Skip to main content

Skip to main content

Maduro and Greenland fail to rain on markets' parade

Despite high-profile geopolitical events and headline risk, global markets started 2026 on a resilient footing, supported by solid economic fundamentals and growth momentum.

The themes that dominated markets last year have carried into the new year, dispelling any expectation that 2026 would be ‘quieter'. The US’s audacious extradition of Nicolás Maduro from Venezuela and President Trump’s announcement to pursue the acquisition of Greenland have reinforced this dynamic.

Arrange your free initial consultation

Once again, we see a clear divergence between the prevailing narrative ‘the noise’ and what is happening in financial markets. Despite these headline grabbing risks, which ultimately proved to be temporary flashpoints, global equity markets were buoyed by stronger growth expectations and a macroeconomic backdrop that remains broadly supportive. In this environment, economic resilience has helped offset lingering inflation concerns.

Equities

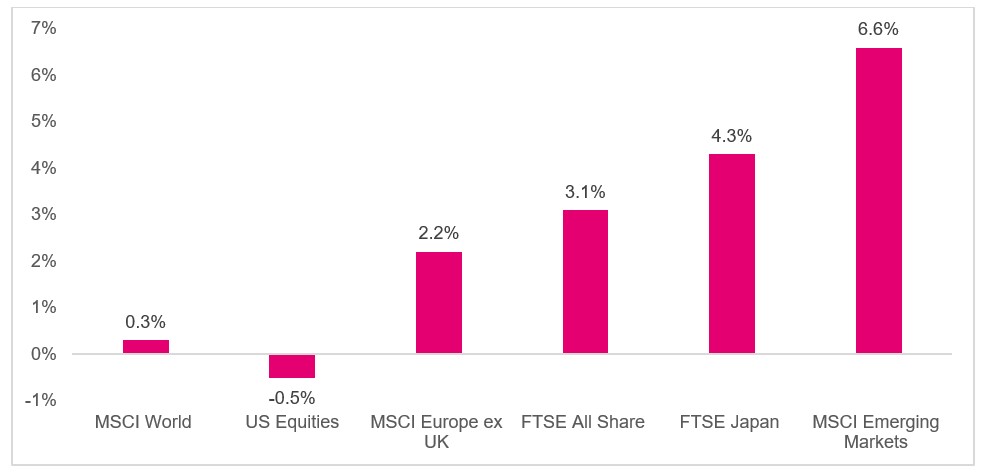

Figure 1. Equity market returns (January 2026, Source: Pacific Asset Management)

Equity markets were broadly positive across regions, although US equities lagged as technology stocks came under pressure. Microsoft notably fell 10% in a single day, highlighting growing investor caution over elevated valuations and increasing scepticism regarding the scale of spending on AI and related projects.

US policy uncertainty increased with the nomination of Kevin Warsh as the next Federal Reserve Chair, set to succeed Jerome Powell in May. Front-runner Kevin Hassett was ultimately passed over, partly due to concerns over his perceived political alignment amid scrutiny of Fed independence. Warsh’s appointment was broadly welcomed, but questions remain given his past reputation during his previous tenure at the Federal Reserve as an inflation hawk - prioritising price stability - and how this will align with President Trump’s preference for lower interest rates, leaving markets watching closely how his approach will unfold.

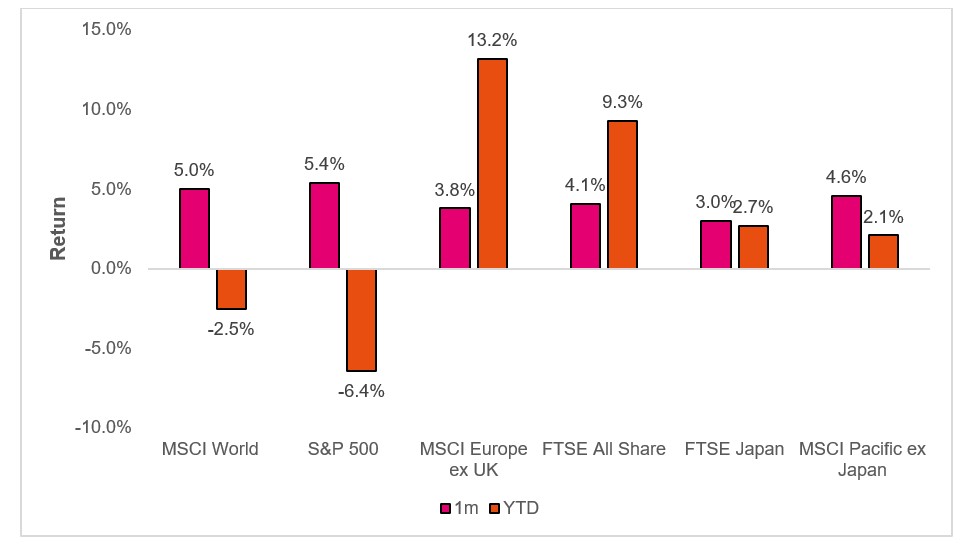

European equities ended the period higher, despite earlier pressure from President Trump’s threat to impose tariffs on European countries over Greenland. Sentiment improved as tensions eased, supported by stronger-than-expected Q4 2025 GDP growth of 0.3% and a near record-low unemployment rate of 6.2% in December.

In the UK, the FTSE 100 surpassed 10,000 points for the first time since its launch in 1984, led by basic materials benefiting from higher metal prices. Domestically focused companies maintained positive momentum, with mid-cap stocks outperforming large caps. Inflation rose to 3.4%, the first increase in five months, leaving the UK with the unenviable record of the highest inflation in the G7. Markets continue to view this as largely transitory, driven by factors such as higher airfare over the Christmas period, and expect inflation to gradually return toward the 2% target.

In Japan, equities continued to rise following the announcement of a snap lower house election on 8 February, called by Prime Minister Sanae Takaichi to strengthen her mandate and support her agenda of easier monetary policy and targeted fiscal stimulus.

Fixed income

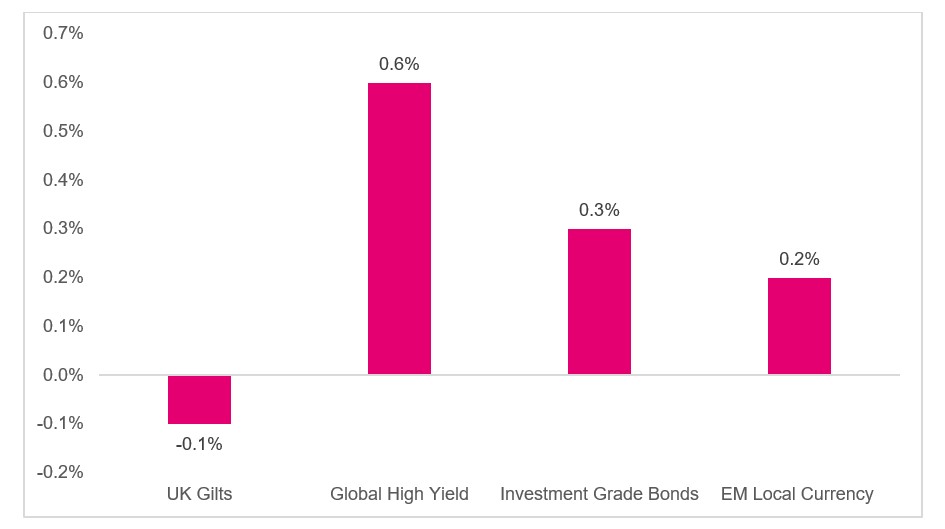

Government bond markets came under pressure as stronger-than-expected economic growth and concerns over elevated public spending dampened expectations for near-term policy easing, pushing yields higher. US Treasuries fell, especially at the short end of the curve, as robust data delayed anticipated Federal Reserve rate cuts. UK gilts also declined, with December inflation coming in above expectations, reducing the likelihood of further easing from the Bank of England. European government bonds were relatively resilient, led by France and Italy, supported by improved risk sentiment across core and peripheral markets. In Japan, government bonds faced significant pressure, recording a particularly challenging start to the year as yields adjusted to evolving domestic policy expectations.

Figure 2. Fixed Income returns (January 2026, Source: Pacific Asset Management)

Figure 2. Fixed Income returns (January 2026, Source: Pacific Asset Management)

Commodities

Commodity markets extended their positive momentum early in the year, underpinned by strong gains in precious metals and oil. Gold performed well through most of the month, buoyed by sustained central bank buying particularly from emerging-market reserve managers and heightened geopolitical tensions that supported safe-haven demand. However, the metal sold off late in the period as speculative positioning shifted and investors took profits from earlier strength. Brent crude oil also advanced, holding near multi month highs as ongoing supply risk concerns continued to provide support to energy prices.

