Skip to main content

Skip to main content

Advice or Guidance? Why it matters

The terms advice and guidance are often used interchangeably when it comes to financial matters, but in reality, they are very different. And in today’s fast-changing financial landscape, understanding this difference is essential.

Since the introduction of the Pension Freedoms in 2015, individuals have had greater control over how and when they access their defined contribution (DC) pension pots. In response, the government established services to offer free, impartial guidance aiming to help people aged 50+ understand their options and avoid costly mistakes.

Arrange your free initial consultation

One such service is the MoneyHelper platform, provided by the Money and Pensions Service (MaPS), previously known as Pension Wise. The idea was (and still is) to ensure people receive basic, unbiased information before making decisions about their retirement income.

As UK Pensions Minister Guy Opperman put it, “We will introduce new provisions requiring trustees of occupational pension schemes to nudge members to appropriate guidance when they seek to access their pension through the pension freedoms.”

This “nudge” while helpful, begs the question: is general guidance really enough when you're making decisions about what could be hundreds of thousands of pounds of lifetime savings?

What’s the difference between guidance and advice?

Guidance

Guidance is all about information rather than recommendations that are specifically tailored to your situation. It helps you better understand the options available, but the responsibility to decide and act lies entirely with you.

Government services like MoneyHelper for example, or your pension provider’s website may offer generalised content, online tools, or telephone support to guide you through the basics of pensions, investments, or budgeting.

In fact, anyone, including friends or colleagues, can technically give “guidance”. But remember, they aren’t liable for the outcome, and you're not protected if things go wrong.

What you won’t get from guidance:

- Personalised recommendations

- Product suggestions

- A risk assessment of your circumstances

- A regulated professional who is accountable for their advice

Advice

Advice, by contrast, is personal, specific, and regulated. When you take financial advice, you're working with a qualified and authorised Financial Adviser who assesses your entire financial situation, whether that be your goals, risk tolerance or future plans, then recommends a course of action tailored to you.

You’re also protected. Advisers are regulated by the Financial Conduct Authority (FCA) and must adhere to strict standards. If something goes wrong, you may have access to the Financial Ombudsman Service and Financial Services Compensation Scheme.

What about the cost? And is it worth it?

Guidance is usually free and is offered by government-backed services or your pension/investment provider, for example. It’s a good starting point, especially if you just want to understand your options or educate yourself.

Advice, however, is a paid professional service, and like any other expert service, the cost reflects the time and complexity involved.

There are two main types of advisers:

- Independent Financial Advisers (IFAs), who offer whole-of-market advice across a full range of products and providers. All our advisers at The Private Office are Independent Financial Advisers.

- Restricted Advisers, who are limited in the scope of advice they can give, often tied to a particular provider or product range.

Choosing the right type of adviser can significantly impact your financial outcomes. Independent advice means you're more likely to get the best solution for you rather than for the adviser’s institution.

The rise and possible risks of AI in financial guidance

A key change in the advice landscape is the increasing use of Artificial Intelligence (AI), particularly Large Language Models (LLMs) like ChatGPT and other advanced systems.

Using LLMs as a substitute for regulated financial advice carries several risks. To be balanced, however, on one hand, there are benefits, including speed, ease of access and lower (or no) cost. But the pitfalls are real and therefore need to be carefully considered.

Here are some of the potential risks:

- Inaccuracy & outdated / partial information

LLMs may rely on data that is not fully up to date, or doesn’t reflect recent regulatory, tax or product changes. They also generate plausible‑sounding but false or misleading information, known as hallucinations, from time to time. - Lack of holistic view

AI tools typically only see what you tell them. They can’t pick up life‑events you haven’t mentioned, emotional preferences, long‑term goals, or unexpected future needs. A human adviser can ask probing follow‑up questions to uncover things you may not have thought to tell them. - No regulatory protection

Advice from AI tools is not regulated in the way financial advice from an FCA‑authorised adviser is. If things go wrong, there is no ombudsman to make claims, no compensation scheme, and no requirement that those giving the advice act in your “best interests.” - Overconfidence & misplaced trust

Because LLMs are good at generating fluent, confident text, people may overestimate their reliability. - Potential for financial loss

Applying generic or inappropriate advice could cost money e.g. picking wrong investment vehicles or mismanaging tax implications.

The value of advice is still stronger than ever

It can often be a daunting task for individuals to think about their financial futures. Working with a qualified financial adviser can help to alleviate the burden of worry, become better educated on their finances and receive actionable advice on how to improve their situations.

An update to the International Longevity Centre’s research showed the long-term value of advice:

- Advised individuals can be up to 24% better off after a decade compared to those who don’t take advice.

- The benefits are especially strong for those with modest wealth, proving that advice isn't just for the wealthy.

- Those who seek advice regularly (e.g. annually) see even stronger outcomes over time.

In Summary – Guidance vs Advice

| Guidance | Advice | |

|---|---|---|

| Cost | Free | Fee-based |

| Personalised? | No | Yes |

| Regulated? | No | Yes (FCA) |

| Recommendations? | No | Yes |

| Protection? | None | Yes - Ombudsman Compensation Scheme |

| Provided by? | Government, websites, AI, providers | Regulated Financial Advisers |

You get what you pay for, and when it comes to your lifetime savings and financial future, that advice could make all the difference.

Start with a free, no-obligation consultation

If you’re thinking about the next stage in your financial journey and want trusted, independent advice, get in touch to arrange your free consultation with a qualified adviser.

At The Private Office, we offer chartered, independent, whole-of-market advice, recognised as the gold standard in the industry. If you have £100,000 or more in pensions, savings or investments, you can start with a free initial consultation (worth £500) with one of our regulated Financial Advisers.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate tax advice or cashflow modelling.

Living to 100 years - are you financially prepared?

The prospect of living to 100 is a concept that has evolved from a distant dream into a tangible reality for a growing number of people. While modern medicine and healthier lifestyles have made it possible to live longer, the question of whether our finances can keep pace with our longevity is a critical one. For many, the traditional notion of retirement at 65 followed by a relatively short period of relaxation is a thing of the past. The increasing life expectancy coupled with the complexities of the modern world are prompting us to rethink our financial futures. The challenge is not just to live a long life, but to ensure that it is a comfortable one, free from financial worry.

Arrange your free initial consultation

The changing landscape of retirement

The traditional retirement we all plan for is undergoing a significant change. The dual factors of increasing life expectancy and the recent rising cost of living have turned the conventional wisdom on its head. Retirement is no longer a fixed point in time but a new phase of life that could span thirty or even forty years. This extended period requires a more robust financial plan than was previously necessary. The era of retiring and simply living off a single fixed income for life is fading, as we all look forward to a longer and in many cases more active retirement.

Instead, individuals are seeking a diverse stream of incomes from various sources to support a new, longer retirement. This could include a combination of pensions, investments, and even part-time work to supplement savings. The rise of the gig economy and flexible working arrangements has also enabled more people to continue earning a living well into what would have traditionally been considered their retirement years. This shift in mindset is not just about necessity; it is also about a desire to remain active and engaged with society.

What you need to live on

The figures from the Office for National Statistics* reveal that the number of centenarians in England and Wales has reached a record high. This demographic shift has important implications for financial planning. It means that the pension pot we build during our working lives may need to stretch for an additional two decades or more. Consider the difference a single decade can make. Our calculations highlighted that a couple needing an income of £25,000 per year from their pension pot only may need a pension value of around £425,000 for a retirement that lasts 20 years, but that same couple would need an additional £159,000 just to last them until the age of 100. The reality for many is that the state pension alone provides a basic safety net but falls well short of supporting a comfortable lifestyle in retirement.

