Skip to main content

Skip to main content

How the 'painful' Budget might damage your finances?

What does Rachel Reeves’ first budget have in store for your finances, and what action should you take now to protect against the possible changes?

When Keir Starmer stood in the garden of Downing Street on 27 August, he spoke of ‘Fixing the Foundations’ of the country and of a ‘£22 billion black hole in public finances’. This has led commentators to conclude that if tax rises weren’t planned in Rachel Reeves’ first budget before, they certainly will be now.

When is the Autumn Budget?

The Autumn Budget will take place on 30th October 2024.

Arrange your free initial consultation

What is likely to be in the Autumn Budget?

When Labour ran for election, they ruled out raising taxes on ‘working people’ and specifically pledged not to increase Income Tax, National Insurance, VAT or Corporation Tax. This potentially limits the taxes they can look at (though we would expect Income Tax thresholds to remain frozen until 2028 as announced by the previous government) and we have summarised our views on these various taxes below:

Pensions

Though this would technically be a change to income tax, one possibility for the Government would be to reduce tax relief on pension contributions for high earners. We already have the pensions’ ‘annual allowance’; which limits pension contributions for very high earners, but there is currently the opportunity for those paying higher rates of income tax, but with overall income below the threshold required to have a tapered ‘annual allowance’, to benefit from significant tax relief and the Government could look to limit this.

Another potential change to pensions is reviewing their beneficial tax treatment upon death, where they fall outside the individual’s estate for inheritance tax purposes and can be passed to future generations at attractive rates of tax. Though taking action in the anticipation of potential future legislation changes would be inadvisable, if changes to pension death benefits are announced in the budget, financial plans will need to be reassessed.

Finally, the 25% tax free lump sum available from pensions has been talked about as an ‘at risk’ benefit for years, but it would certainly be viewed as unfair if this was targeted now, given that people have been saving towards retirement expecting to benefit from this. Additionally, changes to the ‘Lump Sum Allowance’ have only just come into force in the current tax year and the Government has already said it will not be reintroducing the Pensions’ Lifetime Allowance, so they may be reluctant to tamper with this area further.

Capital Gains Tax (CGT)

With capital gains above the £3,000 annual exemption taxed at just 10% for basic rate tax payers and 20% for higher rate tax payers (higher rates apply for second property sales), there are rumours that the Government will review CGT rates.

However, HMRC’s own projections indicate equalising capital gains tax and income tax rates could actually reduce the Government’s overall tax take, given this would discourage individuals from selling assets (and crystallising gains) so they may instead decide to retain them.

Additionally, it should be noted that cost prices for capital gains tax purposes are currently rebased on death (meaning gains essentially die with the individual) and if this was changed, financial plans would need to be revisited.

Inheritance Tax (IHT)

With the UK inheritance tax rate currently 40%, it is somewhat surprising that the tax only raises c. £7bn p.a. (of a total tax take of c. £1trillion in 23/24). The reasons for this are the various reliefs available, including:

The ability to gift unlimited amounts to individuals with, broadly speaking, no tax consequences if the donor lives seven years following the gift).

The ability for couples to pass up to £1m between them tax free to direct descendants upon death.

The Government could look to limit some of these reliefs and with £1 trillion of wealth expected to change hands in the UK in the 2020s alone, according to the Financial Times, the Government could see this as an area to focus on.

How will the Autumn Budget affect me?

We of course do not know what changes will be announced in the Autumn Budget on 30th October and, crucially, from when they take effect.

So, what can you do to protect your wealth?

This means there may or may not be time to take action following the budget, and while we would discourage taking action on the basis of rumours, there are actions that can be taken before the budget to take advantage of reliefs that are available now but could be at risk post 30 October.

To speak to an Independent Financial Adviser about how the Autumn Budget might affect you and any actions you could consider ahead of the budget, please contact us for a free initial consultation.

Arrange your free initial consultation

The details in this article are for information only and do not constitute individual advice.

The Financial Conduct Authority (FCA) does not regulate estate planning, tax or trust advice.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is not a reliable indicator of future performance.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

Pensions vs Property - which is best?

A popular question often asked by clients is whether they should contribute into a pension or invest in a property portfolio to fund their retirement.

The reality is there are pros and cons for each investment vehicle, so it’s important to look at these along with how returns compare over the last 10 years. Here we break these down so you can better understand which option may be better suited for you. Although we would always recommend speaking to a financial expert before embarking on your decision.

Arrange your free initial consultation

Pension

Advantages

- Personal pension contributions attract income tax relief at your marginal rate. This means for basic-rate taxpayers, a £1 contribution essentially costs you 80p, as 20% tax relief is provided by the Government under the ‘relief at source method’. Your contributions can also help you reclaim certain tax allowances, such as the personal allowance, tax-free childcare, and child benefit entitlement. If you’re a higher rate taxpayer, you can claim an additional 20% or even 25% tax relief for an additional rate taxpayer.

- Employer pension contributions are essentially ‘free money’ as your employer is providing this as an additional benefit in your remuneration package – often if you don’t take up the contributions, they won’t provide an alternative income instead. Business owners can reduce their Corporation Tax liability by making contributions into their own name.

- Any investment growth is free of Income Tax and Capital Gains Tax.

- Usually, 25% of the value can be withdrawn tax-free in retirement.

- Ability to invest in a diversified range of asset classes (cash, fixed interest, shares, property, and other instruments). Further diversification can be achieved by diversifying assets geographically.

- Flexibility to draw an income in retirement through various methods such as a Lifetime Annuity, Fixed-Term Annuity, and Flexi-Access Drawdown.

- If structured appropriately, any remaining funds after your death can sit outside of your estate for Inheritance Tax (IHT) purposes. This can be a tax-efficient way of passing wealth on between different generations.

Disadvantages

- You are unable to access your pension funds until age 55. This will be increased to age 57 from 6 April 2028.

- The value of your pension is subject to investment risk.

- Depending on how much you spend and how long you live for, your pension pot could be exhausted during retirement if not managed appropriately.

- Legislation can be complex, and rules are often changed.

- On-going charges will apply (pension provider/platform, investment related charges and financial adviser fees).