Portfolio implications

The start of the year has reinforced the case for international diversification, with opportunities increasingly emerging outside the US. Uncertainty is likely to continue - the classic ‘known unknown’ - requiring investors to remain proactive and adaptable in navigating the evolving market landscape.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 13/02/2026.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

Faithful markets defy traitor headlines

2025 will be remembered as a year in which uncertainty and strong investment performance were not mutually exclusive. For the first time since 2019, global equities, bonds and commodities all delivered positive returns, supported by AI-driven investment themes, central bank easing and eventually falling tariffs.

This headline performance, however, understates the challenges investors faced over the year. Policy and trade uncertainty dominated the news flow early on, with U.S. equities falling more than 20% in sterling terms as markets grappled with the implications of global tariff rates reaching levels not seen since the 1930s. At the same time, government balance sheets came under increased scrutiny amid fiscal largesse, while a shifting world order heightened geopolitical risks.

Arrange your free initial consultation

Equity markets

Equities reached new highs, but unlike much of the past decade, leadership did not come from the United States. Instead, investors were rewarded for adopting a more global approach, as market performance broadened beyond U.S. mega-caps into more attractively valued regions. Structural themes such as artificial intelligence and clean energy also gained traction across a wider range of geographies, reinforcing the shift toward more diversified sources of return.

European equities

European equities led global markets, delivering returns of over 26% in sterling terms. Performance was supported by a combination of attractive valuations and improving investor sentiment, as falling inflation enabled the European Central Bank to cut EU interest rate to 2%. In addition, a renewed commitment to fiscal expansion - most notably in Germany, which announced plans to allocate €500 billion to infrastructure and adopted a “whatever it takes” approach to defence spending - provided a further boost to the region.

UK equities

Outside Europe, UK equities also delivered strong results, recording their fifth-best annual return since 1984. Performance was underpinned by renewed investor interest in lower-valued markets, as well as the index’s structural bias toward defensive sectors, which performed particularly well over the year.

Emerging markets

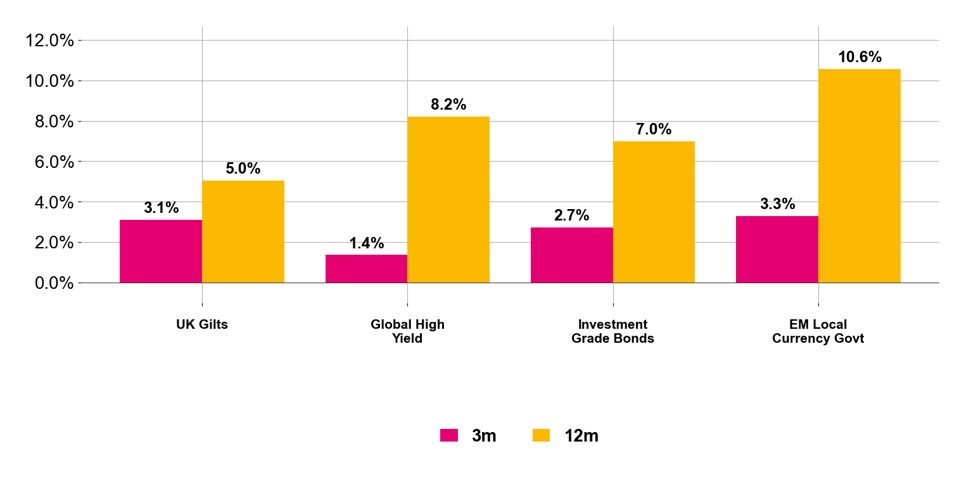

Emerging markets, meanwhile, challenged the notion that the United States is the sole driver of equity returns. A rally in technology companies outside the U.S. supported a broader advance across emerging market equities, with particularly strong performances in China, Taiwan, and South Korea. Combined with a weakening U.S. dollar and that many emerging economies carry lower debt levels and are growing faster than their developed-market peers, the outlook for the asset class remains constructive. Figure 1: 3 and 12 month equity returns (Source: Pacific Asset Management, January 2026)

Figure 1: 3 and 12 month equity returns (Source: Pacific Asset Management, January 2026)

Fixed income

In fixed income, declining inflation and the gradual easing of monetary policy supported bond markets overall.

Interest rates fell in the UK and Europe as the Bank of England and the ECB reduced rates to their lowest levels since 2023. Meanwhile, after holding steady for much of the year, the Federal Reserve resumed its rate-cutting cycle, delivering reductions in September. This contributed to a decline in short-term rates. However, fiscal concerns continued to weigh on government bonds, leading to a steepening of yield curves across major markets as long-term yields rose, which could have implications for future borrowing costs.

Corporate bond spreads - the premium investors receive for holding credit risk - recovered from the widening seen in April. For much of the year, spreads narrowed amid a risk-on environment, which saw higher prices for both investment-grade and high-yield bonds.

Figure 2: 3 and 12 month fixed income returns (Source: Pacific Asset Management, January 2026)

Gold

Gold surged to its strongest performance in half a century, reflecting investors concerns provoked by fiscal profligacy among Western governments, political uncertainty, and a weaker U.S. dollar. The safe-haven metal broke multiple records over the year, reaching $4,482 per ounce in December. Looking ahead, we expect gold prices to remain supported by ongoing central bank purchases and elevated fiscal deficits.

Outlook

Continued global growth and resilient consumer demand underpin a constructive outlook for equities. However, valuations remain high in concentrated markets, and investors are increasingly cautious about the risks associated with AI-driven themes.

This environment presents opportunities as markets broaden, with previously overlooked areas likely to benefit. Thoughtful portfolio construction and rigorous risk management will be critical as emerging opportunities - and potential risks - come into focus over the year.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 16/01/2026.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

2025 – Pensions under pressure as stealth taxes persist

The first Budget of my professional career was the 1988 Nigel Lawson “Giveaway” Budget. As an office junior, my job was to head into the city and queue up (with dozens of other fresh faced office juniors) to receive the printed full Budget from the Government’s press offices. I dutifully returned to work, clutching it in my sweaty palms, so that the senior advisers could pore over it. No internet, no leaks, just a bundle of white pages hastily stapled together.

Arrange your free initial consultation

Since that March day (it always used to be in the Spring) Budgets have come and gone but they all have one thing in common. Namely, the fear and rumour that ferments in the days and weeks beforehand. I have to say that the media are one of the major guilty parties and, more than ever, are responsible for whipping up a frenzy of bitterness and resentment, even before the Chancellor, whoever they happen to be, has stepped up to the dispatch box.

I don’t think I’m wrong in saying that I’ve never witnessed quite so much ‘bracing’ in fear and anticipation as this Budget. The nation became paralysed in apocalyptic fear as if the end of the world were approaching.

So, I thought it was time to take stock and look at the Budget in the clear light of day and also in the context of historical Budgets.

The fear and rumour mill

Ever since that dreary March day in 1988, I can say that one fear has pervaded every single Budget. Namely, the fear that higher rate tax relief will be removed from pension contributions. This Budget was, of course, no exception and the fear spread even further than that. About sometime in September this year, a rumour started (I don’t know from where) that tax free cash (now technically known as the Pension Commencement Lump Sum, or PCLS) would be reduced from £268,275 to £40,000. Personally, I thought it was unlikely and wasn’t afraid to say so. Not only would it not result in higher tax take for the Treasury (who in their right mind would now willingly withdraw £286,275, subjecting themselves to income tax on £246,275?) but it would also have made Rachel and Labour, even more unpopular than they are already.

Nevertheless, a huge number of people acted and withdrew their tax free cash and are now sitting on it in a taxable environment.

But pensions were definitely going to take a bullet somehow. After all, they are still highly efficient methods of saving, something which seems to have been lost on some of the general public, based on a tsunami of negative press, again, which doesn’t always help. Animal Farm springs to mind when the animals, having taking over the farm, come up with the tenets of animal life. “Four legs good, two legs bad”. And so, the media has a similar chant “non pensions good, pensions bad”. But are they? If I were to tell you that you could invest in a pension and get 41.6% tax free cash from it, would you be interested? If you are a higher rate taxpayer, this is exactly what you get! For every £100 put in, you only pay £60 (20% tax relief at source and a further 20% back in your tax returns). So, tax free cash at 25% means 25% of £60 which equals 41.6%. When you retire, if you’re a basic rate taxpayer, you are only paying 20% on the £75 whenever you draw on it. By the way, if you make pension contributions and your earnings are between £100,000 and £125,140, because this income reduces your personal allowance, the equivalent tax relief is not 40%, it is 60% so the effective tax free cash rate is a whopping 62.5%.

Given how generous tax relief is, I think that the slight knock pensions took (future reductions in salary sacrifice) is really getting away with it.