As we look at the latest Retirement Living Standards** data from the Pensions and Lifetime Savings Association, or PLSA, it becomes clear that building your own wealth is crucial. For a single person to achieve a minimum standard of living, which covers all their basic needs with some left over for fun, they would require an income of £13,400 a year. To reach a moderate standard, allowing for more financial security and flexibility, the figure rises to £31,700 a year, while a comfortable lifestyle requires an annual income of £43,900. For a two-person household, the figures are £21,600 for a minimum standard, £43,900 for a moderate one, and £60,600 for a comfortable lifestyle. This is a clear reminder that we need to take control of our financial futures and ensure that we are saving enough for the lifestyle we desire in retirement.

The family factor

As financial pressures grow, an increasingly common phenomenon is the 'bank of mum and dad'. While it might seem like a simple way to help a child get onto the property ladder or pay for a grandchild's education, the financial support offered to the younger generation is putting a significant strain on the retirement savings of their parents. Many well-meaning parents are using their own hard-earned pension pots to assist their children and in doing so are affecting their own financial security.

This act of generosity can inadvertently create a new layer of risk for their own retirement plans. The money that was carefully set aside for their later years is being used for immediate family needs, reducing the total wealth available to them when they stop working. This places even greater importance on having a comprehensive and forward-looking financial plan that accounts for both your own needs and the needs of your family, without compromising your own long-term wellbeing. This intergenerational financial pressure highlights the need for a holistic approach to financial planning, one that considers the entire family's financial health and requirements, not just that of the individual.

Planning for the future

For most people, the idea of living to 100 is intimidating from a financial standpoint. The question of whether you can afford to live that long often feels like a difficult one to answer. This is where the true value of financial planning comes into its own. At its heart, financial planning is not just about numbers; it is about providing peace of mind. A good financial plan will provide a clear and concise visual picture of your financial future, helping you to understand the impact of your decisions on your wealth over time.

For us at The Private Office, cash flow planning is central to how we work with our clients. We begin by gaining a deep understanding of your current financial situation, including all your sources of income, capital and your expenditures. We use this detailed information to create a dynamic cash flow model that illustrates what your financial future might look like for you under different scenarios. This approach allows us to test your wealth against potential events like a market downturn, higher than expected inflation, a long-term health issue, or unexpected expenses. It also gives us the opportunity to see how your wealth can support you to achieve your life goals such as funding your children’s education, renovating your home, or retiring earlier than planned. By providing this comprehensive visual overview, we can work together to ensure you have the financial freedom to live a long and fulfilling life.

Use our retirement calculator

No one has a crystal ball. But what you do have is a range of tools that can help you understand whether your plans are on track. Our retirement calculator is one of the most useful, especially if you’re hoping to retire at 55.

By inputting your current savings, your target retirement age, and the income you’d like to receive, our retirement calculator can provide an estimate of how long your money might last – and what you’d need to contribute to reach your goal.

Retirement Calculator

A useful tool to get a basic understanding of what your future retirement plans look like is our retirement calculator. From your own personal circumstances , you will be able to forecast an estimate of the pension income you will get when you retire and receive a target retirement income to aim for based on your choices.

It’s important to remember that these tools are only as accurate as the assumptions they’re based on. Investment growth, inflation, life expectancy and future tax rules are all variables. But using a calculator is an excellent way to create a picture of what your retirement might look like – and how close you are to achieving it. This is not guaranteed and is for illustrative purposes only.

How we can help you

A comprehensive financial plan allows you to make informed decisions about your future with confidence and clarity. Living to 100 may seem like a distant challenge, but with the right financial planning and advice, it is a future you can look forward to. We’re offering anyone with £100,000 or more in savings, pensions or investment a free retirement review, worth £500. Why not get in to speak to one of our team for a free initial consultation.

Sources:

* Office for National Statistics

** Retirement Living Standards

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

The Financial Conduct Authority (FCA) does not regulate tax advice or cashflow modelling.

Political uncertainty fails to stamp out market momentum

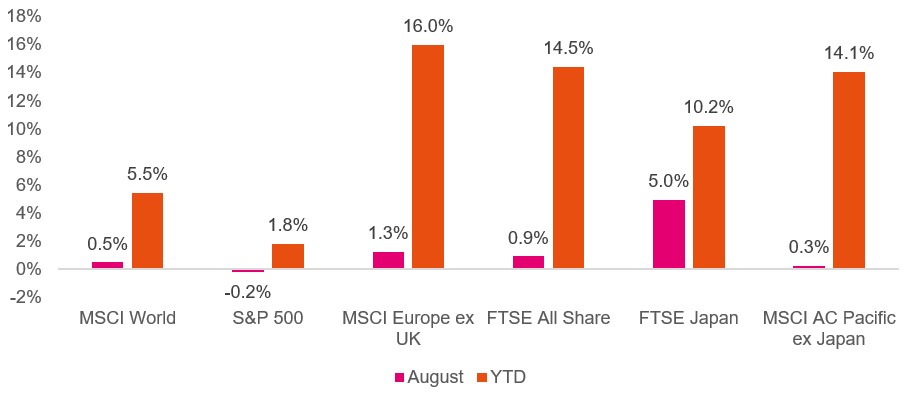

Despite emerging headline risks, global equities continued their positive momentum from the summer with equities broadly higher across major global regions.

US: Strong earnings, AI concerns

Starting with US markets, equities were flat in sterling terms (up 2% in US$) as we witnessed renewed investor scepticism over the commercial benefits of AI. Technology stocks suffered as a research paper from Massachusetts Institute of Technology (MIT) showed fewer than 5% of AI pilot programmes were profitable. Even Nvidia, which delivered one of the earnings season’s highlights with 56% year on year revenue growth, saw its share price fall after a data centre revenue miss - a reminder of the lofty expectations currently priced in.

Arrange your free initial consultation

Despite the relative “disappointment” of Nvidia’s earnings, it was another strong period for US corporates with 81% of companies reporting a positive earnings surprise with companies reporting greater earnings than the markets had been expecting. Furthermore, cyclical sectors - sectors which are sensitive to the health of the US economy improved in Q2 with financials and consumer discretionary sectors reporting higher earnings growth than in Q1.

In a case of “bad news is good news”, US unemployment rose to 4.2%, but equities found support after Federal Reserve Chair Powell’s Jackson Hole remarks signalled shifting economic risks - leading to a belief that this could justify interest rate cuts.

Japan: Growth surprise and political change

Japanese equities advanced on news of a trade deal with the US, easing pressure on export focused companies. Positive GDP growth also surprised to the upside, with the economy expanding 0.3% quarter on quarter. Meanwhile President Ishiba is likely to step down as his party, the Liberal Democratic Party, is looking to hold an internal leadership vote which would see him ousted following their loss of a majority in the recent lower house election. Markets have reacted positively to this news with the expectation that his replacement will be more market friendly and look to increase government spending.

Europe: Gains despite political turmoil

In Europe, political turmoil in France weighed on local markets, but at an aggregate level, European equities posted gains, building on strong year to date performance. This outperformance is a result of a combination of cheap valuations, increased fiscal stimulus and investors looking beyond the US for opportunities.

Figure 1. Regional equity returns (Source: Pacific Asset Management, August 2025).

