Skip to main content

Skip to main content

A million more workers hit by stealth taxes

A million more workers will have to pay income tax this year, according to research done by the new Taxpayers Alliance (TPA), with those aged over 65s getting hit the hardest.

According to the TPA report, in the 2026/27 tax year, a million more workers than the previous year are forecast to be paying income tax, following the continuing trend of more workers paying tax as personal allowance tax thresholds remain frozen, a type of taxation strategy known as ‘stealth tax’.

Arrange a free initial consultation

On average, taxpayers will pay £640 more in income tax in 2026/27 compared to 2024/25, and £1,040 more compared to 2023/24.

Over 65s are getting hit the hardest however, with the number of pensioners liable for income tax up by 630,000 in a single year, totalling 10.2 million pensioners now once again paying a portion of their income back to the Government.

Of these, 9.5 million are of state pension age, meaning seven in every ten pensioners are now taxpayers.

With many allowances remaining frozen, such as inheritance tax, the personal allowance, and income tax, coupled with an increasingly aging population that is living longer each decade, the resulting tax raid is less of a surprise and more of an economic inevitability.

New Prime Minister Andy Burnham initially hinted he would address the frozen threshold issues around the personal allowance. However, he has since pulled back on this issue. With the freeze expected to pull in £55 billion by 2030 for the Treasury’s coffers, and the expected £9 billion it would cost to uprate it in line with inflation, it is unlikely that any changes will be seriously discussed until the upcoming Autumn 2026 Budget.

To give you an idea of the amount of money you are effectively losing through this freezing strategy, the personal allowance currently sits at £12,570, where it has remained since April 2021. If the personal allowance had risen in line with inflation, it would now sit at £17,380.

The forever frozen allowances

It has become the new norm for each Government – regardless of the Party - to announce a further freeze on allowances, kicking the can down the road with each successive freeze. All the while taxpayers are being forced to hand over increasing amounts as fiscal drag pulls them ever further beyond the out-of-date thresholds.

One example of this is Inheritance tax (IHT). Total IHT receipts collected by the Government have been steadily on the rise since the IHT threshold freeze.

This was initially announced by the then Chancellor, Rishi Sunak, in his 2021 Budget. The Budget outlined that the IHT threshold would be frozen for five years until 2026. However, after ex-Chancellor Jeremy Hunt’s 2023 Autumn Statement, it was confirmed that the freeze would be extended a further two years until April 2028, and then after Rachel Reeves’ 2024 Autumn Statement, this was extended once again a further two years until April 2030, and finally after her 2025 Autumn budget, it was again extended, this time until April 2031.

Many have been calling this move an example of stealth tax, as the freeze ultimately means an increasing number of Britons will fall into the tax threshold each year until the freeze ends in April 2031 – if it indeed does end and hasn’t been extended again by that time – and by then the Government will have collected billions of pounds worth of extra IHT from the taxpayer.

If you want to find out more, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our chartered advisers to find out how can help.

Arrange a free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Living Inheritance: how grandparents are reshaping the transfer of wealth

Recent estimates from the Institute for Fiscal Studies suggest the annual value of financial gifts in the UK has now reached £17 billion, with around £9.6 billion going directly towards helping first-time buyers purchase a home. The growing reliance on family wealth highlights the increasing pressure younger generations face in saving for deposits independently, amid general ongoing affordability challenges.

These figures reflect a broader attitudinal shift. A recent survey of 2,126 UK adults aged 45 and over, found that 81% believe parents or grandparents should help younger generations financially during their lifetime rather than just leaving an inheritance on death. A further 83% say younger generations are more reliant on family support than previous ones.

Arrange a free initial consultation

While early inheritance can help children and grandchildren get onto the property ladder, clear debts, or build financial stability, it’s important for those making the gifts to make sure that they don’t fall foul of the gifting rules if they are also hoping to reduce a potential inheritance tax (IHT) liability, and to ensure that they don’t leave themselves financially exposed later in retirement.

Estates of those aged 85+ account for almost 60% of cases of lifetime gifts

According to a Freedom of Information (FOI) request made to His Majesty's Revenue and Customs (HMRC) in May 2026, data shows that in 2022/23 people aged 85 and over account for nearly 60% of all estates that included gifts, as well as the largest share of the total value gifted, suggesting that gifting is largely an end-of-life financial decision.

That said, feedback from our survey suggests this timing does not always reflect preference. We found that 71% of those surveyed say financial support should be given “early, when it can make the biggest impact”. Only 8% believe wealth should mainly be passed on after death, pointing to a growing gap between when people currently give and when they feel it would have a bigger impact.

The figures from the FOI request also show that only a minority of lifetime gifts end up being taxed through inheritance tax. In 2022–23, around 15% of estates that included gifts paid inheritance tax on them, suggesting most gifts fell within tax-free allowances or were otherwise exempt.

86% of those surveyed have already gifted or loaned money to family members

The vast majority of those surveyed have already acted on their views, with 82% having gifted outright, whilst 12% have loaned the money. The purpose of the support tells an interesting story. Property purchase comes at the top of the list, with 51% of those citing this reason. This is followed by general living support (20%) and educational costs (8%).

Among those who have not yet gifted (14%), 40% plan to do so. Of those, outright gifts before death remain the preferred form (59%), with inheritance via a will cited by nearly a third.

Family financial assistance remains a major factor in UK homeownership

Our survey underlines just how important helping loved ones onto the housing ladder has become. 97% of those surveyed say it is difficult or very difficult for young people to buy a home without family support, and 80% believe homeownership is becoming increasingly dependent on family wealth. Meanwhile, 88% say they would consider helping children or grandchildren to purchase a property, with property purchase already accounting for 51% of all support given by survey respondents, making it by far the most common use of family wealth.

