Skip to main content

Skip to main content

Middle East oil crisis creates a slippery slope for markets

Performance in Q1 2026 followed two sharply contrasting trajectories – in sporting terms, it really was a game of two halves (or thirds, to be technically correct)!

The quarter began with equities extending their year-end rally through February, but this optimism was upended in March. The launch of attacks on Iran by U.S. and Israeli forces led to the effective shutdown of the Strait of Hormuz, a vital artery for global oil. This development triggered a spike in market volatility as investors re-priced assets against a backdrop of rising energy costs and heightened geopolitical risk.

Arrange your free initial consultation

Equities

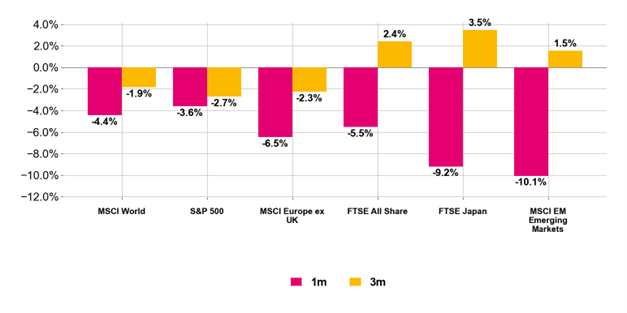

Global equities experienced their worst monthly return since 2022, falling 6.8%, with markets most acutely exposed to energy prices, such as Japan and the broader Asian region, seeing the steepest declines.

European equities sharply sold off, as whilst less dependent on the Strait of Hormuz than Asian economies, they do remain vulnerable to price shocks and supply disruptions with close to 60% of European energy needing to be imported.

Performance across the UK equity landscape was split. Large-cap companies benefited from their international reach and the presence of major oil and gas producers, allowing them to outperform the broader market. In contrast, domestically focused small-cap equities underperformed, as their heightened sensitivity to the UK’s fragile economic outlook weighed on investor sentiment.

Figure 1. Equity market returns (April 2026, Source: Pacific Asset Management)

Fixed Income

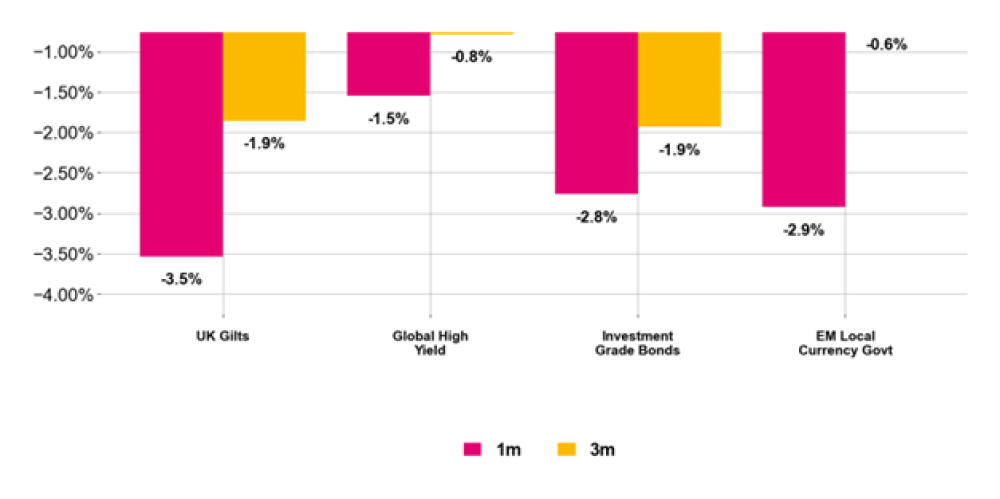

Continuing a post-pandemic trend, government bonds failed to provide the traditional 'safe-haven' shelter investors had become accustomed to during the equity market downturn. This disappointment stemmed from a sharp reappraisal of interest rate trajectories. While developed market yields had been trending lower early in the year, the prospect of conflict-driven inflation in the Middle East abruptly shifted expectations, triggering a broad sell-off across US, UK, and European government bonds in March.

Prior to the geo political escalation, UK Gilts had led sovereign market performance as cooling price pressures fuelled hopes for imminent Bank of England rate cuts. However, the resulting energy shock left the UK - with its high dependence on natural gas - uniquely vulnerable to upside inflation risks. Consequently, the 10-year Gilt yield surged above 5%, marking its worst monthly performance since the 'mini-budget' volatility of 2022.

Figure 2. Fixed Income returns (April 2026, Source: Pacific Asset Management)

Commodities

Commodity markets experienced a historic monthly divergence in March, with the energy sector at the epicentre of the shock. Driven by the escalating Middle East conflict and the closure of the Strait of Hormuz, energy prices rallied sharply; Brent crude surpassed the $100-per-barrel threshold, marking its steepest monthly gain in four decades.

In stark contrast, the metals sector faced intense downward pressure. Following a sustained year-long rally, gold plummeted by more than 10%, marking its worst monthly performance since the 2008 financial crisis. This reversal occurred as investors pivoted toward a more hawkish central bank outlook, stripping gold of its safe-haven momentum. The correction likely reflected a wave of profit-taking and deleveraging, with gold and silver serving as primary sources of liquidity during a period of forced portfolio repositioning.

Although the current geopolitical shock has triggered significant volatility, historical precedents indicate that such episodes are typically short-lived in their market impact. We are closely evaluating the evolving consequences for global growth, inflation, and corporate earnings; however, we also recognise that periods of indiscriminate selling can create attractive entry points for disciplined investors.

At this juncture, we continue to advocate for a strategy of prudent risk management while remaining positioned to capitalise on market dislocations as they arise.

If you have any questions about your own portfolio or more general concerns in this period of heightened uncertainty, do contact your Adviser or more generally The Private Office team.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.