UK Macro Economy and Inflation

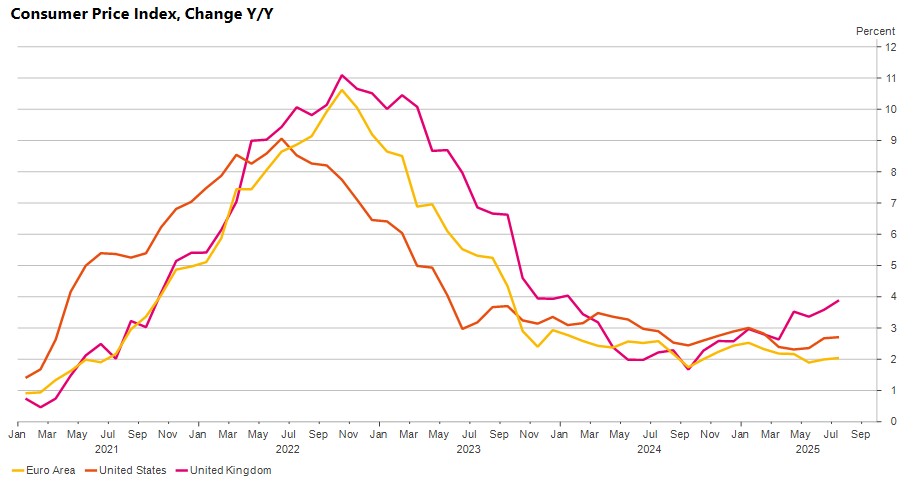

The global economy continues to show resilience, but UK inflation once again surprised to the upside, reaching 3.8% in July versus expectations of 3.7%. Over the past year, UK inflation has more than doubled, while Eurozone inflation has risen more modestly from 1.7% in September 2024 to 2.1% (see Figure 2).

Figure 2. Inflation (Source: Pacific Asset Management, August 2025).

Drivers of the UK’s higher inflation include rising household costs such as electricity, water and utilities, faster wage growth than in Europe, and the impact of new taxes and regulations. This poses a challenge for the Bank of England, whose 2% inflation target remains a distant target at this time. The employment market is also showing signs of strain, with unemployment climbing to 4.7% - the highest in four years.

Rates, Yields and Fiscal Pressures

In early August, the Bank of England cut rates by 0.25% to 4%, a two year low, but cautioned that further cuts may be less likely than markets expect. Yields moved higher, with the 30 year gilt reaching a 27 year peak. This creates a vicious cycle for the UK government: higher yields raise borrowing costs, adding to the debt burden and pushing yields up further (see Figure 3).

Figure 3. 30yr UK Government Bond yield (Source: Pacific Asset Management, August 2025).

Figure 3. 30yr UK Government Bond yield (Source: Pacific Asset Management, August 2025).

However, it is worth noting this is not a UK specific issue. Across developed markets, yields are rising as investors question long term government fiscal stability. Political consequences are also emerging in France, Prime Minister François Bayrou lost a confidence vote over a €43.8 billion budget cut aimed at reassuring markets about fiscal discipline. This means France will see its fifth Prime Minister in less than two years, adding to the feeling of political and economic uncertainty.

Attention will soon turn to the UK’s Budget announcement on 26 November, with speculation building over the measures that may be introduced to address fiscal challenges.

We will, of course, keep you informed as soon as we have more clarity. Until then, I’m reminded of a remark by former President of the European Commission, Jean Claude Juncker: “We all know what to do, but we don’t know how to get re-elected once we have done it.”

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 09/09/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

Oasis of positive market sentiment in July might not live forever

Following a strong run in May and June, markets maintained their upward momentum in July, with risk assets once again delivering healthy returns. Equities benefited from a combination of easing global trade tensions, resilient corporate earnings, and greater policy clarity, particularly from the US. While concerns around inflation and government borrowing remain, investors found several reasons to stay positive on the outlook.

Arrange your free initial consultation

US Policy clarity points the way

One of the key macro developments came from the United States, where the “One Big Beautiful Bill Act” (OBBBA) was passed. The bill outlines front-loaded tax cuts paired with long-term spending reductions, signalling a more expansionary fiscal stance. While the initial market reaction included a sell-off in US Treasuries as investors digested the long-term implications for debt, equities rallied as the bill was seen as reducing short-term political and economic uncertainty.

Markets also welcomed progress on trade. Although the temporary pause on reciprocal tariffs between the U.S. and China is set to expire in early August, July brought signs of cooperation. Renewed trade dialogues with Japan, Vietnam and the EU supported risk sentiment.

Equities and Bonds - a positive picture, generally!

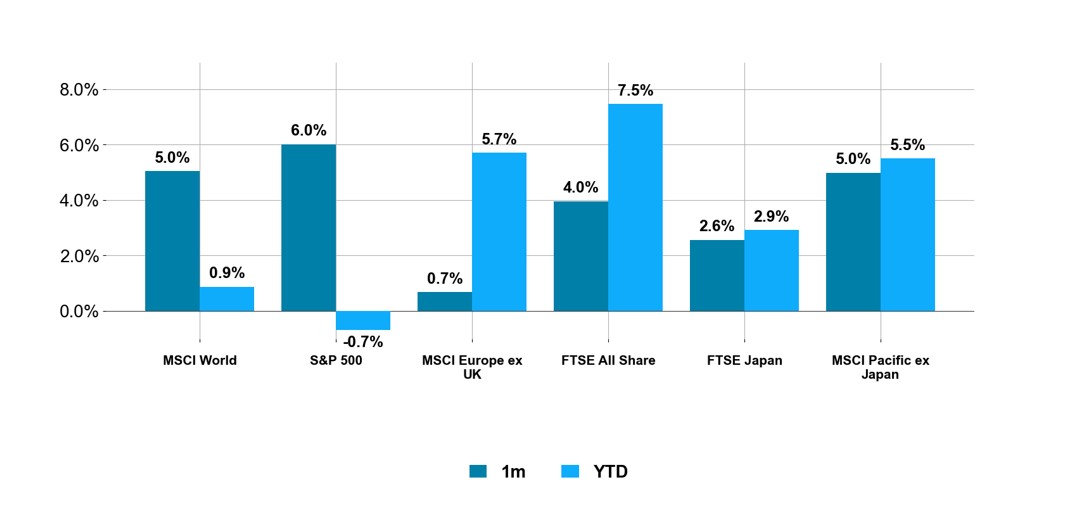

Equities continued their upward march. Global developed markets rose by 5% in July (in sterling terms), with U.S. stocks once again leading the way. The S&P 500 reached new highs as nearly 80% of reporting companies exceeded both earnings and revenue expectations for Q2 2025. The so-called "Magnificent 7" tech giants continued to outperform, though strength was also seen in cyclicals and financials.

UK equities benefited from a rally in energy and materials companies, which continue to trade on low valuations. Notably, both BP and Shell saw gains over the month. At the same time, signs of a revival in the Chinese economy - driven by improving activity and ongoing policy support boosted Chinese equities and supported broader Emerging Market performance.

Figure 1. Regional equity returns (Source: Pacific Asset Management, July 2025).