External data supports this picture. Savills' 2025 property report found that 52% of first-time buyers in 2024 received family financial assistance, with the average contribution now reaching an eye watering £55,572.

The Bank of Mum & Dad provided £38.5 billion in support over the past four years, a 71% increase compared to the previous four-year period. Rising interest rates and more challenging mortgage conditions have made it increasingly difficult for younger buyers to purchase without help from family members.

The benefits and risks of early inheritance gifting

Our survey* confirms that the willingness to give sooner is high with 64% of those surveyed saying they would feel comfortable giving a large sum to younger family members during their lifetime. Yet retirement security remains a genuine brake on generosity. The biggest barrier to early gifting is the fear of running out of money in later life, cited by 37% of respondents, followed by concern about care home costs (16%). Together, these account for more than half of all concerns raised, reinforcing the importance of professional financial planning for anyone considering gifting in their lifetime.

What this research makes clear is that the 'Bank of Mum and Dad' has also become the Bank of Grandparents too. We're seeing a genuine generational shift in how people think about wealth — away from the traditional inheritance model and towards active, purposeful giving during their lifetime.

Early inheritance gifting can be a great way to provide financial support to loved ones at key life stages, but it must be balanced carefully against long-term income needs, tax considerations and estate planning objectives. With the right structure in place, families can pass on wealth in a way that is both efficient and aligned with their wider financial plans, reducing the risk of unintended tax consequences or future shortfalls in retirement income.

The question isn't always 'should I give?’, it's 'how much can I safely give?' That's exactly where good financial planning makes a real difference. With the right advice, families can transfer wealth in a way that supports the next generation without compromising their own retirement.

TPO Partner, David Dodgson, appeared on BBC Money Box Live on Saturday 25th July covering this subject (he's on from 16 minutes into the programme). He answered listener questions, explained the options and exemptions available to those looking to gift and shared his knowledge on gifting surplus income.

If you are considering gifting as part of your wider estate or retirement strategy, it is worth seeking tailored advice before making any decisions; if you make a mistake, it can be costly. HMRC collected an estimated £336 million in inheritance tax (IHT) over the past five years from failed gifting arrangements, after the assets involved were deemed not to have been fully given away.

*The findings are drawn from a survey of 2,126 The Private Office newsletter subscribers, conducted in May 2026. The sample is weighted heavily towards older, asset-rich homeowners, reflecting the demographic most likely to be engaged in intergenerational wealth transfer. Respondents skewed towards the 65 and over age group (77% of the sample), with 40.1% aged 65 to 74 and 36.9% aged 75 and over. The remaining respondents were aged 55 to 64 (18.2%), 45 to 54 (3.8%) and under 45 (1.0%). In terms of housing status, 91.3% were outright homeowners, 5.5% held a mortgage, 1.4% rented privately, and 1.8% fell into other categories. 75.3% of respondents had children, grandchildren, or both.

Arrange a free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions. The Financial Conduct Authority (FCA) does not regulate tax advice.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

HMRC warns landlords about impending tax deadline

With the 31 July deadline closing in, HM Revenue and Customs (HMRC) is reminding millions of Self Assessment tax payers to complete their tax return before the deadline.

In particular, landlords and sole traders with an annual turnover above £50,000 are now required to use Making Tax Digital (MTD) for Income Tax, submitting quarterly updates to HMRC. The first quarterly submissions deadline for the 2026/27 tax year is 7 August 2026. More than 864,000 sole traders and landlords are expected to comply with the first phase of the MTD system.

Generally however, the deadline is for taxpayers who make ‘Payments on Account’ – advance payments towards their next Self Assessment tax bill, based on the amount of tax they owed the previous year. These are designed to spread the cost of a tax bill across two instalments rather than paid in one lump sum, which each payment worth half the previous year’s tax bill.

For most people, the first instalment was due on 31 January, while the second must be paid by midnight on Thursday, 31 July. Any outstanding balance remaining is then payable by the following 31 January.

HMRC lays out a number of ways to pay. All the usual methods such as bank transfer, direct debit and online banking apply, but you can also use the HMRC app.

Myrtle Lloyd, HMRC’s Chief Customer Officer, commented on the upcoming deadline:

“We know managing a Self Assessment tax bill isn’t always straightforward and we are here to help. From paying instantly via the HMRC app to spreading the cost through a payment plan, there’s support available for every customer.”

“Search ‘Pay your Self Assessment tax bill’ on GOV.UK to choose the payment option that works for you.”

What is ‘Self-Assessment’?

Self-Assessment is the process you go through each year where you complete a tax return and declare your income, capital gains and any other income during that tax year to HMRC, outside of income tax that is normally deducted from your wage or pension.

Millions of workers complete Self-Assessment each year, with 11.48 million received by the 31 January deadline earlier this year.

Although most commonly done by those who are self-employed, anyone who has other income outside what is normally deducted from your wages and pension, need to complete a self-assessment form – which can be paper based or digital.

Irrespective of employment status, if you have received any untaxed income before the deadline of that tax year, you may need to complete a tax return. Even if that income comes from Ebay, Etsy or similar enterprises.

For further information, check out our free guide on tax planning strategies. Alternatively, give us a call on 0333 323 9065 to book a free non-committal initial consultation with a member of our team.

Arrange a free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax or trust advice.

NS&I makes more rate hikes

Bearing in mind that the Bank of England maintained the base rate at 3.75% at its latest Monetary Policy Committee (MPC) meeting on 18th June, it was interesting to see that National Savings & Investments (NS&I) subsequently announced rate increases to its fixed rate savings accounts, Guaranteed Growth Bonds and Guaranteed Income Bonds – also known as British Savings Bonds.