Property

Advantages

- Potential for long-term capital appreciation and an opportunity of outperforming inflation over the long-term.

- Potential for a regular rental income stream. This can provide a consistent cashflow which can be reinvested into property or other assets.

- A diversifying asset as part of an overall investment portfolio, which means that it can provide a hedge against market volatility.

- Property improvements can add to the value and/or increase rental yields.

- Physical asset and you own something tangible.

- 20% tax-credit available on mortgage interest.

Disadvantages

- If capital is required, it can often be a lengthy process to release equity.

- High initial costs (legal fees and stamp duty etc). A surcharge of 3% on top of normal stamp duty rates applies on purchase of an additional property.

- Potential debt if you require a mortgage to fund the purchase.

- Property management. This can be a hassle, stressful, and time consuming. Paying a professional will eat into your rental yield.

- Maintenance – any repairs will need to be carried out swiftly and the costs are funded by you.

- Potential void periods. This can be a tricky situation to find yourself in if you have a buy-to-let mortgage.

- Tax credit on mortgage interest restricted to 20%, even if you are a higher-rate or additional-rate taxpayer.

- Capital Gains Tax will be applied on any profit when sold.

- Included as part of your estate for IHT if held until you pass.

Pension vs Property Performance

A common issue UK property investors face is that the value of their portfolio is influenced by the UK economy and sentiment.

Investing through a pension can be a much simpler way to diversify globally and across different asset classes through a basket of funds. This can help smooth out governmental decisions or country specific issues, and benefit from growth in other economies.

Past performance is not a reliable indicator of future performance.

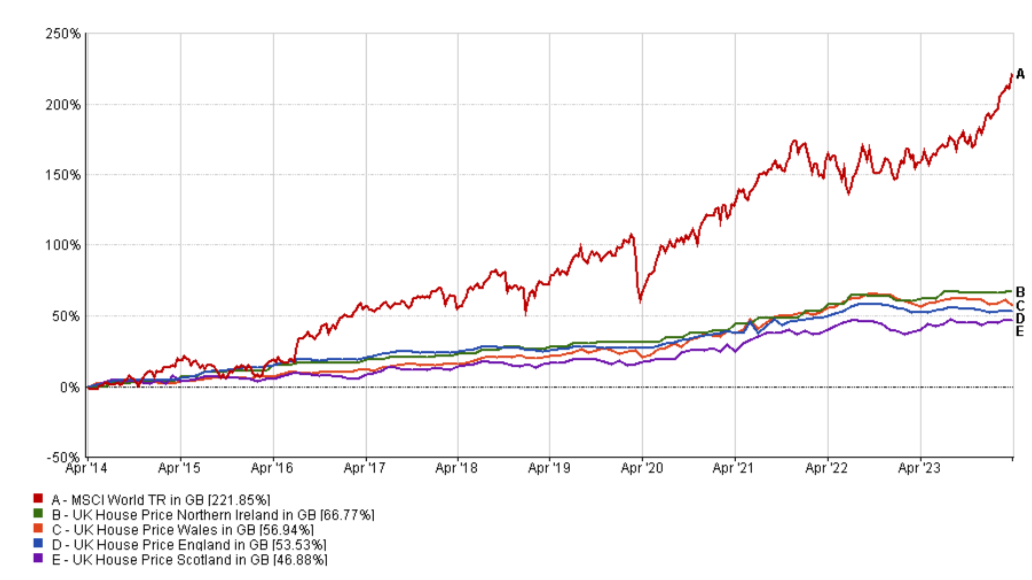

Figure 1: Stock market performance VS Property - Source: FE Analytics, 2024.

The chart above demonstrates the stock market has outperformed UK property over a 10-year period.

The MSCI World Index measures the performance of equity markets across developed countries and has returned 221.85% over this period. UK property returns range between 46.88% - 66.77%.

However, it is important to note these property returns are based on capital appreciation only and do not include any rental incomes received. According to NatWest, as of 2024, the average annual UK rental yield is between 5% and 8% gross.

Should I invest in property or a pension?

Both investment vehicles provide different advantages and disadvantages, as detailed above, and each have a place within a diversified portfolio. As each of our personal circumstances can vary widely, is important to seek advice. An independent financial planner will be able to help you establish which solution is most suitable for your own personal needs. If you’d like to speak to one of our expert advisers, why not get in touch for a free initial consultation, to see if we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate estate planning, tax advice or most types of buy-to-let mortgages.

Your property may be repossessed if you do not keep up repayments on your mortgage.

Investment returns are not guaranteed, and you may get back less than you originally invested.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Our top 5 considerations before moving your pension

Approaching retirement can be a bittersweet thought. On the one hand there is excitement about never having to work again, and on the other, concern as to whether you’ve done enough to have a comfortable retirement. Many individuals suffer from anxiety over the decisions that need to be made relating to life after work, for example:

- "How much do I need to have a good quality of life and meet my expenditure needs?”

- “Is now the right time to retire?”

- “Will my investment returns sustain my expenditure?”

- “How do I even access my pension?”

- “What happens to my pension when I die?

- “Do I have enough in my pensions and other savings?”

Arrange your free initial consultation

And the list goes on. In particular, workplace pensions that have been left to evolve over time with no proper management, may no longer meet the needs of the scheme member i.e. you. So, what are the key factors to consider before moving your pension to another provider, so you can ensure your pension can benefit you and your financial plans? Here's our top 5 considers before moving your pension.

Important Information: This article does not delve into the considerations for Defined Benefit (Final Salary) Pensions – transfers of these schemes are far more complex and require specific financial advice.

Retirement Benefits – How can I access my pension funds at retirement?

Understanding the type of pension you have will determine the options relating to how you can access your pension. Here are the main methods to access your pension for retirement:

Annuity

Use your pension pot to buy an annuity, which provides a guaranteed income for life or a fixed term. This income can either be level or index-linked to keep up with inflation.

Flexi-Access Drawdown (FAD)

This allows you to take your benefits from your pension either a bit at a time or all in one go. This can be beneficial, for example, where you require different amounts from your pension at different times during your retirement, or where you expect your income tax band to change over the course of your retirement.