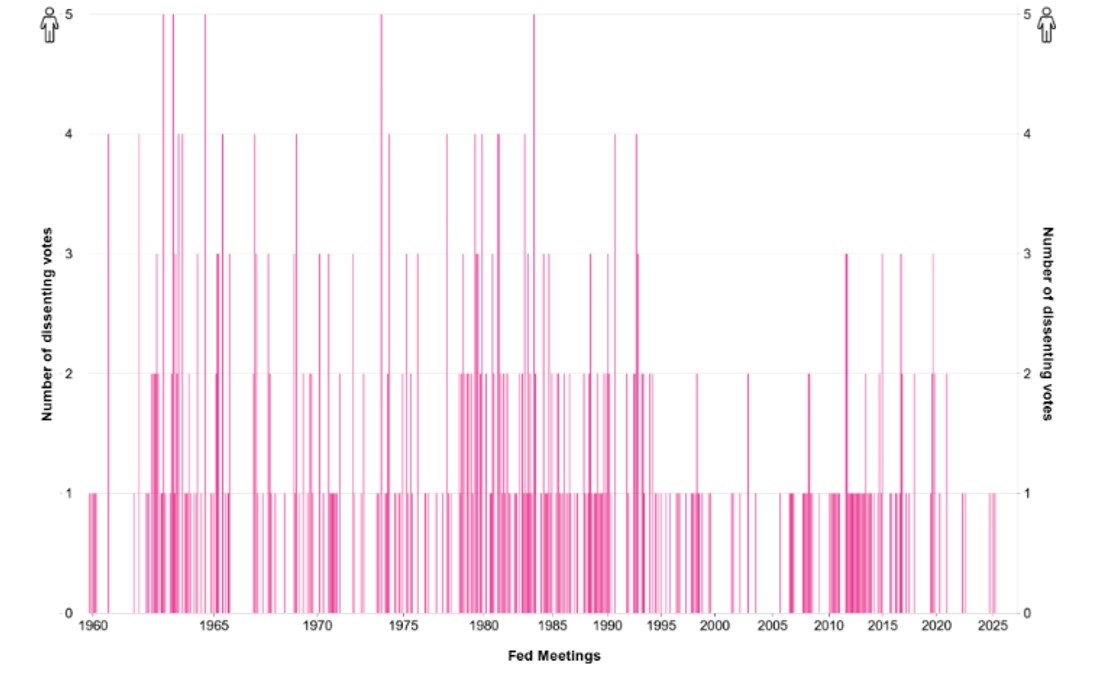

While equity markets rallied, bond markets were more mixed. U.S. Treasury yields rose again as investors grappled with an uncertain inflation outlook and reassessed the likelihood of interest rate cuts in light of fresh fiscal stimulus. This debate played out publicly within the Federal Reserve, which elected to keep rates on hold despite two Governors - Bowman and Waller - dissenting and voting for a cut, marking the first dual dissent since 1993 (see Figure 2).

Figure 2. Federal Reserve voting record: Number of dissents (Source: Pacific Asset Management, July 2025).

European yields also edged higher, while U.K. gilts came under pressure following a hotter-than-expected inflation print, with core CPI rising to 3.7%. In Japan, 10-year government bond yields reached 1.6%, the highest level in years, as markets priced in sticky inflation and growing political uncertainty.

In contrast to sovereign debt markets, corporate credit held up well in July. Credit spreads tightened modestly, supported by strong earnings, healthy balance sheets, and continued demand for yield. Both investment-grade and high-yield bonds saw steady inflows, highlighting investor confidence in the underlying fundamentals of corporate issuers.

The outlook for the year - steady as she goes!

As we head into the latter part of the year, investor sentiment appears cautiously optimistic. The strong performance of risk assets over recent months has been underpinned by solid earnings, stable economic data, and improving global trade dynamics. However, with equity markets pricing in a relatively positive outlook, the bar for up-side surprises is getting higher.

Inflation remains a key variable to monitor. While headline inflation has eased significantly across most regions, underlying pressures particularly in labour and services remain persistent in some economies. Central banks continue to walk a careful line, trying to support growth while ensuring inflation expectations remain controlled. Whether this delicate balancing act can continue without unsettling markets is likely to be a central theme in the months ahead.

Fiscal policy will also be an area of ongoing focus. The ‘OBBBA’ and similar initiatives elsewhere reflect a broader willingness among governments to support growth through targeted stimulus. While these measures have helped underpin market confidence in the short term, they also bring questions about long-term debt sustainability. At present, markets appear comfortable with that trade-off, but investors will be watching closely for signs of strain.

For now, financial markets are navigating these conflicting drivers with a sense of cautious confidence. Earnings remain a key support, and global growth, while not without challenges is holding up better than many had feared earlier in the year.

As always, a diversified approach and close attention to the evolving macro and policy landscape will be key to managing portfolios through what remains a complex and fast-moving environment.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 08/08/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

Planning for the costs of a private education

The introduction of VAT on private school fees in January 2025 has marked a significant turning point for families and private schools alike. Already grappling with inflation and rising living costs, parents now face an even steeper financial hurdle to provide their children with an independent education. Schools themselves are also under pressure, contending with squeezed budgets and declining enrolments.

Arrange your free initial consultation

Since the start of the year, more than 32,000 pupils have left private education in the UK, many moving into the state sector. In the same period, at least 21 private schools have closed their doors permanently due to reduced demand and increasing running costs, this in addition to those who closed pre-empting the increase in taxes, both VAT and employers National Insurance.

Despite some of the political controversy surrounding the role of fee-paying schools, the fact remains that the parents of over 620,000 children choose an independent school.

Many middle-class families spend decades planning in the cost of a private education to their finances, but despite the perception of some, it remains the case that for many, affording a private education is the result of tough decisions and compromises, often made years before a child ever sets foot in a classroom.

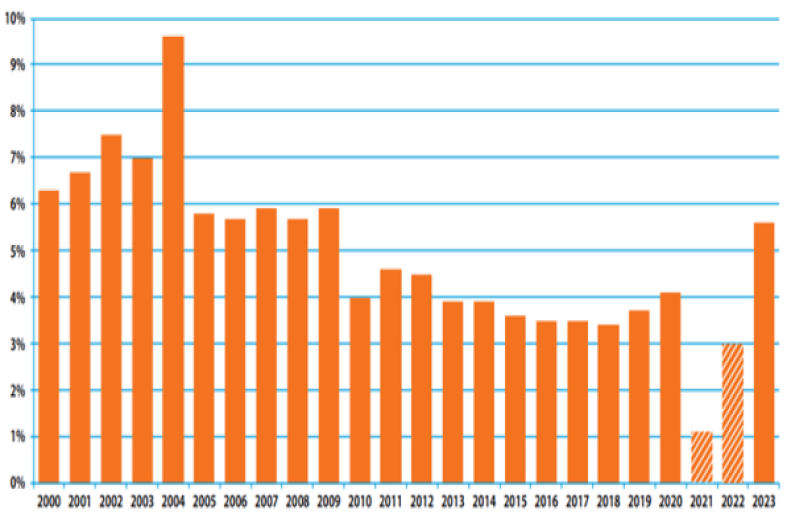

With the cost of living in the UK remaining elevated, many parents will find themselves increasingly stretched in covering Private School fees, which have displayed an average increase of 7.1% from 2024 and some reports suggest this has doubled in 2025.

Figure 1 - Fee increases since 2000 (like-for-like)*

*Source: ONS, ISC Census, 2023

With school fees in England averaging £18,036 a year for day fees, or £42,300 for boarders, this is the highest level on record. Looking back to 2013, the average annual cost of sending a child to a Private School with boarding was £27,600. There is also the implicit sums to be paid beyond the headline fees. The cost of lunches across the school year, musical lessons and overseas trips can often mean that real cost is actually far higher. These are averages and generally junior schools cost much less than senior schools; so many parents face a stark choice at age 11 or 13 when costs can increase significantly.

This, coupled with the added strain of paying such fees from income that has often already been taxed at 40 or 45%, means that many who have previously worked hard to privately educate their children may be reconsidering the affordability of doing so. With many families often having more than one child in education at once, this only serves to add to the pressure on the balance sheet of the Bank of Mum and Dad, or Grandma and Grandad.

Unfortunately, school fees cannot be offset against a tax bill, however there may be some measures that can be taken through careful planning and structuring that can help to ease the burden.

Many could be missing a trick with some of the options available for reducing the all-in cost on parents or grandparents to giving their children or grandchildren an independent education:

Paying fees upfront

Perhaps the simplest option, but with the most significant initial cost. Although less suitable for those concerned with shorter-term affordability, those with sufficient liquid wealth who are willing to take a longer-term view may benefit from paying the cost of their child’s education as a one-off lump sum.

As detailed earlier, private school fees can inflate significantly over the course of an education so there may be merit in locking in a lower cost by paying everything at the outlay. This is something that is offered by many schools.

Some schools will also offer investment schemes, wherein parents or grandparents pay a lump sum in advance which is then invested by the school into low-risk investments. As private schools have charitable status, the returns on the investment will be tax-free. If you were to make the same investments yourself, you could have to pay tax on the growth.

Before considering either of these options you should take advice, paying in advance is in effect making a loan to a business, often a small one and some institutions that have closed their doors offered such options.