What are the new NS&I Guaranteed Growth Bond rates?

- 1-year bond: up from 4.50% to 4.69% AER

- 2-year bond: up from 4.48% to 4.67% AER

- 3-year bond: up from 4.45% to 4.65% AER

- 5-year bond: up from 4.40% to 4.55% AER

Whilst inflation has remained steady in the 12 months to May 2026 at 2.80%, we still expect inflation to jump up a little in the near future, as the effects of the war in the Middle East bite – and we know that the energy price cap increased by 13% this month!

However, the expectation that the base rate would remain the same this month is reflected by the slowdown in savings rate hikes that we’ve seen recently. So, it’s good news that NS&I is getting in on the action.

As well as reacting to the rest of the market, NS&I also adjusts rates it is offering, to manage the flow of funds into the state-owned Bank, to help it meet its Net Financing Target - the amount it is tasked with raising for the Government each tax year after taking account of both deposits and withdrawals.

The target has been increased from £13.6 billion to £15 billion for the 2026/27 tax year. In addition, the recent revelation that some bereaved families had not received all the money due from deceased relatives’ NS&I accounts, may have prompted higher than usual withdrawals. According to the Bank of England, some £160million was withdrawn in the first month of the tax year.*

Be aware if you choose the monthly income option

The British Savings Bonds offer a choice between having the interest paid monthly as income, or allowing it to roll up and be paid at maturity.

That choice is worth thinking about carefully, particularly if you pay tax on your savings.

If you choose to have the interest added to the bond each year so that it compounds, you won't receive it until the bond matures, which could be more important in longer term bonds. For tax purposes, that means all the interest is treated as being received in the tax year in which the bond ends.

Because your Personal Savings Allowance (PSA) can't be carried forward, receiving several years' worth of interest in one tax year could mean you exceed your allowance and pay tax on some of the interest. In some cases, it could even push you into a higher tax band for that year.

It won't affect everyone, but it's certainly something worth considering before deciding how you'd like your interest paid.

Are the new rates competitive?

The latest increases undoubtedly make NS&I more competitive, especially when compared with many of the high street banks.

However, savers prepared to look beyond the familiar names can still find significantly better returns elsewhere.

For example, a £50,000 deposit for 12 months would earn £2,345 (before the deduction of tax) with NS&I’s 1-year bond, compared with £2,450 with Marcus: from Goldman Sachs, which currently pays 4.90% AER.

It's the same with the longer fixed terms. The top 2-year bond is paying 4.86% versus the NS&I bond paying 4.67% Over 3-years, the top rate is 4.85% compared to 4.65% with NS&I and over 5-years you can earn up to 4.90% compared to NS&I’s option which is now 4.55% AER

So, whilst NS&I’s new rates have improved, they don’t make it into the best-buy tables.

Despite rarely topping the tables, NS&I continues to benefit from huge customer loyalty. A key reason is its unique Government guarantee. Every penny held with the provider is backed by HM Treasury, giving savers complete protection, regardless of how much they hold.

You can invest £500 up to £1 million into each issue of the British Savings Bonds, making them particularly appealing for those with larger sums who prioritise safety over the best returns.

For most savers, though, whose balances fall below the £120,000 Financial Services Compensation Scheme (FSCS) protection limit that applies to all other regulated and authorised banks and building societies, there are still better-value options elsewhere.

*Bank of England Table A7.1 (changes tab)

For the latest rates, visit our Best Buy tables.

Arrange a free initial consultation

Rates correct 02/07/2026

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions. The Financial Conduct Authority (FCA) does not regulate tax advice.

The cost of Inheritance Tax gift mistakes soars to £336m

HMRC collected an estimated £336 million in inheritance tax (IHT) over the past five years from failed gifting arrangements, after the assets involved were deemed not to have been fully given away.

Between 2021 and 2026 nearly 2,500 gifts with a combined value of £840 million were classed by HMRC as gifts with “reservation of benefit”. This applies where the person making the gift continues to enjoy some benefit or use of the asset after it has been passed on.

As a result, these gifts, which had an average value of £338,840, did not qualify for inheritance tax exemption and left families facing an estimated £336 million tax charge.

What is a gift with reservation of benefit?

A gift with reservation of benefit essentially means when someone gives away an asset but continues to enjoy, or is able to enjoy, some benefit from it. The classic example is a person who gives their house to their children but continues to live in it rent-free.

As a result, the gift is not regarded as an effective lifetime transfer for inheritance tax purposes. Instead, the asset – the house in the above example - is treated as remaining within the donor’s estate when they die, meaning its full value is included in the inheritance tax calculation. The asset may also be subject to tax again on the death of the recipient.

What counts as the gifter still ‘benefitting’ has a fairly wide definition and applies to many other assets too. Examples include handing over valuable possessions while still making regular use of them and transferring shares in a family company while keeping the right to receive dividends or exercise voting power. In these situations, the legal ownership may have changed, but the donor is still considered to retain an interest in the asset. It is important to understand whether you will be classed as still ‘benefitting’ from the asset you have gifted before you go ahead and ‘gift’.

You can find out more about gifts without reservation of benefit here.