The hammer blow came last year

Of course, last year’s Budget delivered a hammerblow to pensions in that, from April 2027, Inheritance Tax (IHT) will apply. For ten years, since George Osborne announced pensions ‘freedom’ many have earmarked their pension funds for Estate Planning purposes, since so this recent news was very unwelcome. In effect, this now puts pensions in roughly the same position as they were before 2015. Before 1995, remember, people were forced to buy annuities with their pension funds so, in spite of goal post moving, pensions are still the best tax planning vehicles around, so let’s not throw the baby out with the bath water.

Overall, it has to be said that the Budget was probably a slight relief. Many, myself included, had expected increases in Capital Gains Tax and even Income Tax and none of these came to pass. Instead, we saw a continued freezing of allowances. Stealth taxes. The death of wealth by a thousand cuts. Each one painless, but in five years’ time, we’re all significantly worse off without immediately feeling the pain.

Stealth taxes are at the heart of the Budget

There were a few other ‘tampering's’ such as the reduction in cash ISA contributions from £20,000 to £12,000 for under 65s, and an increase to the tax rate on savings interest, both from April 2027, but this is mostly tinkering around the edges and irritants for some, at worst. There was an innovation in the introduction of ‘Mansion tax’ for houses worth over £2m but, again, this was kicked into the future and will not apply until 2028. But the stealth taxes, freezing of allowances, are at the heart of this budget.

I sometimes think of the 1988 “giveaway” Budget with fondness. Lawson reduced higher rate income tax from 60% to 40% and basic rate from 27% to 25%. All of this was possible due to the fact that the economy had been overheating (remember that?) but was now under control and the predicted Budget surplus allowed for such cuts. What luxury! There was uproar in the house and the Speaker had to suspend proceedings due to “grave disorder”. A lesser known MP called Alex Salmond exclaimed that it was an “obscenity” and was duly suspended for breaching Parliamentary convention.

The world has changed though, and the UK doesn’t have the room for manoeuvre afforded by those halcyon days. Nigel Lawson didn’t have the fallout of QE, Brexit, Covid and the Ukraine invasion to hamper him and I doubt if any modern day Chancellor from any persuasion would make us all happy, given the state of the economy. The only one who tried, and failed, was Kwasi Kwarteng who, in cahoots with Liz Truss, grabbed the Treasury money bag and started running down Whitehall throwing £20 notes in the air before being rugby tackled by the bond markets. I sadly, don’t expect too much from any Chancellor, from whichever party, over the next few years at least.

On the plus side, bond markets (the ultimate bellwether of economic prudence) have reacted well to the Budget. Gone are the days when a Labour Government would react to fiscal shortfall by applying for a payday loan!

So, in the final analysis, maybe the 2025 Budget was a bit of a non-event. But fear and loathing were the lasting memories of the days leading up to it, which probably explains why the UK economy reported a contraction in October. Meanwhile, back at Animal Farm, I’d like to paraphrase another animal tenet. “All Budgets are equal, but some are more equal than others”.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

Diversification - the name of the game for 2026

Global markets were a mixed bag in November, pausing after several months of strong gains. Volatility increased, as concerns over stretched AI-related and technology stocks resurfaced, prompting a switch towards defensive sectors such as healthcare and consumer staples. The technology sector was challenged, recording its biggest decline since March 2025.

Arrange your free initial consultation

Figure 1. Regional equity returns (Source: Pacific Asset Management, November 2025)

US Markets

US equities remained largely unchanged as investors looked past the positives of strong Q3 earnings and the end of the 43-day government shutdown - the longest in US history - and instead focused on uncertainty around interest rates and concerns around an AI-driven bubble. Volatility was driven primarily by the shifting expectations around Federal Reserve policy. The probability of a December rate cut swung sharply, falling from nearly 98% in late October to about 40% by mid-November, before rebounding above 80% by the end of November. Market movements reflected not only the potential timing of rate cuts, but also investor interpretations of the Fed’s economic outlook and the likelihood of a ‘soft landing’.

European Markets

Across the Atlantic, Eurozone inflation in November ticked up to 2.2% from 2.1%, slightly above forecasts and suggesting that price pressures remain. Economic expansion was modest, with Q3 growth at 0.2% and unemployment steady at 6.4%. The European Central Bank (ECB) indicated a cautious stance, signalling that keeping interest rates unchanged remains the prudent course. European equities remained relatively flat as investors navigated these mixed economic indicators.

Japan Markets

In Japan, headline inflation climbed to 3.0% in October - the highest since July - driven by energy costs, currency fluctuations, and ongoing supply chain strains. A softer yen provided support to export-focused equities but also contributed to higher inflation, while government bonds underperformed as yields rose amid doubts over the long-term sustainability of fiscal and monetary support.

UK Markets

The UK’s Autumn Budget 2025, long anticipated and partially pre-empted by the early Office for Budget Responsibility (OBR) publication, had a relatively muted immediate impact on markets.

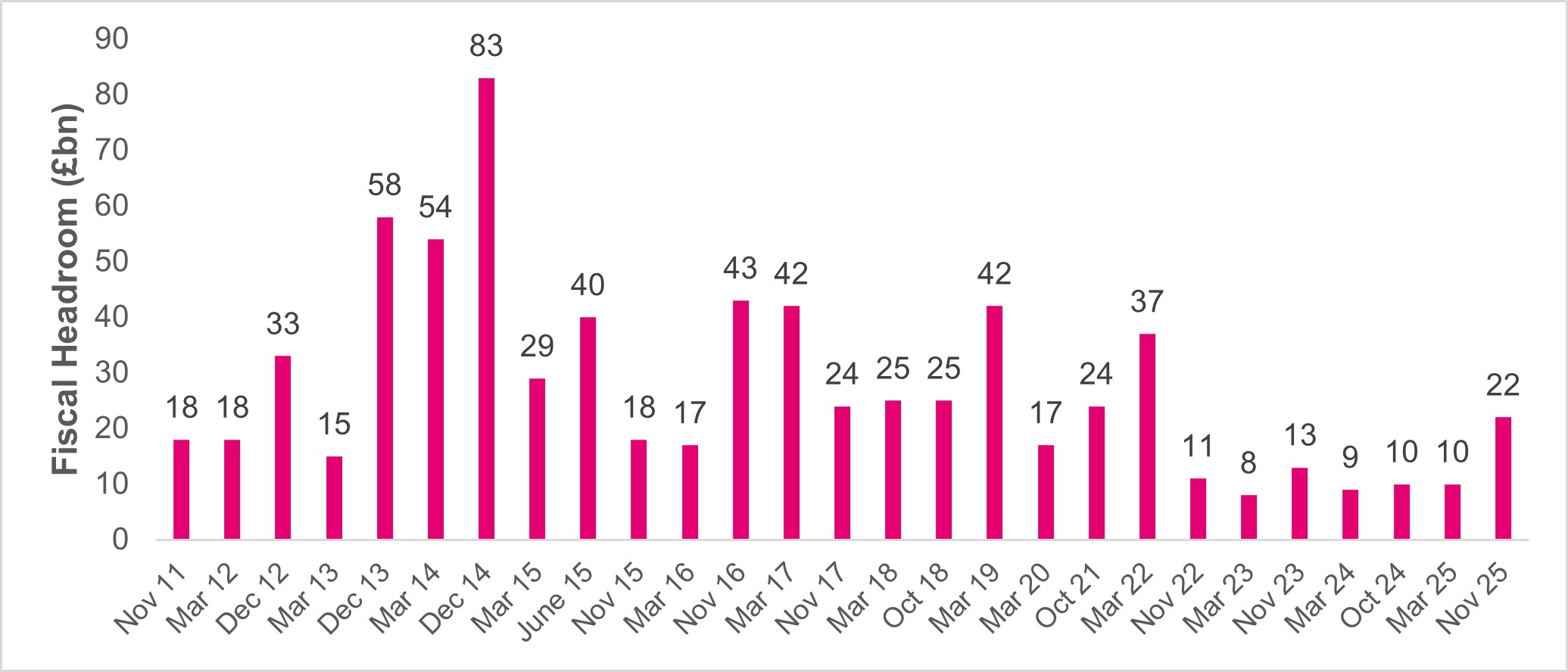

The Chancellor outlined £26 billion in tax measures; however, with many provisions deferred over several years - some beyond the next general election - the near-term fiscal landscape remains largely unchanged. Fiscal flexibility is set to improve, with the Chancellor projecting a buffer of approximately £22 billion - more than double last year’s level - which had been largely eroded and fueled months of speculation over potential tax increases. While this represents a meaningful increase in fiscal headroom, it remains below average, with the typical revision to an OBR forecast over six months around £21 billion, leaving little room for error (see Figure 2.).