Family Investment Companies

Sometimes considered as an alternative to trusts, for those with larger amounts of investable wealth, properly structured they can be excellent planning tools for a family.

Like adults, all children have a personal allowance of £12,570 which can be earned tax free. Similarly, they will also have a dividend allowance of £500 for the 2025/26 tax year.

Given that many school-age children are unlikely to have earnings using up the full extent of their allowances, allocating non-voting shares to children so that these allowances can be utilised can be an effective way to pay fees tax-efficiently, and make use of assets that are already generating capital growth or income for the company.

This can be particularly effective where more than one child is attending a fee-paying school as each child will have their own allowances.

An important point to note is that this option only works where the shares in the company are gifted by grandparents rather than parents. This distinction matters as parents will be taxed on their minor children’s income where they have gifted shares to their children.

The parental rule applies to income and not gains, so in some circumstances funds settled by parents could use a child’s capital gains exemption and then pay the lower rate of CGT, currently 18% for gains in the basic rate tax band, up to £37,700

Family Trust Options

Trusts are separate legal entities, managed and controlled by trustees for the benefit of the trust’s beneficiaries. Like with companies, beneficiaries of a trust will be taxed on any income in their personal name. Therefore, a grandparent settling funds into a trust structure can be a useful way of reducing an inheritance tax liability, whilst retaining control and paying fees tax-efficiently. If a trust is set up by parents then tax falls back on the parents, so this route is only effective for grandparents, or where funds are earmarked for later in life, when the beneficiaries are adult.

Offshore Bonds

For those already holding, or considering the set-up of an offshore bond, there are also planning options:

Bonds are normally split into multiple policy “segments”, and a grandparent can gift segments to the child who encashes it to pay for school fees in a given year or term.

The policy segments can be assigned to children when they reach school age via a Bare Trust. As a result (providing that the grandparents have invested wisely and reviewed their investment on a regular basis) the tax on the gain would, in theory, be payable by the children. However, if within their personal tax allowances, it will be tax-free.

How we can help

As with most complex areas of planning there is a balance to be struck between tax-efficiency, control and flexibility. Whilst the savings can be significant if things are structured correctly, the margin for error is high and can leave you in a worse position than at the outset if the appropriate steps are not taken. There are a number of nuances above that are detailed in this article and it is therefore important to seek professional advice in exploring your options to ensure that you do not fall foul of HMRC rules.

Why not contact us today to speak to one of our experts for a free initial consultation?

Arrange your free initial consultation

The information contained within this article is for guidance only and does not constitute advice which should be sought before taking any action or inaction. Investment returns are not guaranteed and you may get less than you originally invested.

The Financial Conduct Authority (FCA) does not regulate Trusts.

How much do you need to retire at 55?

Retiring at 55 is an appealing prospect. Many people dream of stepping away from work while they’re still active enough to enjoy their newly afforded free time. But while the desire may be common, achieving it is something altogether more complex. Early retirement means giving up years of income and stretching your savings and investments over a longer retirement. For some, this can be done. For others, it may require a more nuanced approach.

So, what does retiring at 55 really take? And how do you know if it’s possible for you?

Arrange your free initial consultation

How much do you need to retire at 55?

The answer to this depends on not just your retirement savings but also on the lifestyle you want to lead once you’ve stopped working. Recent figures from The Pensions and Lifetime Savings Association looked at average retirement income in a more lifestyle focused manner. The groups are split into Minimum, Moderate and Comfortable with a single person varying between an income of £13,400 a year for a minimum retirement to £43,900 a year for a comfortable retirement. For a couple these figures varied from £21,600 to £60,600 respectively.

But retiring at 55 has many additional challenges. Unlike those retiring at state pension age, you may need to support yourself entirely from your own savings for at least 12 years or more, depending on when you qualify for the state pension to supplement your savings. The state pension is unlikely to cover all your needs. The full new state pension currently pays around £11,973 a year as of April 2025, provided you’ve paid at least 35 years of qualifying National Insurance contributions. Until then, your private pension, ISAs, savings, or other investments will need to do all the heavy lifting.

Can I afford to retire at 55?

You may already have a decent pension pot and additional investments. You may own your home outright or have other sources of income, such as rental property. But even with a solid base, it’s vital to understand whether your money will last.

One of the common challenges early retirees face is the temptation to draw too much too soon. The earlier you access your pension, the longer it needs to last – and the more vulnerable it becomes to poor investment performance or inflation. If you withdraw too aggressively during a market downturn, you risk depleting your pot much faster than expected; this is known as sequencing risk.

There’s also the issue of timing. From 2028, the minimum age for accessing defined contribution pensions will rise from 55 to 57, unless you have any existing pension age protections in place. If you turn 55 after this point, your earliest retirement date may be later than you expect. And if you were planning to use your pension as your main income source, this could impact your strategy.

It's worth considering whether full retirement is even what you really want. Semi-retirement, perhaps reducing your hours, freelancing or consulting, can give you more flexibility.

Use our retirement calculator

No one has a crystal ball. But what you do have is a range of tools that can help you understand whether your plans are on track. Our retirement calculator is one of the most useful, especially if you’re hoping to retire at 55.

By inputting your current savings, your target retirement age, and the income you’d like to receive, our retirement calculator can provide an estimate of how long your money might last – and what you’d need to contribute to reach your goal.

Retirement Calculator

A useful tool to get a basic understanding of what your future retirement plans look like is our retirement calculator. From your own personal circumstances, you will be able to forecast an estimate of the pension income you will get when you retire and receive a target retirement income to aim for based on your choices.

It’s important to remember that these tools are only as accurate as the assumptions they’re based on. Investment growth, inflation, life expectancy, long-term care needs and future tax rules are all variables. But using a calculator is an excellent way to create a picture of what your retirement might look like – and how close you are to achieving it. This is not guaranteed and is for illustrative purposes only.

How to really look into your financial future

While calculators give you a high-level snapshot, cash flow forecasting takes your planning a step further. It is a more personalised approach that helps model your financial future in detail.

A cash flow forecast looks at all aspects of your income, spending and assets, both now and in retirement. It takes into account your savings, pensions, investments, property, and any planned large expenses, like helping children with a house deposit or taking a round-the-world trip.

What makes it powerful is that it’s dynamic. With the help of your financial planner, you can run scenarios to see how your financial position changes if you retire earlier, downsize your home, delay your state pension, or take lump sums from your pension. You can also test the impact of market downturns, inflation spikes, or a longer-than-expected retirement.

This kind of planning gives you greater confidence in your decisions. Rather than relying on rules of thumb, you can understand exactly what is affordable – and what changes might be needed to get there.

At The Private Office, we believe cash flow forecasting is a key part of any long-term financial strategy. It provides a visual projection of your financial life, highlighting when and where gaps might arise and helping you take action early to avoid them.

Pension drawdown or annuity – which is best for early retirees?

If you’re planning to retire at 55, it’s likely you’ll be managing your pension using drawdown rather than buying an annuity. Drawdown allows you to keep your pension invested while taking income as needed. This offers more flexibility, especially for those who expect their income needs to change over time.

However, it also means more responsibility. You’ll need to keep an eye on investment performance, monitor your spending, and ensure your pot lasts. For some, this can be daunting, and this is where advice becomes so valuable.

Annuities, on the other hand, offer peace of mind through guaranteed income for life in exchange for flexible access to a ‘pot of money’. But if you buy one at 55, the rates are generally much lower than if you wait until your 60s or later. For that reason, many early retirees opt to draw down first, possibly considering an annuity later on when the rates become more attractive or even a combination of the two later in life.

Is early retirement realistic for you?

For some people, retiring at 55 is entirely realistic. For others, it might require adjustments to spending, saving more in the years ahead, or even considering part-time work to bridge the gap.