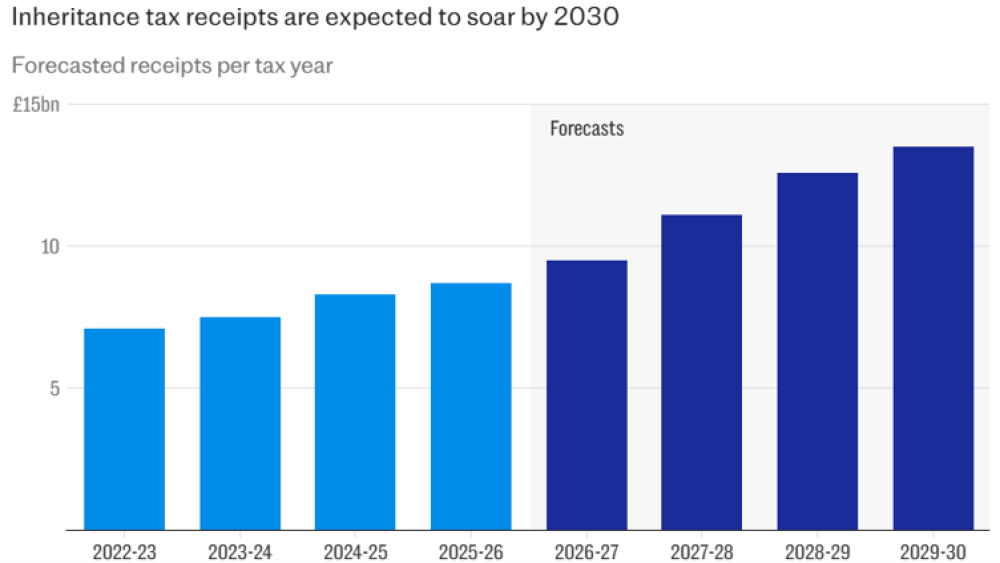

Why are IHT receipts always on the rise?

Total IHT receipts collected by the Government has been steadily on the rise since the IHT threshold freeze and are showing no signs of slowing.

Source: Inheritance tax receipts are expected to soar, OBR, 2023

This was initially announced by the then Chancellor, Rishi Sunak, in his 2021 Budget. The Budget outlined that the IHT threshold would be frozen for five years until 2026.

However, after ex-Chancellor Jeremy Hunt’s 2023 Autumn Statement, it was confirmed that the freeze would be extended a further two years until April 2028, and then after Rachel Reeves’ 2024 Autumn Statement, this was extended once again a further two years until April 2030, and finally after her 2025 Autumn budget, it was again extended, this time until April 2031.

Many have been calling this move an example of a ‘stealth tax’, as the freeze ultimately means an increasing number of Britons will fall into the tax threshold each year until the freeze ends in April 2031 – if it indeed does end and hasn’t been extended again by that time – and by then the Government will have collected billions of pounds worth of extra IHT from the UK taxpayer.

The inheritance tax allowance of £325,000 increased from £312,000 on 6 April 2009. This means the IHT nil rate band has now been frozen for over 15 years and will continue to be frozen until at least 5 April 2031. Though some additional relief was introduced in April2017 through the residence nil rate band, which can increase the tax -free allowance where a main home is passed to direct descendants, the main nil rate band itself will have been frozen for a staggering 22 years of higher taxes on death - over two decades.

If you’re interested in how to manage your inheritance tax to ensure the best possible wealth protection for you or your family, we can help. Give us a call on 0333 323 9065 or book a free non-committal initial consultation with a member of our team to find out more.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice.

The Stealth Tax Squeeze

A new report has highlighted the growing impact of frozen tax allowances in the UK, with some thresholds remaining unchanged for more than four decades.

Research from Association of Taxation Technicians (ATT) found that numerous allowances have remained static for decades, resulting in taxpayers paying more in real terms without any formal increase in tax rates – a policy by the Government known more informally as ‘stealth tax’.

ATT argues that many tax reliefs are overdue a comprehensive review, as years of inflation have steadily reduced their real-world value through fiscal drag.

So, who’s being affected by ‘stealth taxes’?

Almost everyone will in some way or another be losing money to stealth taxes.

Inheritance tax provides some of the clearest examples. The nil-rate band, which determines how much of an estate can be passed on free from inheritance tax, currently remains at £325,000 per individual. This threshold was last increased 17 years ago and is now scheduled to stay frozen until 2031. According to the ATT report, if it had been adjusted in line with inflation, it would stand at approximately £525,000 today, around 60 per cent higher than its current level.

The same pattern can be seen across other inheritance tax exemptions. The annual gifting allowance has been fixed at £3,000 since 1981. Using the Bank of England’s inflation calculator, the ATT estimates that an inflation-linked equivalent would now be around £11,800, almost four times the existing allowance.

Meanwhile, the wedding gift exemption has remained unchanged at £5,000 since 1975, having originally been introduced under the capital transfer tax regime before inheritance tax existed in its current form. Had it increased in line with inflation over that period, it would now be worth £39,876, representing a rise of 697 per cent. With UK weddings in 2026 costing on average an eye watering £20,604, that missed 697 per cent will come with an especially nasty sting for newly weds.

The report also found that savers have been affected by the same phenomenon. Basic-rate taxpayers can currently receive up to £1,000 of savings interest tax-free under the personal savings allowance, while higher-rate taxpayers are entitled to £500. Had these limits risen alongside inflation since their introduction in 2016, they would now be worth roughly £1,400 and £700 respectively.

Homeowners benefiting from the Rent a Room scheme have also seen the value of their tax break eroded. The scheme's £7,500 tax-free income limit has not increased since 2016. If it had kept pace with inflation, it would now be closer to £10,500.

Not even those saving into their pensions have been able to escape the stealth tax net. Individuals without relevant earnings can contribute £2,880 each year to a pension, which becomes £3,600 after tax relief is added. This allowance has remained unchanged since 2000. If uprated for inflation, it would be approximately £5,500 net, or £6,850 including tax relief.

The forever frozen allowances

It has become the new norm for each Government to announce a further freeze on allowances, kicking the can down the road with each successive freeze, all the while taxpayers are being forced to hand over increasing amounts as fiscal drag pulls them ever further beyond the outdated thresholds.