UFPLS (Uncrystallised Funds Pension Lump Sum)

This option allows you to take a lump sum whereby 25% will be tax-free and 75% will be taxable. Each scheme will have its own rules on if you can take multiple lump sums from your pension or only a single lump sum.

Unfortunately, not all pensions are equal, and therefore some of your pensions may have the full suite of options and some may have limited options, therefore it is important you understand what options are specifically available across each of your pensions. This could determine how you can draw an income in retirement. It’s also important to think about what options are suitable for you as a person, for example, if you are risk-averse and want a secure, fixed income for the rest of your life, annuities are a viable solution. However, if you are unsure how much income you will need in retirement and if you expect your spending requirements to change, one of the flexible options could be more beneficial, or the combination of the two.

Investment Choices – What funds can I invest into?

Pensions offer many different investment options and number of funds that you can invest in. Typically, Self-Invested Personal Pensions (SIPPs) offer the most diverse and wide-ranging fund selection (4,000+). Whereas large workplace pension providers may offer funds that are specific only available to the pension scheme and provider, restricting your choices of investment. You need to decide what your short- and long-term objectives are and whether your pension caters to your risk appetite with the funds available, as this will evolve over time.

Fees & Charges – Will the new pension be more expensive than my existing one?

Before moving your pension, you should always evaluate the costs associated with each scheme. Not all pensions operate the same charges; so, it would be prudent to look at the charges schedule for the new provider and scheme. Typical charges to check for include:

- Initial set-up fees

- Annual Management Charges (AMC) for the investments you might choose

- Platform fees for the service/ongoing administration involved

- Charges for specific transactions – transfer penalties, early withdrawal fees, switching investment funds

- Trading fees for the buying and selling of investments within fund

Death Benefits – Can my loved ones access my pension funds upon my death?

Leaving your pension behind after death is a very common occurrence, given that pensions remain outside of individuals estates for Inheritance Tax purposes. Therefore, you want the beneficiaries of your pension to be able to access your pension in an accessible and tax-efficient manner. The main ways to access pensions on death include:

- Lump sum return of fund – This is the value of the pension on death which is paid as a lump sum to your nominated beneficiary.

- Beneficiary Drawdown – This allows you to pass on your pension to your beneficiary so that they have the option of drawing benefits from it as and when required.

- Annuity – On death, the value of your pension can be used to purchase an annuity from your pension provider. This will provide a secure regular income for your beneficiary.

Pension Guarantees – What benefits could I lose on transfer?

Some pensions come with a guarantee, which can impact the amount of income you receive when you retire. These ‘safeguarded’ benefits might include a guaranteed annuity rate (GAR) or a promised minimum level of income (guaranteed minimum pension). These benefits are valuable in most cases so it’s important to take them into account when assessing your options, given that these guarantees are rarely retained when transferring to another provider. These can be very complex so it’s sensible to seek financial advice on these benefits.

Having the wrong pension scheme for your requirements can be detrimental to your overall retirement plans. Having a financial adviser can help you navigate through the quirks and nuances of pension schemes and help simplify the complexities, to ensure you are appropriately positioned for your long-term needs and objectives. If you would like to learn more about the suitability of your pensions and its suitability for your needs, why not get in touch and speak to one of our experts

Arrange your free initial consultation

The details in this article are for information only and do not constitute individual advice.

The Financial Conduct Authority (FCA) does not regulate estate planning, tax or trust advice.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

29% of retirees' reality falls short due to DIY approach

On the run up to retirement, many over 55s are opting to manage their finances without professional guidance, a decision that carries significant risks. According to research by Canada Life, a staggering 79% of individuals in this age group are navigating their retirement plans independently, without seeking financial advice. This DIY (Do-it-Yourself) approach contributes to nearly 29% of retirees finding their reality falling short of their dreams.

Arrange your free initial consultation

Common pitfalls in planning for retirement:

Many retirees are finding themselves unprepared for the financial realities of retirement.

Factors contributing to this gap between their expectations and reality involve a failure to account for several critical aspects:

- Health issues: The Canada Life study found that 36% of retirees reported experiencing unexpected health issues disrupted their retirement plans.

- Inflation: About 21% of respondents did not factor in inflation, leading to a decline in purchasing power over time

- Unforeseen expenses: Unexpected bills and expenses caught 13% of retirees off guard, indicating a shortfall in financial preparation.

- Underestimating financial needs: A significant 11% of retirees underestimated the amount of money needed for a comfortable retirement.

This study underscores the critical importance of thorough and pragmatic financial planning before retirement. Tom Evans, Managing Director of Retirement at Canada Life, emphasises that through consulting a qualified financial adviser, retirees can address these factors proactively, ensuring more secure and fulfilling retirement.

Hurdles faced during retirement:

While understanding the pitfalls before retirement is essential, navigating the hurdles during retirement—such as managing your expenditure, income strategy, and adapting to legislative changes—requires ongoing attention.

Expenditure:

During retirement your needs will evolve, influenced by factors like inflation, healthcare costs, and lifestyle changes. The Pension and Lifetime Savings Association’s Retirement Living Standards study offers a helpful guide, showing that a couple aiming for a comfortable retirement might need an annual income of around £59,000, while a moderate lifestyle requires about £43,100 per year. Whilst this provides a good benchmark, your spending and goals are unique. As a result, it is essential to identify your specific expenditure needs and assess if they are sustainable throughout your retirement.

Income:

Strategising how to draw upon your assets to support your retirement is equally important. Ensuring that your assets work hard for you and that your funds are used in a tax-efficient manner is crucial. Retirees may have multiple income sources, across cash, pensions, ISAs, bonds and rental properties. Effective planning not only ensures tax efficiency but also can helps maintain or increase income potential during retirement. Seeking advice on how to take an income from your pensions and other assets is critical, as planning for the next two or three decades leaves little room for mistakes.

Legislative Changes:

Recent and potential future changes to pension legislation, can profoundly affect retirement planning. Staying informed about these updates is crucial, however navigating these changes within the complex retirement planning landscape can be challenging. In these cases, working with an adviser can be hugely beneficial to provide guidance on how to adjust your plans to mitigate any negative impacts from legislative shifts and take advantage of any new opportunities that arise.