What’s most important is having a plan. That plan should be based on careful analysis, not guesswork. It should be flexible enough to adjust when life changes. And it should take account of your goals and values, not just the numbers.

Seeking financial advice can play a critical role here. We can help you define your goals, assess your current position and build a strategy that puts you on the right path, whether that means retiring at 55, or simply retiring with confidence, whenever the time is right for you.

We’re currently offering those with £100,000 or more in cash, investments or defined contribution pensions a free cash flow forecast review worth £500. For more information why not get in touch.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.

Market resilience trumps geopolitical uncertainty

Quarter 2 2025 Reflecting on ‘interesting times’!

Q2 (April - June 2025) was another eventful quarter for investors, marked by shifting trade policies and heightened geopolitical risks in the Middle East. Despite this, markets remained resilient as the worst-case scenarios, failed to materialise.

The announcement of the US-China trade deal on June 11, giving the US access to China’s rare earth minerals, helped ease investor uncertainty. The deal also reduced tariffs on Chinese goods from 146% to 30% and this was subsequently followed by a separate agreement with Vietnam. While the initial tariff on Vietnamese goods stood at 46% on “Liberation Day”, it was later reduced to 20% for direct imports, and 40% for trans-shipped Chinese goods. This marked a significant step in the US’s effort to prevent tariff ‘avoidance’ via Vietnam.

Arrange your free initial consultation

In the Middle East, tensions escalated between Israel and Iran after Israel launched an airstrike on Iranian nuclear facilities. Oil prices briefly spiked above $80 per barrel, reflecting fears of supply disruption through the Strait of Hormuz, which carries nearly 20% of global oil shipments. The subsequent involvement from the US risked a further fall-out, however, despite Iran launching (a well telegraphed) airstrike on US facilities in Qatar, a truce was ultimately agreed, and the price of oil fell back to below $70 dollar a barrel.

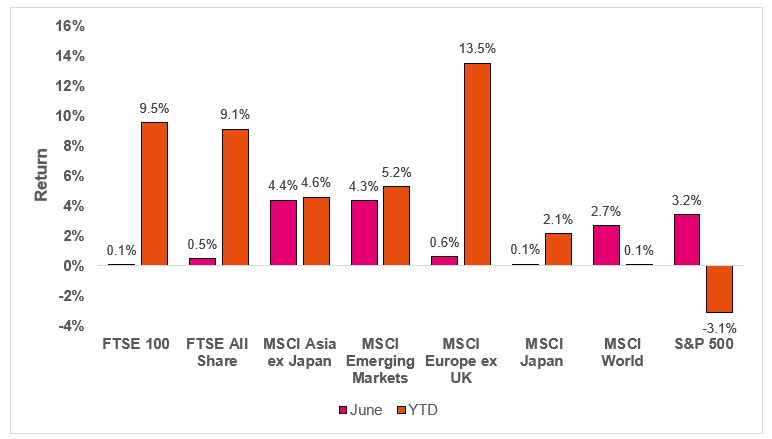

In equity markets, we saw the positive momentum from May continue with most major markets advancing last month (see Figure 1).

Figure 1. Regional market returns (in GBP terms) (Source: FE Analytics, July 2025)

Once again, the S&P 500 had a strong month, delivering a return of 3.2% (in GBP terms). Investors looked beyond the uptick in inflation - its first rise in four months - and the contraction in U.S. GDP, instead focusing on easing geopolitical tensions, an improved trade outlook, and stronger-than-expected corporate earnings.

Gains were broad-based across most sectors with technology stocks once again performing well, climbing more than 7% over the past month.

What a first half! – the key points of 2025 so far

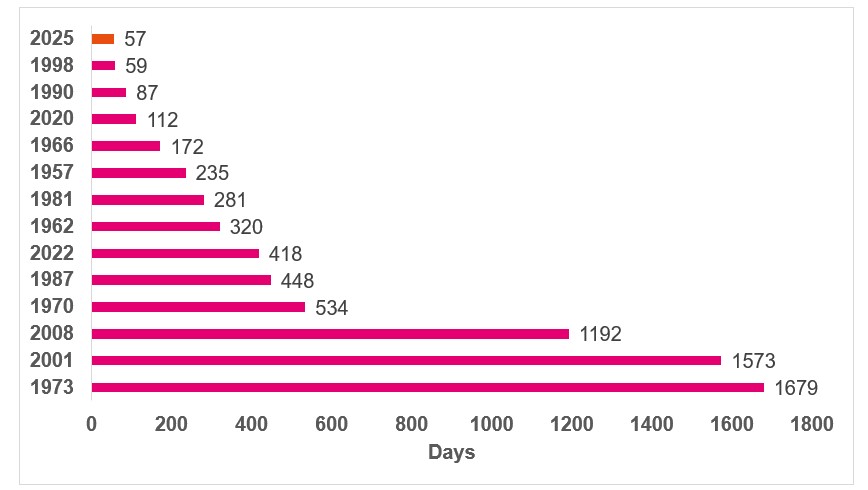

June marked the end of a remarkable first half of the year - not only for U.S. technology companies, which rebounded strongly with a 14% gain in Q2 after falling 15% in Q1- but also for the broader S&P 500. The index staged one of the fastest recoveries in recent history. After declining 20%, it took just 57 days to recover from the falls - making it the quickest rebound since the 1950s. For context, the average recovery time from a similar decline has historically been 511 days (see Figure 2).

Figure 2. S&P 500: Days to recover from a 20% drawdown (Source: Norgate Data, Pacific Asset Management, July 2025)

Beyond the U.S., Euro Area GDP grew by 0.6% quarter-on-quarter in Q1, following a 0.3% increase in Q4 2024. This marks the fastest pace of expansion since Q2 2022. In response to moderating inflation - now at 2% - the European Central Bank (ECB) delivered another 25-basis point rate cut, lowering its benchmark rate to 2%. This was the ECB’s eighth rate cut over the past 12 months. The combination of accelerating growth, declining inflation, easing monetary policy, and ongoing fiscal support has helped drive European equities to a return of nearly 14% in 2025 year-to-date.

In the UK, the Bank of England voted 6–3 to maintain interest rates at 4.25%. However, with signs of labour market stress and slowing economic momentum - as evidenced by a 0.3% contraction in GDP in April - markets are now pricing in two additional 25 basis point cuts before year-end.

Despite ongoing economic and fiscal challenges, the FTSE 100 reached an all-time high last month. Investors looked beyond domestic headwinds, turning to UK equities as an alternative to U.S. markets. The index was further boosted by strong gains in major oil companies such as BP and Shell, which rallied in the immediate aftermath of the Israel–Iran conflict, as rising geopolitical tensions pushed oil prices higher.

Is US ‘exceptionalism’ back?

The recent rally in U.S. equities has led some to suggest that the much quoted "U.S. exceptionalism" is back. While we agree that the outlook has improved - not only for the U.S., but for the global economy - we believe the bigger story lies in the broader structural shifts underway. In a previous update, we discussed how President Trump’s perspective on the U.S.’s global role could mark a watershed moment. His re-election and subsequent policy direction may serve as a pivotal catalyst for change in global territories beyond U.S. borders.

Consider Europe as an example. At the start of the year, both France and Germany were facing political uncertainty, neither with a stable incumbent government. A previous lack of fiscal investment had contributed to low growth across the Euro area. Fast forward to today, and the landscape has shifted significantly: Germany is now planning to deploy €1 trillion in spending, support for the European Union has surged - driven by a "rally around the flag" effect - and European policymakers are signalling a strong intent to step up and fill the leadership void left by a possibly more isolationist U.S.

Time will tell how this transformation plays out, however, it's already clear that President Trump’s return has acted as a catalyst for much-needed strategic realignment in Europe.

Looking to the future?