One example of this is inheritance tax (IHT). Total IHT receipts collected by the Government has been steadily on the rise since the IHT threshold freeze.

This was initially announced by the then Chancellor, Rishi Sunak, in his 2021 Budget. The Budget outlined that the IHT threshold would be frozen for five years until 2026. However, after ex-Chancellor Jeremy Hunt’s 2023 Autumn Statement, it was confirmed that the freeze would be extended a further two years until April 2028, and then after Rachel Reeves’ 2024 Autumn Statement, this was extended once again a further two years until April 2030, and finally after her 2025 Autumn budget, it was again extended, this time until April 2031.

Many have been calling this a clear example of stealth taxes, as the freeze ultimately means an increasing number of Britons will fall into the tax threshold each year until the freeze ends in April 2031 – if it indeed does end and hasn’t been extended again by that time – and by then the Government will have collected billions of pounds worth of extra IHT from the taxpayer.

If you want to find out more, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our chartered financial advisers to find out how can help.

Arrange a free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning, tax or estate planning.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

How will the 'Mansion Tax' impact estate planning?

Inheritance tax is increasingly something more families will need to think about at some stage, particularly where a large share of wealth is tied up in property. The proposed mansion tax could affect estate planning by adding an extra annual charge to high value residential property, which will mean some families will need to rethink their plans for passing on wealth.

For those with a large proportion of their estate tied up in property, it could make decisions around gifting, succession, liquidity and long term affordability more important, particularly as the rules depend on how homes are valued when the charge begins.

Arrange your free initial consultation

Added to that the Government is consulting on how the proposals will work in practice. One suggestion is to defer payment until after death for those on lower incomes. Although not set in stone, this could mean an even bigger inheritance tax bill than expected making forward planning crucial.

What is the mansion tax?

The term ‘mansion tax’ is being used as shorthand for the government’s new High Value Council Tax Surcharge. It applies to owners of residential property in England worth £2 million or more at 2026 prices, and it is separate from the existing Council Tax system. The official charging structure starts at £2,500 a year for homes valued between £2 million and £2.5 million, rising to £7,500 a year for properties worth £5 million or more. The government says fewer than 1% of properties in England are expected to fall within scope.

From an estate planning point of view, that matters because it adds a recurring cost to retaining a valuable family home. For some households that will be manageable. For others, particularly those who are asset rich but cash poor, it could push property higher up the list of assets that need reviewing as part of a long term plan.

How will property values be calculated?

The surcharge will not be based on the current Council Tax bands, which still rely on property values from 1991. Instead, the Valuation Office Agency will carry out a separate targeted valuation exercise in 2026 to identify which properties are worth £2 million or more and to place them into one of four surcharge bands. The government has also said revaluations will be carried out every five years.

That distinction is important. A property sitting in a higher Council Tax band today does not automatically fall into the mansion tax regime, and a change to a home’s Council Tax band will not decide whether the surcharge applies. For estate planning, this means families should avoid relying on rough assumptions or old valuations. If a property is anywhere near the threshold, an up to date professional valuation becomes far more useful, especially if future gifting, downsizing, trust planning or a potential sale is already being considered.

When will the mansion tax apply?

The government plans to introduce the surcharge from April 2028. Eligibility will be based on the separate valuation exercise carried out in 2026, with charges then collected from 2028 onwards. The amounts will rise each year in line with CPI inflation from 2029 to 2030 onwards.

That timing gives affected families a planning window, but not an especially long one. Anyone with property close to or above the threshold has time to review ownership and funding arrangements before the charge starts. In estate planning terms, that may include asking whether the current owner should continue holding the property personally, whether a move is already likely in later life, and whether enough liquid capital exists to cover future annual charges alongside maintenance, care costs and any eventual inheritance tax bill.

Where will the money raised from the mansion tax go?

Although the surcharge will be collected alongside Council Tax by local authorities, the revenue is intended for central government rather than being retained locally in the way Council Tax normally is. The official fact sheet says the measure is expected to raise around £430 million a year from 2028 to 2029 to support funding for local government services, while the Budget and OBR documents put the annual yield at roughly £0.4 billion by the end of the decade.

For estate planning, the destination of the money is less important than the policy direction behind it. The broader message is that higher value property is being asked to bear more of the tax burden. That may encourage more clients to think of the family home not just as a place to live, but as a taxable asset whose ongoing cost could continue to change over time.

Will people sell property to avoid the mansion tax?

Some will certainly consider it, but many will not rush into a sale on tax grounds alone. The annual charge is meaningful, yet for many owners of homes worth well over £2 million it may still be smaller than the emotional and practical costs of moving. In other cases, particularly for older owners with limited income, the surcharge could become one more reason to downsize earlier, release capital, or rethink whether a large property is the best vehicle for passing wealth down a generation.

That is where estate planning becomes practical rather than theoretical. A home that has risen sharply in value can leave a family with substantial paper wealth but limited cash flow. An extra annual charge, on top of existing running costs, may strengthen the case for simplifying the estate while the owner is still able to make deliberate choices. The government has also said it intends to put a support scheme in place for those who may struggle to pay, although the detailed design of that support is still a matter for consultation.

Is mansion tax paid in addition to council tax?

Yes. The surcharge is explicitly in addition to existing Council Tax, not a replacement for it. Current Council Tax bands will still apply and will not be used to determine surcharge eligibility.

This is one of the reasons the measure matters for estate planning. It is an extra annual expense layered on top of the property costs families already face. The government has argued that this corrects an imbalance in the present system, noting that in 2024 to 2025 Council Tax raised £40.3 billion across England and that the average Band D charge for a typical family home was £2,280, which was £250 more than a £10 million property in Mayfair paid under Westminster’s Band H charge.