A recent example of a significant change is the removal of the lifetime allowance. This legislation introduced two new allowances that affect the amount of tax-free lump sums or tax-free death benefits available from a pension. With the new Labour Government expected to release a budget this Autumn, it will be crucial to consider how these changes impact your retirement planning and to strategically respond accordingly.

A successful retirement plan isn't just about reaching a financial goal before you retire—it's about maintaining that security and adapting to changes throughout your retirement years. Regularly reviewing your expenditure, income strategies, and staying informed about legislative changes ensures that your plan remains robust and effective.

Value of Advice:

Financial advice is of course not free so while many can see the benefits of receiving advice, the cost associated may be a driver behind why people are choosing to DIY (Do It Yourself) their plans. According to a report by the International Longevity Centre - ILC, individuals who receive professional financial advice are, on average over a decade, nearly £48,000 better off in pensions and financial assets than those who do not. The study showed that the combined benefits of financial advice over a ten-year period are approximately 2,400% greater than the initial cost of the advice. This significant return on initial cost underscores the value of seeking professional guidance.

In summary, retirement involves many challenges, and the importance of robust financial planning cannot be overstated. Opting for professional guidance rather than navigating these waters alone could significantly improve your financial well-being during retirement and equip you with strategy to manage potential pitfalls effectively. Working with an adviser can ensure that as you transition away from work, you can feel confident in your future, providing you with peace of mind for a comfortable and fulfilling retirement.

If you’re thinking about your own future, we’re currently offering anyone with £100,000 or more in savings, pensions or investment a cash flow review worth £500. Why not get in a touch for a free initial consultation to see how we might help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

The value of your investments can go down as well as up, so you could get back less than you invested.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

Is the minimum pension contribution about to rise?

The Pensions and Lifetime Savings Association, representing UK pension schemes, has called on the Government to increase the minimum contribution level after concerns around the number of people not prepared for retirement.

Currently the level is set to 8% of pensionable earnings, defined as a worker's basic salary excluding bonuses, commission, and overtime. Of this, employers are required to contribute at least 3%, while employees contribute 5%. It was proposed to increase this to 12% of total salary over the next decade, with employees and employers each contributing an equal share.

The annual retirement report, published this week by Scottish Widows, reveals that the percentage of people not on track for even a minimum retirement lifestyle has risen from 35% to 38% during the last year, equating to an extra 1.2 million people.

The Proposals

The proposal to raise the minimum contribution level from 8% to 12% with a 50/50 split is intended to enhance the retirement savings of over 15 million private sector employees. The proposals also include measures to help workers track their pensions when they change jobs, introduce value for money tests for pension schemes and include initiatives such as helping employees keep track of their pensions when they move jobs.

Industry professionals highlighted the urgency of increasing minimum contributions, which currently stand at 8% of pensionable salary, of which companies must pay at least 3% and employees 5%.

The Government announced that its pension bill measures could add an extra £11,000 to the pension pot of an average worker, although no supporting analysis was provided to explain how this figure was calculated. The bill includes an initiative to ensure schemes offer “value for money,” with underperforming funds being removed from the market.

The Government stated that these measures would “enable security in retirement” while allowing pension schemes to invest in a broader range of assets, which should, in turn, help to promote economic growth.

Currently, most people are left on their own to navigate the complex retirement income market. If you’re interested in how to manage your pension contributions to ensure the best possible wealth protection for you or your family, we can help. Give us a call on 0333 323 9065 or book a free non-committal initial consultation with a member of our team to find out more.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

What will Starmer’s Labour Government mean for your finances?

As expected, Keir Starmer’s Labour party have won the 2024 General Election with a landslide victory, but what could this mean for your finances and when will any changes be implemented?

Arrange your free initial consultation

Taxation

In terms of taxation, the introduction of VAT on Private School fees is expected, though there will likely be complexities around the implementation of this change. Beyond this, the Labour Party have said they will not increase taxes on ‘working people’, indicating income tax, national insurance and VAT are unlikely to increase in the short term, though it is understood Labour will retain the Conservative Party’s plans to freeze income tax thresholds until at least 2028. However, there has been no such pledges in respect of capital gains tax or inheritance tax, so these are areas Starmer’s new government may look at.

Pensions

Regarding pensions, the subject of reintroducing the Lifetime Allowance (LTA) for Pensions has been a hot topic since it was announced in the 2023 Spring Budget that the LTA was to be abolished. At the time, Labour pledged to reintroduce the LTA, but it is difficult to see how this could be implemented in practical terms given the abolition has now taken place and additionally, Labour are keen not to disincentivise Doctors who have reached the limit from working. Labour have now indicated they will in fact not reintroduce the LTA, but they have pledged to conduct a detailed review of pensions, so it will be interesting to see the outcome of this review, specifically whether there will be any changes to tax relief on pension contributions, the taxation of pension death benefits or the 25% tax free lump sum.

When might changes be implemented?

In terms of a timeframe for any changes to be implemented, Labour have committed to including a forecast from the Office for Budget Responsibility (OBR) in their first budget, as they look to distance themselves from the approach taken by Liz Truss, who famously did not utilise the OBR’s analysis ahead of her disastrous “mini-budget” in September 2022. Given the OBR require 10 weeks’ notice to provide their forecast, the Budget is therefore unlikely to be delivered before mid-September 2024.

If you would like to discuss the implications of the new government for your finances, please get in touch to arrange a free consultation with one of our Independent Financial Advisers.

Arrange your free initial consultation

The opinions shared in this article are solely those of the individual and they do not necessarily reflect those of The Private Office.

Please note: This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions. The Financial Conduct Authority (FCA) does not regulate tax advice. Investment returns are not guaranteed, and you may get back less than you originally invested.

Navigating Self-Employed Tax Traps

Being self-employed offers the unique opportunity to ‘be your own boss’, but this comes with its own responsibilities and challenges.

Alongside the operational implications of working for yourself or running a business, navigating the world of taxes as a self-employed individual can be complex, and if you don’t manage your tax affairs correctly, this could result in costly penalties. Being on top of your tax planning and being aware of and navigating around potential pitfalls whilst making use of valuable allowances is therefore critical for any self-employed person.