Looking ahead, we do not expect U.S. exceptionalism to persist in the same way it has over the past decade. That said, this is not a call to “sell the U.S.” The United States remains home to some of the most innovative, and resilient companies in the world, underpinned by a deeply entrenched capitalist ethos that is unlikely to fade. However, opportunities outside the U.S. have grown meaningfully - particularly among companies trading at more attractive valuations and better positioned to benefit from a world in which the U.S. becomes more domestically focused.

In this environment, diversification remains essential - not only as a tool for managing risk in a rapidly evolving world, but also as a means to take advantage of emerging opportunities across global markets.

As ever, if you have any questions about our commentary or would like to discuss your own portfolio in more detail, get in touch with your Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 11/07/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

How to decide where to invest your Pension funds

When thinking about retirement, many people focus on how much they’ve saved. But just as important is how that money is invested. Pension investment funds play a vital role in shaping the lifestyle you will enjoy in your later years. Making the right decisions today could mean the difference between just getting by and living comfortably throughout retirement. If you are unsure where to begin, understanding your options and how they align with your personal goals is a key first step.

Arrange your free initial consultation

Making sense of your options

Navigating the landscape of pension investment funds can feel overwhelming. With thousands of funds available, including active and passive strategies, thematic investments, ethical funds and more, the choice is vast. Selecting the most suitable pension investment funds will depend on your unique circumstances, and no single option is right for everyone.

Some investors prefer actively managed funds, where managers hand-pick investments with the aim of outperforming the market and minimising losses with the potential to make a higher return than the average. Others might choose passive funds, which track an index or market rather than trying to beat it and tend to have lower costs. Each approach has its merits, and in many cases a blend of both can be appropriate.

No matter how you choose to invest, the key is to ensure your pension is not left on autopilot. Markets evolve, economic conditions shift, and your personal situation will change over time. Keeping your pension aligned with these developments is essential to giving yourself the best chance of a financially secure retirement.

What is your attitude to risk?

Before deciding where to invest your pension fund, it’s crucial to understand your attitude to risk. Everyone has a different threshold. Some people are more comfortable with the ups and downs of markets, while others prefer the relative stability of more conservative investments.

Your tolerance for risk may depend on a number of factors, including how long you have until retirement, your wider financial situation, and your personal experiences. If you are younger and still several decades away from retirement, you may feel comfortable taking on more risk in exchange for the potential of higher returns. As you get closer to accessing your pension, you may prefer to reduce your exposure to volatility.

When considering risk, it’s important to take emotion out of the equation. Emotional investing, where decisions are driven by fear, anxiety or overconfidence, often leads to poor outcomes. Market fluctuations can tempt investors to make impulsive changes, such as selling during downturns or chasing returns during rallies. These reactions can often do more harm than good. A well-thought-out strategy that matches your true risk tolerance and overarching financial plan will serve you far better than one driven by how markets make you feel at any given moment. Removing emotion helps you stay focused on your long-term objectives and avoid knee-jerk reactions that could undermine your retirement goals.

Investment risk in pension fund portfolios is largely unavoidable, but it can be managed. By aligning your investment choices with your risk profile and timescales, you can create a more resilient pension plan. Speaking to a financial adviser can help to determine an appropriate risk profile and strategy and empower you to make confident decisions that suit your needs.

Where are your pension savings currently invested?

Many people are unaware of where their pension savings are actually invested. If you are enrolled in a defined contribution pension scheme, your contributions, along with those from your employer, are invested in pension funds. These can include a mix of equities, bonds, commodities, property and cash.

A suitable pension investment fund would typically be diversified across different regions and asset types to help reduce the impact of any single area performing poorly. You may already be in a default lifestyle fund, which gradually shifts your investments to lower-risk options as you approach retirement. Whilst seemingly convenient, it’s worth reviewing if this strategy is truly the right fit for your specific goals, timescales and prevailing market conditions.

Looking into where your pension is invested can reveal opportunities to improve potential outcomes. If your current fund has not performed in line with similar alternatives, or if the risk profile does not suit your current circumstances, it may be time to explore other options.

How you plan to take your pension

How you intend to draw on your pension in retirement may have a significant influence on how it should be invested now and in the glidepath towards retirement Some people will want to take a tax-free lump sum and buy an annuity, which guarantees an income for life but offers limited flexibility. Others might prefer pension drawdown, which allows you to keep your pension invested and flexibly withdraw income as needed.

Each of these options carries different levels of investment risk and potential reward. An annuity typically removes investment risk altogether but might provide a lower income, particularly when interest rates are low. Drawdown keeps your pension exposed to the market, offering the possibility of capital growth even in retirement, but with the risk of loss if markets or investments perform poorly.

By understanding your likely income needs and how flexible you want your retirement income to be, you can better match your pension investments to your plans. Receiving professional advice on the options and considerations can be extremely valuable, as the decisions you make now may have lasting consequences.

When do you plan to access your pension?

Your investment choices should take into account the time horizon until you need to start drawing on your pension. If retirement is 20 or 30 years away, you may consider a growth-oriented strategy, as the longer-term time horizon allows you to ride out short-term fluctuations. For those closer to retirement, capital preservation becomes more of a priority.

Timing also affects your exposure to investment risk. Markets and investments may perform unfavourably at the point you begin to withdraw income. If your portfolio suffers a decline just before or during the early years of retirement, the impact on your overall pension pot can be significant.

This is referred to as “sequencing risk” and highlights the importance of reviewing your pension strategy regularly and creating a financial plan. A carefully managed transition from higher to lower risk assets, known as de-risking, is often used to address this concern. Some pension funds do this automatically, but it is not always tailored to your specific plans.

The sooner you engage the better

Deciding where to invest your pension funds is not something to put off until the future. The sooner you engage with the options available, the more control you can have over your financial future. Understanding your attitude to risk, the structure of your pension plan, and how and when you expect to retire are all crucial to making informed choices.

Whether you are seeking long-term growth or greater stability as you approach retirement, there are solutions available. The challenge is identifying what is right for you. Exploring where to invest your pension fund and reviewing the investment risk and suitability of the current strategy should be a regular part of your financial planning.

Speaking to an independent financial adviser can help you gain clarity, avoid common pitfalls and put in place a strategy that evolves as your life does. It is never too early or too late to take control of your pension. The future you want could depend on the actions you take today.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash or tax advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.

The growing burden of Stealth Taxes

Over the past few years, millions of people across the UK have found themselves quietly paying more tax, even if they haven’t seen a single change to their tax rate. This subtle yet powerful shift in the nation’s tax landscape has not been driven by headline-grabbing announcements, but rather by what are commonly referred to as “stealth taxes.” These measures raise government revenue not through overt rate increases, but via frozen thresholds and shrinking allowances, often going unnoticed until the financial pinch begins.

Arrange your free initial consultation

A surge in pensioners paying higher tax

New figures obtained from HM Revenue and Customs under the Freedom of Information Act reveal just how widespread this issue has become. According to Steve Webb, former Pensions Minister, the number of pensioners now paying income tax at the higher (40%) or additional (45%) rates has more than doubled in just four years. In 2021/22, around 494,000 pensioners were affected; today, that number has surpassed one million.

Even more revealing is the total number of pensioners paying income tax at any level. This has risen from 6.7 million to 8.8 million over the same period, an increase of nearly a third. This is not due to tax rate hikes, but instead to frozen thresholds and rising pension income pushing more retirees into tax-paying brackets.

How fiscal drag is quietly hitting retirees

At the heart of this trend is a phenomenon known as “fiscal drag.” This occurs when tax thresholds remain static while incomes, particularly pensions, increase with inflation. The personal allowance and higher-rate threshold have both been frozen since 2021 and are expected to remain frozen until 2028. During this time, state and private pensions have risen, mainly due to inflation and the government's commitment to the triple lock.

From April 2025, the full new state pension rose to £11,973, just below the £12,570 personal allowance. This means that for anyone with a modest workplace or private pension on top of their state entitlement, paying income tax has become the norm rather than the exception.