Why is the mansion tax being introduced?

The official case is fairness. In Budget 2025, the government said the current system leaves some very expensive homes paying less in annual local property tax than ordinary family homes, because Council Tax is still rooted in 1991 values. The surcharge is therefore being presented as a way to make owners of the highest value residential property contribute more. The Budget also frames it within a wider shift towards taxing wealth and asset based income more heavily.

That wider context is the real estate planning takeaway. The mansion tax does not, by itself, rewrite succession planning. What it does do is reinforce the need to look at property wealth holistically. Where a large share of an estate sits in a high value home, families may need to pay closer attention to liquidity, future liabilities and whether the property still serves the family’s goals. In that sense, the impact on estate planning is not simply the annual bill. It is the way that bill may prompt earlier and more realistic conversations about how wealth is held, who will inherit it and how sustainable that plan really is.

How we can help

Good estate planning starts with making sure your arrangements still reflect your wishes and your circumstances. That could mean reviewing your will, considering whether trusts may be appropriate, looking at how property and other assets are owned, and checking whether your wider financial plan is set up to pass on as much wealth as possible in a tax efficient way. A free initial conversation with one of our advisers can be a helpful first step towards getting on top of the changes.

There is some speculation that the introduction of a mansion tax could affect the appeal of properties around or above the £2 million threshold. If buyers know a home will come with an extra annual tax charge, that could make some properties less attractive and place downward pressure on values at the margins. That may not happen in every case, and much will depend on how the rules are finally applied, but it is another factor that homeowners may need to keep in mind when thinking about long term estate planning.

With that in mind, financial advice can be especially valuable. Where a large part of your wealth is tied up in property, even a relatively modest policy change can have wider implications for gifting, retirement income, inheritance tax planning and the overall shape of your estate. Taking advice can help you understand how the proposed mansion tax may affect your plans and what options may be available to you for the best financial outcome.

Arrange your free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning, tax, estate planning, trusts or wills.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

How to calculate Capital Gains tax?

Capital Gains Tax is the tax you may pay when you sell something for more than you paid for it. That could be shares, investments or a second property. It is based on the profit you make, not the full amount you sell it for.

In the 2026 to 2027 tax year, most people can make £3,000 in gains before Capital Gains Tax is due. If your gain is above that, the main rates are 18 per cent and 24 per cent, depending on your income.

Arrange a free initial consultation

That matters even more now because the annual exempt amount has fallen sharply in a short space of time, moving from £12,300 in 2022/23, to just £3,000 from 2024/25 onwards. As that tax free allowance has narrowed, more people have been brought within the scope of Capital Gains Tax, which makes it increasingly important to stay aware of changing tax rules.

How is Capital Gains Tax calculated?

Capital Gains Tax is charged on the gain rather than the full sale price. So, if you bought an asset for £200,000 and later sold it for £260,000, your starting gain is £60,000. From there, you can usually deduct certain costs, such as legal fees, estate agency fees and some improvement costs, which reduces the gain before tax is worked out.

The calculation of the base cost for investments is often not simply the amount you originally invested, as growth can result in the purchase of additional units of investment at a different price. Care needs to be taken, and base cost should be used in the calculation of gain rather than the original investment amount.

Imagine you sell a buy to let property and, after allowable costs, your gain is £40,000. You then deduct the £3,000 annual exempt amount, leaving a taxable gain of £37,000. The tax you pay depends on your income and the asset sold. Residential property now has the same CGT rates as other assets, but for most individuals the current Capital Gains Tax rates are 18 per cent for gains that fall within the basic rate band and 24 per cent for gains above it.

The gain calculation on a second property can be complicated by periods of non-residency, or periods where the property was your Principal Private Residence. These can result in a proportion of the gain being ignored for Capital Gains Tax.

If the asset is a UK residential property and tax is due, there is also a strict deadline. In most cases, you must report and pay the tax within 60 days of completion rather than waiting and reporting it in line with normal self-assessment deadlines. This is one reason people need to calculate the likely bill early.

Who pays Capital Gains Tax?

Capital Gains Tax is usually paid by individuals when they sell or give away something that has risen in value and the gain is above their allowance. That can include shares, investments, second homes and buy to let property, and chattels. Not every sale or transfer of ownership leads to tax, but many investors and landlords are within scope.

Business owners can be affected too, although the rules depend on the structure of the business. A sole trader or partner may pay Capital Gains Tax personally when selling a business asset. A limited company is different, because it does not usually pay Capital Gains Tax itself. Instead, it normally pays corporation tax on any chargeable gains. That is an important distinction for landlords deciding whether to hold property personally or through a company.

There can also be reliefs for business owners. Business Asset Disposal Relief can reduce the rate on qualifying gains, although the rate is now higher than many people still assume. For disposals in the 2025 to 2026 tax year, the rate was 14 per cent, which rose to 18 per cent from 6 April 2026.

How to reduce your Capital Gains Tax bill

The first step is to make sure you are claiming everything you are allowed to claim. Many people focus on the sale price and forget that buying and selling costs can usually be deducted, along with certain improvement costs. That alone can reduce the taxable gain by more than expected.

Losses can also help because if you have made losses on other assets, you may be able to use them to reduce your gains, provided they have been reported properly. With the annual exempt amount now only £3,000, using losses well can make a real difference.

Married couples and civil partners may also have more planning options, because assets can often be transferred between them without an immediate tax charge. In the right circumstances, that can help a couple make better use of allowances and lower tax bands.

