remains secure

What is the average amount saved for retirement?

Despite growing awareness around the importance of pension saving, the average amounts accumulated by the time people reach their late fifties remain worryingly low for many. Data shows that by the age of 55 to 59, women typically have around £81,000 in their pension, while men of the same age group have approximately £156,000. These figures illustrate a stark contrast in retirement readiness and highlight the ongoing issue of the gender pensions gap.

To put this into perspective, if someone were to begin drawing down £11,000 annually from a pension pot of £81,000 from age 67, their savings would last just seven years. For a man with £156,000, the same level of withdrawals could stretch over 17 years. This is before taking into account any additional costs or lifestyle choices, and even with the State Pension added in, the income may fallshort of supporting a moderate or comfortable standard of living throughout a typical retirement.

There are many factors that contribute to disparities in pension savings, often reflecting broader patterns and inequalities in the workplace. Career breaks or part-time work taken for personal or family reasons can naturally impact earnings and reduce opportunities to build pension wealth over time. Understanding these influences is key to developing financial plans that are inclusive, flexible, and tailored to individual circumstances ensuring everyone has the opportunity to build a secure and fulfilling retiremen

How much do people spend in retirement?

Actual spending in retirement varies widely, but research consistently shows that spending patterns tend to follow a curve. Many retirees spend more in the first decade after leaving work, while they are still healthy and active, before costs gradually decline. However, in later life, care costs or health-related expenses can cause a second rise in spending.

The PLSA’s Retirement Living Standards (mentioned above) offer a helpful breakdown of what each level of spending supports. At the moderate level, for example, a couple might afford a week-long European holiday and a long weekend in the UK every year, own a car, and spend around £100 per week on food. At the comfortable level, that might extend to three weeks of holidays abroad annually, regular dining out, and higher quality clothing and home maintenance.

Understanding your likely spending habits can help you build a retirement plan that reflects your real-life needs, rather than an arbitrary benchmark.

What options are there for saving for retirement?

There are a number of avenues available when it comes to saving for retirement, and often the most effective strategy involves a combination of different approaches. Workplace pensions, particularly those with employer contributions, remain one of the most powerful tools for building a retirement pot. Auto-enrolment has helped millions of people start saving, but those with higher incomes may want to increase contributions well above the minimum level.

Personal pensions such as Self-Invested Personal Pensions (SIPPs) offer greater control and flexibility, particularly for those with more complex financial situations or larger sums to invest.

ISAs can also play a useful role, offering tax-free growth and flexible access, which can be particularly valuable for early retirement or to fund specific goals outside of pension rules.

Other investments such as general investment accounts and investment bonds can also be part of a retirement strategy, though they may not offer the same tax advantages as pensions or ISAs.

For business owners, company profits and assets can also be used to support retirement goals.

Investments in property or other assets may also form part of a retirement plan, though they carry their own risks and responsibilities.

In summary, a balanced and well-considered approach, tailored to your lifestyle, priorities, and future plans, is essential for building a secure and sustainable retirement. By combining different savings, investment and pension vehicles and regularly reviewing your strategy, you can create a financial foundation that supports both your needs and aspirations throughout retirement.

Start planning early but review often

Starting your retirement savings early can make a significant difference, thanks to the power of compound growth over time, even small contributions made consistently can grow substantially. However, retirement planning isn’t a one-off exercise. Your goals, lifestyle, and financial circumstances will naturally evolve, and your plan should evolve with them.

Regular reviews are essential to staying on track. This includes monitoring the performance of your pension and investments, reassessing your intended retirement age, and checking whether your savings are aligned with your future needs. By doing so, you maintain control and can make informed adjustments as needed.

At TPO, our approach will help you navigate changes with confidence. We aim to provide clarity and flexibility, ensuring your retirement strategy remains robust and responsive throughout your life.

Getting the right advice

While there are many tools and calculators available to help you estimate your retirement needs, the decisions involved can be complex. How to draw down your pension tax efficiently, how to invest in later life, and how to prepare for unexpected costs such as care all involve detailed planning. For those with a moderate to comfortable level of wealth, speaking with a regulated financial adviser can help you avoid costly mistakes and tailor a plan to your specific situation.

Arrange your free initial consultation

This article is for information only and does not constitute individual advice. The information provided in this article is based on the current allowances and legislation and is subject to change.

The Financial Conduct Authority (FCA) does not regulate cashflow modelling, trust or tax advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.