Figure 2. Forecast headroom against fiscal room (Source: Pacific Asset Management, IfG, November 2025).

Markets responded positively to the extra fiscal headroom and the reduced risk of near-term borrowing pressures or unexpected tax adjustments. UK government bonds delivered one of their strongest Budget-day performances in twenty years, reflecting renewed confidence in the fiscal outlook. Meanwhile, equity markets, which had softened amid pre-budget leaks and speculation, stabilized as investors assessed the measures as supportive of macroeconomic stability without introducing major new uncertainties.

Commodities and Gold

Away from equities, commodities posted modest gains in November, with performance varying across sectors. Gold emerged as the standout performer, supported by sustained investor demand for safe-haven assets amid ongoing macroeconomic uncertainty, including inflationary pressures, central bank policies, and geopolitical risks.

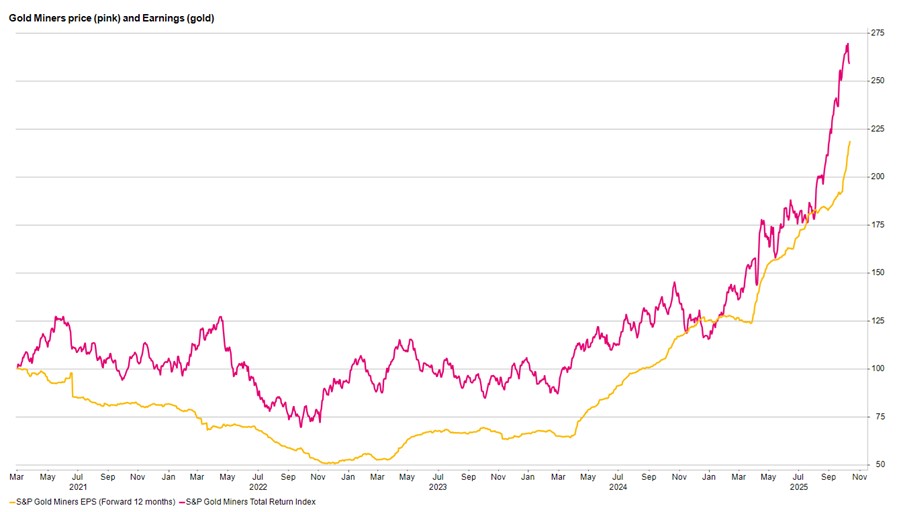

While November’s advance was more measured than recent rallies - partly due to profit-taking - the metal’s underlying fundamentals remain strong. Structural demand, constrained supply, and its role as a portfolio diversifier continue to underpin gold’s outlook into 2026. Gold mining companies also continue to benefit from elevated gold prices and more disciplined capital management, with earnings growth reflecting these favourable conditions (see Figure 3.).

Figure 3: Goldmining companies return and earnings profile (Source: Pacific Asset Management, November 2025).

Summary

Despite some volatility in November, global equities are positioned to deliver another strong year in 2025. Equity markets in the UK, Europe, and Japan have all shown relative outperformance compared with the US, underscoring the value of international diversification. Moreover, the recent underperformance of technology stocks highlights the importance of sector diversification - not only as a risk management tool but also as a potential source of returns.

Looking back over November, there were no major shifts in economic fundamentals. Instead, market movements reflected changes in sentiment, emphasizing how investor perceptions and expectations can drive short-term volatility - even in the absence of significant economic or market developments. This serves as a reminder that as we move into the next year, investors will continue to face sentiment-driven risks alongside structural considerations, including central bank policy, inflation dynamics, and sector-specific trends.

Overall, the performance of global equities this year reinforces the importance of maintaining a diversified investment approach that balances geographic exposure, sector allocation, and risk management strategies.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 12/12/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

Autumn Budget 2025: What changed and what to plan for

Chancellor Rachel Reeves gave her second Budget speech on 26 November 2025. After much worry and speculation, there were thankfully no changes announced to the rules around pension tax relief and tax-free cash (pension commencement lump sums). However, there are going to be changes to the salary sacrifice rules for pension contributions - from April 2029, only the first £2,000 per annum of sacrificed salary will be exempt from employer and employee National Insurance (NI).

Arrange your free initial consultation

Other announcements included an increase in the rates of income tax on dividends, property and savings income by 2 percentage points (some changes from April 2026 and some from April 2027) and a freezing of the income tax bands in England, Wales and Northern Ireland for a further three tax years until April 2031.

From April 2027, changes will be made to the ISA allowance so that only the over 65s will be able to place the full £20,000 into Cash ISAs (capped at £12,000 into Cash ISAs for the under 65s).

TPO Partner, David Dodgson, appeared on BBC Money Box Live on budget day, sharing his thoughts on the Chancellor's statement.

We have summarised the main points of the Budget below, along with a reminder of various changes from April 2026 that we were already aware of. Further guidance will be published as necessary and as more detail becomes available.

Pensions

Salary sacrifice

From April 2029, anyone sacrificing more than £2,000 per tax year for employer pension contributions won’t save NI on the excess. Employers will also pay NI on any excess.

Such contributions still receive income tax relief as they would if made via a different method such as relief at source.

State pension

The triple lock means the new state pension and basic state pension are expected to increase by 4.8% in April 2026. This will mean a full new state pension figure of £241.30 per week and a full basic state pension of £184.90 per week. The government has committed to maintaining the triple lock for the duration of this Parliament.

Restrictions will be introduced on the making of Class 2 voluntary NI (VNICs) to achieve state pension for those living overseas by increasing the initial residency or contributions requirement for VNICs to 10 years. The government is also launching a wider review of VNICs, with a call for evidence to be published in the new year.

Changes will be made from 2027 to avoid those whose sole income is the state pension having to pay small amounts of income tax through Simple Assessment (which will become increasingly likely as the state pension increases, and the personal allowance remains frozen).

Pension Protection Fund / Financial Assistance Scheme

The government will introduce payment of inflation increases on pre-97 pensions to PPF and Financial Assistance Scheme (FAS) members of up to 2.5 per cent. This would apply to those members whose original schemes provided for indexation on pre-97 pensions. The move would broadly align pre-97 indexation rules with those already in place for post-97 pensions for PPF and FAS members.

Investments

Individual Savings Accounts (ISAs)

From April 2027, changes will be made to the ISA allowance so that only the over 65s will be able to place the full £20,000 into Cash ISAs. Those under 65 are capped at £12,000 into Cash ISAs with the balance having to be placed in other ISA types if they wish to make use of the full allowance.

The annual subscription limits all remain at their current levels in 2026/27, i.e.

- £20,000 ISA

- £4,000 Lifetime ISA

- £9,000 Junior ISA (and Child Trust Fund)

Lifetime ISA

Consultation to take place early next year on replacing the Lifetime ISA (LISA) with a new product for first-time buyers.

Enterprise Investment Scheme and Venture Capital Trust

Changes to be introduced in Finance Bill 2025-26 to take effect from 6 April 2026:

- The Income Tax relief that can be claimed by an individual investing in Venture Capital Trust (VCT) to reduce to 20% from the current rate of 30%

- The gross assets requirement that a company must not exceed for the Enterprise Investment Scheme (EIS) and VCT to increase to £30 million (from £15 million) immediately before the issue of the shares or securities, and £35 million (from £16 million) immediately after the issue

- The annual investment limit that companies can raise to increase to £10 million (from £5 million) and for knowledge-intensive companies to £20 million (from £10 million)The company’s lifetime investment limit to increase to £24 million (from £12 million) and for knowledge-intensive companies to £40 million (from £20 million)

The increases to the annual, lifetime and gross asset limits apply only to qualifying companies that are not registered in Northern Ireland trading in goods or the generation, transmission, distribution, supply, wholesale trade or cross-border exchange of electricity. These companies will remain eligible for the current scheme limits.

EIS and VCTs are higher risk investments and they are not suitable for all investors. There is a chance that all of your capital could be at risk and you should not invest into these types of plans without seeking advice.

Enterprise Management Incentive (EMI) scheme

The measure will amend provisions for some of the limits relating to the EMI scheme. For eligible companies, the changes that will apply to EMI contracts granted on or after 6 April 2026 are the limit on:

- Company options will be increased from £3 million to £6 million

- Gross assets will be increased from £30 million to £120 million

- The number of employees will be increased from 250 employees to 500 employees

Taxation

Income tax

Income tax bands in England, Wales and N. Ireland have been frozen for a further three tax years to April 2031 (had already been frozen to April 2028).

All income tax rates and bands remain at their current levels in 2026/27 apart from as outlined below.

Changes to tax rates for property, savings & dividend income

- Tax on dividend income will increase by 2 percentage points. The ordinary rate will rise from 8.75% to 10.75%, and the upper rate from 33.75% to 35.75% from April 2026. The additional rate will remain unchanged at 39.35%. The £500 dividend allowance remains in place.