Capital Gains Tax can also result from making a gift of an asset even if not sold, as this is a transfer of value. In addition, under current legislation, Capital Gains are not payable on death, and the assets are rebased in the hands of your beneficiaries. This is an important consideration in estate planning, as the aim of saving 40% Inheritance tax can be diluted by the Capital Gains Tax due which would otherwise not be payable on death. Capital gains tax in life vs on death should therefore be carefully considered when choosing which assets are most suitable to gift.

Capital Gains Tax rate: Short vs long

In the UK, Capital Gains Tax does not work like some overseas systems where short term and long term gains are taxed at different rates depending on how long you held the asset. Here, the rate is not usually based on the length of ownership. Instead, it depends mainly on your income. Most assets are now taxed at same rates and whether any relief applies.

That means the key question is how much taxable gain is left after costs, losses and allowances, and which tax band that gain falls into, rather than how long you owned the asset. Instead, the tax rate mainly depends on your income tax band, although certain assets and reliefs can be subject to different rules or rates.

Further Capital Gains Tax support

The basic formula for Capital Gains Tax is clear enough. Work out the gain, deduct allowable costs, take off losses and your annual allowance, then apply the right rate. The challenge is making sure the right figures go into the calculation and that nothing is missed.

That is why tailored advice can be valuable, especially for landlords, investors and business owners. When allowances are lower and deadlines are tighter, getting the calculation right first time matters more. If you want clarity on a future sale, or support with a recent one, financial advice can help you understand the likely tax bill and the options available before you make a decision.

Arrange a free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning, tax or estate planning.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Millions of workers and pensioners hit by extra tax

The number of workers paying additional rate tax has jumped to nearly 900,000, up 57 per cent in just 12 months.

Taxpayers paying the 45 per cent additional rate of income tax leapt from 570,000 in 2022/23 to 893,000 in 2023/24 tax year – the latest year for which data is available.

HM Revenue & Customs (HMRC) figures also show that the number of people paying the 40 per cent higher rate grew by close to 13 per cent over the same period, reaching 5.76 million.

Years of wage growth combined with frozen tax thresholds have been steadily dragging more workers into higher tax bands.

The threshold freeze was originally introduced in 2021 under then-chancellor Rishi Sunak and meant that the basic and higher-rate income tax starting thresholds became frozen at £12,570 and £50,270 respectively. Labour has since extended the policy through to 2031, meaning that as wages rise with inflation, ever more people will be dragged into higher tax brackets in a phenomenon known as ‘fiscal drag’.

Forecasts from the Office for Budget Responsibility (OBR) suggest that by 2030, one in four taxpayers will be paying either the higher or additional rates of income tax. This means a greater tax take than ever before for the Government, and more tax paid than ever before by workers.

Another major factor behind the jump in top-rate taxpayers was the reduction of the 45 per cent threshold from £150,000 to £125,140, which took effect on April 6 2023.

Although additional-rate taxpayers represented just 2 per cent of all taxpayers, they contributed almost 38 per cent of total income tax receipts in 2023/24, compared with 32 per cent in 2019/20.

Combined, those paying the higher and additional rates were responsible for more than 70 per cent of the country’s overall income tax revenues.

Pensioners aren’t getting off easy either

The number of pensioners paying income tax rose more than a million in a year, with at least 22 per cent of taxpayers now being over state pension age.

HMRC figures for the 2023/24 tax year showed that there were 8.16 million taxpayers aged over 66, up from 7.14 million in the year before. The jump came as rises in the state pension and a freeze on income tax thresholds pushed more older people into paying 20 per cent basic rate tax on their retirement income.

In 2023/24, an additional 2.17 million people fell into the basic rate income tax band compared with the previous year, while the number paying the 40 per cent higher rate climbed by 654,000 or 12.8 per cent, bringing the total to 5.76 million.

The full new state pension currently stands at £12,548 annually, just £22 short of the basic-rate income tax threshold. As a result, pensioners receiving even a modest extra income are now liable for tax. From next year, recipients of the full state pension could also begin paying income tax on that income alone, because the triple lock ensures payments increase each year by whichever is greatest: wage growth, inflation or 2.5 per cent, and due to the freeze set to remain in place until 2031, even a single year of growth at the lowest possible rate of 2.5% would put the full state pension over the £12,570 personal allowance (also known as the tax-free personal allowance).

Although chancellor Rachel Reeves said in November that pensioners relying solely on the state pension would not be taxed on it, the details of how that pledge would be implemented remain uncertain, and it has done little to alleviate worries from some of the most vulnerable and state-dependant members of society.

Our chartered financial advisers are expert and unbiased, meaning that they can give whole of market advice, and so are best placed to give you a plan tailored exactly to your personal financial goals.

If you’d like to know more, request a free non-committal initial consultation with one of our team or give us a call on 0333 323 9065 and get in touch.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.

What is the threshold for higher rate tax?

Understanding when higher rate tax applies is an important part of making informed financial decisions. While tax can often feel complicated, the basic structure is more straightforward than many people expect. Knowing how much you can earn before moving into a higher band, what counts as taxable income and what allowances may be available, can help you plan more effectively and avoid surprises.

In the UK, Income Tax is charged at different rates depending on how much taxable income you receive. For many people, the key question is when earnings move beyond the basic rate and into the higher rate band. That threshold matters because it affects how much of your income you keep, how you approach pension contributions and how you think about wider financial planning.

Arrange your free initial consultation

Should I pay any Income Tax?

You only pay Income Tax on taxable income above the allowances available to you. For most people, that starts once income rises above the standard Personal Allowance of £12,570. If your earnings stay below that level, you will often have no Income Tax to pay, although there are exceptions depending on the type of income you receive and whether you qualify for any extra allowances.