More than just Income Tax

Crossing into higher-rate tax bands doesn’t just mean paying more on income, it also has knock-on effects for other allowances. For instance:

• The Personal Savings Allowance is halved from £1,000 to £500 for higher-rate taxpayers.

• The Dividend Allowance has been reduced in recent years, currently sitting at just £500 (down from £2,000 in 2022).

• The Capital Gains Tax exemption was halved to £3,000 from April 2024, falling from a high of £12,300 in 2022/23 tax year.

For those crossing into the additional rate tax band (which was lowered from £150,000 to £125,140 in 2023/24) these allowances are cut even more sharply. In the case of savings interest, the Personal Savings Allowance is removed entirely.

Rising Tax bills for savers and investors

Stealth taxation is not just affecting pensioners. The Personal Savings Allowance has remained unchanged since it was introduced in 2016. For years, with ultra-low interest rates, this wasn't a major issue. But the tide has turned.

With the Bank of England increasing interest rates to tackle inflation, savings accounts are now generating more interest and more tax. In the 2022/23 tax year, 1.77 million people paid tax on their savings interest, up from just 970,000 the year before. HMRC reports that the amount raised from this alone more than doubled from £1.2 billion to £3.4 billion.

In the 2023/24 tax year, an estimated 1.9 million people paid tax on their savings interest, up from 1.77 million the year before and just 970,000 in 2021/22. According to HMRC the amount raised from tax on savings interest surged to a record £9.1 billion, more than double the £3.4 billion collected in 2022/23, and over seven times the £1.2 billion from 2021/22. Projections for 2024/25 suggest that over 2 million savers will pay tax on interest, with HMRC expecting to collect £10.4 billion.

A Growing Inheritance Tax catch

Another stealth tax that continues to ensnare more households is Inheritance Tax (IHT). The nil-rate band for IHT has been frozen at £325,000 since 2009. Over this time, property and asset values have risen dramatically. As a result, more estates now breach the threshold and face IHT liabilities. Although, in 2017 the Residence Nil Rate Band was introduced which permitted individuals, passing down their main residence to direct descendants, an additional allowance of up to £175,000. Meaning, for married couples/ civil partnerships up to £1million could be passed down free of IHT. However, those estates of over £2 million would be subject to tapering. You can read more about this here.

In 2024/25, IHT receipts hit a record £8.2 billion. With the freeze extended until at least 2030 and no indication of major reform, families are increasingly vulnerable to unexpected tax bills, even those with relatively modest estates.

What can be done? The case for proactive planning

While stealth taxes are largely outside of our control, their impact doesn’t have to be. With careful planning, it’s possible to reduce unnecessary tax exposure and protect long-term wealth. Strategies may include:

- Making full use of ISAs for tax-free savings and investments

- Structuring pension drawdowns to minimise tax liabilities

- Gifting assets in a tax-efficient manner to reduce IHT exposure

- Reviewing income regularly to avoid crossing thresholds unnecessarily

- Increasing pension contributions to lower taxable income through salary sacrifice.

Each individual’s situation is different, and the tax system is becoming increasingly complex. For many, professional advice can help clarify their position and create a clear, forward-looking financial strategy.

60% tax trap

For those earning between £100,000 and £125,140, the tax system becomes especially punitive. In this income band, individuals lose £1 of their tax-free personal allowance for every £2 earned above £100,000, effectively creating a 60% marginal tax rate. This stealthy threshold has increasingly drawn in middle- and upper-middle earners, particularly as it hasn’t been adjusted for inflation since 2010. Despite rising wages and fiscal drag, the government has so far resisted reform, leaving many professionals facing disproportionately high tax bills.

Staying ahead in a shifting tax landscape

As the government continues to rely on threshold freezes to raise revenue without increasing tax rates, more households, particularly pensioners, will feel the squeeze. These are not sudden shocks, but slow, creeping changes that can significantly erode financial wellbeing over time.

Understanding the full picture and taking early, informed action is key. Whether you are drawing a pension, managing savings, or planning your estate, speaking with a qualified financial adviser can help you navigate the challenges ahead and ensure your finances remain aligned with your goals.

If you’re concerned about an increasing tax burden on your wealth why not get in touch and speak to one of our financial advisers to see how we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

The information in this article is based on current laws and regulations which are subject to change as at future legislations.

A pension is a long-term investment. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested.

Markets reaction to US strike on Iran nuclear capability

Over the weekend, President Trump ordered the US military to carry out airstrikes on three of Iran’s key nuclear enrichment facilities — Fordow, Natanz and Isfahan — marking a stark departure from his longstanding anti-war posture.

Under the guise of a two week window of negotiation, Trump claimed that Operation Midnight Hammer “completely obliterated” these facilities, and that the move was necessary to halt Iran’s potential nuclear weapon development, despite assessments from international watchdogs and U.S. intelligence that Iran had not yet committed to making a bomb. He warned Tehran that any retaliation would invite even harsher strikes.

Iran condemned the attacks as an “outrageous” with Iran’s foreign mister, Abbas Araghchi declaring that “Iran reserves all options to defend its sovereignty, interest, and people,” While there have been no immediate signs of radiation leaks, Iran’s leadership has vowed to defend the country by all means and may exit the Nuclear Non-Proliferation Treaty, which would further reduce transparency about its atomic activities.

What we are watching for

The reaction of Iran to this attack will dictate whether this is an isolated incident or another chapter in the tumultuous history of western powers and middle east relations.

One key area of focus will be on the Strait of Hormuz, that runs between the Persian Gulf and the Gulf of Oman. About a fifth of the world’s oil runs through this narrow body of water, and so any disruption would cause a spike in oil price, which would impact consumer spending and fuel inflationary pressures.

Its parliament has voted to block the Strait, but such a move would be unprecedented and cannot proceed without the approval of Supreme Leader Ayatollah Ali Khamenei. It should also be noted that Iran cannot legally block the strait under international law, so this would have to be achieved by force or threat of force.

At this stage, it benefits lower-ranking Iranian officials to talk about closing the Strait of Hormuz, given Iran’s reliance on oil revenues. But actually doing so would be economically crippling. Over 90% of Iran’s oil exports go to China, a key ally, so a closure would hurt Iran more than the U.S. and risk straining ties with Beijing.

Further escalation could also come from the US or Israel targeting Iran’s strategically important oil exportation facilities at Kharg Island, which handles ninety percent of Iranian crude oil exports. This would be contrary to the stated aims of the current military action, which has focussed on nuclear proliferation.

Markets

The market reaction has been somewhat muted so far.

Oil futures initially spiked to $81 a barrel but have since pulled back. While the market appears to be pricing in higher prices in the short term, the long-term outlook has not significantly changed, as reflected in the futures curve. The dollar also rose on the geopolitical instability, having been weak for much of the year.

In equity markets we have seen a modest softening with Asian equities down overnight, Europe opened down slightly while the FTSE 100 - reflecting the significance of the energy sector in the index - was up as oil majors such as BP and Shell were positive on the market open. During the course of the morning, markets have firmed up somewhat and are close to flat in sterling terms.

Conclusion

The conclusion one can take now is that the market is pricing in ‘one and done’. The situation is still very dynamic though and what this period shows is the role and significance of geopolitics.

Global uncertainty has been a feature of markets over the last year and whilst attention has turned from trade wars to military wars the result is the same: heightened volatility. However, history teaches that very often, geopolitical conflict often does not lead to protracted equity market weakness.

During these periods an investors best course of action is to look beyond the noise and assess the fundamentals of the market. This job – whilst potentially an uncomfortable experience - is made much easier if one’s portfolio is diversified and not positioned for a singular outcome.

If there’s anything you are concerned about and would like to speak to a financial adviser, please get in touch.

Arrange a free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.