- Tax on savings income will increase by 2 percentage points across all bands. The basic rate will rise from 20% to 22%, the higher rate from 40% to 42%, and the additional rate from 45% to 47% from April 2027. The starting rate band and personal savings allowance remain unchanged.

- The government is creating separate tax rates for property income (any income from letting land and buildings). From April 2027, the property basic rate will be 22%, the property higher rate will be 42% and the property additional rate will be 47%. Finance cost relief will be provided at the separate property basic rate (22%). The £1,000 property allowance and Rent a Room Scheme remain in place.

The way individuals report and pay tax on property, savings and dividend income will remain the same – it is only the rates of tax charged that will change. The income tax ordering rules will be changed from April 2027 so that the Personal Allowance will be deducted against employment, trading or pension income first.

The changes to property income rates will apply in England, Wales and Northern Ireland. The government will engage with the devolved governments of Scotland and Wales to provide them with the ability to set property income rates in line with their current income tax powers in their fiscal frameworks. The changes to dividend and savings income rates will apply UK-wide as these rates are reserved.

Tax and NI thresholds

- No increases to the headline rates of income tax (see above regarding future rates for savings/dividend/property income), National Insurance contributions (NICs) or VAT

- Income tax thresholds and the equivalent NICs thresholds for employees and self-employed frozen at current levels for a further three years from April 2028 to April 2031

- NI Secondary Threshold frozen at its current level from April 2028 to April 2031

- Plan 2 student loan repayment threshold will be frozen at its 2026/27 level for three years from April 2027

National Living Wage

National Living Wage will increase by 4.1% to £12.71 per hour for eligible workers aged 21 and over.

Capital gains tax

The annual exemption remains at £3,000 (a maximum of £1,500 for discretionary/interest in possession trusts – shared between all settlor’s trusts subject to a minimum of £300 per trust).

CGT rates remain as they currently are:

- 18% for any taxable gain that doesn’t fall above the basic rate band when added to income and 24% on any gain (or part of gain) that falls above the basic rate band when added to income

- Unused personal allowance can’t be used for capital gains

- Discretionary/interest in possession trustees and personal representatives pay at the higher rates (24%)

Inheritance tax

In an improvement to the Business and Agricultural Relief changes from next April, the £1 million limit on 100% Business and Agricultural Relief will be transferable between spouses if unused on first death (including where first death was before 6 April 2026).

Capping inheritance tax trust charges for former non-UK domicile residents - this measure introduces a cap on relevant property inheritance tax charges for trusts which held excluded property at 30 October 2024. The relevant property charges are capped at £5 million over each 10 year cycle.

Anti-avoidance measures for non-long-term UK residents and trusts - this measure will look-through non-UK companies or similar bodies to treat UK agricultural land and buildings as situated in the UK for inheritance tax purposes. It also provides that where a settlor ceases to be a long-term UK resident, there will be an Inheritance Tax charge if there is a later change in situs of their trust assets.

Also, Inheritance Tax charity exemption will be restricted to gifts made directly to UK charities and registered clubs and excluded from gifts to trusts which are not registered as UK charities or clubs.

IHT thresholds to be fixed at their current levels for one further tax year to April 2031, as shown below:

- Nil-Rate Band (NRB) at £325,000

- Residence Nil-Rate Band (RNRB) at £175,000

- RNRB taper, starting at £2 million

- combined £1 million allowance for 100% APR and Business Property Relief (BPR) relief

Previously announced changes:

The government is implementing previously announced reforms to taxes on wealth and assets including:

- From 6 April 2026, the CGT rate for Business Asset Disposal Relief and Investors’ Relief will increase to match the main lower rate at 18%

- From 6 April 2026, the government will reform agricultural property relief and business property relief

- From 6 April 2026, the government will introduce a revised tax regime for carried interest which sits wholly within the income tax framework

- From 6 April 2027, the government is removing the opportunity for individuals to use pensions as a vehicle for IHT planning by bringing unspent pots into the scope of IHT

Internationally mobile individuals

The government is to make changes to the way internationally mobile individuals are taxed, closing loopholes and capping relevant property trust charges payable by certain trusts. Further details are to follow.

New mileage tax on electric cars

A new 3p charge per mile on electric cars.

Universal credit

The two-child benefit cap is to be abolished from April 2026.

Employee ownership trusts (EOT)

The 100% relief from capital gains tax on businesses sold to Employee Ownership Trusts will be reduced to 50%.

High value council tax surcharge HVCTS (‘Mansion tax’)

From April 2028, a council tax surcharge will apply to properties worth more than £2m in 2026. This will be £2,500 for properties worth £2m-£2.5m rising in bands to a maximum of £7,500 for homes valued at over £5m. Charges will increase in line with CPI inflation each year from 2029 onwards. Homeowners, rather than occupiers, will be liable to the surcharge and will continue to pay their existing Council Tax alongside the surcharge.

GOV.UK : High Value Council Tax Surcharge

Stamp duty

From 27 November 2025, there is an exemption from the 0.5% Stamp Duty Reserve Tax (SDRT) charge on agreements to transfer securities of a company whose shares are newly listed on a UK regulated market.

The exemption will apply for a 3-year period from the listing of the company’s shares.

Tax Support for Entrepreneurs

A Call for Evidence has been published seeking views on the effectiveness of existing tax incentives, and the wider tax system, for business founders and scaling firms, and how the UK can better support these companies to start, scale and stay in the UK. The Call for Evidence will close on 28 February.

If you’d like to know how the budget may impact your financial plans, why not get in touch and speak to one of our advisers today for a free initial consultation.

Arrange your free initial consultation

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

This article is intended as information only and does not constitute financial advice.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Key changes from Rachel Reeves’ Budget 2025

Rachel Reeves’s long-awaited budget arrived earlier than expected, as it was published by the Office for Budget Responsibility an hour before it was supposed to be delivered in Parliament, leading to unprecedented scenes in the House of Commons.

The key changes were:

-

Frozen tax bandings

Having already been frozen from 2021until 2028, there were rumours of an extension until 2030, but in fact the freeze was extended for three further years to 2031. The impact of this over a decade will be significant as was explored in this recent article from The Times to which The Private Office were pleased to contribute.

-

A 2% increase on Dividend, Savings and Rental Income Tax

Dividend tax rates will increase from 8.75% and 33.75% to 10.75% and 35.75% respectively for basic and higher rate taxpayers with effect from April 2026. Additional rate dividend tax will remain unchanged at 39.35%

Savings and Property income tax will increase from 20%, 40% and 45% to 22%, 42% and 47% for basic, higher and additional rate taxpayers with effect from April 2027.

-

The Cash ISA allowance will be limited to £12,000 with effect from April 2027 for under 65s

This had been widely rumoured, but investors will be pleased to see the Stocks & Shares ISA remaining at £20,000 and for the over 65s they can still use the cash ISA allowance in full.

-

Salary sacrifice on pension contributions

With effect from April 2029, there will be a limit of £2,000 p.a. for pension contributions being paid directly into workers’ pensions, thereby saving national insurance being paid on the income. However, investors will be pleased to see tax relief on pension contributions remaining unchanged.

-

A mansion Tax on homes worth over £2,000,000

This will be set at a rate of £2,500 for homes valued at over £2m, rising to £7,500 for homes valued at over £5m and will come into effect in 2028 .

-

Agricultural and Business Property Relief threshold of £1m can be transferred between spouses if unused on death

This will have been welcomed by Business Owners and Farmers as assets will no longer need to be passed to children on first death to take advantage of the additional Agricultural and Business Property relief, though many may have already changed their Wills to reflect the previous rules so further planning may now be required.

-

Failed pre-1997 pensions that have entered the Pension Protection Fund (PPF)

Individuals will benefit from indexation in a boost for those who lost out when their scheme failed.

-

Infected Blood Compensation Scheme

The government has confirmed that compensation will be relieved from Inheritance Tax. This has caused a great deal of distress over the years to a number of families so this will be a welcome change.

-

Tax relief on Venture Capital Trust (VCT) investments reduced from 30% to 20% from April 2026

The government says this will better balance the amount of upfront tax relief offered compared to EIS investments, where dividend relief is not available.

|

Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. |

|---|

TPO Partner, David Dodgson, appeared on BBC Money Box Live on budget day, sharing his thoughts on the Chancellor's statement.

As well as the above changes, it is important to acknowledge the following areas that did not change despite strong rumours prior to the budget:

- Income Tax rates

- Pension contribution tax relief

- Pension tax free cash

- Capital Gains Tax rates

At the time of writing, Bond markets appear to have digested the budget relatively well, with Gilt rates remaining broadly unchanged.