Arrange your free initial consultation

Income Tax and the 60% ‘trap’

A benefit of being self-employed is being able to claim allowable expenses against your taxable income, which can significantly reduce your tax bill. This can range from office costs such as rent, to business-related travel expenses, and professional fees such as accountancy fees.

It is however important to be aware of tax traps that you may fall into, such as the 60% income tax ‘trap’. This is a band of earnings between £100,000 and £125,140 where you will effectively experience an income tax rate of 60%. This is because for every £2 you earn over £100,000 per annum, alongside being subject to income tax at 40%, you lose £1 worth of your £12,570 tax-free Personal Allowance. Within this banding of earnings, you will also be subject to national insurance contributions of 2%, given a combined rate of income tax and national insurance contributions of 62%. Known as the 62% tax trap.

One of the main levers you can pull to help reduce your tax liability and help you avoid this trap is increasing your pension contributions, as this reduces your ‘adjusted net income’. Pension contributions can effectively receive tax relief of 60% within this band of earnings. As an example, for a higher rate taxpayer earning £110,000, a £10,000 gross pension contribution will effectively only ‘cost’ £4,000, once all income tax relief (totalling £6,000) is received.

National insurance contributions and your State Pension entitlement

For the employed, as the case with income tax, national insurance contributions are typically taken directly from gross earnings, hence there is no need to calculate your national insurance liability due each tax year. For the self-employed, it is critical to make sure you calculate your correct national insurance liability, otherwise you may end up paying too little or too much national insurance contributions.

You must tell HMRC when you become self-employed, as most people pay any required class of national insurance contributions through a self-assessment tax return. There are two types of national insurance contributions you may have to make as a self-employed individual, which will depend on your profits for the tax year.

If your profits are £6,725 or more a year:

- Class 2 national insurance contributions are treated as having been paid, hence do not have to be paid.

- If your profits are more than £12,570, you must pay class 4 contributions. For the 2024/25 tax year, you’ll pay 6% on profits between £12,570 and £50,270, and 2% on profits over £50,270.

If your profits are less than £6,725 a year:

- You do not have to pay anything, but you can pay voluntary class 2 contributions.

- The class 2 rate for the 2024/25 is £3.45 a week.

One potential pitfall in planning is that if your profits are below £6,725 a year, and you do not make voluntary class 2 contributions, you may not receive a ‘qualifying year’ towards your national insurance record. In more challenging lower profits years, it therefore may be wise to pay voluntary contributions (totalling £179.40 a year currently) in order to access a potentially higher state pension entitlement along with other state benefits.

You may also have ‘gaps’ in your national insurance record for previous years, where profits were below the threshold for receiving a qualifying year’s credit. This could result in a reduced State Pension. However, you may be able to pay voluntary contributions to plug any gaps. It is therefore worthwhile checking your national insurance record, which can be done online on the government gateway, to see if you have any gaps, or how much it will cost to pay voluntary contributions and if you’ll benefit from paying voluntary contributions.

Have you built up enough wealth in a private pension?

Employers are obliged to automatically enrol their employees into a workplace pension plan, but if you’re self-employed then it’s up to you to set up a private pension plan. Some self-employed people say their business is their pension and can be sold when they want to retire. However, this can be a high-risk strategy, and if your business goes under, not only have you lost your job, but also your potential pension fund.

It is therefore important to be diligent with pension saving if you are self-employed. One strategy may be to allocate a proportion of your income, or a fixed amount each month, to a private pension plan. This way any pension saving may be ‘automatic’ and builds good saving discipline.

This approach can be combined with lump sum pension contributions. This type of planning is often undertaken towards the end of a tax year when there is a better understanding of earnings for the year, which may be more appropriate for those with more variable earnings year on year.

Each year, as a self-employed individual, you will have an ‘annual allowance’ for pension contributions that are eligible for tax relief, as is the case for personal pensions in general. The annual allowance is currently set at £60,000 per tax year, although your tax relievable pension contributions will be restricted to 100% of your profits if your profits are lower than £60,000 in a tax year.

If your earnings are over £260,000 as a self-employed person who is therefore not receiving employer pension contributions, your annual allowance may be ‘tapered’ down to as low as £10,000 per tax year.

It can also be possible to make use of any unused annual allowance from the previous three tax years, known as ‘carry forward

Registering for VAT

You must register for VAT with HMRC if your annual turnover in a year exceeds £90,000, or if you expect your annual turnover to go over £90,000 in the next 30 days. This threshold was recently increased from £85,000.

The registration timeline is within 30 days from the end of the month in which you exceed the threshold. For example, if total business sales in the previous 12 months exceed £90,000 on 14th March, you will have until 30th April to register.

Should I set up a limited company?

Setting up a limited company means your company’s finances are independent from your own. If you choose to be a sole trader, you only need to register with HMRC and complete a personal self-assessment tax return. If you are setting up a limited company, you’ll need to register the business with Companies House and with HMRC for tax purposes.

With a limited company, as the business is a distinct separate legal entity, the company’s finances are separate from the shareholders’ or directors’ personal finances, so you are only responsible for the amount of money you put into the business. As a sole trader, you are responsible for both personal and business debts, so personal assets such as your home could be at risk if something goes wrong.

Forming a limited company does come with incorporation costs, along with additional responsibilities such as filing annual accounts and management responsibilities. Being a sole trader comes with few formalities in comparison.

A sole trader is typically a more straightforward approach and involves limited paperwork and obligations, but you might be at a disadvantage when it comes to benefiting from tax reliefs and being more tax efficient. The business structure that is the best option for you ultimately will depend on your personal circumstances, with both advantages and disadvantages to each approach.

It's all about the planning

Whether you are a sole trader or run a limited company, it is crucial to work closely with professional advisers to ensure that you are mitigating tax as far as possible, as well as making use of valuable tax allowances. Alongside helping put in place a suitable financial planning approach, we can make suitable introductions to accountants and solicitors where appropriate.

As a business owner you may be working tirelessly to create and grow a legacy to give you financial freedom. Our expert business financial advisers can help you accomplish these goals and work with you to protect the legacy you’ve worked hard to achieve.

