Skip to main content

Skip to main content

Markets stay hot in June

Markets continued to be volatile in June but both equity and bond markets ended the month modestly higher. After initial weakness at the start of the month, a ceasefire between the United States and Iran, formalised in a Memorandum of Understanding signed at the Palace of Versailles on 17 June following the G7 summit, was the catalyst to a sharp relief rally across risk assets. Under the surface, there was significant rotation within equity markets.

Arrange your free initial consultation

Equities

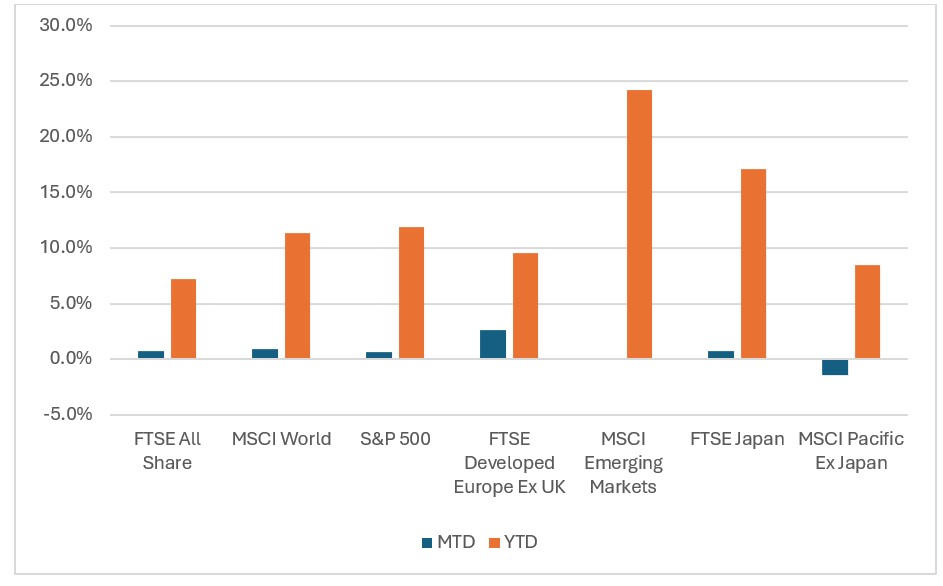

US Equities delivered positive returns over the month, supported by US dollar strength, yet with considerable intramonth volatility due to the rotation into and out of AI-related names. Semiconductor stocks continued to surge higher, whilst the “Mag7” stocks fell back. SpaceX completed the largest IPO in stock market history, raising $75 billion and surging 19% on its first day to achieve a market capitalisation exceeding $2 trillion.

In the UK, the FTSE All Share Index rose over the month, mainly driven by FTSE 100 performance, supported by financials, industrials, and a handful of international diversified blue-chips. The more domestically focused FTSE 250 lagged large cap stocks in June.

Emerging Markets (EM) were exposed to similar swing factors surrounding AI supply chain stocks which led to a volatile month, ending with flat performance. Nevertheless, EM continues to benefit from a strong earnings upgrade cycle, with consensus EPS (Earnings Per Share) growth expectations lifted when compared to the start of the year.  Figure 1: Equity market returns (Source: Bloomberg 2026)

Figure 1: Equity market returns (Source: Bloomberg 2026)

Fixed Income

Sovereign bond markets moved higher even as several central banks, including the Bank of Japan and the ECB, raised interest rates to push back against lingering inflation pressures.

UK Gilts were volatile in June with the political uncertainty surrounding the Labour leadership driving the 10-year gilt yield close to 5%, before retracing as Burnham committed to existing fiscal rules and falling oil prices reduced near-term inflation expectations. The Monetary Policy Committee voted 7-2 to hold interest rates at 3.75%, with two members favouring a rise to 4.0%. The Bank cautioned that inflation is likely to climb again, projecting a return towards 3.25% in Q4 as earlier energy price increases pass through household bills.

The US Federal Reserve held its policy rate steady in June, but the meeting carried added significance under new chair Kevin Warsh, who struck an early hawkish tone, signalling a willingness to raise rates further should inflation risks resurface. Somewhat counterintuitively, this firm stance appeared to reassure markets on the Fed's inflation credibility, helping underpin a broader Treasury rally over the month.

Figure 2: Fixed income returns (Source: Bloomberg 2026)

Figure 2: Fixed income returns (Source: Bloomberg 2026)

Commodities

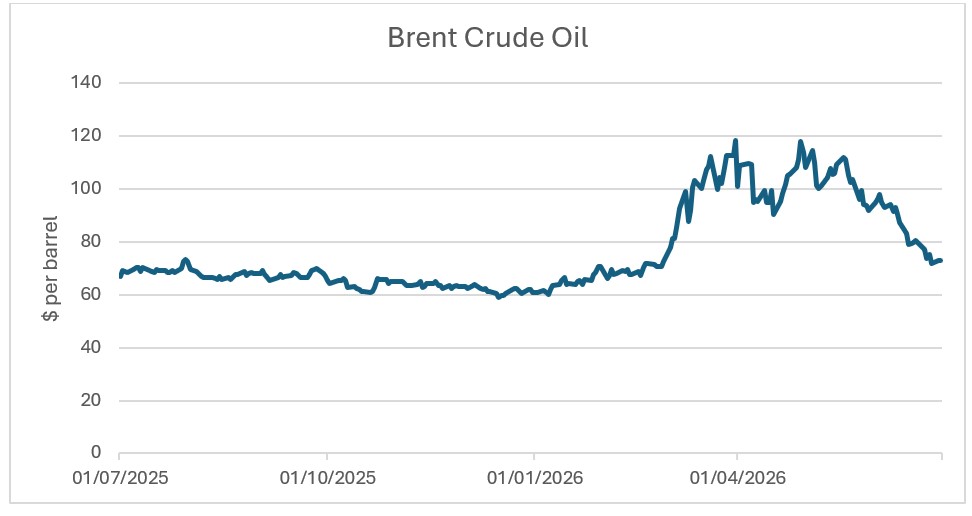

Oil prices fell sharply over June, moving back in line with pre-Iran War levels. The partial reopening of the Strait of Hormuz sent prices tumbling and eased the inflation concerns that had weighed on markets since the spring. By month-end, Brent crude was hovering around $73 a barrel, down sharply from highs of $118 in late April, marking one of the steepest monthly declines of the year.

After a volatile few months of elevated prices, June's move lower was more directional and sustained, reflecting a market increasingly confident in a durable resolution even as it remained alert to the risk of relapse, with renewed clashes around the Strait resurfacing briefly in the final days of the month.

Figure 3: Brent Crude Oil price one-year changes (Source: Bloomberg 2026)

Figure 3: Brent Crude Oil price one-year changes (Source: Bloomberg 2026)

Summary

Overall, the easing of energy-related inflation fears supported a broad rally in sovereign bonds and helped stabilise risk assets, even as renewed tensions near month-end and the AI-momentum rotation kept equity performance uneven.

Looking ahead, June's events have materially improved the inflation and policy outlook. However, the peace agreement remains provisional, the Federal Reserve has turned more hawkish and UK political transition introduces fresh uncertainty.

In a market environment that continues to evolve, diversification and active portfolio management remain key to navigating uncertainty. We continue to monitor market developments closely, ensuring portfolios remain well diversified and appropriately positioned to manage volatility while capturing opportunities as they arise.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to contact your adviser or contact us centrally through our website.

Arrange your free initial consultation

Watch a summary of market activity in June

Download: World Markets At A Glance June 2026![]()

This information in this article is correct as at 09/07/26.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.