In summary, after months of speculation, many of the rumoured changes did not materialise, but the combination of further frozen income tax bandings, increases to dividend, saving and property income tax and reduced cash ISA allowances, will make planning more important than ever. Many of the upcoming changes will take effect at different times, so there will be opportunities to limit the impact of the changes through careful planning over the coming years. Pensions remain attractive from a tax relief perspective and Stocks and Shares ISAs remain a tax efficient way of saving.

If you’d like to discuss the impact of the budget on your finances, why not get in touch to speak to one of our advisers. We’re offering everyone with £100,000 in savings, investments or pension a free financial review worth £500.

Arrange your free initial consultation

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

This article is intended as information only and does not constitute financial advice.

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Gold loses some sparkle as global equities continue to shine

Continued enthusiasm around Artificial Intelligence (AI), coupled with news of a trade agreement between the US and China under which the US reduced tariffs and Beijing eased restrictions on rare earth exports, helped drive global equities higher for the second consecutive month in October.

Arrange your free initial consultation

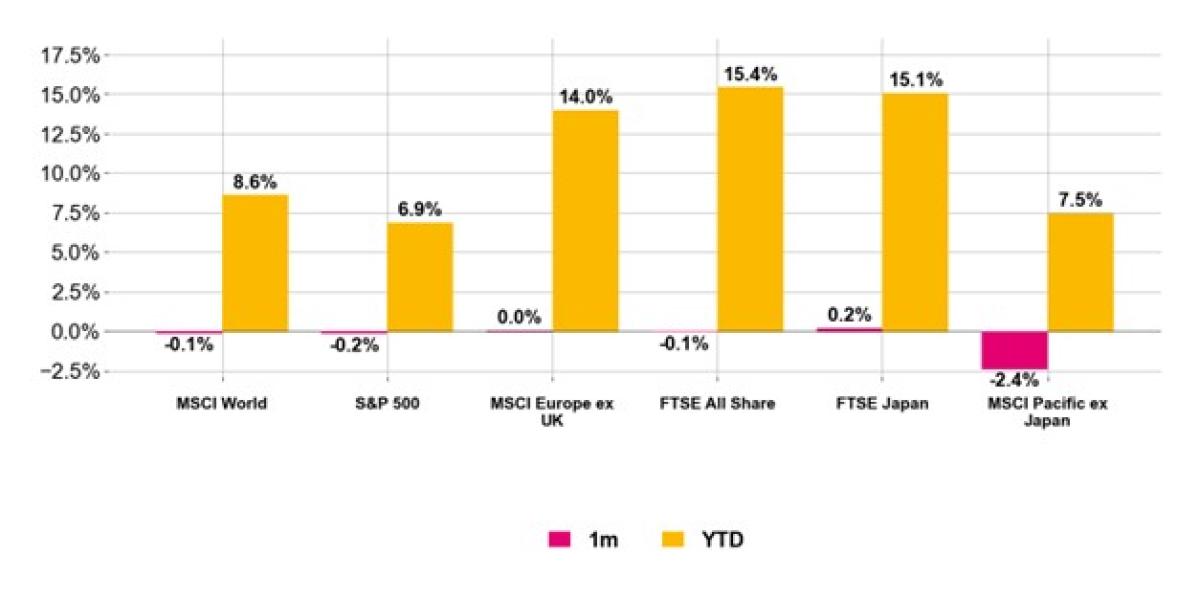

Equity Markets

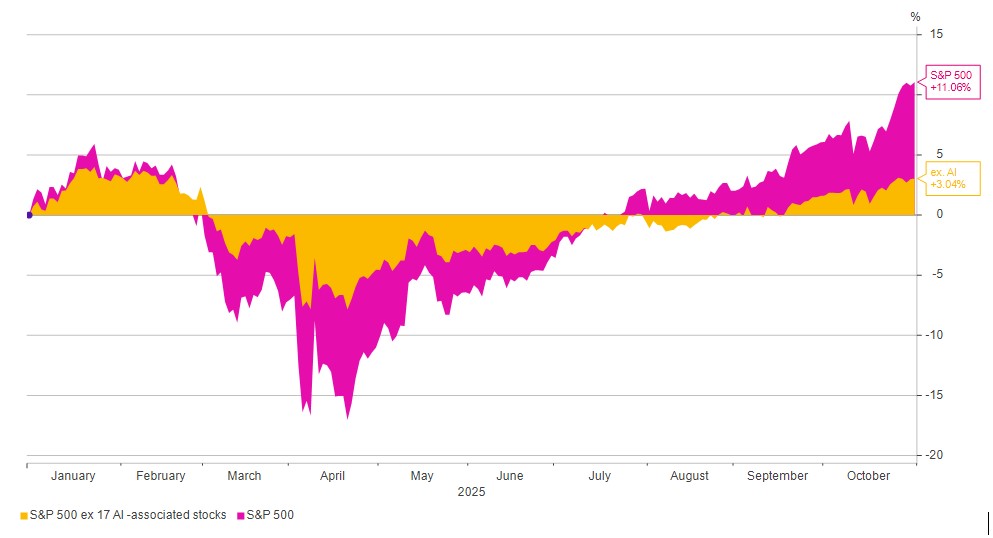

Developed market equities led the gains, with US stocks rising 4.9% in sterling terms as large-cap companies once again outperformed mid-caps. This highlights the growing concentration and dependence on a handful of AI-related companies, with the index up 11% year to date, but a more modest 3% when those firms are excluded (see Figure 1).

Figure 1. US Equities vs US Equity ex AI companies (Source: Pacific Asset Management, October 2025).

Outside the US, Japan was the standout performer, with equities rallying over 5% as the market benefited from enthusiasm around AI and the appointment of Sanae Takaichi - the country’s first female prime minister. Her policy stance, aligned with Abenomics (named after former Japanese Prime Minister, Shinzo Abe), led investors to price in further fiscal expansion and a weaker yen, which supported Japan’s exporters. Meanwhile, UK equities rose 3.7%, aided by a softer sterling that boosted overseas earnings for exporters, whilst commodity and mining stocks advanced on the back of higher commodity prices, particularly in precious metals.

Figure 2. Regional equity returns (Source: Pacific Asset Management, October 2025).

Fixed Income

In fixed income markets, developed market government bonds posted positive returns.

UK gilts led the gains, returning nearly 3% last month, as September’s inflation figure of 3.8% came in below market expectations of 4%, prompting investors to bring forward interest rate cut expectations. This view was further reinforced by speculation around the upcoming Budget, with the UK Treasury expected to raise additional revenue through tax increases, which is likely to weigh on growth prospects and consumer sentiment.

In the US, Treasuries posted positive returns last month, supported by concerns over the government shutdown and the collapse of First Brands and TriColor. The Federal Reserve cut interest rates by 0.25%, bringing rates to their lowest level in three years, which initially boosted the market. However, some of these gains were pared back following Chair Powell’s more hawkish rhetoric, which cast doubt on a December rate cut. The decision also saw duelling dissents for the first time since 2019, with Federal Reserve officials Stephen Miran advocating a further cut and Jeffrey Schmid voting to keep rates unchanged.

Corporate Bonds

Turning to corporate bonds, spreads in both Investment Grade and High Yield bonds widened modestly, but with all-in yields remaining high, returns were still positive. Technical conditions also remain supportive, highlighted by Meta’s $30 bn debt issuance the largest since 2023 which was massively oversubscribed, attracting over $125 bn in investor orders.

Looking ahead, debt issuance from technology companies is expected to pick-up. Morgan Stanley estimates that of the $3tn planned for data centre investment through 2028, roughly half will be financed via debt.

Figure 3. Fixed Income returns (Source: Pacific Asset Management, October 2025).

Commodities

Given the positive backdrop in October, it was unsurprising to see a pullback in gold, with the safe-haven asset falling 7% towards the end of the month, despite climbing above $4,000 per ounce for the first time. For an asset that has risen over 45% year-to-date, a single-digit pullback is within normal expectations. We continue to believe that the factors that drove gold higher - increased uncertainty, a shift away from the dollar, and central bank purchases remain firmly in play.

Gold miners, while leveraged to the gold price, are now much better-run companies than in previous cycles. Improved capital allocation, a controlled cost base, and rising revenues following higher gold prices have strengthened their balance sheets, making them more resilient and better positioned to deliver sustainable shareholder returns even amid short-term volatility in the gold price.

Summary

The theme of AI-driven capital expenditure is expected to continue and accelerate into 2026, keeping investors focused on both the opportunities and the surrounding hype. One debate that is likely to continue is whether the tech-led ‘Magnificent 7’can maintain their ‘magnificent’ status if significant portions of their vast cash reserves are devoted to AI investment, potentially weighing on margins and testing the premium investors have historically been willing to pay.