Please do therefore get in touch for a free initial consultation if you have any concerns surrounding tax planning as a business owner. We’re offering anyone with £100,000 or more in pensions, investments or savings a free cash flow review worth £500.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax or trust advice.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

Tax planning for high earners

After years of frozen thresholds, reduced allowances, and quiet but powerful fiscal drag, the most recent Budget offered little respite for those deemed ‘High Earners’ which used to be those earning just over £50,000. In fact, for many, it marked a new phase in what’s becoming a stealthy but sustained squeeze on take-home pay.

While many higher earners accept the principle of paying their fair share, there's a growing sense that we’ve hit a tipping point. Tax is no longer just a cost of success; it’s fast becoming a sticking point to long-term financial growth. With more and more people drifting into higher tax bands, the cumulative impact is starting to bite.

That’s why tax planning is no longer just prudent, it’s essential. If you’re a ‘high earner’ whether that be on a little over £50,000 or well into six figures, navigating the tax system could mean the difference between merely treading water and building real, lasting wealth. From reclaiming lost allowances to making strategic use of pensions, charitable giving, and relief schemes, the opportunities are still there, you just need to know where to look.

Arrange your free initial consultation

Tax can have a big impact on your ability to preserve the value of your savings and investments in retirement. As such, one of the main focuses when advising clients, is creating a plan that helps them achieve their objectives in the most tax efficient manner. There are several ways to reduce the tax you pay on your annual income, especially if you’re in the higher or additional rate tax bracket.

What are the main taxes?

Income tax

Income tax is a tax imposed directly on your personal income. In simple terms, it is paid at rates between 0% and 45% dependent on which of the income tax brackets you fall into.

Once your earnings exceed your personal allowance, you are required to pay tax on the following sources of income:

- Income from employment

- Income from pension

- Interest on savings

- Property rental income

- Employment benefits

- Income from a trust

As of the 2025/26 tax year:

- The personal allowance remains at £12,570

- Basic rate tax (20%) applies to income from £12,571 to £50,270

- Higher rate tax (40%) applies from £50,271 to £125,140

- Additional rate tax (45%) applies from £125,141+

These thresholds are now frozen until 2031, further extending the impact of fiscal drag.

The tax rates on dividends are lower but again will increase by 2 percentage points for basic and higher rate taxpayers from 6 April 2026.

Furthermore, an additional 2% tax will be introduced from 6 April 2027 on savings interest and property rental income, increasing the tax burden from these sources. If you're a Scottish taxpayer, note that income tax bands differ from the rest of the UK. It's essential to consider regional differences when planning.

Capital Gains Tax

Capital Gains Tax (CGT) is paid on the profit made when you dispose of certain assets, such as shares, second homes, or other investments held outside of a tax efficient wrapper.

Update for 2025/26:

- The CGT annual exemption is £3,000, much lower than £12,300 in 2022/23

Tax is charged on gains above this allowance at: - 18% (basic rate) or 24% (higher rate) for individuals (not including carried interest gains) on financial assets and property depending on the tax band the proportion of the gain falls within

- With the CGT allowance significantly reducing in recent years, proper use of tax wrappers (like ISAs and pensions) is crucial.

Inheritance Tax

Inheritance Tax (IHT) is a tax on the value of an estate upon death or on certain gifts made during your lifetime.

- The nil-rate band remains at £325,000

- The residence nil-rate band offers an additional £175,000 if passing a home to direct descendants

- The standard rate of IHT is 40%, or 36% if at least 10% of the net estate is left to charity

From April 2027, pensions will form part of a person's estate for inheritance tax purposes. Currently, pensions are generally outside of IHT calculations, but this will change for most type of pensions. If you're relying on your pension as an IHT-efficient tool, it's important to review your estate planning and options now.

How to reduce taxable income as a high earner

Reducing your taxable income can be one of the most effective ways to lower your overall tax bill. For high earners, this might mean utilising pension contributions, salary sacrifice, or charitable giving to stay within lower tax bands or reclaim lost allowances.

For example, reducing your adjusted net income to below £100,000 can help you reclaim your personal allowance, while staying below £50,270 may mean avoiding higher rate tax entirely. Strategic use of deductions and allowances can significantly reduce the income you are taxed on, without reducing your overall wealth.

Why is tax planning important?

Tax planning involves minimising tax liabilities by utilising allowances, exemptions, and tax reducers to lowerthe tax you pay, so it should be an essential part of an individual’s financial plan.

Effective tax planning can be instrumental in saving individuals money, maximising wealth and achieving your financial goals. By proactively managing finances and optimising tax planning opportunities, individuals can ensure they are on track to meet their objectives.

What is higher rate tax?

In the UK, we do not get taxed on the first £12,570 we earn from our salary, bonuses, rental income, pensions, and other various income types - this is called our Personal Allowance. Income exceeding the Personal Allowance is then subject to income tax. This is banded so:

- Your earnings between £12,570 and £50,270 are currently taxed at the basic rate of 20%.

- Earnings from £50,271 and £125,140 at the higher rate of 40%.

- Anything above £125,140 is taxed at an additional rate of 45%.

The personal allowance and the higher rate threshold (£50,270) have been frozen until 2031 following an announcement by the Chancellor in the Autumn Statement 2025.

Therefore, more people are and will continue to be pulled into paying 40%-45% tax on their earnings, so it is increasingly important we utilise the tax planning opportunities available to us to minimise the impact of the frozen tax allowances and tax bands.

High earners cutting pay: Should you consider it?

Some high earners are now deliberately cutting their pay or exchanging salary for pension contributions or other benefits as a strategic way to reduce tax liability. This is often done through salary sacrifice or personal pension contributions, which can lower your taxable income, increase pension savings, and in some cases reclaim lost allowances such as the personal allowance or avoid additional tax charges like the High-Income Child Benefit Charge.

Reducing pay might not be a step back, but a smarter move towards long-term financial efficiency. It’s worth speaking to a financial adviser before making any changes, to ensure it aligns with your wider goals and that you aren’t giving up valuable benefits or protections.

Ways to reduce your income tax bill

There are a few ways in which you can reduce your income tax bill. Broadly, they are as follows:

Contribute to your pension

Contributions to a pension are usually made from taxed money unless in a 'net pay' scheme' or using 'salary sacrifice' . However, when you pay in, you will pay the “net” amount (80% for a basic rate taxpayer). The government will then make up the tax paid on the amount contributed.