It is also worth remembering that Income Tax is not charged on every type of money in the same way. Earnings from work, pension income, rental income and some savings income can all be taxed differently, and some people will have tax deducted through PAYE while others need to report income through Self-Assessment.

In practice, the question is not simply whether you earn money, but how much taxable income you have after any allowances and reliefs are taken into account.

When do you pay higher rate tax?

If you live in England, Wales or Northern Ireland, you start paying higher rate tax when your taxable income goes above £50,270. Income between £12,571 and £50,270 is taxed at the basic rate of 20 per cent, and income from £50,271 to £125,140 is taxed at 40 per cent. Above £125,140, the additional rate is 45 per cent. These are the current bands published by GOV.UK for the 2026 to 2027 tax year.

Scotland uses different Income Tax bands on earned income. There, the higher rate is 42 per cent and begins at £43,663 if you have the standard Personal Allowance, with an advanced rate of 45 per cent above £75,000 and a top rate of 48 per cent above £125,140. That means a Scottish taxpayer can move into higher rate tax sooner than someone elsewhere in the UK.

One detail that often catches people out is that crossing the higher rate threshold does not mean all of your income is taxed at 40 per cent. Only the part above the threshold is taxed at that rate. This is why a pay rise that takes you over the line is still usually beneficial, even if more of your income is taxed.

What is a Personal Allowance?

The Personal Allowance is the amount of income you can usually receive before paying Income Tax. For the 2026 to 2027 tax year, the standard figure is £12,570. For most employees and pensioners, this is the foundation of their tax calculation. It reduces the amount of income that is exposed to tax bands and helps determine when basic or higher rate tax starts to apply.

There is another important point here for higher earners. Once your adjusted net income goes above £100,000, your Personal Allowance is reduced by £1 for every £2 above that level. It falls to zero once income reaches £125,140. This creates a particularly harsh pinch point because you are not only paying higher rate tax, you are also losing part of your tax free allowance as income rises. This is where what’s known as the 60% tax trap kicks in, as it creates an effective 60% tax rate when taking income tax and reduced tax free allowances into consideration. Add in National Insurance and you’re paying a 62% effective rate.

What is Income Tax used for?

Income Tax is one of the main ways the government raises money to fund public services. HMRC states plainly that it collects the money that pays for the UK’s public services. GOV.UK also provides taxpayers with an annual summary showing how Income Tax and National Insurance contributions feed into government spending.

In broad terms, that revenue helps support areas such as health, education, welfare, transport, defence and day to day public administration. The Office for National Statistics also notes that taxes make up the majority of government income. So while Income Tax can feel like a deduction that disappears from your payslip, it remains one of the central pillars of how the state funds essential services.

How much Income Tax will I pay?

That depends on where you live in the UK and how much taxable income you have. In England, Wales and Northern Ireland, someone with taxable income of £60,000 and the standard Personal Allowance would pay no tax on the first £12,570, 20 per cent on the next £37,700 and 40 per cent on the remaining £9,730. That works out as £7,540 at basic rate and £3,892 at higher rate, for a total Income Tax bill of £11,432. The key point is that the higher rate only applies to the slice above £50,270. This calculation follows the current GOV.UK bands.

If you are in Scotland, the same salary can produce a different result because the bands are different. The tax system is not uniform across the UK, so using the right set of rates matters. This is especially relevant for people who are comparing job offers, approaching retirement, drawing income from multiple sources or trying to decide how much of a bonus to take as salary.

A further complication is that your tax bill can change if your Personal Allowance is reduced, if you receive taxable benefits, or if part of your income comes from dividends or savings. Income Tax is simple at the headline level, but once income sources multiply, the true figure can move quickly.

It is also worth understanding the order in which different types of income are taxed, as this can catch people out. Non savings income is taxed first. This includes earnings from employment, self employed profits, pension income and rental income. Savings income is taxed next, which includes things like interest from bank and building society accounts. Dividend income is taxed last. This matters because your non savings income uses up your Personal Allowance and tax bands before savings interest and dividends are taken into account, which can mean those later sources of income are taxed at a higher rate than expected.

For example, if someone in England has a salary of £45,000, savings interest of £3,000 and dividend income of £2,000, their salary is taxed first and uses up all of their Personal Allowance as well as most of the basic rate band. The savings interest then sits on top of that salary, and the dividend income sits on top of both. Even though none of the income sources looks especially large on its own, the order they are taxed in can push part of the interest or dividends into a higher band. That is why it is so important to look at your total income as a whole rather than viewing each source in isolation.

How to minimise the tax you pay

The starting point is to make full use of the allowances and reliefs that are already built into the system. Pension contributions can be particularly valuable because by paying your relief at source (so paying into a pension without the deduction of basic rate tax) this may increase your basic rate tax band which in turn can reduce the amount of income that will be taxed at the higher rate tax band. This can help you reduce the amount of tax you pay at the higher rate or preserve your Personal Allowance if income is above £100,000.

ISAs can also play an important role because returns within an ISA are sheltered from Income Tax and Capital Gains Tax. Salary sacrifice, where available, may improve tax efficiency too, depending on your circumstances. For couples, holding assets and drawing income in the most tax efficient name can also make a meaningful difference over time. None of this is about avoiding tax. It is about using the rules properly and planning ahead rather than reacting once the tax year has ended.

This is where financial planning becomes useful. The higher rate threshold is a point where decisions about pensions, remuneration, investment wrappers and income timing can start to have a much bigger impact. Knowing where the threshold sits is helpful. Structuring your finances around it is where the real value often lies.

If you want to find out more about minimising the amount of tax you might have to pay, you can request a free non-committal initial consultation with one of our team or give us a call on 0333 323 9065 and get in touch.

Arrange your free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age).

The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.