In this environment, we continue to advise that diversification remains an investor’s best tool not only for risk management, which is crucial, but also to capture opportunities arising from the widening gap between valuations and underlying fundamentals.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 14/11/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.

What to expect from the Autumn Budget 2025

Rachel Reeves will deliver her second budget on 26th November 2025, and with speculation mounting regarding the potential changes, it can be hard to cut through the noise and make good decisions about what action to take, and importantly, not to take.

What is likely to be in the Autumn Budget?

Speculation has been rife about potential changes in a number of areas, so what might these changes look like?

Arrange your free initial consultation

Pensions

As has been the case in previous years, a reduction in individuals’ tax free cash entitlements is rumoured once again to be in the Autumn 2025 budget. These rumours have been fuelled by reports that Pensions Minister Torsten Bell, who in 2019 had stated that the tax free lump sum should be limited to £40,000, had been appointed as a key aid for the Chancellor ahead of the budget. However, while a change is of course possible, it is important to note that:

- When tax free cash has been reduced before (by reductions to the then Lifetime Allowance), protections (such as Fixed Protection 2012, 2014 and 2016) were put in place to ensure individuals who had already built up pension savings were not disadvantaged.

- The current Labour government previously tried to reinstate the Lifetime Allowance, which the previous Conservative government had scrapped. However, the government abandoned these plans when they realised it was unworkable to exclude Doctors (who had been retiring due to the high tax rates they were subjected to through a combination of the lifetime allowance and the annual allowance) from the Lifetime Allowance tax charge. Having now finalised legislation around the Lump Sum Allowance, a further change affecting Doctors’ pensions could prove very unpopular.

- Pension legislation notoriously takes months or years to finalise, as was the case with the recent Lump Sum Allowance (LSA) changes and as is currently the case with the legislation which will bring pensions into scope for inheritance tax from April 2027. This could indicate any reduction may come into force at a given date in future, rather than with immediate effect.

To make a change ‘overnight’ would be administratively difficult for pension providers.

Capital Gains Tax (CGT)

Despite the administrative issues associated with implementing an overnight change as outlined above, one change that was brought in with immediate effect in last year’s budget was an increase in the main rate of capital gains tax from 10% to 18% for basic rate tax payers and 20% to 24% for higher rate tax payers. These increases weren’t as substantial as some thought they would be, so there is the possibility of further increases. However, there are question marks over how much revenue such an increase would actually raise given individuals can simply choose to stop selling their assets.

Inheritance Tax (IHT)

This is the area that saw arguably the biggest changes in the 2024 budget with:

- Pensions brought into scope for inheritance tax purposes from April 2027

- Business Relief and Agricultural Relief limited to £1m per person and 50% of the full rate thereafter

- AIM shares Inheritance Tax Relief limited to 50% of the full rate

The government may see the estimated £5.5 trillion of wealth that is expected to be passed down from ‘Baby Boomers’ over the next two decades (known as the ‘Great Wealth Transfer’) as a target for additional taxation. This could include a tax on gifting (currently gifting to individuals is unlimited if the donor lives 7 years from the date of the gift) or a reduction in the tax free allowances available on death (for example the removal of the Residence Nil Rate Band – RNRB). For this reason, those considering making a gift in the not too distant future could consider making the gift before the budget, though only if the implications of this on their overall financial situation are fully understood.

ISAs

There are rumours that there will be a reduction to the Cash ISA allowance. However, a cut to the Stocks and Shares ISA allowance is perhaps less likely given Reeves spoke positively about Stocks and Shares ISAs in her Mansion House speech in July.

Salary Sacrifice

This is the ability for employees’ pension contributions to be paid directly into their workplace pensions, reducing both employer and employee national insurance contributions. Limiting or removing the ability to do this could raise significant revenue for the government without them needing to renege on their manifesto commitment not to increase tax on working people (income tax, national insurance or VAT).

Other rumours

Other recent rumours include:

- An increase in tax with a corresponding reduction in National Insurance. This could in theory raise revenue without raising tax on ‘working people’, with landlords and pensioners instead footing the bill.

- A further freezing of income tax bandings. Though this is described by many as a stealth tax as it means more and more individuals will move into higher tax bandings over time, these have been frozen since 2021/22 until 2028 and an extension of this freeze to 2029/30 could raise an estimated £7bn p.a.

- A tax on Limited Liability Partnerships (LLPs) favoured by Solicitors, Accountants and Doctors, as such arrangements allow individuals to be self-employed and not subject to employer’s national insurance contributions.

- A windfall tax on banks, though the Chief Executive of Lloyds Banking Group Chalie Nunn argued this would impact banks’ ability to lend.

An increase in gambling taxes, though the Chairman of Betfred Fred Done has stated all its shops on UK high streets could close if the rumoured changes were implemented.

When does the Autumn budget take effect?

Though the budget will take place on 26th November 2025, most changes are expecting to come into effect from the next tax year on 6 April 2026 and beyond.

What can you do to protect your wealth?

In an environment where taxes are increasing, it is becoming more and more important to:

Utilise the various tax allowances that are available to you and your family, for example:

- Your ISA allowances

- Your pension contribution allowances

- Your capital gains tax, savings and dividend allowances

- Your personal income tax allowance.

Have a plan in place with diversified sources of income and investments. This way you can adapt your plan as a result of any changes in the budget.

In summary, it is clear that the state of public finances mean taxes will need to increase in the upcoming budget and Labour’s manifesto commitment not to increase tax on ‘people working’ has led to mounting speculation that changes will be made to a number of different areas. These headlines are usually followed by a quote from a leader within the industry in question stating how the tax increase would be devastating for that industry and how the government should look elsewhere. As Private Eye’s headline from September rightly stated: ‘Raise taxes for other people’, agrees everyone, so some difficult decisions will need to be made.

To consider the potential impact of the budget on your overall financial situation, please get in touch or contact your TPO Adviser.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning or tax advice.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age).

The value of your investments (any income derived from them) can go down as well as up, so you could get back less than you invested. This could also have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.

Autumn Budget 2025: your go to guide

When is the Autumn Budget?

As we head into the final months of the year, attention is turning towards one of the key economic milestones, the Autumn Budget. Scheduled for 26th November this year, the Budget is an essential part of the financial calendar, not just for policymakers and economists, but for households, businesses and advisers to understand the direction of travel.

Arrange your free initial consultation

While every Budget matters, the stakes feel especially high this year. The economic outlook remains uncertain, government borrowing costs have rocketed, and a growing number of taxpayers are already feeling the pain from continued frozen allowances and the changes announced in last year's Budget.

So, what exactly is the Autumn Budget for, and why is it such an important event?

Understanding the Budget’s role

The Autumn Budget is the government’s main opportunity each year to set out its plans for taxation, public spending and economic strategy. It’s when the Chancellor outlines how the government will raise and allocate money in the year ahead, usually supported by economic forecasts from the Office for Budget Responsibility (OBR).

These forecasts cover everything from inflation and interest rates to borrowing, debt levels, and projected economic growth, all of which shape the decisions being made in the Budget itself.

The Autumn Budget is often accompanied by a Spending Review, which sets departmental budgets for the medium term, though not necessarily every year. In contrast, the Spring Statement, usually delivered in March, tends to be lighter, more of an economic update than a full fiscal event, though it can include policy changes when needed.

In recent years, the Autumn Budget has become the main fiscal moment of the year. The Spring Statement, while still useful, is generally more reflective in tone. Some recent commentary has suggested that the government may be considering a move to just one formal fiscal event per year, but as of now, the current two-event framework remains firmly in place.

Raising revenue by stealth

One of the most effective tools for raising revenue in recent times has been the simple decision to freeze tax thresholds and allowances, rather than increase them in line with inflation. This is often referred to as “fiscal drag” or stealth tax.

The concept is straightforward. When income tax thresholds stay fixed, but wages rise, even modestly, more people are pulled into higher tax bands. Likewise, with allowances reduced for capital gains or frozen for inheritance tax, for example, more estates and investments gains become taxable over time.

These quiet changes can bring in billions in additional revenue without altering headline tax rates, and they’ve become a central part of the government’s fiscal approach. The freeze on the personal allowance and higher-rate income tax threshold began in 2021 and is currently extended to at least 2028, with rumours this could be further extended in the coming Budget.

For financial planning, this makes the Autumn Budget a critical event. It’s not just about new taxes or reliefs being introduced or withdrawn; it’s about understanding how existing policies evolve by, some cases, staying exactly the same.

How will the Autumn Budget affect me?

With the Autumn Budget fast approaching, attention is turning to what the Chancellor might announce this time around.