For example, if you’re a basic rate taxpayer you can receive tax relief of 20% from the government, therefore it costs you 80p to make a £1 pension contribution. For a higher rate taxpayer the cost is only 60p.

Contribute to your pension via salary sacrifice

You can ask your employer to enter into a salary sacrifice contribution arrangement to your pension, which will reduce the amount of money subjected to the highest rate of income tax (or various rates depending on the tax bands the income falls into after the sacrifice), along with also providing valuable National Insurance savings. This can become quite complicated, and more details can be found on the government website.

A notable additional benefit of salary sacrifice arrangements is that depending on your employer, they may pay the National Insurance Contributions savings they make from the forgone salary into your pension.

Do take care though as the government is planning to make changes to how salary sacrifice for pension contributions work from April 2029 by capping the National Insurance (NI) exemption to £2,000 per year.

Make full use of your pension annual allowance

The annual allowance is currently £60,000 and this is the maximum that you can tax efficiently contribute to a pension each tax year, without suffering a tax charge. This rose from £40,000 in the 2023/24 tax year.

If you are not subject to tapering of your annual allowance and you have not utilised your full allowance of £60,000, then you could consider making use of the full allowance from a personal contribution or carrying-forward unused annual allowance from previous years. Please note, however, this can only be done up to a maximum of the three previous tax years, and personal tax-relievable contributions are capped at 100% relevant UK earnings regardless of the amount of unused annual allowance.

Make full use of your ISA annual allowance

Both income and growth within an ISA are free of tax making this one of the best savings wrappers in the UK. You can currently contribute £20,000 per year into a Cash or Stocks and Shares ISA however the Cash ISA allowance will be reducing to £12,000 for under 65s from April 2027.

Up to 60% tax relief available when you invest in a Pension

Investing in your pension pot is an attractive option to increase your savings in a tax efficient way. We actively encourage clients, when suitable, to contribute regular amounts to their pension to not only build up their pension pot but also to benefit from tax efficiencies.

For those earning between £100,000 and £125,140 you could be in the 60% tax trap. But this also presents an opportunity when it comes to saving for retirement. If you have taxable income in this range, you can effectively receive income tax relief of 60% on your pension contributions as this is the marginal rate of tax paid on earnings within this band. This is due to the impact of your personal tax allowance of £12,570 being reduced by £1 for every £2 you earn over £100,000 meaning the allowance is reduced to zero when your income reaches £125,140. A pension contribution within this band of earnings effectively reclaims part, or all, of your personal allowance thus increasing the rate of tax relief to 60%.

How to avoid the High Income Child Benefit Charge

For the 2025/2026 tax year in the UK, Child Benefit rates are £26.05 per week for the eldest or only child and £17.25 per week for any additional children, with these rates increasing to £27.05 and £17.90 respectively from April 2026, based on CPI uprating. Payments are usually every four weeks and eligibility applies for children under 16, or under 20 if in full-time education or training, with higher earners potentially facing the High Income Child Benefit Charge (HICBC).

If you are a couple claiming Child Benefit, where one or both individuals have an income above £60,000 per annum, or someone else claims Child Benefit for a child living with you and they contribute at least an equal amount towards the child’s upkeep, you may have to pay a tax charge. This is known as the ‘High Income Child Benefit Charge’.

The tax charge is calculated through the tax return on any partner whose income is more than £60,000 a year. In the event that both partners have incomes over £60,000, the charge will apply to the partner with the higher income. The tax charge will be one percent of the amount of Child Benefit received for every £200 of excess income, meaning that the Child Benefit is completely removed when income reaches £80,000.

One way you may avoid the tax charge is if a personal pension contribution is made, as the adjusted net income used by HMRC will reduce. If the contribution is enough to reduce this to below £60,000, the High Income Child Benefit tax charge will be avoided.

The benefits of charitable giving

Giving to charity is not only good for the cause receiving your donations but is also beneficial to your annual tax bill. If you keep a record of your donations, you will be entitled to report these on your tax return.

The most common way to donate to a UK registered charity or community amateur sport clubs (CASCs) is through Gift Aid. Gift Aid can only be claimed by UK taxpayers and is effectively the repayment of basic rate tax on the donation. This is not repaid to the donor but is given to the charity as they can claim an additional 25p for every £1 they receive.

If you are a higher (40%) or additional rate (45%) taxpayer, you are able to claim the difference between your tax rate and the basic rate of tax (20%) on your total charitable donation. An example of this is shown below:

If you make a charitable gift of £100, the charity will be able to receive £25 from HMRC to reclaim the basic rate tax. As a higher/additional rate taxpayer, you can then claim a further £25 (higher) or £31.25 (additional) relief back via your self-assessment for the £125 (gross) contribution you originally made. To do this, you must register for gift aid with a ‘Gift Aid Declaration’, keep a record of your gifts and gift no more than four times your total income and capital gains tax payment for the tax year in question. More information can be found here.

And not forgetting, charitable giving is a great way to lower your loved one's inheritance tax bill.

Tax relief schemes and other allowances

An investment into a qualifying Venture Capital Trust (VCT), Enterprise Investment Scheme (EIS) or Seed Enterprise Investment Scheme (SEIS) attracts significant tax benefits. For an EIS or VCT, you can receive 30% income tax relief (reducing to 20% for VCTs from 6 April 2026) on the amount you invest, for SEIS this increases to 50% relief. This 30% or 50% is only achievable if you have paid sufficient tax for the year in question. For example, if you invested £200,000 into a VCT, you would receive £60,000 tax relief if you had an income tax bill of at least £60,000.

These investments were created by the government, as an initiative designed to help small and medium sized companies raise finance to grow, by offering tax benefits to investors. Given the type of companies they invest in, they are classified as to be high-risk investments.

They can be attractive to those who have maximised their other allowances for the tax year and are earning a significant salary which takes them into the higher and additional rate tax band.

But, as higher risk investments they are not suitable for all investors. There is a chance that all of your capital could be at risk and you should not invest into these types of plans without seeking expert advice from a reputable firm of independent advisers such as The Private Office.

|

Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. |

|---|

How we can help

There are a number of steps that can be taken to reduce the amount of income tax you pay, which are especially beneficial if you fall into the higher or additional rate tax bands. These tax efficiencies are built into our financial plans, and we actively help clients maximise their allowances and income so they can achieve their goals throughout their lives. If you would like to find out more about how The Private Office can help you with personalised tax efficient financial plans, please enquire for a free initial consultation with one of our Independent Financial Advisers.

Arrange your free initial consultation

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

The content in this article is for information only and does not constitute individual financial advice.

The value of your investments can go down as well as up, so you could get back less than you invested.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Your eventual income may depend on the size of the fund at retirement, future interest rates and tax legislation.

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.

VCTs are high risk investments and there may be no market for the shares should you wish to dispose of them. You may lose your capital.

Labour drops LTA reintroduction plans

According to a recent report in the Financial Times, The Labour Party will be dropping their previous pledge to reinstate the lifetime allowance on pensions after Chancellor Jeremy Hunt abolished the policy earlier this year.

Labour is due to publish its manifesto on June 13, and it is understood that the reintroduction of the lifetime allowance will not appear in their manifesto as anticipated previously. This u-turn will cost an estimated £800m but is likely to be welcomed by many savers, particularly higher earners with generous defined-benefit schemes.

What was the ‘lifetime allowance’?

Essentially, the lifetime allowance was the total amount of capital you could accumulate in all your pension savings tax efficiently. When it was abolished by chancellor Jeremy Hunt earlier this year, the lifetime allowance stood at £1,073,100. This included any employer contributions or investment returns that your pension had amassed over the course of its life.

If your total pension size exceeded this limit then you would be taxed on the excess amount. The amount you will be taxed depended on how you accessed the funds. If the excess was taken as a lump sum then it would have be taxed at 55% but if you took the excess as an income then you would have only been taxed at 25%. This 25% tax charge was paid in addition to the tax you paid on the income you received.

Reintroduction considerations

Despite Labour’s pledge to reinstate the lifetime allowance, the legislation to reintroduce this has proven to be more complex than anticipated.

Last week, the Institute for Fiscal Studies said reintroducing a reformed LTA would be "sensible" and it laid out several options for how this could happen.

The first would be to simply reinstate it at its previous level, but this would raise several questions, it stated. One option set out by the IFS was to reinstate the lifetime allowance at a higher value alongside a reduction in the amount of pension from which 25 per cent can be taken tax free. Another option could be to reintroduce the lifetime allowance as a cap on contributions to DC pensions and accrued benefits in DB pensions, rather than on the pensions’ estimated value.

Carl Emmerson, deputy director of the IFS and co-author of the piece, said given the current way in which pensions are taxed there is a case for reintroducing a lifetime allowance. This is mainly because many other aspects of the system are overly generous to high earners who get sizeable employer contributions and accumulate big pension pots, he said.

He added: “Rather than a simple knee jerk return to the system of two years ago, a new Labour chancellor would be well advised to implement a comprehensive and lasting reform which could rationalise, simplify and make fairer the current system of pension taxation whilst also raising revenue in the medium term."

“The danger is that a reintroduced lifetime allowance ends up being just another bump in the pensions tax road, and another missed opportunity to rationalise the system with a coherent package of measures.”

Although the Lifetime Allowance has been abolished, it has been replaced with two new allowances, so some complexity remains if you planning to take benefits from your pension funds. At The Private Office we can offer advice and guidance about how to best navigate this often difficult area, particularly if you have already taken benefits from some of your pension funds before the new allowances were introduced. If you want to find out more, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our chartered advisers.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Pensions Dashboard hit by digital delays

A recent report found that the delays in the delivery of the Pensions Dashboards Programme (PDP) were due to a shortage of digital skills and governance issues, according to the national spending watchdog.

The report, produced by the National Audit Office (NAO) after a year-long investigation, found that there were “capacity and capability issues” in the rollout of the programme.

Now almost eight years on from the initial proposition, and still with no official release date set for the public launch of the Pensions Dashboards Programme, the NAO report has detailed a range of delivery problems for the project. So far, an estimated £54 million more of tax-payer’s money has been used to help deal with these unexpected delivery problems, and the figure is only rising as the delays continue.

The Pensions Dashboards Programme

First proposed by the Government back in 2016, the Pensions Dashboards Programme was intended to allow individuals to see their own pensions information – state, workplace and personal – for free in one place online. The programme was also intended to help reunite savers with lost or forgotten pensions, whose combined value totals over £19 billion as of 2023.

With the ability to access information easily it was hoped that the service would increase individuals’ awareness and understanding of their pension information and that it could support people with better planning for their retirement.

What did the NAO report show about the delays?

The report found numerous factors contributing to the delays that cast the organisation and management of the development of the Pensions Dashboard Programme in an unfavourable light.

The report outlined that in 2019, the Department for Work and Pensions delegated responsibility for delivering the programme, or the digital architecture to make Dashboards work, to the Money and Pensions Service (MaPS). However, the DWP did not have assurances at the outset that MaPS had the capability and capacity to deliver a major digital project as the Pensions Dashboards Programme was forecasted to be.

In December 2022, MaPS informed DWP that the PDP’s delivery timetable was no longer viable. A subsequent review carried out by DWP in February 2023 found that multiple factors had contributed to the delivery problems, including a lack of skilled digital resources and ineffective programme governance.

As the delays and issues in development pile up, the cost of the programme, and by extension the cost on the taxpayer, rises in equal measure. The NAO investigation also found that estimated cost of the Pensions Dashboard Programme had risen from £235m in 2020 to £289m in 2023, an increase of 23%.

Gareth Davies, head of the NAO, commented on the findings.

“Delivery delays due to shortfalls in digital capacity and capability have pushed back the final deadline for pension providers and schemes to connect to the Pensions Dashboard Programme by a year, with no date currently set for citizens to benefit.”

With no official date in sight, it is unknown when, if ever, taxpayers will be able to access the Pensions Dashboard Programme that they have been waiting for – and paying for – for over eight years.

If you’d like to discuss your own retirement options why not contact us for a free initial consultation to see how we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.