While nothing is confirmed, early speculation includes:

- An extension of existing tax band freezes, particularly income tax and inheritance tax thresholds

- Restrictions on pension tax reliefs or changes to contribution limits

- Restrictions on the tax-free cash available from pensions, though it is important to remember when the tax-free lump sum has been reduced before, protections were put in place to ensure individuals who had already built up savings in their pensions were not disadvantaged.

- Property tax reforms, potentially around stamp duty or council tax

- ISA reforms, possible reduction in the Cash ISA allowance

This is purely speculation at this point so it’s advisable not to make rash decisions before knowing exactly what the outcome will be. However, given the current economic environment, including sluggish growth and high debt interest costs, the government has limited room to manoeuvre, so sadly it’s wise to be prepared. Potentially, if there were financial decisions you were planning to make anyway, that could possibly be impacted by the Budget, now could be the time to make them.

How we can help

Whether you're a business owner, investor, retiree or employee, the Autumn Budget can affect you in ways both obvious and subtle. Whether through active policy changes or passive revenue generation via fiscal drag.

We’re following developments closely now and in the run-up to November’s announcement. We’ll be keeping these pages updated with the latest news, including on the day of the Budget with a full run down of all the announcements

In the meantime, if you’re concerned in anyway how the Budget may affect your finances, why not get in touch and see if we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

FAQs

The Autumn Budget is the government’s main opportunity each year to set out its plans for taxation, public spending and economic strategy.

It's scheduled for 26th November of 2025.

Pension tax relief is a government incentive that helps you save more efficiently for retirement by reducing the tax you pay on your pension contributions. When you pay into a pension, some of the money that would have gone to HMRC is instead added to your pension pot.

If you're a basic-rate taxpayer (20%), contributing £80 means the government tops it up with £20, so £100 goes into your pension. Higher-rate taxpayers (40%) and additional-rate taxpayers (45%) can claim back even more through their self-assessment tax return, reducing the real cost of saving even further. It’s one of the most tax-efficient ways to build your retirement fund.

A Cash Individual Savings Account (ISA) is a type of tax-free savings account. There is no tax to pay on any interest earned, making them especially attractive for tax payers who are already fully utilising their Personal Savings Allowance (PSA) – and in particular high and additional rate tax payers.

You can contribute up to £20,000 per tax year into ISAs. You can spread your contributions across different types of ISAs, or contribute all of your annual allowance into one type, such as a Cash ISA. Since the start of the 2024/25 tax year, you can now subscribe to more than one of each ISA type per tax year.

AI gold rush to continue as September returns continue to shine

Global equities moved higher in September with most major indices making positive returns, with US equities leading the way returning 4% (in sterling terms). This meant it was another strong quarter for risk assets as market enthusiasm around AI gained momentum, trade tensions were eased and we saw the Federal Reserve cut rates for the first time since December 2024.

Figure 1. Regional equity returns (Source: Pacific Asset Management, September 2025)

Arrange your free initial consultation

US Tech - AI sentiment continues to shine brightly

Much has been made about the AI theme in recent weeks as investors contemplate whether we are entering a golden age of heightened productivity or whether the Nvidia circular economy, in which Nvidia invests or lends money to other companies who in turn use Nvidia Graphics Processing Unit (GPU) may be creating an inflated perception of the demand for AI.

This creates an innovators dilemma for Corporate America: if they don’t embrace new technology they risk losing their competitive edge…..think Blockbuster video dismissing ‘streaming’ as being too expensive and instead continuing to focus on their bricks and mortar model back in the 2000s.

The fear of being left behind has seen management teams at US technology companies adopt a cavalier approach with Mark Zuckerberg (CEO of Meta) expressing that misspending a couple of hundred of billion in the US would be ‘unfortunate’ but ‘the risk is higher on the other side’. Similar comments have been made by Larry Ellison of Oracle and Sundar Pichai of Alphabet.

The ability to invest billions of dollars in projects with uncertain returns has been made possible only by the exceptional financial strength of leading US technology companies. Simply put, few firms have the scale or resilience to take such risks. In today’s market - where investors are rewarding companies viewed as ‘enablers’ and ‘beneficiaries’ of the emerging AI economy - this dynamic has led to a renewed period of narrow leadership, with a small group of companies driving the majority of returns.

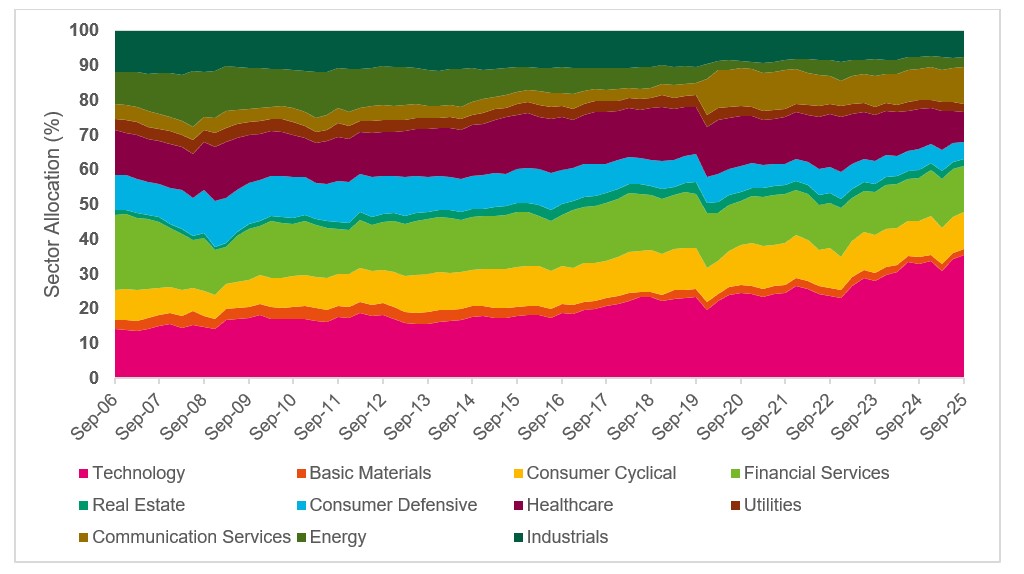

This can be seen in the returns of US Technology companies. After a challenging start to the year they’ve returned over 30% since April compared to the 14% return of the broader market. Meanwhile technology companies as a share of the US equity market have more than doubled to 35% from 15% in September 2006.  Figure 2. Returns of US Mega Cap companies (Source: Pacific Asset Management, September 2025)

Figure 2. Returns of US Mega Cap companies (Source: Pacific Asset Management, September 2025) Figure 3. US Equity Market: Sector composition (Source: Pacific Asset Management, September 2025)

Figure 3. US Equity Market: Sector composition (Source: Pacific Asset Management, September 2025)

Are we entering ‘financial bubble’ territory?

This combination of enthusiasm, unprecedented levels of spending and market moves have raised the inevitable question of valuations and whether we are in a ‘financial bubble’. The challenge lies in that bubbles in markets are only known after the fact - one person’s richly valued stock is another’s growth company of the future.

What is worth noting, however, is that there are several ways to gain exposure to the AI theme beyond simply buying US technology companies. Chinese technology firms, for instance, which trade at significantly lower valuations than their US counterparts, rose 12.6% last month. Meanwhile, sectors such as clean energy - which will form critical infrastructure in an AI-driven world - could also present attractive opportunities for investors.

This challenges the convention that the US is the only game in town as the rally in technology companies outside of the US has supported a broader rally in emerging market equities with strong returns seen in China, Taiwan and South Korea. This combined with a weakening dollar and emerging market economies having lower levels of debt than their western peers - the average debt-to-GDP ratio of Emerging Markets (EM) economies is 75%, while for Developed Markets (DM) economies it is 110% - means the outlook continues to look positive.

Gold looks polished as safe haven prices soar

Another notable development in markets is the continued rally in gold. While the surge in AI-related stocks might suggest unbridled investor optimism, the historic safe-haven asset has also been on the rise. The price of gold reached $4,000 per troy ounce briefly, as investors sought diversification amid concerns over the fiscal profligacy of Western governments, heightened political instability, and a weaker US dollar. Meanwhile, gold mining companies gained 21% over the same period, benefiting not only from higher gold prices but also from a marked improvement in corporate balance sheets across the sector.

This highlights the importance of not only being regionally diversified and looking beyond the US but also expanding into asset classes beyond traditional equities and bonds - such as real assets and alternatives. While it’s impossible to know with certainty when a market bubble might form or burst, investors should always prepare prudently and take a diversified approach to managing their investments.

If you have any questions or concerns about your investments or your future plans, don’t hesitate to get in touch with your TPO Adviser or contact us centrally through our website.

Arrange your free initial consultation

This information in this article is correct as at 10/10/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.